Robust Testing Of the Allais Paradox By Paired Choices vs. Paired Valuations

Abstract.

McGranaghan, Nielsen, O’Donoghue, Somerville, and Sprenger [2024] argue that standard paired choice tests for the common ratio effect are structurally biased when choice is stochastic, proposing valuation tests as a robust alternative. Using valuation tests, they find no systematic evidence for the common ratio effect, seemingly overturning much of the extant literature. We evaluate this conclusion in light of stochastic choice theory. We demonstrate that valuation tests are inherently biased and lack predictive power under standard expected utility assumptions. In contrast, we advocate for a “strong” paired choice test, proving it remains robustly unbiased across standard models of stochastic choice. Applying this strong test to existing experimental data, we find that the common ratio effect remains highly prevalent.

Tserenjigmid: Department of Economics, UC Santa Cruz, gtserenj@ucsc.edu.

1. Introduction

Few behavioral phenomena have had the impact of the Allais [1953] paradox. It has sparked a large empirical literature and motivated many theoretical models of non-expected utility [Machina, 1987; Camerer, 1995; Machina, 2008; Barberis, 2013; Machina, 2018]. We are concerned with a basic aspect of the Allais paradox, the common ratio effect. In particular, we focus on the meaning of the common ratio effect when there is noise or randomness in agents’ choices. Such randomness seems inevitable in any serious empirical discussion of the Allais paradox.

To be concrete, consider two choice problems. First, a choice between a sure payment and a risky lottery . Second, a choice between and , which are scaled-down versions of and involving the same probabilities. An expected utility maximizer chooses over if and only if they choose over . The Allais paradox is the systematic violation of this prediction. The common ratio effect is the behavior of choosing over and over . A test for whether the probability of choosing over equals the probability of choosing over is called the weak paired choice test.

Loomes [2005] and McGranaghan, Nielsen, O’Donoghue, Somerville, and Sprenger [2024] argue that randomness in choices may induce the common ratio effect even for an expected utility agent. In other words, the weak paired choice test that defines the common ratio effect is biased against expected utility when choices are random.

This bias has motivated McGranaghan et al. [2024] (MNOSS) to propose paired valuation tests instead of paired choices (essentially eliciting certainty equivalents, or scaled certainty equivalents, for lotteries and ). There is a mean and sign version of the valuation test (see Section 2.5). MNOSS argue that these tests perform better than the weak paired choice test when choices are stochastic, and run new experiments to elicit valuation data. Their analysis using valuation tests shows little support for the common ratio effect using aggregate data, and “substantial heterogeneity” at the individual level. They find that individual evidence for the common ratio effect in valuations is predictive of common ratio effects in paired choices, which validates their methodology. Consequently, they conclude, there is no support for a systematic common ratio effect.

The results in MNOSS thus seem to overturn the majority of the existing empirical evidence, which has overwhelmingly favored the common ratio effect. For example, a recent survey by Blavatskyy et al. [2023] documents that 78% of 143 studies testing expected utility theory find evidence consistent with the common ratio effect.

Our paper contributes to the debate by taking a close look at models of expected utility and stochastic choice. The bias of the weak paired choice test relies on an assumed model of stochastic choice. The test is biased under the stochastic choice model that adds an i.i.d. noise term to expected utility: we shall call it the i.i.d. Additive Random Expected Utility (iAREU) model. While common in the experimental literature, as a random version of expected utility, the iAREU is questionable. Under the iAREU, each realized utility function will, with probability one, be non-expected utility. The independence axiom is violated with probability one.

A natural alternative model is the random expected utility model of Gul and Pesendorfer [2006].111For an exposition of stochastic choice, including a discussion and comparison of iAREU and random expected utility, see Strzalecki [2025]. We follow his terminology here and repeat some of the points he makes in comparing various models. The random expected utility model delivers an expected utility function with probability one. Our first observation is that the weak paired choice test is unbiased under the random expected utility model. In fact, the main axiom used by Gul and Pesendorfer rules out the common ratio effect in a weak paired choice test.

If one abandons the weak test, a robust alternative exists. We advocate for a strong paired choice test: If choices are noisy, it is natural to say that an agent prefers to if they choose more than half the time. The strong test simply requires that an EU agent prefers to if and only if they prefer to . We show that the strong test remains unbiased for the different models of random utility that we consider in the paper, including the iAREU.

Next, we study the proposed valuation tests and show that they can be problematic. Under reasonable assumptions about noise and heterogeneity, valuation tests are consistent with a wide range of valuations: We prove an “anything goes” result (Proposition 1). The mean valuation test is biased unless agents are exactly risk-neutral, and the sign valuation test relies on symmetry assumptions about the correlation of error terms.

Table 1 contains a summary of our results.

| Weak paired choice test | Strong paired choice test | Mean valuation test | Sign valuation test | |

|---|---|---|---|---|

| Random EU | Unbiased | Unbiased | Unbiased | Unbiased |

| Fechnerian random utility | Biased | Unbiased | Biased | Unbiased∗ |

| Random Perception and Utility | Unbiased∗ | Biased | Biased∗ | |

| Random prospect theory | Unbiased | Biased | Biased | |

| Assumption 2b | Biased | Unbiased | Anything goes | Anything goes |

| Weak expected utility | Unbiased |

The models listed in Table 1 are described in detail in Section 2.1 below. The “Random EU” model is Gul and Pesendorfer’s random expected utility model, while Fechnerian models are well-known generalizations of iAREU. Random perception and random prospect theory assume randomness in probabilities, either as perception or measurement error or as a random probability weighting function. The row for “Assumption 2b” corresponds to the assumptions in MNOSS, under which the weak test is biased. MNOSS show that the sign test is unbiased under different assumptions, which we have called “Assumption 3” in the paper.

The result on the unbiasedness of the strong paired choice for the model of random prospect theory, which seems to be new, also requires assumptions that are laid out and discussed in our paper. The entries in the table that are marked with an asterisk require assumptions that are described in the paper.

Table 1 highlights, on the one hand, that all the tests we have considered are unbiased for random expected utility. On the other hand, the strong paired choice is broadly robust across the different ways in which one may model stochastic choice in the expected utility framework. If we adopt the strong paired test as our test for the common ratio effect, there is substantial support for the Allais paradox in the existing literature. The evidence on the strong paired choice is discussed in Section 4.

Finally, the strongest critique of the weak paired choice tests argues that a wide range of choice frequencies is consistent with expected utility and unrestricted preference shocks. We reproduce this critique in Section 4. The flip side of this critique is that allowing for such arbitrary noise leads to a test with very low power. Using simulated choices from prospect theory, in Section 4, we illustrate the problem of low power and compare it with the strong paired test.

Empirical implications.

When we look at the data using the strong paired choice test, we find strong empirical support for the common ratio effect. In the 143 experimental studies from the recent meta-analysis by Blavatskyy et al. [2023], 41% of these studies display a common ratio effect, while 7% display a reverse common ratio effect. When weighting these studies by the number of participants, over 50% of all surveyed experiments exhibit either a common ratio effect or a reverse common ratio effect.

Applying the strong test to the experimental data in MNOSS reveals a 10% prevalence of the common ratio effect and a 10% prevalence of the reverse effect. This lower detection rate reinforces one of their critiques: parameter selection affects results. Historically, the literature has tested for the common ratio effect within a selective region of the parameter space. Our analysis of their data and additional numerical exercise in Section 4 confirm that stepping outside the traditional window diminishes the effect. Arbitrary parameters often fail to induce the behavioral tension of the common ratio effect, even under prospect theory. Understanding how and why specific parameter choices drive these preference reversals, and what the proper strategy should be for testing the common ratio effect seems like an important question that deserves more attention, which we begin to discuss in Section 4.

Section 5 summarizes the main takeaway messages of our paper and discusses potential applications of our strong paired choice test and methodology for detecting different behavioral puzzles, such as present bias in intertemporal choice, from choice data.

2. Preliminaries

We study choices between lotteries with objective risk. Given is a finite set of monetary prizes with . A lottery is a probability distribution over . We denote by the set of all lotteries. We focus on simple lotteries with two outcomes: a monetary payoff and . The lottery that pays with probability and with probability is denoted by .

Before stating our results, we briefly review the necessary background notions from stochastic choice theory. Our terminology follows the recent monograph by Strzalecki [2025].

2.1. Stochastic choice.

A stochastic choice function specifies, for any finite set , the probability of choosing each lottery in . Thus is the probability of choosing . We focus on sets with two lotteries, which allow us to simplify the notation. When , we write , or just , for the probability of choosing lottery from the doubleton set .

Empirical analysis of choice data often assumes that choice is random. There are at least two sources of random choice: preference heterogeneity and random preferences. First, if the choice data are collected from a population of agents, choices are stochastic due to preference heterogeneity — different people make different choices when they face the same choice problem. Second, choice data may be stochastic due to random preferences: the same agent makes different choices when they face the same choice problem. The same agent may choose different options due to mistakes, a preference for randomization, and so on.222Individuals often make different choices in apparently identical situations, even when the interval between successive choices is very short (see Tversky [1969], Ballinger and Wilcox [1997] Hey [2001], and Agranov and Ortoleva [2017].)

In deterministic settings, a typical test of expected utility theory is to check the Independence Axiom via paired choice tasks. For example, if is chosen over , but is chosen over , then we would conclude that expected utility theory is violated in favor of the common ratio effect. The question at hand is how to test expected utility theory (or the common ratio effect) when stochastic choice data is observed, where stochasticity is due to preference heterogeneity and random preferences. In particular, we observe and . Without restrictions on (or a model of) stochastic choice data, such testing is not possible. Below, we review some of the most popular models of stochastic choice.

2.1.1. Random utility

We say that a stochastic choice function is a random utility choice function if there exists a utility function , together with a random function , such that

for all , where denotes the probability inherent in the probability model of the random function .333When the set of alternatives is finite, which is always true in the experimental setting, the additive structure of error is without loss of generality (see Strzalecki [2025]).

2.1.2. Fechnerian random utility

The stochastic choice function is Fechnerian if there exists a utility function , together with a strictly monotonically increasing function that is symmetric (meaning that ) such that

A random utility model given by a utility and a random error , such that are i.i.d. draws from some strictly increasing distribution function, is Fechnerian, where is the cumulative distribution function of the difference .444Since , we need to have . This implies . In this case, we shall always assume (in fact, without loss of generality) that .

2.1.3. i.i.d. Additive Random Expected Utility (iAREU)

A special Fechnerian model obtains when the utility function takes the expected utility form. Let the von Neumann-Morgenstern (vNM) utility function be such that ; the latter expectation is taken over the random prizes in the lottery . We shall always normalize so that and assume that is continuous and strictly monotonically increasing. In a notational shortcut, we write as .

If is the simple lottery , then . Once has an expected utility representation, the assumption that is restrictive.

Note that, if the errors are independent and identically distributed (i.i.d), then

where is the cumulative distribution function of the differences in errors, . Such a random choice function is termed an i.i.d. additive random expected utility (iAREU).

2.1.4. Random Expected Utility

In contrast to the model of additive random utility, the random expected utility model takes the function to be random. For example, if the utility of a monetary payoff is , where is a random function, then the utility of a simple lottery is . The stochastic choice between two simple lotteries and is

The random expected utility model is axiomatized by Gul and Pesendorfer [2006]. The key axiom behind the model, termed Linearity, is motivated as a stochastic version of the Independence Axiom of the expected utility theory. We shall see that Linearity is intimately tied to the weak paired choice test.

2.1.5. Random expected utility vs. iAREU

For our purposes, it is important to understand the choice between iAREU and random expected utility as modeling devices. Strzalecki [2025] provides a detailed discussion (see Section 4.6), which we proceed to summarize. The bottom line is that the iAREU model is problematic.

First, under the model of random expected utility, the random utility has the expected utility form with probability one. Under the iAREU model, this occurs with probability zero. In other words, the iAREU model of stochastic choice puts zero weight on a preference over lotteries that has the expected utility form.

Second, the iAREU model can violate monotonicity in the sense of first-order stochastic dominance. Random expected utility, in contrast, always respects first-order stochastic dominance.

2.2. Random choice in McGranaghan et al. [2024]

MNOSS formulate their model using a reduced-form device. They use the iAREU model to argue that weak paired choice tests are biased, but then move to a reduced-form model that is particularly well suited to analyzing valuation tests. The model is motivated as a generalization of iAREU.

We lay out their assumptions here.

Assumption 1. There is a strictly increasing function with the property that for all . The pair of random variables is drawn from a continuous joint distribution with convex support such that

and

For iAREU, it is easy to see that and .

It is important to note that noise terms and are fundamentally different from error terms . In particular, captures perceptual errors and preference heterogeneity/random preferences, while and are residual terms that will be derived from given the random choice model and von Neumann-Morgenstern utility (see Section 3.3 and the model in Equation 1 for an example of how these errors may be obtained from more primitive preference shocks).

MNOSS show that the weak paired choice test is biased under either of the following two assumptions.

Assumption 2a: , for , and .

Assumption 2b: for , and is symmetric around zero.

Comparing the two sets of assumptions, note that Assumption 2a imposes stronger restrictions on but weaker restrictions on noise terms, while Assumption 2b imposes no restrictions on but stronger assumptions on noise terms. Either way, the assumptions impose that for and . When introducing Assumption 2a, MNOSS interpret the noise terms as an additive disturbance to an underlying value. They think of the additive model as a statistical model of valuations, not as the result of an underlying model of stochastic choice.

MNOSS also show that the sign valuation test is unbiased under the following assumption.

Assumption 3: The joint distribution is symmetric around some median vector .

Assumption 3, when compared to Assumption 2b, drops the requirement for , but imposes joint symmetry (a central symmetry of the joint density function). Assumption 3 implies that each marginal distribution is also symmetric around ; and the symmetry around a median implies that the mean is also equal to .555We are assuming here that the errors have finite means.

Thus, all three assumptions in MNOSS imply that . We discuss this property in Proposition 6 and Proposition 10 below.

Remark 1.

Observe that Assumption 3 is not weaker than 2b. For example, suppose with probability and with probability where . Note that and and . Yet, is not symmetric. (In Appendix A we provide a more elaborate example that has a positive density on .)

2.3. Tasks

Given two lotteries, and , a paired choice task elicits a choice between and . The common ratio effect typically involves two paired-choice tasks:

AB choice:

CD choice:

A valuation task takes as given a probability and a lottery . Then it elicits a monetary quantity such that is indifferent to . MNOSS use paired valuation tasks motivated by the AB and CD choices in the common ratio effect. This task elicits two monetary amounts and such that

2.4. Paired Choice Tests

The linearity axiom of Gul and Pesendorfer [2006], a stochastic-choice version of the independence axiom, implies that . The weak paired choice test for expected utility theory is that . When this is rejected in favor of , we say that the stochastic choice exhibits the common ratio effect.

The strong paired choice test for expected utility theory is that if and only if . When this is rejected in favor of and (or and ), we say that the stochastic choice exhibits the common ratio effect. Kahneman and Tversky [1979] described the common ratio effect in these terms, as a rejection of the strong paired choice test. Indeed, the common ratio effect is defined in this way by Ballinger and Wilcox [1997], who pioneered the literature on testing the common ratio effect in a stochastic choice framework (see p.1092).

The idea behind the strong test goes back to a classical question in welfare economics and stochastic choice: when can we conclude that is preferred to ? If one insists on deterministic choice, we might decide that is preferred to only when . For empirical purposes, however, one has to work with stochastic choice. We may then say that is preferred to whenever is large enough (e.g., see Fishburn [1978]); and it is natural to say that large enough means . So we might decide that is preferred to when . This is in line with Logit models of discrete choice (in fact, by all Fechnerian models), and used by Kahneman and Tversky [1979]’s descriptions of the common ratio effect as well as the common consequence effect.

Experimental evidence on the Allais paradox often involves a between-subjects analysis: Stochastic choice reflects the choices of a population of individuals, and the data are only useful to the extent that the population shares some common preferences. Here we seek to infer whether is commonly preferred to from observing . And again, is a natural requirement for the inference that is ranked above .

What does this mean for the common ratio effect and the Allais paradox? In Allais’ original deterministic-choice thought experiment, he would require to be preferred over and to be preferred over (with at least one strict preference). Given our discussion of how to formulate the question in a setting of stochastic choice, the minimum requirement for the common ratio effect is that (or ). See Ballinger and Wilcox [1997] for a similar argument. Note that, while these inequalities are a minimal requirement for the effect, they imply that . Hence, the strong test requires stronger evidence than the weak test does before it rejects expected utility theory.

2.5. Valuation Tests

In contrast to the paired choice tests, the valuation test involves eliciting valuations for lotteries and as described above. The valuation test is the statement that .

When choice is stochastic, these valuations will be random, even when the decision maker is consistent with expected utility theory. Therefore, we have two versions of the valuation test:

-

•

The sign test requires that .

-

•

The mean test requires that .

When the sign test is rejected in favor of , or the mean test is rejected in favor of , then we say that the decision-maker exhibits the common ratio effect.

We start by pointing out that valuation tests do not provide sharp predictions under the iAREU model that motivated the move away from the weak paired choice test. One might have hoped that valuation tests are more robust to individual heterogeneity and noise, but the following proposition shows that, in a sense, “anything goes” for the valuation tests. In the next proposition, we assume that for some CRRA von-Neumann Morgenstern utility function .

Proposition 1.

Consider an expected utility agent with a CRRA von-Neumann Morgenstern utility function , where . Fix and . Suppose that .

-

(1)

For any , there exists and a distribution of satisfying Assumption 2b, and for which each marginal distribution is symmetrically distributed around its mean and median (which equals 0), such that

-

(2)

For any , there exists a distribution of satisfying Assumption 2b, and for which each marginal distribution is symmetrically distributed around its mean and median (which equals 0), for which

The first statement of Proposition 1 is illustrated in Figure 1, which shows the range of possible values of the expected valuations as the coefficient of relative risk aversion decreases to .

Remark 2.

Proposition 1 is in contrast with Proposition 2 of MNOSS, which shows that when , and that under Assumption 3.

The explanation for this discrepancy is that the mean test is very sensitive to the curvature of , which depends on the agents’ level of risk aversion. In the context of the iAREU model, Proposition 2 of MNOSS requires risk neutrality. We show that the level of risk aversion may be chosen to achieve any pair of non-negative expected valuations. The problems with the mean tests are acknowledged by MNOSS, who show that it can be biased under Assumption 2b.666This is shown formally in their online appendix and mentioned in the main text of the paper. Their main message is that there are assumptions under which the traditional weak paired choice test may be problematic, while tests using paired valuations may not be problematic.

The sign test, on the other hand, is sensitive to the correlation between errors. When errors are independent, of course, we obtain that . But it seems important to allow for deviations from independence, especially (but not exclusively) if the test is to be used for individual-level data. Assumption 3 allows for correlated errors and ensures that the sign test is unbiased; however, it also limits the correlation among errors in significant ways, as we saw in the remark following Assumption 3 above.

3. Paired choice tests

In light of the issues with valuation tests highlighted by Proposition 1, we proceed to discuss the paired choice tests. We discuss the properties of the paired choice tests in the context of the different models of stochastic choice that we have introduced.

3.1. The iAREU model

Following Loomes [2005] and McGranaghan et al. [2024], we first consider the weak paired choice test under the Fechnerian iAREU model of stochastic choice (see Section 2.1.3). Let be a vNM utility and be strictly increasing and symmetric such that

Then, for the weak paired choice test, we have

Hence,

unless . More importantly,

So the weak paired choice test is biased in the sense that it detects the common ratio effect even when the underlying model is iAREU, and therefore “consistent” with expected utility. In making this point, Loomes [2005] cautioned that the statement “ is significantly higher than ” is sensitive to the assumptions made regarding the underlying model of stochastic choice. Under the iAREU model, the common ratio effect, as defined through the weak paired choice test, should not be seen as grounds to reject expected utility theory. MNOSS use the bias of the weak paired choice under the iAREU as a starting point to motivate their focus on valuation tests.

The status of iAREU as the “correct” formulation of the expected utility model for stochastic choice is, however, questionable. There are several arguments against the iAREU: the iAREU model delivers non-expected utility preferences with probability one; it may violate monotonicity with respect to first-order stochastic dominance, and it can overturn the decision-maker’s underlying risk preferences. See our discussion in Section 2.1.5. What should we then make of the bias of the weak paired choice test? Is the bias of the test due to problems of the iAREU as a stochastic incarnation of expected utility theory; or is the test itself problematic?

3.2. Random Expected Utility Model

In random expected utility (Section 2.1.4), the random utility of a binary lottery is given by , where captures a utility shock. The paired choice test is unbiased under this model of stochastic choice because

In fact, the unbiasedness of the test holds without needing to make any assumptions about the (joint) distribution of errors .

Notice that the random expected utility is a special case of additive random utility where . However, the i.i.d. assumption made in the iAREU model (3.1) is violated under random expected utility. Under random expected utility, errors are independent but not identically distributed when are i.i.d.

Gul and Pesendorfer [2006] propose a behavioral justification for random expected utility in the form of the stochastic analogue of the independence axiom of classical expected utility theory. Independence requires that is preferred to if and only if is preferred to . The version of the independence axiom in the context of stochastic choice, called Linearity, is:

Linearity is the key axiom that characterizes random expected utility, and justifies this model as the “correct” extension of expected utility theory to the stochastic choice framework. Gul and Pesendorfer [2006] write “Studies that investigate the empirical validity of expected utility theory predominantly use a random choice setting. For example, Kahneman and Tversky describe studies that report frequency distributions of choices among lotteries. These studies test expected utility theory by checking if the choice frequencies remain unchanged when each alternative is combined with some fixed lottery; that is, by testing our linearity axiom.”888They also write “Linearity is analogous to the independence axiom of the von Neumann–Morgenstern theory. Note that this “version” of the independence axiom corresponds exactly to the version used in experimental settings. In the experimental setting, a group of subjects is asked to make a choice from a binary decision problem . Then the same group chooses from a second decision problem obtained from the first by replacing the lotteries in the original problem with and . Linearity requires that the frequency with which the lottery is chosen in the first problem is the same as the frequency with which the lottery is chosen in the second problem.” Their arguments imply that if one assumes a stochastic choice model that violates Linearity, then one already assumes, from the beginning, that a basic tenet of the theory is violated. We formalize this as Proposition 2.

Indeed, the iAREU model violates Linearity. To illustrate, consider lotteries and . The random utility of is where is i.i.d. Let and . Hence, . However, when and , we have and . Hence,

This example shows that the iAREU model exhibits counterintuitive behavior in contexts that are similar to the Allais paradox. However, the problem is deeper than a single counterexample may suggest. Consider the following version of Linearity, formulated for simple binary lotteries. This version essentially amounts to the weak paired choice test.

Weak Linearity: For any and ,

It turns out that Weak Linearity is fundamentally in conflict with the iAREU. To formalize this observation, we shall need an additional assumption. A stochastic choice function is scalable with respect to expected utility if there are functions and such that is strictly increasing in the first argument when , and for any ,

Proposition 2.

Any stochastic choice function that is scalable with respect to expected utility violates Linearity. If it satisfies Weak Linearity, then it is Fechnerian but not iAREU.

We now turn to the connection between the strong paired choice test, valuation tests, and Linearity. We may relax Weak Linearity in the following two ways.

Tied Linearity I: For any and ,

Tied Linearity II: For any and ,

Tied Linearity II implies Tied Linearity I. The reverse is true under a monotonicity assumption that is satisfied throughout the paper. Hence, Tied Linearity I and II are equivalent for our purposes. Monotonicity is also assumed by the multiple-price list method used to elicit valuations.

The strong paired choice test assesses Tied Linearity II, while the paired valuation test essentially evaluates Tied Linearity I. Thus, at a conceptual level, the strong paired choice and valuation tests are assessing the same weakening of Weak Linearity. However, a difference is that the nature of the valuation test (where certainty-equivalents are elicited) requires some additional assumptions. This means that the strong paired choice test is unbiased under weaker assumptions than the valuation test.

3.3. The unbiasedness of strong paired choice test

In this section, we show that the strong paired choice test is robustly unbiased across various standard models of stochastic choice.

The strong paired choice test is unbiased under the Fechnerian model of iAREU. The statement that is equivalent to , while is equivalent to . Hence,

More formally, the strong paired choice test is unbiased as long as the stochastic choice satisfies weak stochastic transitivity with respect to expected utility: there is such that

In light of our discussion of how preferences are inferred from stochastic choices, the connection between and is natural. In particular, Fechnerian models satisfy strong stochastic transitivity with respect to expected utility.

Consider a generalization of the Fechnerian model that is motivated by He and Natenzon [2024]. The stochastic choice has a weak expected utility representation if there is a cdf , and a strictly positive valued function , such that .999He and Natenzon [2024] characterizes the weak utility presentation by means of weak stochastic transitivity. The above model is the expected utility version of the weak utility representation.

Proposition 3.

Suppose that the stochastic choice has a weak expected utility representation. Then

Many stochastic choice models have a weak utility representation when errors are correlated. For example, some of the most famous discrete choice models in economics and psychology such as the covariance probit (Thurstone [1927]), nested logit (Ben-Akiva [1973], McFadden [1978]), the elimination-by-aspects (Tversky [1972]), and the random coefficients model of Hausman and Wise [1978] have a weak utility representation, but not Fechnerian.101010See He and Natenzon [2024] for more examples. Hence, the expected utility version of these models will have weak expected utility representations. It is also important to note that weak utility representation goes beyond the random utility framework. Hence, the above result demonstrates that the strong test is unbiased under a general class of stochastic choice models.

Finally, we turn to the strong paired choice under the assumptions of MNOSS (see Section 2.2). MNOSS show that the weak paired choice test is biased under either of Assumption 2a or 2b. We first show that the strong paired choice test is unbiased under an assumption weaker than Assumption 2b. Then we show in Appendix B that their Assumption 2a is violated except for very narrow cases (this fact is already acknowledged by MNOSS ).

Proposition 4 (Unbiasedness of Strong Paired Choice Test).

Assume Assumption 1 and that . Suppose that . Then,

The assumption on noises in Proposition 4 relaxes Assumption 2b of MNOSS in two directions. First, we drop the assumption for . Second, holds whenever and are symmetric around zero, which is required by Assumption 2b.

Assumption 2b is satisfied under the iAREU model, which has a Fechnerian representation. Below, we show that guaranteeing either or the assumption is challenging once we deviate from iAREU.

To demonstrate that the strong paired choice test can be unbiased beyond Assumption 2b, consider the following model that allows for a “perceptual” error (or random probability weighting) and a utility over money.

| (1) |

Here, captures a perceptual error, captures randomness in the evaluation of monetary payoffs, captures the remaining error (or the interaction of perceptual and preference heterogeneity). Such a model obtains, for example, when the utility of is .111111Note that this model nests both cases where or and with are identical distributions.

Proposition 5.

Consider the model in Equation (1) and suppose that one of the following assumptions is satisfied:

-

(1)

All errors are symmetric about zero, and any two error terms are either independent or linearly dependent.

-

(2)

Let for some constants where errors are identical or symmetric about zero. All other errors are independent and symmetric about zero.

-

(3)

Errors are independent, either identical or symmetric around the same fixed constant, and independent from and . All other errors are symmetric about zero, and any two of them are either independent or linearly dependent.

Then

The key assumption behind Proposition 5 is symmetry around zero. Due to the existence of , it is without loss of generality in (1) to say that . The results above assume that and are symmetric about zero. If the errors are not symmetric about zero, the model deviates systematically from expected utility. For example, suppose and . Then we have , where the perceived probability is . If is not symmetric, then the model itself has a bias for or against the common ratio effect. In other words, the strong paired choice test would not reject expected utility when the underlying model is unbiased.

Going back to the model of MNOSS discussed in Section 2.2, recall that it implies that . We now connect this property with the model in Equation (1).

Proposition 6.

This result and its proof show that even when are independent and symmetric around zero, we may have .

4. Detecting the Common Ratio Effect via Paired Choice Tasks

In this section, we discuss various methods for detecting the common ratio effect based on paired choice datasets.

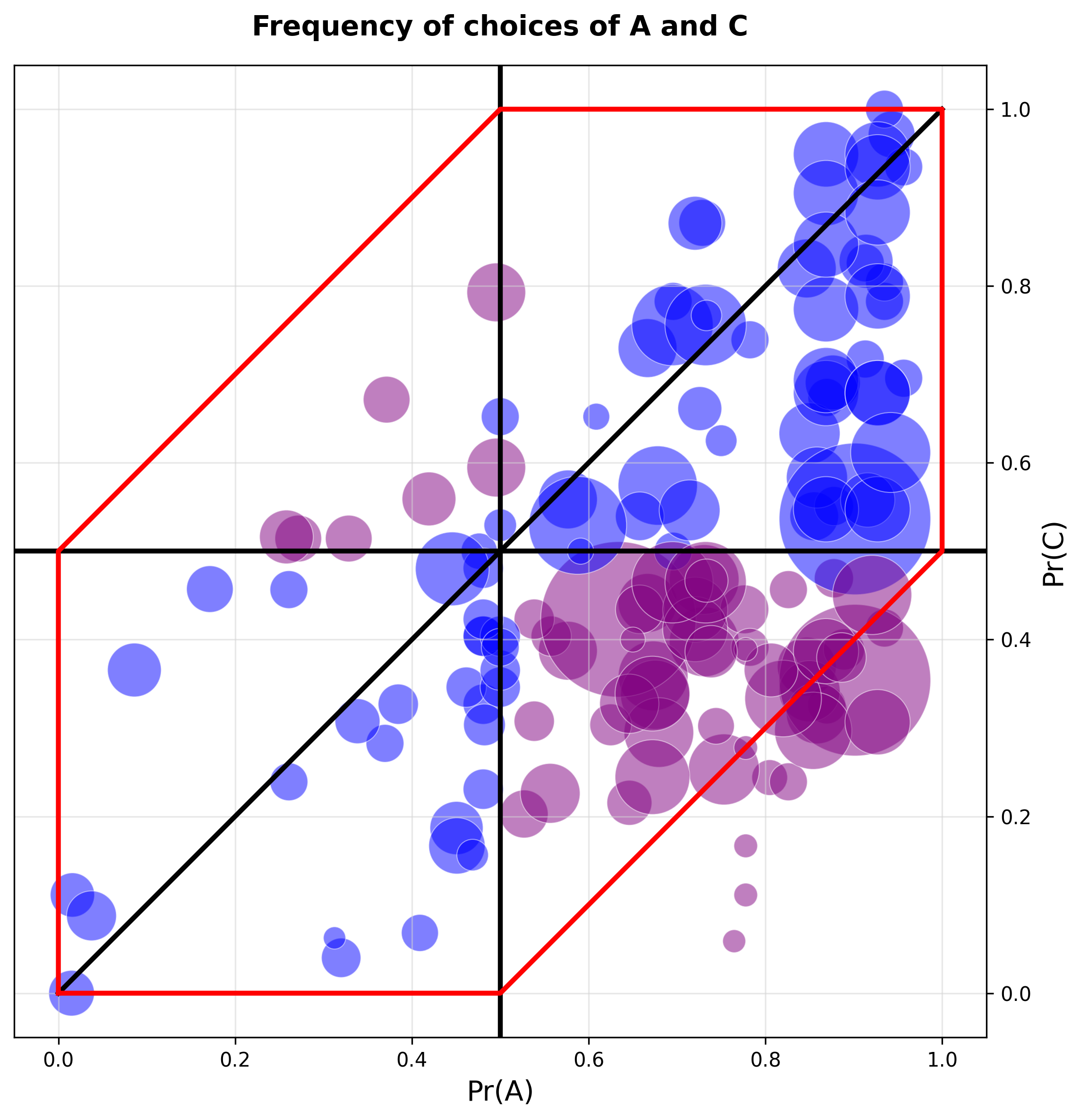

Figure 2 illustrates three possible uses and views of the paired choice test. Panel (a) illustrates the weak paired choice tests: choice frequencies on the diagonal () are consistent with expected utility (EU), while choices below the diagonal indicate the common ratio effect (CRE), and those above the diagonal indicate the reverse common ratio effect (RCRE). Panel (b) illustrates the strong paired choice test that we advocate in Section 3. Finally, Panel (c) reproduces Figure 2 in MNOSS . It shades in gray all the choice frequencies that are consistent with expected utility and a general structure of random utilities. Specifically, the gray area comprises all the choice frequencies obtained when agents 1) choose either and or and with frequencies (say) and ; and 2) when intending to choose a lottery , they indeed choose it with a probability of at least .

We reproduce one of MNOSS results in Figure 3, which depicts the choice frequencies in 143 studies taken from the meta-analysis in Blavatskyy et al. [2023]. Each study is represented by a “bubble” that is scaled in size to reflect the number of participants in the study.121212See Panel A of Figure 2 and Figure D.1 of MNOSS . Our graph is made from the data in the replication package in Blavatskyy et al. [2023], while Table 2 is calculated from the data in MNOSS . The choice frequencies in the literature largely fall in the gray area of Panel (c) in Figure 2. The conclusion is that the paired choice test fails to reject expected utility once one allows for general noise in participants’ utilities.

In contrast, the strong test has substantial empirical bite. In Figure 3, the studies shown with purple “bubbles” are those that fall outside the two squares on the main diagonal. These exhibit a violation of expected utility according to the strong test. Those that fall to the right of the vertical line and below the horizontal line exhibit the common ratio effect. The studies to the left of the vertical line and above the horizontal line exhibit the reverse common ratio effect.

The discrepancy between the strong test and Panel (c) of Figure 2 is easy to understand. Consider, for example, the choice frequencies . In Panel (c), one could argue that these frequencies reflect an expected utility agent, or a population of agents, who would choose and with probability ; and and with probability ; however, when they are to choose , they do so for sure, and when they are to choose , they do so with probability . For the strong test, we turn the threshold on its head: we infer from that is preferred to , and from that is preferred to . Then we conclude that these choices are inconsistent with expected utility theory.

Using the strong paired choice test, 41.26% of the designs surveyed in Blavatskyy et al. display a common ratio effect, while 7% display a reverse common ratio effect.131313The observed percentages of the (reverse) common ratio effect in Blavatskyy et al. will be 51% (resp., 6%) if we allow for a 95% confidence interval for sampling errors. For example, the observed frequencies and will be consistent with the common ratio inequality and . The corresponding numbers in the experiments conducted by MNOSS are 10% each. These results are summarized in Table 2. The strong test finds the same prevalence of the common ratio effect and the reverse common ratio effect in the experiments conducted by MNOSS, which is consistent with the message in their paper. If we weight the studies in Blavatskyy et al. by the number of experimental participants, we see that almost 50% of experimental participants across the surveyed experiments exhibit either a strong common ratio effect or a reverse common ratio effect.141414The sizes of the different experiments in MNOSS are similar. There are a total of 900 participants in their experiments and 14909 in the experiments surveyed by Blavatskyy et al..

| SPC | ||||||

|---|---|---|---|---|---|---|

| PrA | PrC | CRE | CRE | RCRE | ||

| McGranaghan et al. | 49.46% | 46.77% | 65.83% | 10.00% | 10.00% | 120 |

| Blavatskyy et al. | 67.37% | 48.27% | 79.02% | 41.26% | 6.99% | 143 |

Note: CRE is the prevalence of the common ratio effect according to the weak paired test. The following two columns contain the prevalence of the common ratio effect and the reverse common ratio effect, according to the strong paired test. The number of experiments in each study is .

To reiterate, the criterion in Panel (c) means that expected utility is largely not rejected by the studies on the common ratio effect in the literature. The flip side of this is that the paired choice test, when interpreted as in Panel (c), has very low power to test for expected utility. To illustrate this lack of power, we simulate choices made under prospect theory. Consider a CRRA utility function and distortion function . Let , , and and . We run 1000 simulations for and , which are the sample averages of 100 independent choices according to the above prospect theory preference with i.i.d. and uniform errors and on . We plot distributions of in Panel (b) of Figure 3.

We find that, among 10000 simulations, only 3 choice frequencies lie within the CRE area in Panel (c). In other words, there is almost zero chance of rejecting expected utility, even for a prospect theory preference that deviates substantially from expected utility, if we use the criterion of Panel (c). In contrast, under the strong paired choice test (see the CRE area in Panel (b) of Figure 2), expected utility is correctly rejected for 9727 of 10000 simulations.

To further illustrate the low power of the test criterion in Panel (c), we note that it is very unlikely to generate a preference reversal consistent with the common ratio effect when the values of are arbitrarily chosen as in MNOSS .151515As noted in MNOSS, the prior literature on the common ratio effect has focused on values such that . For example, consider a CRRA utility function and distortion function with . Let us consider all parameter value combinations of such that with , . There are 3645 possible combinations of such values. However, only 383 combinations (10.5%) exhibit a preference reversal consistent with the common ratio effect: and . For the remaining 3262 combinations (89.5%), comparisons are consistent with expected utility: either and or and .

In other words, we are unlikely to observe the common ratio effect, even for prospect theory preferences that the strong test would reject as being inconsistent with expected utility, for arbitrary combinations of the parameters in the paired choice task. The reason is that the expected values of and , and may be too far apart for a preference reversal. Conditional on exhibiting the common ratio effect (i.e., within the aforementioned 383 combinations), the average is and the average ratio is (the median is and the median is ). Moreover, for all the 383 combinations that produce the common ratio effect, we have . To some extent, our exercise reinforces the message of MNOSS that finding the common ratio effect depends on where one looks for it.

The issue of parameter selection poses an important question. The implicit assumption in choosing arbitrary parameter values is that we want to understand how “global” the common ratio effect is; how prevalent it is across possible decision problems. Another perspective is that we want to know whether subjects at all exhibit the common ratio effect — somewhere. A formal definition of the effect in a deterministic setting is and for any . The paired valuation test is based on this definition, and it is reasonable to expect to observe the effect for various combinations of if the effect is robust. However, this is not the case for paired-choice tasks, where the same values of are used across many experimental subjects with different risk preferences. It is not possible to find such that for many different subjects. Moreover, if the values are such that , then we cannot find the effect, i.e., there is a bias against the common ratio effect. So experimentalists need to find values such that and if expected utility is the null hypothesis and the common ratio effect is the alternative hypothesis. Similarly, if is too large relative to , then we obtain and ; i.e., no choice reversal. It is arguably for this reason that the literature has focused on parameter values such that the expected values of and , and , are close to each other, and the majority of subjects prefer over ; i.e., .

5. Implications

What is the takeaway message of our results? First, the assumed model of stochastic choice is very important. When we follow the decision theoretic literature and adopt the model of random expected utility, the weak paired choice test is unbiased and reinforces the standard conclusion in the literature that the common ratio effect is prevalent.

Second, if we instead focus on other models of stochastic choice (including the model of Fechnerian additive random utility), then the strong paired choice is unbiased. Indeed, the literature has often focused on the strong paired choice test. Kahneman and Tversky [1979] describe one of the earliest experimental demonstrations of the common ratio effect. Their result is that 80% of subjects choose over , while 65% of them choose over . They write, “To show that the modal pattern of preferences in Problems 3 and 4 is not compatible with the theory,” and then they proceed to explain why the patterns and are inconsistent with expected utility theory. Ballinger and Wilcox [1997], who pioneered the literature testing the common ratio effect in the stochastic choice framework, defined the common ratio effect in this way. Under the unbiased strong paired choice test, we find significant support for the common ratio effect, as discussed in the previous section and in Figure 3.

Third, our results qualify the findings in MNOSS, who find no evidence of a systematic common ratio effect in their aggregate data. Their central conclusions contrast with the previous literature, which is almost exclusively based on paired-choice tasks and shows strong evidence of a common ratio effect. MNOSS explain the discrepancy through three mechanisms. The first is that the weak paired choice test is biased towards finding a common ratio effect, while the paired valuation test is (under the same assumptions) unbiased. Using valuation tests, they do not find evidence of an aggregate common ratio effect. Third, their experiments with paired choice tests are validated at the individual level by the valuation test and indicate little evidence of a systematic common ratio effect. We offer a somewhat different perspective on these discrepancies.

In Proposition 1, we demonstrate that for paired valuation tests under Assumption 2b, essentially “anything goes.” The mean test is systematically biased unless participants are exactly risk neutral, and the sign test hinges on a demanding symmetry condition that tightly constrains the correlation of preference shocks across tasks. In sharp contrast, the strong paired choice test remains unbiased across a wide range of stochastic choice models and requires assumptions strictly weaker than Assumption 2b. We also show that the Panel (c) test for the weak paired choice condition has low power, making it difficult to reject the null of expected utility even when it is false.

Taken together, these findings provide robust empirical support for the Allais paradox in the guise of the common ratio effect. If we treat the random expected utility model as the canonical representation of expected utility in stochastic choice, the common ratio effect typically emerges through the weak paired choice test. But if we want conclusions that are robust to alternative formulations of stochastic expected utility theory, the strong paired choice test is the tool of choice. Under this more demanding standard, we still find clear and substantial evidence for common ratio and reverse common ratio effects.

The strong paired choice test we advocate can be applied more broadly and is useful for detecting various behavioral puzzles in choice data. Many behavioral puzzles take a form similar to the common ratio effect: is preferred over , but is preferred over , where and are certain transformations of and , respectively. As long as if and only if , where is the corresponding utility representation of the standard model, our strong test “ iff ” is robustly unbiased. For example, consider the common consequence effect of the Allais paradox, which is exhibited if is preferred over while is preferred over . Since under expected utility, the strong test is unbiased. Alternatively, consider present bias in intertemporal choice. The bias is exhibited if is preferred over while is preferred over , where is a delayed reward that returns at time . Since under exponential discounting, the strong test is unbiased. Therefore, our strong test and the corresponding discussion of different approaches to modeling expected utility are readily applicable to various behavioral puzzles and choice contexts.

6. Proofs

6.1. Proof of Proposition 1

For notational economy, define . We need to study the following random valuations:

| (2) | ||||

| (3) |

Part 1. First, we prove the first statement in Proposition 1. Suppose that and are mean-zero, symmetric, random variables such that for some . Specifically, we assume symmetric two-point distributions and , subject to the constraint that the base of the exponent remains strictly positive (so and ).

We seek to determine the full range of achievable values for as span their permissible supports and as varies from down to .

Because , the transformations of the two random variables are convex. By Jensen’s Inequality, the minimum expected value for any mean-zero distribution occurs when the variance is zero. For both functions, this absolute minimum is:

The maximum expected value is achieved by maximizing the variance. For , as :

Substituting yields the supremum:

Because the variances of and can be chosen independently via the scalar , the joint achievable range for any fixed is exactly the Cartesian product of their individual ranges:

Note that the minimum is monotonically increasing in and the maximum is monotonically decreasing as long as .

As , the limits converge to and . The square collapses to the point . In contrast, as we get and . So

Part 2. We now turn to the proof of the second statement in Proposition 1. In particular, we now consider the values that

can take under the same assumptions as above, with the difference that we now fix to be uniform distributions because this allows for a richer behavior of the joint distribution of .

As before, we may define ; the actual numbers of , and do not matter, only that and . Note that

We assume that and are two mean-zero uniform random variables, possibly with different supports. This ensures that equals in distribution for some . The supports need to be such that and with probability one because the power may not be defined otherwise.

Suppose first that the support of is greater than the support of . Define and . Let and be positive real numbers such that . Let and be two independent, uniform, random variables. Define the random variable piecewise, conditional on the value of and , by

where and . This construction is illustrated in Figure 4.

First, we show that . To this end, we focus on the decomposition of according to the values of . Specifically,

Case 1: . Since the minimum value of conditional on is , the term is zero for any . Conditional on , . Thus,

as and .

Case 2: . Again, we use the decomposition of according to . We have that and the event implies that . Therefore, the intersection of these events is simply :

For the second term, conditional on , . By the independence of and :

Now,

Substituting and , we note that and . This simplifies the expression to . Multiplying this by we obtain

Adding the two partitioned terms together gives the CDF for :

We conclude that equals the CDF of a uniform random variable on .

Finally, we calculate . Again we decompose this probability according to the possible values of :

First consider the case when . Here, . Since has minimum value , and , we have . Thus .

Second, consider when . We need to evaluate the inequality , i.e., . Since , we have with probability . Geometrically, this is clear from Figure 4. Thus, .

Putting these together, we obtain that

For each value of we may find such that .

Finally, we turn to the case when the support of is smaller than the support of . Then we can let and . Our previous analysis constructs a joint distribution with the desired marginals, and such that, for each we may find for which

The only value of not covered by the proof is , but this is achieved trivially with independent errors.

6.2. Proof of Proposition 2

Suppose there are functions and such that is scalable with respect to expected utility. It is without loss of generality to assume that . Suppose that Weak Linearity is satisfied. Note that Weak Linearity implies that

For any and ,

Recall that is a finite set of monetary prizes such that . Let and fix .

Take any . First, suppose that . Since the range of is connected, we can find such that , , and . Hence, we have

Second, suppose that . Then we can find such that , , and . Hence, we have

Hence, we have for any . Since , we also have for any .161616Notice that is redundant if either or . Moreover, there is a function such that Hence,

This proves the second part of the proposition. To prove the first part, let us now assume that linearity is satisfied. Then, by the proof of the second part, for any , we need to have

which is violated because for any with .

6.3. Proof of Proposition 3

Since , we have

iff iff .

6.4. Proof of Proposition 4

Suppose there is such that . Since is strictly increasing, we have

and

Hence, since , is equivalent to and is equivalent to . Hence, if and only if .

6.5. Proof of Proposition 5

By Equation (1),

where

and

where

It is enough to show that and are symmetric around zero. Let us prove that is symmetric around zero for all three cases (essentially identical arguments will imply that is also symmetric around zero). We repeatedly use the following two facts:

Fact 1: and are symmetric around zero and either independent or linearly dependent. Then is symmetric around zero for any .

If and are linearly dependent (and since they are symmetric around zero), for some . Hence, is symmetric around zero. If and are independent, then is also symmetric around zero.

Fact 2: and are symmetric around zero and independent. Then is symmetric around zero for any .

Notice that we wrote as a weighted sum of five error terms. All three cases directly assume that each of the first four terms is symmetric around zero. Note that the fifth term is also symmetric around zero. For the first case, and are symmetric around zero and either independent or linearly dependent. Hence, is symmetric around zero. For the second case, and are symmetric around because and are symmetric around zero and independent. For the third case, is symmetric around zero because and are independent, and either identical or symmetric around the same fixed constant.

Finally, is symmetric around zero by Fact 1 in the first and third cases, while by Fact 2 in the second case.

6.6. Proof of Proposition 6

Let us assume that errors are i.i.d. and symmetric around zero and with probability . This case satisfies all three assumptions of Proposition 5. Then by the proof of part one of Proposition 10, we have . It is not difficult to provide examples with non-degenerate error distributions.

References

- Agranov and Ortoleva [2017] Agranov, M. and P. Ortoleva (2017): “Stochastic choice and preferences for randomization,” Journal of Political Economy, 125, 40–68.

- Allais [1953] Allais, M. (1953): “Le comportement de l’homme rationnel devant le risque: critique des postulats et axiomes de l’école américaine,” Econometrica: journal of the Econometric Society, 503–546.

- Apesteguia and Ballester [2018] Apesteguia, J. and M. A. Ballester (2018): “Monotone stochastic choice models: The case of risk and time preferences,” Journal of Political Economy, 126, 74–106.

- Ballinger and Wilcox [1997] Ballinger, T. P. and N. T. Wilcox (1997): “Decisions, Error and Heterogeneity,” The Economic Journal, 107, 1090–1105.

- Barberis [2013] Barberis, N. C. (2013): “Thirty years of prospect theory in economics: A review and assessment,” Journal of economic perspectives, 27, 173–196.

- Ben-Akiva [1973] Ben-Akiva, M. E. (1973): “Structure of passenger travel demand models.” Ph.D. thesis, Massachusetts Institute of Technology.

- Berry et al. [1995] Berry, S., J. Levinsohn, and A. Pakes (1995): “Automobile Prices in Market Equilibrium,” Econometrica, 63, 841–890.

- Blavatskyy et al. [2023] Blavatskyy, P., V. Panchenko, and A. Ortmann (2023): “How common is the common-ratio effect?” Experimental Economics, 26, 253–272.

- Camerer [1995] Camerer, C. (1995): “Individual decision making,” in The handbook of experimental economics, ed. by J. H. Kagel and A. E. Roth, Princeton University Press, 587–704.

- Fishburn [1978] Fishburn, P. C. (1978): “Choice probabilities and choice functions,” Journal of Mathematical Psychology, 18, 205–219.

- Gul and Pesendorfer [2006] Gul, F. and W. Pesendorfer (2006): “Random expected utility,” Econometrica, 74, 121–146.

- Hausman and Wise [1978] Hausman, J. A. and D. A. Wise (1978): “A conditional probit model for qualitative choice: Discrete decisions recognizing interdependence and heterogeneous preferences,” Econometrica: Journal of the econometric society, 403–426.

- He and Natenzon [2024] He, J. and P. Natenzon (2024): “Moderate utility,” American Economic Review: Insights, 6, 176–195.

- Hey [2001] Hey, J. D. (2001): “Does repetition improve consistency?” Experimental economics, 4, 5–54.

- Kahneman and Tversky [1979] Kahneman, D. and A. Tversky (1979): “Prospect Theory. An Analysis of Decision under Uncertainty,” Econometrica, 47, 263–291.

- Loomes [2005] Loomes, G. (2005): “Modelling the Stochastic Component of Behaviour in Experiments: Some Issues for the Interpretation of Data,” Experimental Economics, 8, 301–323.

- Machina [1987] Machina, M. J. (1987): “Choice under uncertainty: Problems solved and unsolved,” Journal of Economic Perspectives, 1, 121–154.

- Machina [2008] ——— (2008): “Non-expected utility theory,” in The New Palgrave Dictionary of Economics, Springer, 1–14.

- Machina [2018] ——— (2018): “Non-expected utility theory,” in The New Palgrave Dictionary of Economics, Springer, 9570–9582.

- McFadden [1978] McFadden, D. (1978): “Modeling the Choice of Residential Location,” Spatial Interaction Theory and Planning Models, 75–96.

- McGranaghan et al. [2024] McGranaghan, C., K. Nielsen, T. O’Donoghue, J. Somerville, and C. D. Sprenger (2024): “Distinguishing common ratio preferences from common ratio effects using paired valuation tasks,” American Economic Review, 114, 307–347.

- Nevo [2000] Nevo, A. (2000): “A Practitioner’s Guide to Estimation of Random-Coefficients Logit Models of Demand,” Journal of Economics & Management Strategy, 9, 513–548.

- Prelec [1998] Prelec, D. (1998): “The Probability Weighting Function,” Econometrica, 66, 497–527.

- Strzalecki [2025] Strzalecki, T. (2025): “Stochastic choice theory,” Cambridge Books.

- Thurstone [1927] Thurstone, L. L. (1927): “Psychophysical analysis,” The American journal of psychology, 38, 368–389.

- Tversky [1969] Tversky, A. (1969): “Intransitivity of preferences.” Psychological review, 76, 31.

- Tversky [1972] ——— (1972): “Elimination by aspects: A theory of choice.” Psychological review, 79, 281.

- Wilcox [2011] Wilcox, N. T. (2011): “‘Stochastically more risk averse:’ A contextual theory of stochastic discrete choice under risk,” Journal of Econometrics, 162, 89–104, the Economics and Econometrics of Risk.

Appendix A Assumptions 2b and 3

Here, we provide a more elaborate example where Assumption 2b holds while Assumption 3 is violated. MNOSS define the symmetry assumption for bivariate random variables with a density. So here we provide an example that has a (strictly positive) density.

Let be a bivariate random vector defined on the support with the following joint probability density function:

Proposition 7.

The marginal distributions of and are uniform on , but Assumption 3 is violated: the property of central symmetry, does not hold.

Proof of Proposition 7.

Observe first that is a strictly positive density function on . Indeed, for and the minimum value of the term occurs when and , yielding a value of . Substituting this into the density function provides its global minimum over :

Second, we show that the marginal distributions are standard uniform. To find the marginal density of , we integrate the joint density over the support of :

Thus, . That is immediate by integrating the density.

Finally, note that

Thus, we have and the symmetry property in Assumption 3 is violated. ∎

Appendix B Biasedness of the mean valuation test

MNOSS show that, under their Assumption 2a, the mean valuation test is unbiased. Under the iAREU model, however, Assumption 2a imposes very strong restrictions on the utility function. The assumption does not hold, even in the iAREU case with errors that are additive and i.i.d. Note that the equality is equivalent to as . However, the equality cannot be satisfied unless is linear. In fact, even the weaker condition cannot generally be satisfied. For example, when is strictly concave and , we have .

Consistent with this observation, the mean valuation test is always biased when is strictly concave or strictly convex.

In order for the mean test to be unbiased, it must be that

where , under the hypothesis of additive random utility.

By the mean value theorem,

where . Unless is linear (meaning that is linear), is a non-constant random variable that depends on both and .

Hence, the mean test is theoretically valid (or unbiased) only if

Observe that for any random variables and . So for the paired valuation test to be unbiased, we require that

as by our assumption that errors are mean zero.

Our first observation is that and can be correlated, and therefore the paired valuation test biased, even when individual errors are i.i.d. and symmetric around zero. To this end, we present two simple examples, which we then generalize in Proposition 8.

Example 1.

Let and the errors be i.i.d. Note that and are independent and symmetric random variables, and there is such that (i.e., Assumption 2b is satisfied). Note that . Hence,

Consequently,

Example 2.

Let , and let are independently and uniformly distributed on . Note that and are independent and symmetric random variables, and there is such that (i.e., Assumption 2b is satisfied). Note that . Let , and . Then,

Let us generalize the above two examples.

Proposition 8.

Suppose that are i.i.d.

-

(1)

If is strictly concave, then .

-

(2)

If is strictly convex, then .

A similarly negative result is included in the online appendix to MNOSS and is mentioned in the main text of the paper.

Proof of Proposition 8.

Let and . Note that and is symmetric about zero. Therefore, is a mean-preserving spread of (which will be shown below). Hence, if is strictly concave (i.e., is strictly convex), we have

Similarly, if is strictly convex (i.e., is strictly concave), we have

Finally, let us show that is a mean-preserving spread of , equivalently, is a mean-preserving spread of , i.e., there is such that and for all For simplicity, we prove for the discrete case. Let us construct as follows: for each , is equal to with probability and with probability . Note that

Suppose that and . There are two possibilities: either or . In the first case, , so . In the second case, , so . Hence,

the last equality holds because is symmetric about zero. Hence, . ∎

Appendix C Biasedness of the sign valuation test

In this appendix, we provide further discussion on the sign valuation test. We show that the sign test can be biased under natural assumptions regarding the model of stochastic choice. We present results that complement the findings in Proposition 1, and we complete the table that was presented in the introduction.

First, we complement the “anything goes” message of Proposition 1. The proof of the second statement in the proposition assumes correlated errors. Here we show that, in the model of Equation 1, we still obtain a result in the same spirit as Proposition 1.

For simplicity, we assume that with probability 1. We construct error distributions for , , and for , , for which the sign test can be biased either in the direction of the common ratio effect or the reverse common ratio effect.

Proposition 9.

Let and . There are independent mean-zero distributions , , , and , so that if and , then

and if and , then

Remark 3.

The proof of Proposition 9 assumes errors that are degenerate, but it is easy to extend the construction to non-degenerate errors on .

Proof of Proposition 9.

Suppose that . Let be small enough that . Suppose that with probability one and let equal with probability and with probability , for . Then has mean zero. Now choose small enough that

Then with probability one, and we have the following sequence of implications:

where ; we have used that and that is strictly increasing. This means that, when for all , then we have that . But this occurs with probability .

To obtain the opposite inequality, we may choose and as before and small enough that . Define with probability and with complementary probability. Then it is easy to see that when , which occurs with probability .

An analogous construction works for the case when .

∎

C.1. Sign valuation test under Equation (1)

To prove the unbiasedness of the paired valuation sign-test, MNOSS impose assumptions that all imply . Here, we explain why this assumption is violated under the random utility model given by Equation (1). Consequently, it may be difficult to justify the model with Assumption 2 (or the assumptions behind Proposition 2 in their paper) beyond iAREU.

For expositional simplicity, let us consider the following special case of Equation (1): the random utility of a simple lottery is , where and are such that and have mean zero for all and . We do assume that for all ; otherwise, we might incur a violation of monotonicity. We consider both cases where (i) , and (ii) for , and have identical distributions. We shall also single out the case when occurs with probability 1 (i.e., ), reflecting a common assumption about probability weighting functions.

Before turning to the details, note that the utility of a lottery is now

| (4) |

which means that there is some important structure hidden behind the assumption of an additive error. Any assumption on such errors masks an underlying assumption on the model of random utility that can be hard to evaluate.

The valuation tasks give us and such that:

Hence,

where

and

Again, and are the residual terms that are fundamentally different from errors and . To provide a simple intuition for why , notice that

and

It turns out that unless , i.e., we are in the case of random expected utility of Section 2.1.4. Hence, the preference error and “perceptual,” or probability weighting, errors have to be correlated in a particular fashion so that

is satisfied. Hence, unless such knife-edge equality is satisfied, we cannot have . Let us consider the three specific cases in the following result.

Proposition 10.

Assume Equation (1).

-

(1)

If errors are independent and either for sure, or , then .

-

(2)

If (“perfect correlation”), and are independent, and or , then .

-

(3)

If (“perfect correlation”), then:

-

(a)

When , and , then .

-

(b)

When and , then .

-

(a)

In all three cases, . Moreover, if all errors are symmetric around zero, then

Remark 4.

Proof of Proposition 10.

To prove the first part, let us assume that all errors are independent. Then . Hence, we have

where we have used that by independence and mean zero. Then, since is a strictly convex function as long as , we have by Jensen’s inequality. Thus, .

When , we have . When and have identical distributions, we have

Note that . Hence, in either case, we have .

Note that implies that , i.e., the stochastic choice follows the random expected utility of Gul and Pesendorfer (2006).

To prove the second part, let us now assume that and and are independent. In this case, we still have . Hence,

Since is a strictly convex function as long as , we have by Jensen’s inequality. Hence, .

When , we have . When and have identical distributions, we have . Hence, in either case we have . Again, in this case, implies that , i.e., the stochastic choice follows the random expected utility.

To prove the third part, let us now assume that . In this case, we have

and

Hence,

Since , iff .

When , we have . Then

Hence, if , then

When , we have

and

Hence,

Since , iff . Hence, if , then

Again, in this case, implies that , i.e., the stochastic choice follows the random expected utility.

Finally, suppose now that all errors are symmetric around zero. Note that the second assumption of Proposition 5 is satisfied. Hence, we obtain the desired inequalities by Proposition 5.

∎

C.2. Prelec’s probability weighting function

Stochastic choice is often modeled by means of a random coefficients specification. See, for example, the survey by Nevo [2000] of the methodology introduced by Berry et al. [1995]. The question is whether valuation tests are unbiased when we take a random deviation from expected utility theory that is modeled through a random coefficients specification. In particular, we start from a parametric version of prospect theory [Kahneman and Tversky, 1979], and take the parameters to signify random deviations from expected utility theory.

In prospect theory, the utility of a lottery that pays with probability and with probability is when we normalize . Suppose, moreover, that utility takes the constant relative risk aversion form with a coefficient of relative risk aversion . The valuation tasks now give us:

First, we could let and model random choice by allowing to be random. The resulting model will be a special case of random expected utility, which we have already discussed.

Second, suppose instead that we take the function to be random. More specifically, suppose that it is random but “centered” on expected utility to capture random, unbiased deviations from expected utility. Let denote the random . One draw of random determines and another draw determines .

Hence, if and only if

We should emphasize here that each elicitation involves a different realization of the probability weighting function. So, is one draw, and and are obtained from a second draw of evaluated at two different points. This is important because we are going to draw the parameters of the function at random. The first draw of corresponds to one realization of the random coefficients. The second draw corresponds to a second realization.

Now suppose that takes the form proposed by Prelec [1998]. So with . When , we have expected utility. When (), we obtain the (reverse) common ratio effect.

Proposition 11.

Let be drawn from a full-support probability distribution on that is symmetric around . Suppose that .

-

(1)

If , then .

-

(2)

If , then .

In contrast, if is drawn from a probability distribution on with median , then the strong paired choice test is unbiased.

Remark 5.

Proposition 11 means that, even though the deviations from expected utility are “unbiased” in the sense of being equally likely on each side of expected utility, the valuation test gives a biased conclusion regarding the common ratio effect. We should note that the proof allows for correlated draws of the random coefficients, and that the unbiasedness of the strong paired choice test only requires that the median of is 1, not that its distribution be symmetric.

Finally, we should note that the second statement in the proposition is the most relevant case for the existing experimental literature. In 97% of the studies reported by Blavatskyy et al. [2023], it holds that . Moreover, in 10 out of 15 experimental cases of MNOSS, they have , in which the sign test is biased against the common ratio effect.

Proof of Proposition 11.

Throughout the proof, we use the notation and , and assume that (i.e., ). Note that . Under the assumptions we have made, if and only if

Note that

where is the draw relevant for and the one relevant for . Let

be the value of for which we get .

Let and and consider . Note that . Note also that the sign of equals the sign of if and only if , which occurs exactly when . For the remainder of the proof, we assume that and obtain the first statement in Proposition 11. The second statement follows by reversing the signs.

So we have that

The denominator is positive. We only need to study the numerator, .

Thus,

as . Conclude that , and therefore , is strictly concave.

Now consider a pair . If then and therefore . If then and therefore . Since and is strictly concave, its graph lies below the tangent line at . This line bisects the square . So the hypograph of is a proper subset of the area below this tangent. Thus, the area of that lies above the graph of is strictly greater than the area that lies below.

Hence, for any symmetric distribution of on , we have that the probability that is strictly greater than the probability that .

To prove the final statement regarding the strong paired choice test, let . Note that

Similarly,

We shall show that if and only if . Note that when . Hence, it is enough to show that

To prove the first equality, note that is strictly monotonic in (either increasing or decreasing). Hence, when , for all and for all . When , for all and for all . We obtain in either case.

To prove the second equality, let us first prove the following useful fact.

Fact: If is strictly monotonic on , then .

Since and is strictly monotonic, we have either for all and for all or for all and for all . Hence, we obtain .

We now consider two cases.

Case 1. .

In this case, is strictly increasing. To see this, note that . Since , we have . Hence, we obtain the desired result from the fact.

Case 2. .

In this case,

If , then is strictly monotonic on . Hence, we obtain the desired result from the fact.

We now assume . Note that it is not possible to have . If , then is strictly decreasing on . However, we have , a contradiction.

Hence, we should have . In this case, since is strictly increasing on and , we have for any and for any . Moreover, since is strictly decreasing on and , we also have for any . To sum up, we have for any and for any , which gives the desired result.

∎