Optimal Data Integration and Adaptive Sampling for Efficient Treatment

Effect Estimation

Abstract

This study addresses the challenge of estimating average treatment effects (ATEs) for advertising campaigns in online marketplaces where complete randomized experimentation is infeasible. We propose two key innovations: (1) a shrinkage estimator that optimally combines observational and experimental data without assuming smooth treatment effects across campaigns, and (2) a Bayesian adaptive experimental design framework that efficiently selects campaigns for randomized evaluation that minimizes cumulative risk. Our shrinkage estimator achieves lower risk compared to existing methods by balancing bias-variance tradeoffs, while our adaptive design significantly reduces the costs of campaign randomization. We establish theoretical guarantees including asymptotic normality and regret bounds. In an application to Amazon Ads data analyzing 2,583 campaigns, our approach achieves equivalent estimation precision while requiring only half of the randomized experiments needed by random sampling, the standard method widely used in practice today. The proposed method serves as a practical solution for marketplace platforms to efficiently measure advertising effectiveness while managing experimentation costs.

Keywords: Average treatment effects (ATE), Adaptive sampling, Online advertising, Shrinkage estimator

1 Introduction

Online marketplaces such as Amazon, AliExpress, eBay, and Etsy allow sellers to compete for advertising space to increase product exposure and sales. With online advertising comprising a substantial portion of sellers’ marketing budgets, understanding campaign effectiveness is critical. While the gold standard for estimating the ATE is a randomized experiment, running such experiments for each campaign is expensive, inefficient, and may harm the customer experience (Lewis & Rao, 2015; Gui, 2020). Conversely, large observational data are collected as a matter of course, but they may be subject to unmeasured confounding and lead leading to biased estimation. Thus, online marketplace advertising services are looking for ways of combining large observational data with experimental data collected through a small number of judiciously chosen randomized studies.

We address both the problem of how to fuse observational and experimental data and how to select which future campaigns to evaluate via randomized experiments. For the first task, we propose a shrinkage estimator of the ATE across all campaigns that is valid even when randomized study data are available for only a subset of the campaigns. We combine a regression-based de-biasing approach and shrinkage estimators to minimize risk in estimating ATEs, and derive an expression for the risk under weighted squared error loss. For the second challenge, we propose a Bayesian adaptive experimental design framework that sequentially selects campaigns for randomization. Instead of relying on arbitrary rules or simple random sampling, our approach uses Thompson sampling to balance exploration and exploitation while systematically minimizing cumulative risk.

Efficiently combining observational and RCT data is crucial for studying causal effects ’in the wild’ (Colnet et al., 2020; Degtiar & Rose, 2021). When both data sources are available, RCT data can be used for de-biasing observational estimates (Kallus et al., 2018; Yang et al., 2020). However, this involves a bias-variance trade-off: observational data have larger sample sizes but are potentially biased, while RCT data provide unbiased estimates with higher variance. Shrinkage estimators optimize this trade-off by combining these sources to minimize overall risk, such as the weighted squared error of estimated ATEs (Chen et al., 2015; Fourdrinier et al., 2018; Rosenman et al., 2020). Additionally, recent work in causal inference has explored adaptive design under limited experimental resources, such as sequential optimization for intervention effects (Dawson & Lavori, 2008; Zhang et al., 2023) and active learning for causal discovery (Toth et al., 2022). While existing designs typically focus on a single data source, our work is the first to develop adaptive experimental design methods that leverage both observational and RCT data to minimize estimation risk.

Our contributions are threefold. First, we address the practical setting of multiple concurrent interventions with spillover effects, which is common in online marketplaces where advertisers compete for space and customers see multiple advertisements. Second, we develop a unified framework that jointly considers optimal data fusion and adaptive experimental design. Finally, we establish theoretical guarantees for both components of our approach. In Section 2, we set notation and introduce our de-biased regression model. Section 3 presents our proposed methods. Section 4 shows simulation results and Section 5 illustrates the Amazon Ads application. Concluding remarks are given in Section 6.

2 Background

2.1 Notation and setup

We assume that there are binary interventions to be evaluated concurrently in each of rounds. In an online marketing application, the interventions might be the advertising campaigns for brands while the rounds are days or weeks. During each round, interventions can be independently turned ‘on’ or ‘off’ for each unit (customer, patient, etc.). In round , one source of information about the effectiveness of interventions is a large observational study

which comprises independent copies of , where: is contextual information, e.g., customer and campaign information; is intervention status with equal to one if intervention is on and zero otherwise; and is an outcome of interest. To account for unobserved confounding, denoted as , we assume intervention is determined by a function , where is an unknown mapping that needs to be estimated. Note that here we assume that the interaction between treatment assignments is fully determined by contextual information and unobserved confounders.

In addition to the observational study, we assume that in each round , we can select a subset of the interventions, , to evaluate via auxiliary randomized experiments. Suppose randomized data in round are of the form

which comprises independent copies of , where is a single intervention uniformly drawn from to be randomized in copy . The context , the outcome , and the unobserved confounder are distributed as in the observational data. The th intervention is constructed from as follows:

where is the th component of Thus, for each copy in each round , we uniformly select one intervention from to evaluate in randomized experiments, while generating all other interventions as the same process as in the observational study.

Before characterizing intervention effects, we first introduce the concept of a behavior policy. Let denote the space of probability distributions over , and define a behavior policy as a map . In other words, a behavior policy is a probability distribution over the space of intervention status conditional on inputs. Given context and confounder , under policy , an intervention is selected with probability . Let be the potential outcome under and let be the collection of all potential outcomes. For a policy , we define a collection of mutually independent random variables , independent of , such that for all . The potential outcome under a behavior policy is thus defined as

For each intervention , define as the behavior policy that turns intervention off while ensuring other interventions are generated as the same process as in the observational study. That is, we define the th component of the mapping as , . Similarly, define to be the behavior policy such that , so that the -th intervention is on while the others are generated as in the observational study. The average treatment effect in the wild (ATE-ITW) of intervention is then defined as

In the terminology of dynamic treatment regimes, might be termed the blip-to-reference with business-as-usual as the reference (Moodie et al., 2007). Let . Given any estimator of , we consider weighted squared error loss

where is a symmetric positive definite weight matrix. We aim to 1) construct an estimator of minimizing expected loss (i.e., risk), and 2) efficiently select the interventions to evaluate via randomized study in each round so as to minimize cumulative risk.

2.2 Estimation of intervention effects

Recall that denotes the intervention that is randomized in copy in round . Suppose for all , there exist some and such that . That is, assume that each intervention available for randomization by round has been selected at least once. We define the RCT estimator of as

While the RCT estimator is unbiased, using only randomized data is suboptimal for two reasons. First, it overlooks the information in the observational study, which typically has a sample size orders of magnitude larger. Second, in online marketing applications, only a small fraction of the total interventions can be evaluated via RCT study. To overcome these limitations, we leverage observational data by constructing a doubly robust estimator (DR; Funk et al. (2011)) of each . Define as the cumulative observational sample size. The DR estimator of is defined as

where is the estimated propensity score and and are regression outcome estimates of expected potential outcomes in the treatment and control groups, respectively.

Due to unmeasured confounding, might not be consistent for (Vermeulen & Vansteelandt, 2015). To de-bias these estimators, we assume each intervention is associated with a vector of attributes , ; e.g., in the context of online marketing, these attributes might characterize the nature of an advertising campaign including channel(s), brand reputation, market share, and so on. We assume that

where is a user-specified feature mapping, is an unknown parameter, and is a remainder satisfying . The proposed bias model has two important features. First, the remainder term relaxes the assumption of unbiasedness to consistency. Second, we assume smoothness only in the bias structure across , not in the treatment effects which reflects the practical reality that similar brands can have dramatically different campaign effectiveness (Kaptein & Eckles, 2012).

Let and suppose . Define the least squares estimator of as

Denote as the matrix whose -th column equals to . Under relatively mild conditions given in the Appendix, it follows that is asymptotically normal with mean zero as grows large. While consistently estimates , it has relatively higher variance compared to , due to being estimated using the (much smaller) randomized data. In the next section, we propose a shrinkage estimator that optimizes the bias-variance trade-off by minimizing weighted risk.

3 Proposed methods

3.1 Optimal shrinkage estimator

We consider estimators of of the form

| (1) |

where the dependence on , historical interventions evaluated in randomized studies, has been made explicit for convenience when we consider optimal design. When , reduces to the DR estimator , which is efficient but can be seriously biased. Conversely, when , is equivalent to the fully-de-biased estimator, , which is consistent for the oracle treatment effects but prone to high variance. The objective is to tune to minimize the estimated risk when is fixed.

To derive an optimal shrinkage estimator , we will first make use of the following Lemma derived from similar results in Strawderman (2003) and Rosenman et al. (2020) (see also Fourdrinier et al., 2018) for risk estimation.

Lemma 3.1

Suppose that and is a random vector in . Define the weighted squared error loss

where is a fixed positive definite matrix. Let be differentiable and satisfy . Then the risk of is given by

where , , and are given in the Appendix.

A proof is provided in the Appendix. Lemma 3.1 provides a closed form of risk given a weight matrix , the covariance of an estimator , and a shrinkage function . While the expression appears complex, the shrinkage estimator (1) has the required form to apply Lemma 3.1:

Here, corresponds to the fully-debiased estimator , is the DR estimator , and is the estimated bias vector shrunk by and scaled by . While our proposed shrinkage estimator resembles the approach in Rosenman et al. (2020), a key difference is our use of the debiased estimator instead of direct RCT estimates as proxies for true treatment effects. This makes our method more general since it does not require RCT estimates for all interventions, which is common in online marketing experiments where complete randomized data is rarely available. Instead, we only require at least RCT estimates. This allows us to fuse observational and RCT data even when randomized data is incomplete. In the special case where only a single intervention is considered, our estimator in (3.1) reduces to that in Rosenman et al. (2020).

We first establish the asymptotic normality of the fully de-biased estimator before proving the asymptotic normality of our proposed shrinkage estimator. Let be the asymptotic variance of and let be the asymptotic variance of . Define as the cumulative RCT sample size. The asymptotic behavior of the fully-debiased estimator is summarized in Lemma 3.2.

Lemma 3.2

Suppose that is defined as in (3.1) and assume that . Suppose . Under regularity conditions (B1)-(B4) and (C1)-(C3), it can be shown that , where

| (2) |

with given in the Appendix.

Plugging , , and specified in (3.1) and (2) into yields the risk of . Since and are unknown in practice, we replace them with their respective plug-in estimators, and . By substituting these estimators and approximating the expectation with observed realizations, we derive an empirical unbiased risk estimator (eURE) of the shrinkage estimator :

where a proof and closed forms for and are given in the Appendix. The optimal shrinkage parameter is thus defined as

The following theorem summarizes the closed form of the optimal shrinkage factor and the corresponding eURE. The proof is provided in the Appendix.

Theorem 3.1

Under weighted squared error loss with weights , the optimal shrinkage factor is given by

and the corresponding eURE is

Closed forms of and are provided in the Appendix.

3.2 Bayesian Adaptive design

We propose a Bayesian adaptive design framework for selecting interventions to be randomized in the RCT study. The goal is to sequentially identify the set of interventions at each stage such that the cumulative risk is minimized. A key challenge is that the next-stage risk function requires the plug-in covariance estimates of the RCT estimates, , which cannot be directly estimated since future randomized data has not yet been observed. To address this challenge, we introduce a Bayesian structure on , the asymptotic covariance of randomized treatment effects. We start with the case where and denote as the expected next-stage risk conditional on randomizing intervention at round , where denote the historical information up to round .

Recall that for all as different interventions are estimated using independent data. We assume a Bayesian hierarchical structure on the diagonal elements of :

where , , and are user-specified hyperparameters. In practice, the hyperparameters can be chosen to center the prior distribution around the estimated asymptotic variances of , where are the interventions randomized in the first round, while accommodating uncertainty through a larger variance. Let be the total sample size of RCT studies in which intervention was randomized by the end of round . A choice of hyperparameters is to set , so that the prior mean of is approximately the average of observed asymptotic variances of randomized treatment effects. Increasing or can lead to stronger priors, and vice versa.

A key challenge of conventional Bayesian updating in our framework is that it can fail to incorporate full information from new observations. Unlike usual posterior updates where new information consists of newly observed data points, in our context, the new information is a single asymptotic variance estimate for the -th treatment effect derived from samples. The critical point is that gives a more accurate estimate of through the additional samples collected. To properly incorporate this information, we need to consider information in two forms: the plug-in estimate and the sample size used to obtain it. Since conventional Bayesian updating would lead to a posterior that treats the new variance estimate as a single data point rather than recognizing that it contains information from data points, we propose updating the posterior of as follows:

This approach allows us to incorporate both the contribution of the samples used to estimate and its estimated asymptotic variance. The intuition is straightforward: we account for the increasing sample size by updating to , similar to how we would update to in the regular case where additional observations are directly included in the likelihood. The estimate of interest is then incorporated in the updated scale parameter as usual.

Posterior sampling is carried out as follows. After observing new estimates for some , we estimate the next-stage variances for all in two stages. First, we sample the posterior predictive of conditional on and (see Lines 1-4 of Algorithm 1). Then, we scale these posterior predictive means by the appropriate sample sizes—either if intervention is selected in round , or if not selected—to obtain the plug-in variance estimates for the next stage (Line 6 of Algorithm 1). To ensure sufficient exploration during the process, we adopt Thompson sampling (TS) for selecting optimal designs. Algorithm 1 summarizes the adaptive design framework.

While we illustrate the algorithm assuming , it can be easily extended to the case where by selecting the interventions corresponding to the smallest . In Proposition 3.1, we show that under algorithm 1, each intervention will be selected infinitely many times as , which assures the asymptotic behavior of the proposed shrinkage estimator.

Proposition 3.1

Let be a sequence of actions selected according to Algorithm 1. Suppose for some for all . Then, there exist hyperparameters such that the following properties hold:

-

(i)

Each intervention will be selected infinitely many times as , i.e. almost surely as for all .

-

(ii)

There exists such that for all .

We then establish a regret bound for the proposed TS algorithm, which is a direct result from Russo & Van Roy (2014).

4 Simulation Studies

We evaluate the performance of the proposed optimal shrinkage estimators and adaptive design strategies in this section. We consider interventions with oracle treatment effects . The outcome model for both observational and RCT studies is:

where , , and is a mapping function defined later. This setting mimics scenarios with heterogeneous variances across interventions. Regression parameters are set to be and . For notation simplicity, we drop the subscripts in the rest of the section. We generate , where , and for all . The th intervention attributes are sampled as . For the observational study, we assume that the -th intervention assignment follows a Bernoulli distribution with probability where is a mapping function and . The unobserved confounder is generated from a zero-mean Gaussian process model with the Matèrn-1/2 kernel function.

For RCT data, we sample , the intervention to be randomized in experiment at round , randomly from as described in Section 2. The -th intervention assignment in the RCT study thus follows a Bernoulli distribution with , where and are generated the same as in the observational study. In this numerical experiment, we set and

We consider standard squared error loss with identity weighting matrix , and set the sample sizes of the observational and RCT study to be and for all , respectively. We use degree-three spline regressions for the bias model and fit the propensity score model using logistic regression with spline basis functions of context . Initially, we randomly select 15 interventions to be evaluated in the RCT study, and select additional interventions for randomized evaluation at each subsequent round. For hyperparameters, we pick , and . All experiments are run on 2.5GHz Intel Xeon Platinum 8259CL CPU with 16 vCPUs and 8G RAM.

We benchmark our approach against several state-of-the-arts methods: (1) random sampling (Random), (2) D-optimal designs followed by random sampling (Dopt-R), and (3) proposed adaptive design with upper-confidence-bound algorithm (UCB). The Dopt-R approach uses D-optimal sequential designs until each intervention has been selected once, after which it shifts to random sampling since traditional D-optimal designs are not designed to repeatedly sample the same interventions. Figure 1 shows the performance of the optimal shrinkage estimator and adaptive design. First, we validate that the estimated optimal shrinkage factor (dotted line) accurately identifies the risk-minimizing value, with decreasing over rounds as RCT confidence grows. This matches our expectation, as larger RCT samples provide greater confidence in bias estimates, naturally shifting preference toward the fully-debiased estimator . The right plot of Figure 1 presents the cumulative risk across different designs and sampling methods. While D-optimal designs demonstrate strong initial performance, their efficiency diminishes after exhausting unique intervention selections. In contrast, our proposed adaptive designs achieve substantially lower cumulative risk compared to both random and D-optimal approaches, with the Thompson Sampling implementation showing particularly strong performance.

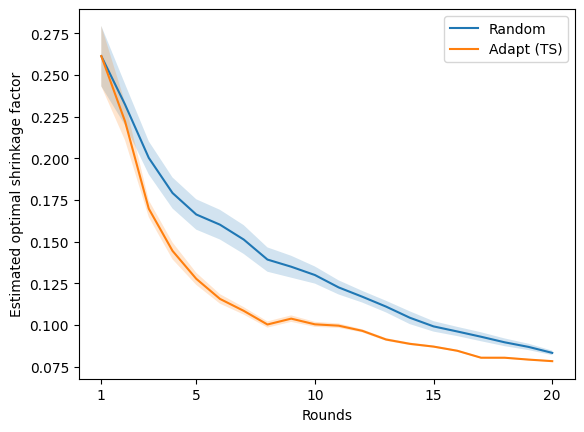

5 Application

Finally, we evaluate our proposed shrinkage estimators and adaptive sampling method using Amazon’s advertising campaign data. In collaboration with Amazon Ads ECON team, we analyze 2,583 campaigns implemented in 2024. Figure 2 provides an example of the campaigns of interest. The treatment effect of interests in this study is the change in product page view rate. RCT campaign-level treatment effects and their standard errors are estimated through a ghost-ads infrastructure (Johnson et al., 2017), while observational campaign-level effects are derived by aggregating impression-level effects from a DNN-uplift model developed by the Ads ECON team. Based on domain expertise, we identify 18 intervention attributes, including campaign types, media types, targeted product price, and targeted product views. The bias model is fit using spline regression of degree three.

In implementing our adaptive design framework, we initialize with data from 500 RCT campaigns. At each round, we select 100 campaigns for RCT evaluation in each of the 20 rounds. Since it is an offline analysis and it is infeasible to update RCT effects without additional experimental data, choosing previously-sampled campaigns for RCT evaluation will not provide new information in this analysis. Thus, we focus on change without replacement sampling scheme in this real data application. We compare our proposed method against random sampling, which represents the standard approach widely used in practice for this type of experimental design task.

Figure 3 shows the estimated optimal shrinkage factors and RCT costs versus instantaneous risk difference. Since oracle treatment effects for all treatments are unknown, we use risk difference as a proxy metric to evaluate model performance. We define risk difference as the difference between our shrinkage estimator based on RCT data from selected campaigns and an optimal benchmark estimator that uses RCT data from all 2,583 campaigns. First, we observe that the estimated optimal shrinkage factors derived using our sampling method is significantly lower than the of the random sampling, demonstrating that our approach identifies informative interventions for randomization more effectively. As increases, both estimated optimal shrinkage factors converge, which aligns with our expectation since by round 20, both methods will have leveraged nearly all 2,583 randomized campaigns. On the other hand, The right plot of Figure 3 reveals substantial cost savings that can be benefited from our method: the proposed sampling method achieves the same performance level that random sampling achieves (instantaneous risk: 0.02) while reducing the costs by approximately 50%. While these cost estimates are proportional, they indicate the significant resource savings potential of our adaptive approach. Additional cost savings are possible due to opportunity costs of impressions and unrealized incremental conversions.

6 Discussion

We proposed an optimal shrinkage estimator and adaptive sampling framework for multiple campaign effect estimation in large marketplaces, where evaluating all campaigns through RCTs is impractical. Our Bayesian adaptive design framework maximizes resource efficiency by judiciously selecting which campaigns to evaluate through RCT at each time point. Application of our method to Amazon’s advertising campaign data demonstrates substantial efficiency gains, reducing costs by approximately 50% compared to random sampling. To the best of our knowledge, this paper is the first to develop: 1) an optimal shrinkage estimator that handles missing randomized data, and 2) a sequential sampling algorithm for efficient implementation of randomized experiments.

There are several future directions worth investigating. First, allowing different shrinkage factors across interventions could improve performance by applying more shrinkage to where RCT sample variance is larger. Second, our current method assumes the de-biased model is correctly specified. While we adopt flexible feature mapping to capture nonlinear bias, the model may yield misleading results if important features are omitted. Developing a feature selection framework for the de-biased model and assessing model robustness under misspecification would therefore be valuable extensions. Finally, adapting our sampling method to account for heterogeneous intervention costs would broaden its practical applications across different marketplace settings.

Acknowledgement

The authors Yen-Chun Liu, Alexander Volfovsky, and Eric Laber acknowledge support from Amazon.

References

- Chen et al. (2015) Chen, A., Owen, A. B. & Shi, M. (2015). Data enriched linear regression. Electronic journal of statistics 9, 1078–1112.

- Colnet et al. (2020) Colnet, B., Mayer, I., Chen, G., Dieng, A., Li, R., Varoquaux, G., Vert, J.-P., Josse, J. & Yang, S. (2020). Causal inference methods for combining randomized trials and observational studies: a review. arXiv preprint arXiv:2011.08047 .

- Dawson & Lavori (2008) Dawson, R. & Lavori, P. W. (2008). Sequential causal inference: Application to randomized trials of adaptive treatment strategies. Statistics in Medicine 27, 1626–1645.

- Degtiar & Rose (2021) Degtiar, I. & Rose, S. (2021). A review of generalizability and transportability. arXiv preprint arXiv:2102.11904 .

- Fourdrinier et al. (2018) Fourdrinier, D., Strawderman, W. E. & Wells, M. T. (2018). Shrinkage estimation. Springer.

- Funk et al. (2011) Funk, M. J., Westreich, D., Wiesen, C., Stürmer, T., Brookhart, M. A. & Davidian, M. (2011). Doubly robust estimation of causal effects. American journal of epidemiology 173, 761–767.

- Gui (2020) Gui, G. (2020). Combining observational and experimental data using first-stage covariates. arXiv preprint arXiv:2010.05117 .

- Johnson et al. (2017) Johnson, G. A., Lewis, R. A. & Nubbemeyer, E. I. (2017). Ghost ads: Improving the economics of measuring online ad effectiveness. Journal of Marketing Research 54, 867–884.

- Kallus et al. (2018) Kallus, N., Puli, A. M. & Shalit, U. (2018). Removing hidden confounding by experimental grounding. Advances in neural information processing systems 31.

- Kaptein & Eckles (2012) Kaptein, M. & Eckles, D. (2012). Heterogeneity in the effects of online persuasion. Journal of Interactive Marketing 26, 176–188.

- Lewis & Rao (2015) Lewis, R. A. & Rao, J. M. (2015). The unfavorable economics of measuring the returns to advertising. The Quarterly Journal of Economics 130, 1941–1973.

- Moodie et al. (2007) Moodie, E. E., Richardson, T. S. & Stephens, D. A. (2007). Demystifying optimal dynamic treatment regimes. Biometrics 63, 447–455.

- Niemiro (1992) Niemiro, W. (1992). Asymptotics for m-estimators defined by convex minimization. The Annals of Statistics , 1514–1533.

- Rosenman et al. (2020) Rosenman, E., Basse, G., Owen, A. & Baiocchi, M. (2020). Combining observational and experimental datasets using shrinkage estimators. arXiv preprint arXiv:2002.06708 .

- Russo & Van Roy (2014) Russo, D. & Van Roy, B. (2014). Learning to optimize via information-directed sampling. In Advances in Neural Information Processing Systems.

- Strawderman (2003) Strawderman, W. E. (2003). On minimax estimation of a normal mean vector for general quadratic loss. Lecture Notes-Monograph Series , 3–14.

- Toth et al. (2022) Toth, C., Lorch, L., Knoll, C., Krause, A., Pernkopf, F., Peharz, R. & Von Kügelgen, J. (2022). Active bayesian causal inference. Advances in Neural Information Processing Systems 35, 16261–16275.

- Vermeulen & Vansteelandt (2015) Vermeulen, K. & Vansteelandt, S. (2015). Bias-reduced doubly robust estimation. Journal of the American Statistical Association 110, 1024–1036.

- Yang et al. (2020) Yang, S., Zeng, D. & Wang, X. (2020). Improved inference for heterogeneous treatment effects using real-world data subject to hidden confounding. arXiv preprint arXiv:2007.12922 .

- Zhang et al. (2023) Zhang, J., Cammarata, L., Squires, C., Sapsis, T. P. & Uhler, C. (2023). Active learning for optimal intervention design in causal models. Nature Machine Intelligence 5, 1066–1075.

Appendix A Proof of Lemmas and Theorem

Proof of Lemma 3.1

The following is a well-known result in linear algebra. We include it here along with a proof for completeness.

Lemma A.1

Suppose that and are symmetric and strictly positive definite. T hen there exists a non-singular matrix such that and , where is a diagonal matrix.

Proof:

Write , then as is also symmetric, there exists orthogonal matrix such that where is diagonal. Hence, inverting both sides, it follows that , where we have used the fact that Define . It easily verified that satisfies the desired properties, as

and

Proof:

[Proof of Lemma 3.1] Let be the Cholesky decomposition of and let be an orthogonal matrix such that , and define , where The risk associated with is

where , , and . Note that

where . Because , if we define , it follows that ; this is slight extension of Theorem 3.13 in Fourdrinier et al. (2018).

Proof of Lemma 3.2

Let and . Suppose and . The least square estimator can be represented as

where be a submatrix of consisting of the rows indexed by unique elements in , and let be with entries not indexed by replaced with zeros. Assume each intervention will be selected infinitely many times as , then

and thus

if and Since

we have

Proof of the closed form of eURE

Recall that in Lemma 3.1 we show that

where , , and Note that elements in is different from the shrinkage factor . Let , , and , so that . We first derive the closed form of . By Stein’s lemma, it is equivalent to evaluate

Define . Note that

and . Thus,

Here we use the fact that that Suppose is fixed. We therefore show that the risk of is

Replacing with and with yields

Proof of Theorem 3.1

Optimal exists since is strictly convex when . Solving yields

Plugging into and replacing expectation with realizations yield the eURE.

Proof of Proposition 3.1

Let . For notation simplicity, we denote as and as the complement event in the following proof. Before proving Lemma 3.3., we will show the following proposition.

Proposition A.1

For sufficiently large , the following inequality holds:

Proof:

Let be a positive constant and define . Recall that is the total sample size used for randomizing by the end of round . Denote the plug-in variance estimate of the next-stage estimator where is selected at round as , where is a posterior sample of the asymptotic variance of , and is a posterior sample of the hyperparameter. Then,

Recall that is the plug-in estimate of the asymptotic variance of observational ATE so that for all . Further, since is bounded with probability 1, we can simplify as

Thus, minimizing is asymptotically equivalent to minimizing and consequently, for large enough , we have

Since , we have

Define . Conditional on the events and using the fact that is a decreasing function of , we have for all and for . Recall that for all and follows a Gamma distribution with mean

We therefore show

We will now prove that occurs infinitely often, i.e. . First, note that

Since for all and , we have

where the inequality holds because for all . Thus, for all ,

The proof of Lemma 3.3 (i) is therefore complete. The second part of Lemma 3.3 is a straightforward result of law of large numbers and the consistent assumption of the debiased model.

Appendix B Consistency and asymptotic normality

Marginal logistic regression model for propensity scores

Let be a fixed feature vector, and define . For any and define . We consider a working marginal logistic regression working model for the propensity scores in the observational data of the form

where

is the usual logistic regression model, and is a vector of unknown coefficients. Note that we do not assume this model is correctly specified.

Let . Given a sample comprising independent copies of , we construct and estimator using maximum likelihood, i.e., solves

where is the empirical measure. Define to be the solution to

| (3) |

We assume (B0) that a solution to (3) exists and is unique (this assumption is mild as the loss function is strictly convex). In addition, we assume

-

(B1)

for all in a neighborhood of ;

-

(B2)

exists and is strictly positive definite.

These assumptions are quite weak. It follows from standard theory for -estimation (e.g., see Niemiro, 1992) that

where .

Asymptotic distribution of

Let be the empirical distribution on . The IPWE estimator of the th treatment effect is

Define the population analog of as

Define the first and second terms in as and , respectively. Similarly, we can define and as the corresponding terms in The estimators can be derived by solving for

| (4) |

where the last estimation equation results from the score function of the propensity score likelihood. Define . Let , and be the corresponding estimating equations in (4). We will use these estimating equations to derive asymptotic distributions of in the following sections.

We first show that converges in probability to . Assume (B3) and (B4) for in a neighborhood of and some .

Note that

Since the class of maps for in a neighborhood of is Glivenko-Cantelli, we have almost surely. In addition, we have

By assumptions (B4) and (B5) and the consistency of , we show that converges in probability to 0. Following similar arguments, we can show that the nominator converges in probability to . Thus, by Slustky’s theorem and the positivity assumption, we have Similarly, Applying Slutsky’s theorem again, we thus prove that

To show the asymptotic noramlity of the proposed estimator, we will start with the asymptotic normality of . Define for and . Let and be the values of and at , respectively. In addition to assumptions (B1)-(B3) for the asymptotics of , we assume

-

(C1)

has a unique solution at .

-

(C2)

for all .

-

(C3)

is differentiable at and is strictly positive definite for all .

By Taylor expansion, we have

where

Here is the -th block on the diagonal of , which was defined in the asymptotics of . Note that when the propensity score model is correctly specified, we have . By block matrix inverse formula, we can show that

where denotes as . Therefore,

where is the standard basis vector with -th entry being 1 and 0 otherwise. Specifically, when both propensity score and outcome models are correctly specified, the asymptotic variance of reduces to

To derive asymptotic distribution of , we assume that assumptions hold for . Following the above approach, we can derive by simultaneously solving estimating equations , where . Thus, the asymptotic distribution of is:

where

and