LR-Robot: A Unified Supervised Intelligent Framework for Real-Time Systematic Literature Reviews with Large Language Models

Wei Weia

Jin Zhenga

Zining Wanga

aSchool of Engineering Mathematics and Technology, University of Bristol, Ada Lovelace Building, Tankard’s Close, Bristol, BS8 1TW, England, United Kingdom

Corresponding author: Jin Zheng

Email: jin.zheng@bristol.ac.uk

Abstract

Recent advances in artificial intelligence (AI) and natural language processing (NLP) have enabled tools to support systematic literature reviews (SLRs), yet existing frameworks often produce outputs that are efficient but contextually limited, requiring substantial expert oversight. To address these challenges, we propose LR-Robot, a novel supervised–augmented framework that integrates expert judgment with AI capabilities to enhance literature synthesis. The framework employs a human-in-the-loop process to define sub-SLR tasks, evaluate models, and ensure methodological rigor, while leveraging structured knowledge sources and retrieval-augmented generation (RAG) to enhance factual grounding and transparency. LR-Robot enables multidimensional categorization of research, maps relationships among papers, identifies high-impact works, and supports historical, fine-grained analyses of topic evolution.

We demonstrate the framework using an option pricing case study, enabling comprehensive literature analysis. Empirical results reveal the current capabilities of AI in understanding and synthesizing literature, uncover emerging trends, reveal topic connections, and highlight core research directions. By accelerating labor-intensive review stages while preserving interpretive accuracy, LR-Robot provides a practical, customizable, and high-quality approach for AI-assisted SLRs.

Key contributions: (1) a novel framework combining AI and expert supervision for contextually informed SLRs, (2) support for multidimensional categorization, relationship mapping, and fine-grained topic evolution analysis, and (3) empirical demonstration of AI-driven literature synthesis in the field of option pricing.

keywords:

Systematic Literature Review, Large Language Models, Bibliometric Network, Knowledge Graph1 Introduction

A systematic literature review (SLR) is not merely a preparatory step in academic research but a fundamental methodological process that underpins all forms of scholarly inquiry. It serves as the intellectual foundation upon which rigorous and credible research is constructed, enabling scholars to consolidate existing knowledge, identify theoretical and methodological gaps, and position new contributions within the broader disciplinary landscape [snyder2019, webster2002]. When conducted systematically, a SLR offers both a comprehensive overview of the state of knowledge and a critical evaluation of its limitations. Conversely, insufficient or unsystematic reviews often lead to redundant, fragmented, or poorly contextualized studies that lack theoretical coherence and fail to engage meaningfully with the research frontier [boell2015]. Beyond its value for researchers, literature synthesis also plays a vital role for learners and practitioners, providing structured access to complex bodies of knowledge, supporting evidence-based understanding, and facilitating the transfer of insights across domains. In this sense, SLR serves not only as a research instrument but also as a powerful learning and knowledge integration mechanism for the wider academic and professional community.

Over the past decades, the academic publishing landscape has expanded exponentially, producing millions of new articles each year across disciplines. This explosive growth has made traditional SLR methods of relying heavily on human judgment, manual screening, close reading, classifying studies by topic, method, or contribution, and finally synthesizing the findings into coherent narratives or frameworks [okoli2015] increasingly time-consuming and cognitively demanding, often struggling to maintain completeness, timeliness, and reproducibility. As highlighted by [tsertsvadze2015], conventional expert-driven reviews can take months or even years to complete, rendering them increasingly impractical for keeping pace with rapidly evolving research domains.

In response to these challenges, numerous scholars have developed methodological innovations to make literature reviews more systematic, quantitative, and scalable. Techniques such as citation network analysis [shi2021], co-citation clustering [vsubelj2016], keyword co-occurrence and thematic clustering [lages2023], and co-authorship network analysis [donthu2021] have been widely applied to uncover structural patterns, thematic clusters, influential works, and collaboration networks within large bodies of research. Even though they offer clear advantages in scalability and objectivity, they have inherent limitations. They primarily rely on bibliometric metadata, which may overlook nuanced conceptual contributions, subtle methodological differences, and evolving semantic shifts over time [baccini2016]. Additionally, clustering results can be sensitive to parameter settings and data quality, and quantitative patterns alone cannot fully capture the depth, context, or critical appraisal that expert-driven synthesis provides [allen2009]. Consequently, while bibliometric and network-based methods provide valuable structural insights, they remain complementary to, rather than a replacement for, expert judgment in conducting comprehensive and rigorous literature reviews.

Recent advances in artificial intelligence (AI) and natural language processing (NLP) have facilitated the development of tools to assist SLR [bolanos2024]. Some studies have further proposed automated frameworks for SLR, designed to streamline the entire review process from the screening and data extraction of relevant studies to the generation of synthesized content. In these frameworks, large language models (LLMs) are typically employed to interpret user requirements, retrieve and classify relevant articles, and generate preliminary summaries or conceptual overviews based on the selected corpus [han2024, dennstadt2024, agarwal2024]. While these approaches can substantially improve the efficiency of literature synthesis, several challenges remain. First, user intent is often not clearly defined, particularly when users lack sufficient domain knowledge to formulate precise or comprehensive search criteria. This may result in overly narrow, incomplete, or even misleading document retrieval. Second, as most existing frameworks generate content solely in response to user-specified topics, they tend to overlook the need for a broader, forward-looking, and integrative synthesis of the research field. In contrast, a rigorous literature review requires situating focused topics within a comprehensive and theoretically informed understanding of the domain [snyder2019, boell2015]. Consequently, current AI-driven LR systems often produce outputs that are efficient but contextually limited, emphasizing the continuing necessity of expert supervision to ensure conceptual depth, methodological rigor, and interpretive accuracy.

To address these limitations, we have developed a supervised–augmented framework that integrates expert understanding with AI capabilities. During system development, all processes are conducted under expert supervision, with researchers validating outputs, refining prompts, and ensuring contextual and methodological accuracy. The integration of structured knowledge sources such as knowledge graphs and retrieval-augmented generation (RAG) frameworks further enhances factual grounding and transparency [meloni2023, salatino2022]. Leveraging AI’s ability to rapidly process large volumes of documents, complete classification, and perform large-scale text analysis, the system can analyze all relevant literature within a field to provide a comprehensive overview of the topics. While AI accelerates labor-intensive review stages and supports content synthesis, it is used to augment expert judgment rather than replace it. Once established, the framework enables end-users to automatically generate customized literature syntheses and targeted document selection, producing their own systematic literature reviews tailored to specific research needs.

The remainder of the paper is organized as follows. Section 2 introduces the supervised–augmented framework, LR-Robot for SLR, which standardizes a human-in-the-loop process to define sub-SLR tasks and identify the best-performing models through systematic evaluation. Section 3 presents the implementation of the human-in-the-loop process using an option pricing sample dataset. Section 4 demonstrates the comprehensive application of the framework to the entire option pricing literature, enabling detailed literature analyses, including network analysis and temporal evolution studies, which help researchers understand emerging trends, topic connections, and core directions in the field. Finally, Section 5 summarizes our conclusions and outlines directions for future research.

2 Framework: LR-Robot

2.1 Overview

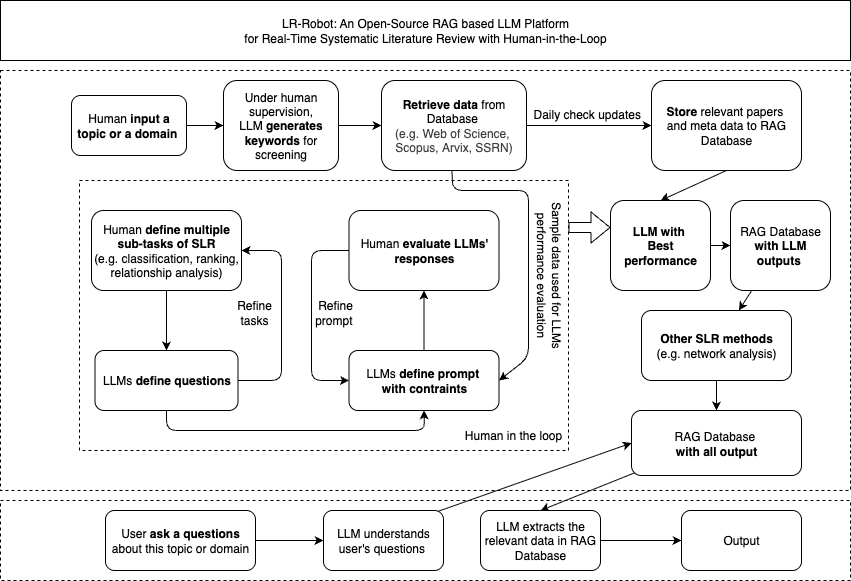

This section presents the framework (see Fig. 1) for an open-source, RAG-based LLM platform that supports real-time SLRs with human-in-the-loop supervision. The framework orchestrates data gathering, pre-processing, task definition, prompt design, model evaluation, and output synthesis, while enabling iterative refinement through human feedback. The architecture separates developer-mode operations (for task creation, data curation, and model evaluation) from user mode interactions (querying and receiving outputs).The framework comprises four layers: Data Retrieval, Human-in-the-loop Processing, RAG Database with ALL Output, and Interactive Output Visualization. The first three layers pertain to developer mode, while the fourth layer supports user mode.

2.2 Architecture and Components

2.2.1 Developer mode

Data RetrievalIn the data retrieval layer, we provide a data collection protocol capable of aggregating information from multiple sources. Initially, a query is generated from the user’s prompt to target an LLM. This prompt may specify topics, domains and research ideas. The LLM, in collaboration with a human operator, identifies keywords and automatically searches across the databases. Once the keywords are selected, the system performs daily checks for data updates and automatically stores relevant papers and metadata to our RAG databases. \bmheadHuman-in-the-loop Processing The process starts with LR-Robot formulates multiple sub-tasks of the SLR (e.g., classification, ranking, relationship analysis, data extraction, et al.) based on human instructions. It subsequently defines prompts for the tasks. A human researcher reviews and approves the LLM-generated instructions and provides more precise guidance to shape the LLM’s output, i.e. constraints in the prompt. Evaluation is conducted on a representative sample dataset, with the researcher assessing outputs for accuracy, relevance, completeness, and other predefined evaluation metrics. The evaluation loop informs refinements to the prompts to support iterative improvement. The research may also compare the performance of a variety of LLMs, and offer recommendations for the best-performing models.

RAG Database with All Outputs After identifying the best-performing models, we generated outputs across the entire dataset and stored the results in our RAG database. These aggregated outputs enable downstream SLR-related tasks—such as network analysis, topic evolution, and others—to be conducted effectively. Furthermore, the outputs are automatically updated on a daily basis to incorporate newly available data.

2.2.2 User mode

Interactive Output Visualization In the user mode, a user submits questions on the topic, and the LLM interprets these queries and extract relevant data from the RAG database. The system then generates an organized output, and the user may choose among multiple visualization options to view the results.

3 Framework Implementation and Evaluation in Option Pricing Research

3.1 Data Overview

To investigate the practical applicability of the proposed framework, we employ it to analyze the body of literature related to option pricing. We collect bibliometric data from the Scopus database, encompassing all publications related to option pricing up to April 2, 2025. The dataset includes comprehensive metadata such as article titles, author names, publication years, source titles, abstracts, and references. Both journal papers and conference papers are included to ensure broad coverage of the research landscape.111The data are retrieved using the following query: TITLE-ABS-KEY (”pric* of option*” OR ”option pric*” OR ”implied volatility” OR ”European option*” OR ”American option*” OR ”stock option*” OR ”crypto* option*” OR ”interest option*” OR ”interest rate option*” OR ”exotic option*” OR ”basket option*” OR ”barrier option*” OR ”binary option*” OR ”Bermuda option*” OR ”compound option*”) AND (LIMIT-TO (LANGUAGE, ”English”)) AND (LIMIT-TO (DOCTYPE, ”ar”) OR LIMIT-TO (DOCTYPE, ”cp”) OR LIMIT-TO (DOCTYPE, ”re”) OR LIMIT-TO (DOCTYPE, ”cr”)). This query ensure the inclusion of English-language research articles and conference proceedings relevant to option pricing and its associated domains.

The initial search yield a total of 15,424 articles from the Scopus database. After removing records with missing or incomplete bibliometric information (such as absent abstracts), 11,916 valid samples are retained for subsequent analysis. These articles are published across a wide range of journals and conference proceedings, reflecting the interdisciplinary nature of research on option pricing. The distribution of publications across source titles is illustrated in Fig.2, which presents the top 10 most frequent source titles in the dataset.

3.2 Multi-Dimensional Topic Modelling and LLMs

We select four dimensions for analyzing the option pricing problem: (1)whether pricing models are used or developed, (2) underlying types, (3) option types, and (4) model types. The dimension set is grounded in the existing literature [shrma2025, ruf2020neuralnetworksoptionpricing, broadie2004] and aims to provide a comprehensive framework for analyzing option pricing problems.

3.2.1 Option Pricing Models

In the first dimension, we classify each paper based on whether it discusses the development or comparison of pricing or volatility models. This classification is further refined by incorporating human expertise to guide the AI-based categorization. Specifically, the AI is instructed to respond “no” when a paper primarily focuses on empirical studies, market microstructure, credit risk, risk management, non-traditional markets, or other unrelated topics. The full list is in Appendix A.1.

To evaluate the performance of different LLMs, we randomly select a sample of 1,000 papers and manually labeled them. We then assess several LLMs—including GPT-4o, Gemini Flash 2.0, DeepSeek-8B, DeepSeek V3, and DeepSeek R1—based on their prediction accuracy and consistency. From the experiments, we selected the best results. A total of 417 papers were labeled by an LLM with positive classification, and we will use those 417 papers for the remaining three dimensions of analysis.

Table 1 presents the performance of each model. Each model is run three times, and the reported values are the averages of accuracy and F1 score across the runs. The rate of consistency is defined as the proportion of papers that a model assigns to the same category in all runs (i.e., no category changes across the three executions). As a result, both Gemini Flash 2.0 and DeepSeek R1 outperform in terms of accuracy and F1 score. However, Gemini Flash 2.0 shows a 5.9% higher self-consistency rate, which defined as the percentage of identical responses produced by the LLM across three runs. Therefore, we use Gemini Flash 2.0 to categorize both samples and the entire dataset for all dimensions222We further validated the results via robustness checks under several constraint configurations. Gemini Flash 2.0 provided the strongest performance across all tested settings..

We also compare the results obtained without human-in-the-loop instructions for classification (see Table 2). Across all models, we observe a decline in accuracy, F1 score, and self-consistency. This degradation suggests that incorporating human-in-the-loop guidance enables AI systems to better understand domain-specific academic concepts and make more accurate and consistent classification decisions.

| Model | Average Accuracy | Average F1 | Self-consistency |

|---|---|---|---|

| GPT-4o | 0.8273 | 0.7906 | 0.914 |

| Gemini Flash 2.0 | 0.8327 | 0.8152 | 0.947 |

| DeepSeek8b | 0.7187 | 0.7090 | 0.672 |

| DeepSeek V3 (API) | 0.7857 | 0.7010 | 0.978 |

| DeepSeek R1 (API) | 0.8403 | 0.8175 | 0.888 |

| \botrule |

| Model | Average Accuracy | Average F1 | Self-consistency |

|---|---|---|---|

| GPT-4o | 0.7110 | 0.6471 | 0.782 |

| Gemini Flash 2.0 | 0.7281 | 0.7419 | 0.905 |

| DeepSeek8b | 0.6750 | 0.6672 | 0.660 |

| DeepSeek V3 (API) | 0.6470 | 0.3418 | 0.899 |

| DeepSeek R1 (API) | 0.6837 | 0.6484 | 0.880 |

3.2.2 Option Underlying Types

In the second dimension, we classify the selected papers according to their underlying asset types. We determine whether each paper focuses on one or more common categories of underlying assets, including Stocks, Indices, Commodities, Currencies, Interest Rates, and Cryptocurrencies. Some papers, however, primarily develop mathematical frameworks (e.g., stochastic differential equation (SDE) solvers) or option pricing models (e.g., alternative assumptions for constructing SDEs) without referencing or implying any specific underlying assets. These papers are categorized as Not Specified. We allow for multi-label classification, as some studies examine multiple types of underlying assets simultaneously. The detailed prompt design is in Appendix A.2.

Using the Gemini Flash 2.0 model, we conducted both consistency and accuracy evaluations on the sample of 417 papers. As shown in Table 3, the model demonstrates high internal reliability and moderate agreement with human annotations. Specifically, the self-consistency across repeated AI responses reached 0.9517, indicating strong stability in the model’s predictions across runs. When compared with human labels, the mean Jaccard similarity between AI and human annotations was 0.8185, and the Lenient Accuracy, which measures whether the model correctly predicted at least one human-labeled category per sample, was notably higher as 0.8753. This reflects that the AI responses has good performance to match the human annotations. Regarding classification performance, the model achieved a micro-averaged F1 score of 0.8048 (Precision = 0.7490, Recall = 0.8697) and a sample-averaged F1 score of 0.8329 (Precision = 0.8158, Recall = 0.8717)333The Micro-F1 score is defined as: which computes precision and recall globally by counting all true positives , false positives , and false negatives aggregated across all classes. The Sample-F1 score, in contrast, is calculated for each sample and then averaged: where is the total number of samples, denotes the true label set for sample , the predicted label set, and is the number of correctly predicted labels for sample .. Overall, these results indicate that the AI model exhibits excellent reproducibility and robust performance in underlying asset classification.

| Metrics | Score | ||

|---|---|---|---|

| Self-consistency (AI repeatability) | 0.9594 | ||

| AI vs. Human (Mean Jaccard similarity) | 0.8185 | ||

| AI vs. Human (Lenient Accuracy) | 0.8753 | ||

| Precision | Recall | F1 Score | |

| Micro-averaged | 0.7490 | 0.8697 | 0.8048 |

| Sample-averaged | 0.8158 | 0.8717 | 0.8329 |

3.2.3 Option Types

In the third dimension, we classify the papers by option type. We group papers into topics such as European, American, and Exotic. As with the second dimension, papers that do not mention or imply any option type are labeled as “Not Specified”. Our classification relies on text mapping to assign papers.

It is noteworthy that some papers do not explicitly mention Exotic options but discuss related concepts such as Asian, Barrier, or Basket options, et al. We take all such option types into account during the text-mapping process and classify these papers as Exotic.

3.2.4 Option Model Types

In the fourth dimension, we classify the papers based on the type of option pricing model described in their abstracts. The classification framework was developed through extensive consultation involving AI-assisted analyses and expert domain discussions, resulting in eight primary categories: (1) Analytical Models, (2) Numerical Methods, (3) Multi-Factor and Hybrid Models, (4) Market Imperfections and Frictions, (5) Calibration and Model Estimation, (6) Machine Learning and Data-Driven Approaches, (7) Behavioral and Alternative Paradigms, (8) Emerging and Niche Approaches or Others. Each category encompasses more fine-grained subclasses that capture specific modeling nuances within the broader conceptual framework. The detailed prompt design and classification procedure are documented in Appendix A.3 . Given that some papers contribute to multiple modeling perspectives simultaneously, the classification adopts a multi-label scheme, ensuring that overlapping or integrative methodologies are appropriately represented.

Similarly, we also evaluate the reliability and validity of the fourth-dimension classification on the sample. Table 4 shows that the Gemini Flash 2.0 achieves a self-consistency score of 0.9472, indicating highly stable predictions across repeated runs. When compared with human annotations, the Lenient Accuracy is 0.6739 but the mean Jaccard similarity was 0.5545, suggesting a moderate level of agreement between AI-generated and human-labeled classifications but difficult to perfectly match the human annotations. In terms of classification performance, the model achieved a micro-averaged F1 score of 0.6586 (Precision = 0.5505, Recall = 0.8196) and a sample-averaged F1 score of 0.6426 (Precision = 0.5884, Recall = 0.7846). These results indicate that while the model demonstrates excellent internal consistency and strong recall performance, there remains a moderate precision gap, reflecting the inherent complexity and overlap among option pricing model categories.

| Metrics | Score | ||

|---|---|---|---|

| Self-consistency (AI repeatability) | 0.9472 | ||

| AI vs. Human (Mean Jaccard similarity) | 0.5545 | ||

| AI vs. Human (Lenient Accuracy) | 0.8657 | ||

| Precision | Recall | F1 Score | |

| Micro-averaged | 0.5505 | 0.8196 | 0.6586 |

| Sample-averaged | 0.5884 | 0.7846 | 0.6426 |

4 Comprehensive Application to Option Pricing Literature

In this section, we apply the best-performing model, refined through human-in-the-loop instruction, to the full dataset. We perform analyses, including category classifications across four dimensions, citation network analysis, and the evolution of option pricing literature, demonstrating the effectiveness and versatility of our framework.

4.1 Static Analysis

Using the best-performing prompt and LLM model, we identified 5,942 of 11,916 papers (49.86%) as focusing on pricing or volatility model development and comparison, a proportion close to our sample estimate of 41.7%. Building on this classification, subsequent analyses focused on the second through fourth dimensions, using these 5,942 papers as the target dataset.

The frequency distribution of underlying type combinations reveals several notable patterns. Table 5 shows that a majority of studies do not specify the underlying asset, addressing option pricing in general terms. Among papers with specified assets, stocks, indices, and interest rates dominate, while currencies, commodities, and cryptocurrencies are far less represented. Multi-asset studies are rare, with the most common combinations being indices + stocks and interest rates + stocks. Currencies, commodities, and cryptocurrencies appear far less frequently, likely due to their more limited representation or narrower research coverage in the literature.

| Single Label | Freq. | Multi-Label Combinations | Freq. |

|---|---|---|---|

| Not Specified | 3347 | Indices + Stocks | 261 |

| Stocks | 1144 | Interest Rates + Stocks | 57 |

| Indices | 405 | Currencies + Stocks | 30 |

| Interest Rates | 281 | Currencies + Interest Rates | 20 |

| Currencies | 161 | Commodities + Currencies + Stocks | 10 |

| Commodities | 135 | Indices + Interest Rates | 10 |

| Cryptocurrencies | 11 |

The combinations less than 10 are omitted

In addition to variations across underlying assets, the literature also exhibits diverse modeling interests with respect to option contract types, spanning both standard and path-dependent instruments. As summarized in Table 6, European, exotic, and American options occur with comparable frequencies, indicating balanced research attention across these categories. A substantial proportion of papers (36.05%) are marked as not specified, likely reflecting cases where the option type was not explicitly mentioned in the source material.

| Single Label | Freq. | Multi-Label Combinations | Freq. |

|---|---|---|---|

| Not Specified | 2142 | American + European | 368 |

| European | 1128 | European + Exotic | 296 |

| Exotic | 890 | American + Exotic | 195 |

| American | 815 | American + European + Exotic | 108 |

Turning to model classifications, Table 7 summarizes the distribution of model types in option pricing research. Given the complexity of analyzing all eight types, we focus on the proportion of each type’s occurrence, even when multiple types appear within a single paper. The results reveal that (1) Analytical Models and (2) Numerical Methods overwhelmingly dominate the literature, highlighting the enduring influence of classical mathematical and computational approaches that form the methodological core of option pricing research. In contrast, (3) Multi-Factor and Hybrid Models and (5) Calibration and Model Estimation occupy a secondary yet significant role, reflecting growing attention to empirical validation and model integration. Meanwhile, (4) Market Imperfections and Frictions, (6) Machine Learning and Data-Driven Approaches, and (7) Behavioral and Alternative Paradigms remain comparatively underrepresented, suggesting that these emerging directions are still at a developmental stage within the broader literature.

| Model Types | Occurrence | Proportion |

|---|---|---|

| (1) Analytical Models | 3956 | 66.58% |

| (2) Numerical Methods | 4038 | 67.96% |

| (3) Multi-Factor and Hybrid Models | 1682 | 28.31% |

| (4) Market Imperfections and Frictions | 373 | 6.28% |

| (5) Calibration and Model Estimation | 213 | 3.58% |

| (6) Machine Learning and Data-Driven Approaches | 1492 | 25.11% |

| (7) Behavioral and Alternative Paradigms | 377 | 6.34% |

| (8) Emerging and Niche Approaches or Others | 158 | 2.66% |

Allowing multi-label assignments in model type classification, we constructed a chord diagram (Fig. 3) to visualize co-occurrence relationships and identify the most frequently overlapping types. The strongest co-occurrences are observed between (1)&(2), (1)&(3), and (1)&(5) . The linkage between (1) and (2) indicates that analytical formulations often provide the theoretical foundation for computational implementations. The connection of (1) and (3) reflects efforts to enrich analytical frameworks with multi-factor structures capturing complex market dynamics, while the association of (1) and (5) highlights the practical importance of aligning models with empirical data. Collectively, these dominant interactions show that (1) Analytical Models remain the conceptual core of option pricing research, frequently integrated with (2), (3), and (5) types to achieve both theoretical rigor and empirical relevance.

4.2 Network Analysis

To further analyze the structural relationships within the collected literature, we constructed a citation network based on the bibliographic information of the full dataset comprising 11,916 articles. Among these, a subset of 11810 papers contained detailed reference information, which enabled the development of the citation network. In this network, each node represents an individual article, and each directed edge indicates a citation relationship from one paper to another.

Given our focus on studies specifically addressing option pricing models, and the categorization of these articles by underlying asset types, option types, and model types, we refined the citation network to include only option pricing papers as source nodes (i.e., citing papers). Target nodes (i.e., cited papers) include either other option pricing studies or works related to their applications, ensuring the network captures the intellectual linkages and citation dynamics underlying option pricing research within the broader financial modeling literature.

We applied several widely used network analysis algorithms—degree centrality [freeman1978], PageRank [page1999], and betweenness centrality [freeman1977]—to identify the most influential articles in option pricing modeling. As shown in Table 8, degree centrality and PageRank rankings are dominated by classical foundational works, notably [black1973], [heston1993], and [merton1976], reflecting their central role in shaping the theory. In contrast, betweenness centrality highlights studies that bridge theoretical, numerical, and empirical strands of research, such as [broadie2004, bakshi1997, carr2003], emphasizing computational and hybrid modeling approaches linking theory with practice.

| Rank | Degree Centrality | PageRank | Betweenness Centrality |

|---|---|---|---|

| 1 | [black1973] | [black1973] | [broadie2004] |

| 2 | [heston1993] | [heston1993] | [bakshi1997] |

| 3 | [merton1976] | [merton1976] | [carr2003] |

| 4 | [cox1979] | [cox1979] | [broadie1996] |

| 5 | [hull1987] | [cox1976] | [bates1996] |

| 6 | [longstaff2001] | [hull1987] | [boyle1997] |

| 7 | [bakshi1997] | [harrison1979] | [fang2009] |

| 8 | [kou2002] | [harrison1981] | [lord2008] |

| 9 | [bates1996] | [longstaff2001] | [kou2004] |

| 10 | [carr1999] | [merton1974] | [fang2009-2] |

Using the labels for option type, underlying type, and model type, we constructed category-specific citation networks and applied PageRank centrality to rank papers by their structural importance within each category. As shown in Table 9, this ranking successfully captures influential works across all major categories, encompassing both classical foundational studies (e.g., [heston1993], [longstaff2001]) and more recent contributions (e.g., [hutchinson1994], [amilon2003]). The inclusion of key papers across multiple categories reflects the broad recognition and impact of these studies within the option pricing literature [ruf2019, bates2022, sharma2024]. These findings are consistent with previous literature reviews in the field, which identify these works as seminal and widely cited across theoretical, numerical, and applied research on option pricing models.

| Rank | Indices as Underlying | American options | Model Type (3) | Model Type (6) |

|---|---|---|---|---|

| 1 | [bakshi1997] | [longstaff2001] | [heston1993] | [hutchinson1994] |

| 2 | [hull1987] | [heston1993] | [margrabe1978] | [yao2000] |

| 3 | [hutchinson1994] | [jaillet1990] | [heath1992] | [tsitsiklis2001] |

| 4 | [heston2000] | [geske1984] | [longstaff2001] | [garcia2000] |

| 5 | [ait1998] | [kim1990] | [ho1986] | [amilon2003] |

4.3 Topic Evolutions

To uncover the long-term evolutionary trajectory and intellectual synergies, we study the co-occurrence frequency of model-type pairs over time. Co-occurrence is defined as the frequency with which specific pairs of model types are studied together and Fig. 4 shows the cumulative frequency of co-occurrence pairs over time. We can clearly see that the co-occurrence of (1) and (2) has consistently high frequency from the 1970s to the present. This observation aligns with the reality that these two methods are cornerstones of option pricing research. We also observe an increasing co-occurrence of the pairs (1)&(5), (1)&(3), (2)&(5), and (2)&(3) starting around 1995, as multi-factor and hybrid models, and model calibration gained popularity. These approaches blended with analytical and numerical methods. This is also consistent with the findings in Section 4.2, where the paper by heston1993 is published and quickly becomes influential in this domain. (5) has a similiar pattern where most high-ranked papers are published around 1995. Another trend is the emergence of (6) as a focal point for cross‑thematic co‑occurrence from the 2010s to 2025. This aligns with the data and machine learning boom of the last decades, when many research, including in option prices, has shifted to data‑driven methodologies.

Building on the preceding network analysis of model-type co-occurrence, Fig. 5 presents the cumulative directed citation relationships among model types. The notation ‘1 → 2’ indicates that a paper labeled as model type (1) cites a paper labeled as model type (2). A prominent pattern emerges in the sustained volume of citations between (1), (2), (3) and (5). These four categories maintain relatively strong citation relationships among one another, suggesting that modern research in this field relies on a collaborative methodological ecosystem. Analytical models provide theoretical foundations that numerical methods operationalize, while multi-factor/hybrid models and calibration techniques refine these tools to reflect real-world complexity, creating a feedback loop that reinforces methodological rigor across all four areas. From the mid-2000s onward, we observe the emergence of (6), (7), and (8); these three categories have established themselves as both recipients and sources of citations. This pattern is consistent with the anticipated shift in the methodology for option pricing.

5 Conclusion

In this study, we introduced LR-Robot, a supervised–augmented framework that combines AI capabilities with human expertise to enhance systematic literature reviews. Applied to the option pricing literature, the framework demonstrated strong performance in accurately categorizing papers, mapping citation networks, identifying high-impact studies, and tracing the historical evolution of research topics. The case study illustrates LR-Robot’s ability to accelerate labor-intensive review processes while maintaining interpretive accuracy, providing comprehensive insights into both classical and emerging trends in option pricing research.

Beyond this domain, LR-Robot offers considerable potential for application in other research fields, particularly those characterized by large, complex, and rapidly evolving literature. By integrating structured knowledge and human-in-the-loop evaluation, the framework can support multidimensional analyses, uncover key contributions, and facilitate historical and thematic mapping in a wide range of disciplines. Overall, LR-Robot provides a practical, flexible, and high-quality approach for AI-assisted systematic reviews, bridging the gap between efficiency and methodological rigor.

Future research could extend the application of LR-Robot through longitudinal and cross-disciplinary studies to evaluate its generalizability and refine best practices for human–AI collaboration in literature synthesis. Expanding the framework to multiple research domains would also allow the exploration of interconnections between disciplines and the evolution of scientific knowledge across fields. Moreover, integrating LR-Robot with dynamic knowledge graphs or citation-based forecasting models could enable the identification of emerging research frontiers and the prediction of future thematic shifts.

Acknowledgements WW is supported by Individual Funding Awards, School of Engineering Mathematics

and Technology, University of Bristol.

Author Contributions All authors conceived and designed the experiments, performed the experiments, and contributed to the main manuscript as well as to the discussion and revision of the content.

Data Availability Data and code will be available upon request

Declarations

Conflict of interest The authors declare no conflict of interest.

References

Appendix A Prompt for classification

A.1 Prompt for option pricing model classification:

Please clarify whether the abstract discusses developing or comparing pricing models or volatility models. I need a response that uses only the options listed below: [Yes, No]. What is your answer? Your answer should consist solely of the item from the list and nothing else. Your answer should also follow the constraints below:

- •

You should answer No if the abstract primarily focuses on the application of option pricing, rather than the development or comparison of option pricing models themselves.

- •

You should answer Yes if the abstract focuses on methods of solving the existing option pricing or volatility model.

- •

You should answer No if the abstract is about real estate investment or real option.

- •

You should answer No if the abstract is purely about volatility and does not mention option pricing at all.

- •

You should answer No if the abstract is purely about Greeks and risk management and does not mention option pricing at all.

- •

You should answer No if the abstract is purely about hedging strategies and does not mention option pricing models at all.

- •

You should answer No if the abstract describes a application of option pricing principles to a non traditional financial market.

- •

You should answer No if the abstract is purely an empirical study testing the performance of existing, well-established option pricing models, without proposing any modifications or new solution methods.

- •

You should answer No if the abstract focuses on market microstructure related to options, such as bid-ask spreads or trading volume, without discussing model development.

- •

You should answer No if the abstract applies option pricing theory to model or predict bankruptcy or credit risk, without developing or comparing new option pricing models or solution methods.

- •

You should answer No if the abstract primarily focuses on comparing or developing volatility models without a direct focus on option pricing models or their solution methods.

- •

You should answer Yes if the abstract focuses on comparing different option pricing models, even if it involves an empirical study.

- •

You should answer No if the provided text is a list of diverse paper topics from a proceedings or collection, rather than a single abstract focused on developing or comparing pricing/volatility models.

- •

You should answer No if the abstract focuses on developing or comparing estimation methods for implied volatility surfaces, without directly developing or comparing option pricing models.

- •

You should answer No if the abstract focuses on developing or analyzing numerical methods for solving PDE used in option pricing, without directly developing or comparing option pricing models.

- •

You should answer No if the abstract applies option pricing theory to model or analyze insurance products, without developing or comparing new option pricing models or solution methods.

- •

You should answer No if the abstract applies option pricing theory to model or analyze real options or investment opportunities, without developing or comparing new option pricing models or solution methods.

- •

You should answer No if the abstract talks about cash-settled American-style options

- •

You should answer No if the abstract talks about energy markets

- •

You should answer No if the abstract talks about weather derivatives

- •

You should answer No if the abstract talks about employee stock options

- •

You should answer No if the abstract talks about vulnerable chained options

- •

You should answer No if the abstract contains the phrase ’The proceedings contain’

A.2 Prompt for option underlying types classification:

Task: Classify Underlying Asset Type. Classify the underlying asset type of options mentioned in the abstract. We have six questions for you to answer. For each question, please respond with only ’yes’ or ’no’ and nothing else.

Q1: Does this abstract specify Stocks as underlying assets?

Q2: Does this abstract specify Indexes as underlying assets?

Q3: Does this abstract specify Commodities as underlying assets?

Q4: Does this abstract specify Currencies as underlying assets?

Q5: Does this abstract specify Interest Rates as underlying assets?

Q6: Does this abstract specify Cryptocurrencies as underlying assets?

Please merge your responses to the final output as the following format {Stocks: your response for Q1, Indexes: your response for Q2, Commodities: your response for Q3, Currencies: your response for Q4, Interest Rates: your response for Q5, Cryptocurrencies: your response for Q6}.

A.3 Prompt for pricing model types classification:

Task: Classify this abstract of an academic paper into the option pricing methodology taxonomy. Please only assign up to all applicable subclass from the taxonomy. Use the exact subclass index [1.1, …,8.3] provided below and give me just a list in form of [subclass_index; subclass_index]. The taxonomy index and toxonomy are as followings:

1.1 Analytical Models: Black-Scholes Extensions

1.2 Analytical Models: Stochastic Volatility Models

1.3 Analytical Models: Jump/Discontinuity Models

1.4 Analytical Models: Regime-Switching Models

1.5 Other Analytical Models

2.1 Numerical Methods: PDE/PIDE Solvers

2.2 Numerical Methods: Monte Carlo Simulation

2.3 Numerical Methods: Lattice/Tree Methods

2.4 Numerical Methods: Transform Methods

2.5 Other Numerical Methods

3.1 Multi-Factor and Hybrid Models: Stochastic interest rates/term structure of interest rates

3.2 Multi-Factor and Hybrid Models: Stochastic dividends

3.3 Multi-Factor and Hybrid Models: Multi-asset correlation

3.4 Multi-Factor and Hybrid Models: Hybrid local-stochastic volatility

3.5 Other Multi-Factor and Hybrid Models

4.1 Market Imperfections and Frictions: Transaction costs

4.2 Market Imperfections and Frictions: Illiquidity/funding costs

4.3 Market Imperfections and Frictions: Taxes/regulation

4.4 Other Market Imperfections

5.1 Calibration and Model Estimation: Implied volatility fitting

5.2 Calibration and Model Estimation: Density recovery

5.3 Calibration and Model Estimation: Statistical calibration

5.4 Other Calibration and Model Estimation

6.1 Machine Learning and Data-Driven Approaches: Neural PDE solvers/Deep learning for pricing prediction

6.2 Machine Learning and Data-Driven Approaches: Reinforcement Learning for optimal exercise

6.3 Machine Learning and Data-Driven Approaches: ML for calibration

6.4 Other Machine Learning and Data-Driven Approaches

7.1 Behavioral and Alternative Paradigms: Utility-based pricing

7.2 Behavioral and Alternative Paradigms: Behavioral biases

7.3 Behavioral and Alternative Paradigms: Ambiguity aversion

7.4 Other Behavioral and Alternative Paradigms

8.1 Emerging and Niche Approaches: Quantum computing

8.2 Emerging and Niche Approaches: ESG-adjusted models

8.3 Others (cannot find in the previous class)