Weighted Generalized Risk Measure and Risk Quadrangle: Characterization, Optimization and Application

Abstract

Various financial market scenarios may cause heterogeneous risk assessments among analysts, which motivates the usage of the Generalized Risk Measure in Fadina et al. (2024). Effectively synthesizing these diverse assessments avoids over-relying on a single, potentially flawed or conservative forecast and promotes more robust decision-making. Motivated by this, we establish analytical characterizations of the Weighted Generalized Risk Measure (WGRM) under both discrete and continuous settings. Building upon the WGRM, we incorporate the Fundamental Risk Quadrangle (FRQ) in Rockafellar and Uryasev (2013) into the Weighted Risk Quadrangle (WRQ) and show that the intrinsic relationships among risk, deviation, regret, error, and statistics in FRQ are preserved under weighted aggregation across scenarios. Moreover, we demonstrate that certain complex risk optimization problems under the WGRM can be reformulated as tractable linear programs through the WRQ structure, thus ensuring computational feasibility. Finally, the WGRM and WRQ framework is applied to empirical analyses using constituents of the NASDAQ 100 and S&P 500 indices across recession and expansion regimes, which validates that WGRM-based portfolios exhibit superior risk-adjusted performance and enhanced downside resilience and effectively mitigate losses arising from erroneous single-scenario judgments.

Keywords: Financial Risk Management, Weighted Generalized Risk Measure, Weighted Risk Quadrangle, Portfolio Optimization, Empirical Validation.

Mathematics Subject Classification (2020): 91G70, 91G10

JEL Classification: D81, G32, G11

1 Introduction

1.1 Background and Motivation

The global financial crisis of 2008 revealed a fundamental weakness in modern risk management: risk assessments that appeared conservative in normal times proved fragile when market regimes shifted. Many highly rated financial institutions collapsed not solely due to excessive risk-taking, but because of an over-reliance on a single or a narrow set of scenarios and the unchecked confidence in singular probabilistic models. A key lesson from this episode is that financial risk is inherently scenario-dependent. In adverse markets, different analysts often arrive at different risk assessments—even when applying the same formal risk measure—since they rely on distinct data sources, data process techniques and stress scenarios. In such settings, the central question for a department manager is no longer whether a risk measure is conservative enough, but how to avoid the catastrophic losses that can result from trusting any single, potentially flawed analyst’s forecast in isolation (Cont et al., 2010; Embrechts et al., 2015).

As a response, practitioners increasingly rely on consulting and combining heterogeneous scenario analyses. Consequently, the traditional risk measures—which are typically characterized as functionals operating either on random variable spaces or, given law-invariance, on the spaces comprising their distribution functions (see Artzner et al. 1999)—are no longer adequate. It is of significance and interest to switch from single-scenario traditional risk measures to multi-scenario settings; see Kou and Peng (2016); Wang and Ziegel (2021). A recent framework in Fadina et al. (2024), the generalized risk measure (GRM), accepts two inputs: the loss variable along with a collection of admissible probability measures, which together provide a richer characterization of the underlying stochastic environment.

Under that framework, for an arbitrary measurable space , we denote by the collection of all atomless probability measures on and, for simplicity, we assume it is a compact Polish space. Correspondingly, let denote the set of all random variables defined on this space. The power set of is denoted . The formal definition of GRM in Fadina et al. (2024) is as follows.

Definition 1.

A generalized risk measure is a mapping : .

The worst-case, coherent, and robust GRMs are characterized via different sets of axioms in Fadina et al. (2024), where the worst-case one might be too conservative. Actually, the weighted aggregation form is worthy of exploration as it fully incorporates different analysts’ expertise. Motivated by this, we introduce the Weighted Generalized Risk Measure (WGRM), a principled framework designed to aggregate heterogeneous risk perspectives into a single, analytically tractable functional under both discrete and continuous settings to align with real-world risk management needs. Specifically, For any , we aim to find a probability measure that assigns weights to the elements of , satisfying and , along with for all . We formally define WGRM as follows.

Definition 2.

The mapping admits a weighted generalized risk measure (WGRM) representation if for every , such that

| (1) |

If is a discrete set, then reduces to discrete measure and is equivalent as

| (2) |

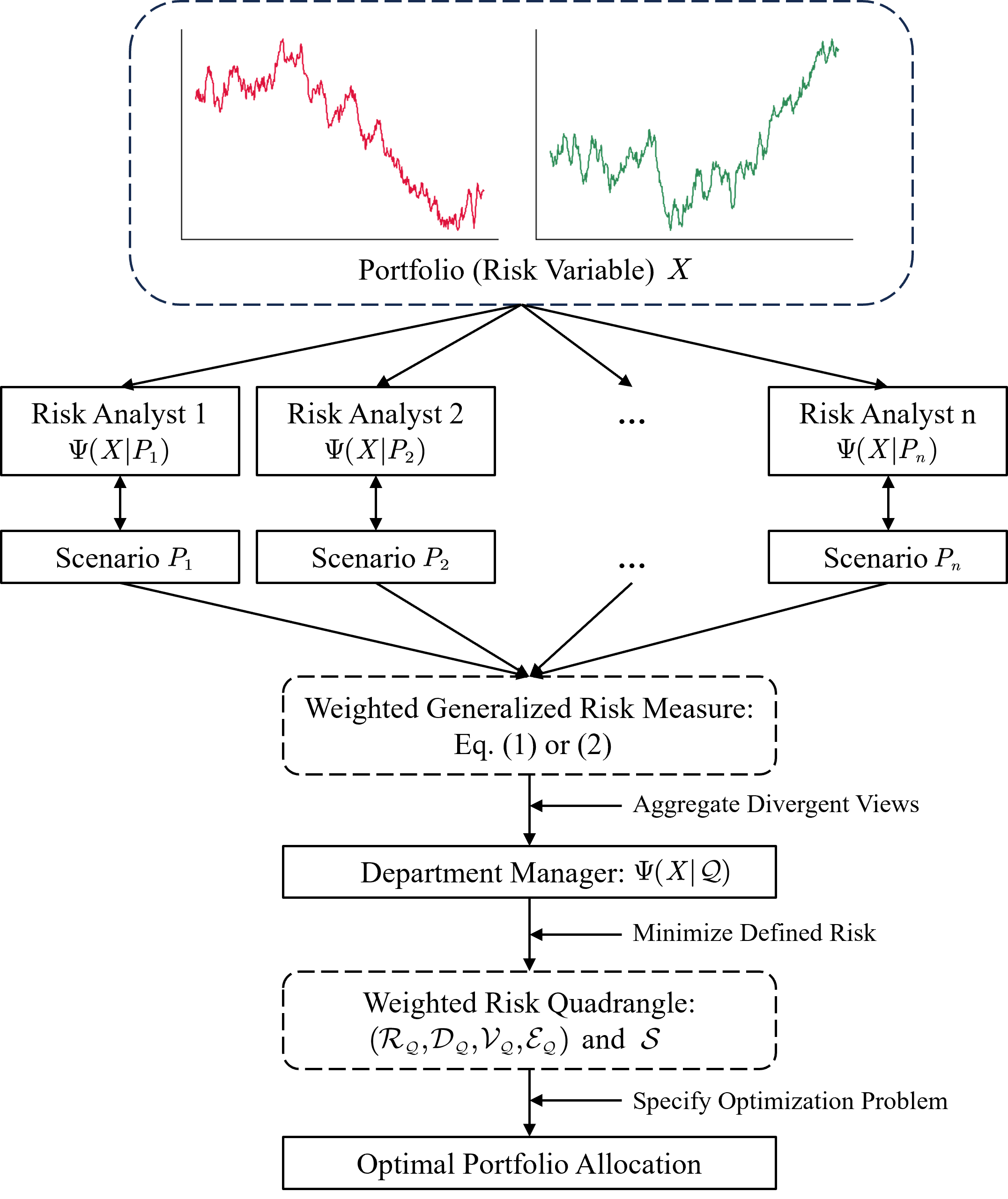

Subsequently, building on the WGRM model, we further extend the Fundamental Risk Quadrangle (FRQ), which is a framework combining optimization and estimation in risk management proposed by Rockafellar and Uryasev (2013). We use Figure 1 to briefly illustrate the FRQ with details postponed to Section 3. By leveraging the weight structure derived from WGRM, we perform a weighted aggregation of the single-probability-measure risk quadrangle to develop the Weighted Risk Quadrangle (WRQ).

Before elaborating on the theoretical framework, Figure 2 presents a specific application. Consider a department manager allocating capital across assets based on the assessments from multiple risk analysts. Even when applying a common metric like , analysts typically report divergent estimates due to distinct modeling choices and stress scenarios. These differences reflect distinct subjective probability measures each analyst adopts, collectively forming a family of probability measures . Crucially, relying on a single analyst’s estimate may expose the portfolio to idiosyncratic model bias, but also not fully make use of others’ effort and expertise. Thus, the WGRM framework serves as a structural defense to perform a weighted aggregation of the analysts’ heterogeneous assessments. The weights assigned to each analyst can be based on their historical prediction accuracy, professional competence, or other relevant criteria. Such process corresponds to assigning a weight to each probability measure . The manager then aims to minimize the aggregated risk while ensuring a predefined level of expected return. Thus, the obtained risk measure by the WGRM can be used as the objective function, which is then integrated into the WRQ. By defining relevant constraints (e.g., expected return targets, position limits) and solving the optimization problem, the manager ultimately obtains a robust asset allocation strategy. By design, this WRQ-based portfolio is inherently resilient, dampening the adverse financial consequences that would arise from relying on an isolated, incorrect market outlook.

1.2 Connection to Other Frameworks and Contribution

Our study is directly inspired by and develops the GRM proposed in Fadina et al. (2024), thus exhibiting substantial differences in both mathematical structure and methodology from traditional risk measures (e.g., Frittelli and Rosazza Gianin 2002; Föllmer and Schied 2002; Föllmer2004; Wakker 2010; Castagnoli et al. 2022). Nevertheless, Fadina et al. (2024) primarily discuss the worst-case GRM, which can be regarded as a special case of the WGRM in this paper under certain regularity conditions. This generality gives rise to disparities in mathematical treatments. Conceptually, our framework requires to accommodate information within each probability measure, whereas the worst-case one relies more on extreme scenarios; see also Gilboa and Schmeidler (1989); Zhu and Fukushima (2009); Zymler et al. (2013); Adrian and Brunnermeier (2016); Liu and Wang (2021); Chen et al. (2022); Blanchet et al. (2025).

While another analogous framework also accounting for multiple scenarios is the scenario-based risk measure in Wang and Ziegel (2021), they are fundamentally distinct in nature. Specifically, their framework, under the assumption of mutually singular probability measures, emphasizes model uncertainty other than heterogeneous assessments, whereas our framework focuses on the weight structure, particularly on how convex weights are derived. This critical difference leads to distinct methodological treatments, resulting in no overlap in research scopes or analytical approaches. Other similar weighted aggregation frameworks appear in Klibanoff et al. (2005); Brutti Righi (2018); Jokhadze and Schmidt (2020); however, these works lack a systematic theoretical characterization of the weight structure itself.

For recent advances in risk measure theory, we refer to Bellini and Bernardino (2017); Wang and Zitikis (2021); Fissler and Pesenti (2023); Bernard et al. (2024); La Torre and Rocca (2024); Gomez et al. (2024); Battiston and Rimella (2025); Cai et al. (2025). Our goal is to provide a comprehensive discussion of the weight structure inherent to the GRM framework; as such, this work may enable further synergistic integration with the aforementioned strands of research, laying groundwork for more comprehensive and context-aware risk management paradigms.

The contributions of this paper include the following aspects. Our primary contribution is that, building upon the foundational work of Kou et al. (2013); Kou and Peng (2016), Section 2 establishes analytical characterization of the WGRM framework under both discrete and continuous scenario settings. This dual formulation accommodates the diverse analytical demands of real-world risk management applications. This work represents a crucial deepening of the GRM theory, complementing the worst-case structure that the GRM initially focuses on. Furthermore, we analyze the specific conditions under which the aggregation weights can be uniquely determined. By focusing on the weighting structure itself, the WGRM achieves broad generality, seamlessly adapting to the heterogeneous individual risk measures utilized in the aggregation process.

It must be emphasized that the weighted aggregation of separate risk assessments is distinct from evaluating a single risk measure under a pre-aggregated probability distribution. The latter excessively smooths inherent risk volatility, an information loss that adjusting quantile parameters or other ad hoc modifications cannot adequately offset.

Our second key contribution, detailed in Section 3, is to introduce the WRQ by extending the FRQ via the proposed WGRM weighting structure. This extension provides an integrated framework that theoretically unifies risk management, optimization, and statistical estimation in multi-scenario settings. While existing literature typically enhances FRQ by aggregating single-measure components with varying parameters, as noted earlier, heterogeneity across distinct scenarios and probability measures remains a more critical dimension to address for practical risk management. WRQ inherently integrates risk management and portfolio optimization in a cohesive, theoretically consistent manner. Accordingly, in Section 4, we elaborate on the embedded optimization problems within WRQ, as well as how to transform complex risk-minimization problems using WRQ’s components.

Finally, an empirical validation is provided in Section 5, where we use NASDAQ 100 and S&P 500 data to compare portfolio performance with and without WGRM (and WRQ) across expansion and recession regimes, and conduct sensitivity analyses. Our results validate that WGRM-based portfolios exhibit superior risk-adjusted performance and pronounced downside resilience, effectively mitigating adverse consequences caused by isolated, erroneous market judgments.

2 Weighted Generalized Risk Measures

2.1 Properties and Technical Discussions

In this section, we examine the conditions under which the WGRM representation exists. To begin with, we recall several properties of a GRM : from Fadina et al. (2024) to facilitate a preliminary comparison between the worst-case GRM and WGRM.

The measure is called standard if . When it is a single scenario case, the measure takes the form of : . Clearly, the explicit inclusion of as an input generalizes traditional risk measures. When is restricted to a singleton set (i.e., for some ), this generalized risk measure reduces to its traditional counterpart. The worst-case GRM satisfies the following properties.

(A1) Scenario monotonicity: if holds for every , then .

(A2) Scenario upper bound: holds for every and .

(A3) Uncertainty aversion: for every and .

For a WGRM , properties (A1) and (A2) are intuitively justified. Property (A1) holds due to the monotonicity of the integral: . And property (A2) is derived from .

However, property (A3) is rarely satisfied by most of WGRMs but aligns more closely with the worst-case one. The defining characteristic of (A3) is that risk evaluation is monotonically non-decreasing with respect to expanding the scenario set. This monotonicity may induce excessive conservatism in risk assessment. Intuitively, if posterior scenarios incorporate more favorable states, the aggregate risk measure should exhibit a non-increasing trend rather than a non-decreasing one. This is why the characterization of the WGRM is worth being investigated.

Remark 1.

While the codomain of is formally defined as , alternative specifications such as or are both theoretically admissible. However, from a practical standpoint, risk measures with finite values are generally more interpretable and operationally meaningful in financial applications.

Remark 2.

We require that is a compact Polish space, which is a simplified technical assumption made for clarity of exposition. The collection of all atomless probability measures on can be endowed with topologies (e.g., the topology of weak convergence, provided that supports a metric making it a Polish space) under which it forms a Polish space. However, itself is generally not compact in these natural topologies. For instance, consider with the Borel -algebra. The sequence of atomless measures , where is the uniform distribution on the interval , typically lacks a convergent subsequence within under weak convergence; the probability mass escapes to infinity. Nevertheless, we can always restrict attention to a suitable compact subset containing the relevant scenario sets under consideration. Examples include families of atomless measures defined by bounded likelihood ratios with respect to a reference atomless measure (e.g., for some and ) or parametric families of atomless measures (e.g., with compact parameter spaces ).

Critically, since is an arbitrary subset of which may be either discrete or continuous, these two cases exhibit different mathematical structures and must be discussed separately. We first examine the case where is discrete.

2.2 WGRM under a Discrete Setting

In the discrete case where is finite, e.g., of size , our focus is on the Euclidean space . For notational simplicity, we present as a vector, i.e., . Let , which is a translation-invariant and closed convex cone. And denote by the interior of . Let be the whole weight set in . Let denote the inner product on . For a function , we define its domain as and is said to be proper if .

When is finite, we can index its elements as . Generally, the GRM can be constructed through an aggregation function that combines all individual risk measures under each , i.e.,

For simplicity, we define . Thus, the above can be expressed as . To be a satisfactory aggregation function, is expected to satisfy several properties (Kou et al., 2013; Kou and Peng, 2016):

(B1) Positive homogeneity and translation invariance: . Here, .

(B2) Monotonicity: , if , where is understood component-wise, i.e., , for all .

(B3) Comonotonic sub-additivity: whenever and are comonotonic, i.e., for any .

(B4) Permutation invariance: for every , where is the set of all permutations of and is therefore the corresponding permuted vector.

(B1) indicates that is robust to affine transformation. (B2) is equivalent to (A1) scenario monotonicity. A direct observation is that, under (B1) and (B2), is Lipschitz continuous with respect to the maximum-norm , ensuring stability under small perturbations of risk inputs. (B3) is also a common assumption which focuses on the co-movement consistency across two risk inputs. (B4), though less frequently stated in literature, is intuitive for risk aggregation, as the overall risk measure should be invariant to the ordering of individual evaluations.

Remark 3.

One might argue that (B1) should be , where is a fixed constant related to each aggregation function . However, since here is designed for weighted-averaging individual risk measures, it is reasonable to impose the invariance of aggregating constant values, i.e., .

The assumption of (B3) comonotonic sub-additivity holds practical relevance in real-world data contexts. For instance, if each component of represents an individual risk measure under a specific market scenario, the risk measures of correlated assets across a family of coherent scenarios often exhibit comonotonicity. Nevertheless, the comonotonicity constraint is not sufficiently elegant for a general risk structure. If we instead require the aggregation function to satisfy full sub-additivity (unrestricted to comonotonic vectors), it will impose more stringent conditions on the resulting weights. Formally, we write

(B3’) Full sub-additivity: for any .

We first propose the following characterization result on worst-case WGRM, where we technically get inspired from Ahmed et al. (2008).

Theorem 1.

(1) The aggregation function satisfies (B1)-(B4) if and only if there exists a closed convex set of weights , such that

| (3) |

where is the vector of order statistics obtained by sorting the individual risk assessments into non-decreasing order.

(2) The aggregation function satisfies (B1), (B2), (B3’) and (B4) if and only if there exists a closed convex set of weights , such that

| (4) |

Remark 4.

The key distinction between Parts (1) and (2) in Theorem 1 lies in the origin of convexity. Under full sub-additivity, the aggregation function inherently possesses convexity, whereas under comonotonic sub-additivity, convexity is induced by restricting the domain to due to . Specifically, considering the setting in Theorem 1, for any with components , the closed and convex nature of guarantees the existence of a weight vector that achieves the supremum of . If we suppose is not non-decreasing, then there exist indices such that . Define as the weight vector obtained by swapping the -th and -th components of . Clearly, still belongs to . However, direct calculation yields

This implies , which contradicts the definition of as the supremum-achieving weight. Nevertheless, this contradiction does not directly indicate that , since the swapped vector may not belong to in the first place.

The above theorem provides a formal representation of via a linear weighting of individual risk assessments . However, it should be noted that the weighting vectors in this representation are not uniquely determined. More precisely, the weights depend functionally on the input risk vector , exhibiting variability as changes. While this theoretical formulation possesses mathematical elegance, the state-dependent nature of the weights may present practical implementation challenges. Consequently, we shall introduce additional structural constraints to enhance the stability and applicability of the weighting scheme.

(B6) Comonotonic additivity: whenever and are comonotonic, i.e., for any .

(B6’) Full additivity: for any .

(B6) transforms the (B3) comonotonic sub-additivity into comonotonic additivity and (B6’) transforms the (B3’) full sub-additivity into full additivity at the expense of weakening the convexity of the function. The rationality behind this transformation is that the sub-additivity should be represented in rather than in to avoid overemphasizing the diversification effects. In other words, this aligns with scenarios where hedging effects are primarily captured within the individual risk measures rather than the aggregation process. (B6) and (B6’) necessitate the linearity of , which enables us to apply the Riesz Representation Theorem to attain unique weighting vectors .

Proposition 1.

(1) The aggregation function satisfies (B1), (B2) and (B6) if and only if there exists a unique weighting vector , such that

(2) The aggregation function satisfies (B1), (B2), (B4) and (B6) if and only if there exists a unique weighting vector , such that

(3) The aggregation function satisfies (B1), (B2) and (B6’) if and only if there exists a unique weighting vector , such that

(4) The aggregation function satisfies (B1), (B2), (B4) and (B6’) if and only if

where .

2.3 WGRM under a Continuous Setting

The results for the discrete case cover a vast majority of practical applications. However, in situations where the number of distinct individual risk measures requiring aggregation is substantial, or the scenarios under consideration become exceedingly numerous, the elements in may proliferate toward infinity. In such asymptotic regimes, the existing framework is no longer adequate. Therefore, we are motivated to discuss the WGRM structure in the continuous case. Nevertheless, due to the significant differences between two settings, we begin by establishing the basic framework for the continuous version of WGRM.

In such setting, we assume to be a closed subset of . Let be a fixed atomless Borel probability reference measure on . By the isomorphism theorem for standard probability spaces, there exists a measure-preserving bijection , where denotes the Lebesgue measure on . This isomorphism allows us to transfer the analysis from the abstract space to a concrete interval . Define the scenario risk functional as

| (5) |

which directly maps points in to the corresponding single-scenario risk evaluations. The quantile function (or non-decreasing rearrangement) of is defined as

| (6) |

Previously, in the discrete case, the finite number of scenarios ensures bounded risk vectors. However, in the continuous setting, to ensure the mathematical robustness of the aggregation function, we assume that the scenario risk functional remains bounded. As a common practice, we consider the space . Consequently, the aggregation function is defined as a mapping , satisfying . By restricting the domain to , we avoid a pathological behavior such as non-integrability of the scenario risk functional , thereby guaranteeing the existence and integrability of the quantile function. Note that if , then as well, with .

Also, the aggregation function is expected to satisfy the following properties under the continuous case. These properties are not totally different, but are the counterparts in a continuous context of (B1) to (B4).

(C1) Affine invariance: , , , , where is an indicator function over interval .

(C2) Pointwise monotonicity: if . Here, means for almost every .

(C3) Comonotonic sub-additivity: whenever are comonotonic, i.e., for almost every .

(C4) Strong permutation invariance: holds for any measure-preserving transformation with respect to the Lebesgue measure , i.e., for any Lebesgue measurable set .

Similar to the discrete case, we can also transform (C3) comonotonic sub-additivity into (C3’) full sub-additivity, which yields non-decreasing weighting measures as shown in the following result.

(C3’) Full sub-additivity: , for any .

But unfortunately, relying solely on conditions (C1)-(C4) does not directly yield the infinite-dimensional extension of Theorem 1. While these parallel properties ensure a reasonable behavior for standard risks, they fail to exclude pathological functionals known as Banach limits (purely finitely additive measures). Consequently, we propose introducing a non-trivial condition to filter out these pathological instances.

(C5) Fatou property: For any sequence such that , we have .

In Theorem 2 below, condition (C5) is explicitly invoked in Part (1) but omitted in Part (2), since the Fatou property is automatically satisfied under the assumptions of Part (2) (see Theorem 2.2, Jouini et al. (2006)). Based on these considerations, we formally state the following theorem.

Theorem 2.

(1) The aggregation function on satisfies (C1)-(C5) if and only if there exists a closed convex set of density such that

| (7) |

(2) The aggregation function on satisfies (C1), (C2), (C3’) and (C4) if and only if there exists a closed convex set of density such that

| (8) |

One may question the expressions in Theorem 2 differ from our original definition in Eq.(1). Despite formal differences, they are essentially equivalent. For any density function with a.e. and , we can define an absolutely continuous probability measure on by

for any Lebesgue measurable set Conversely, by the Radon-Nikodym Theorem, for any probability measure on satisfying , where denotes the Lebesgue measure, there exists a unique (up to a.e. equivalence) density function with a.e. such that

for any Lebesgue measurable set This establishes a bijective correspondence (up to a.e. equivalence) between non-negative density functions integrating to and absolutely continuous probability measures on . Now we define two sets of absolutely continuous probability measures:

where denotes the space of non-negative finite measures on . By the bijective correspondence established above, we have

Then for any or , and for any , we have

This allows us to reformulate Theorem 2 within the framework of measure-theoretic integration.

Proposition 2.

(1) The aggregation function on satisfies (C1)-(C5) if and only if there exists a closed convex set of measures such that

(2) The aggregation function on satisfies (C1), (C2), (C3’) and (C4) if and only if there exists a closed convex set of measures such that

Recall that in the discrete setting, replacing (comonotonic) sub-additivity with (comonotonic) additivity guarantees the uniqueness of the weights via the Riesz Representation Theorem. A natural question arises: Can the weighting density in the continuous setting also be unique in this way? Unfortunately, the answer is not straightforward. Unlike the discrete case, working within presents a topological hurdle. Its dual space is not , but rather , which includes pathological purely finitely additive measures. Consequently, a standard application of the Riesz Representation Theorem on does not yield a unique weighting density function.

To secure uniqueness within the framework, one would typically need to impose additional constraints—such as -continuity (see property (D5) below)—to force the functional to behave like an functional, thereby allowing it to be extended to the space. However, rather than navigating this circuitous route of constraining an functional to mimic the behavior, we find it more mathematically natural to directly shift the underlying domain to . This approach may be of greater interest as accommodates a broader class of risk profiles.

Define the set . For any , its quantile function is defined as in Eq.(6). We examine the following properties under this new setup.

(D1) Affine invariance: for all , , , where is an indicator function over interval .

(D2) Pointwise monotonicity: if almost everywhere on , i.e., for almost every .

(D3) Comonotonic additivity: whenever and are comonotonic, i.e., for almost every .

(D3’) Full additivity: for all .

(D4) Strong permutation invariance: for any Lebesgue measure-preserving transformations , i.e., for any Lebesgue measurable set , where denotes the Lebesgue measure.

(D5) continuity: There exists a constant such that for all .

Based on these properties, we present the following results.

Proposition 3.

(1) The aggregation function satisfies (D1), (D2), (D3), and (D5) if and only if there exists a unique density function such that

(2) The aggregation function satisfies (D1), (D2), (D3), (D4), and (D5) if and only if there exists a unique density function such that

(3) The aggregation function satisfies (D1), (D2), (D3’), and (D5) if and only if there exists a unique density function such that

(4) The aggregation function satisfies (D1), (D2), (D3’), (D4), and (D5) if and only if

which implies almost everywhere on .

3 Weighted Risk Quadrangle

WGRM offers a wide range of potential applications. In this section, however, we concentrate specifically on how it extends the Fundamental Risk Quadrangle framework introduced in Rockafellar and Uryasev (2013). We begin with a detailed explanation of this foundational quadrangle. Several examples are then provided to illustrate the form and implications of WGRM within the expanded quadrangle framework. Although slight notational or presentational variations may occur across different settings, for consistency we adopt the expression given in Eq.(1) throughout this section, regardless of the discreteness or continuity of the scenario or the uniqueness of the weighting measure .

3.1 Fundamental Risk Quadrangle Overview

Recall that an overview of the FRQ is illustrated in Figure 1. Starting from the upper-left corner of the quadrangle, denotes a measure of risk, which quantifies the overall risk inherent in a random variable (representing loss or cost) by assigning it a numerical value. Such measures are frequently employed in the constraints of optimization problems or used as the objective function. For a constant , the implicit constraint implied by the uncertain condition can be replaced by the explicit inequality . This substitution leverages a concrete numerical metric to offset the uncertain outcomes, thereby eliminating the uncertainty associated with and yielding a well-defined constraint.

Formally, we define as a regular measure of risk if is a closed convex functional with values in ; for any constant , we have , i.e., the risk of a deterministic cost equals itself; for any non-constant random variable , we have , i.e., the risk measure exhibits risk aversion by assigning a value greater than the expected loss of a non-deterministic .

In the upper-right corner of the quadrangle, denotes a measure of deviation, which quantifies the nonconstancy, i.e., uncertainty inherent in the random variable . Classic examples include the variance and standard deviation. Formally, a regular measure of deviation is defined as a closed convex functional taking values in such that for any constant , we have , while for any non-constant random variable , it holds that . Notably, symmetry is not imposed as a general requirement. In other words, deviation measures where may be of greater interest in practical applications, since downside risk is somewhat always more annoying than upside risk.

In the lower-left corner of the quadrangle, denotes a measure of regret, which quantifies the dissatisfaction associated with the potential outcomes—positive, zero, or negative. Formally, a regular measure of regret is defined as a closed convex functional with values in that satisfies ; and for any non-zero random variable , it holds that .

Regret measures are naturally connected to utility measures , another central concept in decision-making under uncertainty. Specifically, if is viewed as a loss, then corresponds to a gain, and the two concepts are interconvertible through the relation . Equivalently, if denotes a gain, the inverse conversion holds: .

In the lower-right corner of the quadrangle, denotes a measure of error, which quantifies the nonzeroness of a random variable. Formally, a regular measure of error is defined as a closed convex functional with values in that satisfies , and for any non-zero random variable ; moreover, for any sequence of random variables , if , then we have .

In estimation problems, particularly in regression where a loss random variable is approximated by a function of other random variables, serves as a metric to evaluate the magnitude of the prediction error , thereby assessing the quality of the estimation. As with , asymmetric measures of error, where , often warrant greater attention.

| (9) | ||||

| (10) | ||||

| (11) | ||||

| (12) |

The four corner elements of the quadrangle are not independent; rather, they interact and are interconnected through Eqs.(9)–(12). Specifically, it is noted in Figure 1 that bidirectional arrows connect the risk measure to the deviation measure , and the regret measure to the error measure —their conversion relations are given by Eqs.(9) and (10), respectively. In contrast, there is no direct equivalent conversion relation between and , nor between and ; instead, these pairs are linked through , the statistic located at the center of the quadrangle.

Concretely, for a given error measure and random variable , we seek a constant that minimizes . The minimum value attained by this error measure is exactly the deviation measure of , and the constant that achieves this minimum is precisely the statistic of , with for any . This relationship is reflected in the right-hand segments of Eqs.(11) and (12). The relationship between and follows the same logic, as illustrated in the left-hand segments of Eqs.(11) and (12).

For expositional brevity, we refer to the five quantities (i.e., , , , , and ) in Figure 1 that satisfy Eqs.(9)–(12) a quadrangle quartet associated with the statistic . If the four measures (i.e., , , , and ) within this quartet are all regular, we term this structure a regular quadrangle quartet. In what follows, our primary focus will be on regular quadrangle quartets.

3.2 Weighted Risk Quadrangle

While the quadrangle framework ingeniously integrates the five quantities into a unified structure, it suffers from a notable limitation that it is confined to various measures defined under a single probability measure. With the advancement of risk management technologies and the growing complexity of real-world stochastic environments, this single-measure setting has become restrictive. Thus, in this subsection, we build on the WGRM proposed earlier to further expand this quadrangle framework, which is denoted as Weighted Risk Quadrangle (WRQ), enabling it to accommodate multi-measure and multi-scenario risk modeling.

To avoid notational confusion, we denote the measures of the original FRQ under a single probability measure as , while using to represent the corresponding measures within WRQ under a family of probability measures. Leveraging the results from Section 2, we naturally adopt the proposed WGRM as the risk measure in the WRQ. Specifically, . Under the weight defined, the risk quadrangle can be extended to a multi-scenario setting.

Prior to this extension, we first observe that the relationships in Eqs.(9)–(12) also need to be extended to a multi-scenario context. In the original framework, the expectation operator plays a crucial bridging role. However, in the multi-scenario setting, this operator should also be extended to a multi-scenario expectation, defined as . Then we can carry out a parallel generalization of Eqs.(9)–(12) in the multi-scenario context as follows.

| (13) | ||||

| (14) | ||||

| (15) | ||||

| (16) |

The expansion implied by Eqs.(13)–(16) requires theoretical justifications. Inspired by the Mixing Theorem by Rockafellar and Uryasev (2013), we further propose the following theorem.

Theorem 3.

Under the weighting measure defined within , let denote a regular quadrangle quartet with statistic for each . A muti-scenario quadrangle quartet with statistic is generated by

| (17) | ||||

where is a functional on .

So far, we have presented the theorem formulation of the WRQ. Next, we provide several relevant examples. Notably, due to the equivalent conversion relationships in Eqs.(13) and (14), as long as we know one of and , and one of and , we can derive the entire quartet . We can then further obtain via Eq.(15), thereby constructing the complete quadrangle.

Example 1.

Value-at-Risk (VaR, or quantile) and Expected Shortfall (ES, or Conditional VaR/CVaR) are both common tail-based risk metrics that have gained substantial significance in modern risk management frameworks (Basel Committee on Banking Supervision, 2019; McNeil et al., 2015). However, the latter is often preferred over the former because it accounts for tail risk and satisfies coherency. Thus, in this example, for each , we set , where denotes the -level Expected Shortfall of under probability measure . For the error measure, we adopt the Koenker-Bassett error with appropriate adjustments to ensure that it projects to the desired . Specifically, we define , where and . Using the conversion relations in Eqs.(13)–(16), we can derive the remaining quantities of the single-measure quadrangle: , , and . Leveraging Theorem 3, we immediately obtain the corresponding WRQ:

For appropriately chosen values of the -level, each individual quadrangle quartet corresponding to a single probability measure is regular. Thus, the resulting multi-scenario quadrangle quartet is also regular.

Remark 5.

Notably, in Example 1, neither nor is necessarily symmetric. This asymmetry inherits from the single-measure components. The operator in preserves the asymmetry of asymmetric distributions. For any random variable , it holds that , which shows that in general, thus directly introducing asymmetry into . Additionally, the single-measure error measure assigns distinct weights to the positive and negative parts of ; specifically, a weight of to and a weight of to . This weighted distinction between and inherently makes asymmetric. Crucially, this asymmetry carries over to the weighted aggregation.

4 Optimization under WGRM and WRQ

This section presents a discussion on the connection between the WGRM, the WRQ, and optimization problems. In a typical optimization setting, the random variable , representing loss, generally depends on a decision vector , where denotes the feasible region. The objective is to determine an optimal decision vector within that optimizes an objective function involving . While the above theoretical framework accommodates both discrete and continuous scenarios, discrete scenarios are predominant in most practical optimization applications. Consequently, Eq.(17) can be reformulated for a discrete set as follows.

A straightforward observation is that the expressions for and are inherently minimization problems. While the proof of Theorem 3 directly indicates that , which in turn allows us to derive an explicit expression for , practical implementation may favor numerical solutions via linear programming. This is particularly advantageous when confronting issues such as the complexity and nonlinearity of the individual functional , which makes linear programming more computationally tractable. Specifically, under a regular WRQ, each is a closed convex functional. Then there exists a family of linear functions , where and denotes an index set, such that . Thus, when is linear in , by introducing auxiliary variables , the optimization problem in can be transformed into the following linear program:

| s.t. | |||

Another set of optimization problems inherent to the WRQ is encapsulated in Eq.(15). Taking the relationship between and as an example, a typical risk management optimization problem might aim to minimize with respect to the decision vector . Notably, leveraging the key relation , the constraint for any is equivalent to the existence of some such that . Consequently, the original objective function is equivalent to , which can be further transformed using the linear programming result above. Namely:

| (18) |

Example 2.

We present here an application of Eq.(18) in portfolio management (Zhu and Fukushima, 2009; Behera and Kumar, 2025). It is assumed that there are financial assets in the market, with their returns denoted by random variables () and corresponding expected values . We can thus use to represent their potential losses. Our goal is to determine the optimal investment weights for each assest by incorporating the heterogeneous assessments of analysts on financial assets. The total loss of the portfolio can be expressed as .

Following the approach in Example 1, we adopt as the portfolio risk metric (see Basel Committee on Banking Supervision (2019)). Each analyst forms a view on the probability distribution of based on their own insight, leading to the individual risk measure . Due to differences in analysts’ experience, professional competence, historical performance, and other factors, their perspectives are assigned different weights by the department manager. The corresponding optimization problem is therefore to select the optimal asset allocation weights that minimize the portfolio’s ES, given a target expected portfolio return (denoted by ). The objective function of this problem can be written as:

| (19) |

However, directly solving (19) using the relation requires a complete estimation of the cumulative distribution function, which is generally unavailable. Notably, within the risk quadrangle, the regret measure corresponding to the risk measure is . This regret measure, for each Analyst , can be estimated using a series of historical data (), specifically as . Thus, by introducing auxiliary variables , this optimization problem can be transformed into the following linear program:

| (20) | ||||

| s.t. | ||||

Remark 6.

It is worth noting that in Example 2, the specific reflection of each analyst’s subjective probability measure lies in the selection of historical data when estimating . This estimation relies on empirical average, where the choice of historical data encodes the analysts’ perspectives on future market dynamics. Particularly, the length of the time horizon reflects Analyst ’s view on the differences between historical and future market conditions. A longer indicates a belief that historical patterns are more representative of future trends without much structural change, while a shorter signals a perception of greater market divergence from the past. Meanwhile, the selection of specific historical return data embodies an analyst’s judgment on potential future market cycles (e.g., expansion, recession, or stability). For instance, if an analyst believes the future will be characterized by high growth and low inflation without huge structural changes to fundamental market conditions, they will select return data from historical periods with similar macroeconomic contexts and adopt a longer time horizon.

5 Empirical Study

In this section, we illustrate the methodology introduced in Example 2 and apply it to the stock market. Using real-world examples, we conduct a discussion on the advantages and limitations of portfolio optimization leveraging the WGRM and WRQ. Specifically, we select constituent stocks of the NASDAQ 100 Index as the underlying assets, compare portfolio returns under different optimization methods with the index return across both expansion and recession market conditions, and subsequently perform sensitivity analysis by varying model parameters. The data used in this study are publicly available and were retrieved from https://finance.yahoo.com.

5.1 Empirical Setup

We assume there are 4 analysts () with heterogeneous assessments in future macroeconomic trends. Based on their outlooks, each analyst estimates stock returns and informs stock selection in the portfolio, resulting in four distinct scenarios (Scenarios 1–4). The department manager integrates these four analysts’ assessments to make the optimal investment decision. Analyst 1 expects future interest rates to rise. Thus, when using historical data to estimate expected stock returns, they select periods where interest rates exceeded the median within the observation window, yielding estimated expected returns . Analyst 2 anticipates future interest rates to fall, so they use data from periods where interest rates were below the median to estimate expected returns, denoted by . Analyst 3 and Analyst 4 focus primarily on inflation, emphasizing the impact of real economic fluctuations on stock prices. Thus, Analyst 3 predicts rising inflation, with corresponding expected returns denoted by , while Analyst 4 predicts falling inflation, with expected returns . For this study, we use the U.S. 10-year Treasury bond yield as the interest rate proxy since its maturity is more aligned with that of stocks, and use the CPI for inflation measurements. For each analyst , the corresponding portfolio optimization problem is formulated as:

| (21) | ||||

| s.t. | ||||

The manager integrates the four analysts’ assessments, so their expected stock returns are a weighted aggregation of the analysts’ estimates, i.e., . For simplicity, we assign equal weights to each analyst’s perspective, i.e., , adopting a purely synthetic lens to evaluate the framework. Thus, the manager’s optimization problem is exactly the one formulated in Eq.(20).

To conduct a comprehensive assessment, we examine two distinct market regimes, recession and expansion respectively, to evaluate how the manager using the integrated multi-scenario approach performs compared to individual analysts relying on single-scenario frameworks. For the ES metric, we adopt the commonly used level . During February and March 2025, the NASDAQ 100 Index experienced a sharp decline, with a cumulative two-month return of . Although this episode reflects market turbulence rather than a macroeconomic recession, we refer to it as a recession regime for terminological convenience. For this scenario, we use a total time window of trading days, spanning from August 23, 2024, to March 31, 2025, and split the data into a training set and a backtesting set using February 1, 2025, as the cutoff date. The target return is set to the average daily return of January 2025, calculated as . We construct portfolios using weights estimated from the training set, evaluate their performance using backtesting set data, and compare the results to the actual NASDAQ 100 Index return.

In contrast, September and October 2025 saw robust growth in the index, with a cumulative two-month return of , designated as the expansion regime. Following a consistent methodology, we again use a 150-trading-day time window (May 12, 2025, to October 30, 2025), splitting the data at September 1, 2025, into two sets. The target return is the average daily return of August 2025, computed as , while all other parameters remain identical to the recession regime.

We use these two regimes as benchmark cases, and then conduct sensitivity analysis by adjusting key model parameters to test the framework’s robustness. Specifically, within each regime, we modify the time window to and trading days, adjust the ES level to and , scale the target return by a factor of 2 and 0.5, and finally replace the underlying assets from NASDAQ 100 constituents with S&P 500 constituents.

Intuitively, since ES explicitly accounts for tail risks, ES-based portfolios exhibit inherent robustness. While this conservative focus on downside protection may moderate returns during market expansions, it should deliver superior resilience during recessions to the broader index. Furthermore, the manager’s equal-weighted aggregation of conflicting scenarios (i.e., opposing views on interest rates and inflation) achieves a form of view diversification. This prevents overexposure to any single bullish forecast, effectively mitigating the idiosyncratic risk of an isolated misjudgment and lowering overall portfolio volatility. Therefore, to comprehensively evaluate the portfolios beyond raw two-month returns, we incorporate annualized Sharpe and Sortino ratios. By explicitly penalizing total and downside volatility, these metrics properly align with our focus on tail-risk mitigation. The one-year U.S. Treasury yield (3.65%) serves as the risk-free rate.

5.2 Baseline Results

Table 1 presents the baseline results. During the recession regime, all ES-based portfolios demonstrate excellent downside resilience by delivering positive returns despite a substantial index decline. Although Analyst 1 achieves the highest raw return, the manager’s portfolio yields the highest annualized Sharpe and Sortino ratios, generating the highest risk-adjusted return per unit of risk. This indicates the robustness of the WGRM-based portfolios during market distress. In the expansion regime, the inherent conservatism of ES optimization causes all portfolios to underperform the strongly rallying index. Crucially, however, while Analyst 1’s isolated forecast results in a negative return, the manager’s portfolio maintains moderate profitability and mid-tier risk-adjusted performance. This outcome directly underscores the method’s inherent trade-off: while the WGRM-based approach may lag during aggressive market expansions, it excels in distressed markets by providing robust downside protection and structurally buffering against the idiosyncratic risk of a single erroneous forecast.

Recession regime Expansion regime Portfolio Two-month return Sharpe ratio Sortino ratio Two-month return Sharpe ratio Sortino ratio Analyst 1 5.98% 2.574 4.387 -2.81% -1.893 -2.610 Analyst 2 1.85% 0.713 1.355 3.93% 1.533 3.514 Analyst 3 4.27% 1.895 3.890 6.93% 3.307 5.224 Analyst 4 4.56% 1.723 2.584 1.67% 0.432 0.671 Manager 5.71% 2.809 5.336 3.28% 1.665 2.857 Index two-month return -11.86% 10.58%

Figure 3 visualizes the daily portfolio returns across both market regimes. The manager’s portfolio exhibits lower volatility than any single analyst’s strategy. By avoiding extreme return fluctuations and structurally reducing both the frequency and magnitude of deep drawdowns, the WGRM-based method confirms its distinctly conservative and downside-protective risk profile.

5.3 Sensitivity Analysis

In this subsection, we conduct a sensitivity analysis to ensure our baseline findings are not artifacts of specific parameter choices. Table 2 reports portfolio performance under alternative time windows ( and ). During the recession regime, the manager’s portfolio is more noticeably dragged down by Analyst 2’s misjudgment than in the baseline; crucially, however, it still significantly outperforms Analyst 2’s isolated strategy. In the expansion regime, the integrated portfolio maintains mid-tier performance similar to the baseline case at but underperforms at .

Remark 7.

Varying time windows induces performance fluctuations due to the bias-variance tradeoff inherent in historical data estimation: shorter windows increase estimation variance, whereas longer windows may incorporate outdated market fundamentals. However, our primary goal here is not to evaluate the absolute robustness of ES itself, but rather to verify whether the manager’s WGRM-based approach consistently maintains its structural advantage across diverse parameter specifications.

Recession regime Expansion regime Portfolio Two-month return Sharpe ratio Sortino ratio Two-month return Sharpe ratio Sortino ratio Panel A: Change time window to Analyst 1 8.38% 2.910 5.480 9.85% 3.396 5.061 Analyst 2 0.71% 0.059 0.094 10.08% 4.321 9.064 Analyst 3 3.91% 1.675 3.529 6.93% 3.307 5.224 Analyst 4 5.64% 1.515 2.680 19.26% 5.974 16.135 Manager 3.00% 1.266 2.695 7.42% 3.960 7.586 Panel B: Change time window to Analyst 1 5.20% 2.388 4.290 -2.02% -1.518 -2.208 Analyst 2 -1.29% -0.748 -1.079 2.27% 0.841 1.420 Analyst 3 4.68% 2.154 3.653 3.92% 2.067 3.239 Analyst 4 3.56% 1.172 1.937 1.24% 0.288 0.503 Manager 0.26% -0.161 -0.285 -1.16% -0.913 -1.292

Table 3 reports the results when the ES level is adjusted to and . The manager’s portfolio performs consistently with the baseline, except for notable underperformance during the expansion regime at . The observed underperformance might be attributed to excessive conservatism. This heightened risk aversion likely leads the optimization process to over-allocate to low-volatility, defensive assets. Such assets tend to underperform in bull markets, as they fail to capture the strong upward momentum typically associated with growth-oriented stocks during economic expansions.

Recession regime Expansion regime Portfolio Two-month return Sharpe ratio Sortino ratio Two-month return Sharpe ratio Sortino ratio Panel A: Change level to Analyst 1 1.30% 0.363 0.686 1.01% 0.223 0.324 Analyst 2 1.42% 0.435 0.884 11.43% 5.960 12.281 Analyst 3 0.04% -0.270 -0.534 9.70% 5.252 10.859 Analyst 4 4.63% 1.757 2.523 2.43% 0.853 1.515 Manager 2.63% 1.078 2.153 8.01% 4.579 9.388 Panel B: Change level to Analyst 1 6.70% 2.715 5.529 -2.78% -1.866 -2.565 Analyst 2 -0.19% -0.382 -0.869 3.70% 1.256 2.546 Analyst 3 6.96% 2.977 6.180 9.91% 5.073 11.733 Analyst 4 4.56% 1.723 2.584 0.27% -0.138 -0.216 Manager 7.88% 3.927 7.604 -2.62% -1.471 -2.618

Table 4 displays the results with target returns scaled by 0.5 and 2. The manager’s portfolio aligns with the baseline except during the expansion regime with a doubled target, unexpectedly posting a negative return while all individual analysts remain profitable. This counterintuitive result highlights the tension between aggressive return targets and the WGRM framework’s mandate for risk mitigation. Pressured to pursue outsized gains in a market already exceeding historical averages, the integrated method’s requirement to balance heterogeneous assessments structurally prevents over concentration in high-momentum assets. Consequently, the optimizer defaults to less volatile, value-oriented stocks, which inherently lag in a momentum-driven bull market.

Recession regime Expansion regime Portfolio Two-month return Sharpe ratio Sortino ratio Two-month return Sharpe ratio Sortino ratio Panel A: Change target return to Analyst 1 7.68% 3.156 5.752 3.83% 1.370 2.160 Analyst 2 1.18% 0.285 0.497 7.89% 2.326 5.134 Analyst 3 7.11% 2.501 5.829 18.24% 5.470 8.988 Analyst 4 4.52% 1.876 3.623 2.92% 0.914 1.495 Manager 7.98% 3.568 7.228 -1.70% -0.937 -1.367 Panel B: Change target return to Analyst 1 6.70% 2.715 5.529 -1.49% -1.114 -1.407 Analyst 2 -0.16% -0.369 -0.837 1.80% 0.507 0.840 Analyst 3 8.74% 3.811 7.434 8.23% 4.998 9.160 Analyst 4 4.56% 1.723 2.584 0.71% 0.037 0.052 Manager 7.47% 3.762 7.699 7.24% 3.814 6.165

Table 5 replicates the baseline and sensitivity analyses using S&P 500 constituents. Outcomes consistently match, and occasionally surpass, the initial findings. In several cases (e.g., Panels A, D, E, and G), during the recession regime, the manager’s portfolio maintains a positive return even in instances where every individual analyst’s strategy incurs losses. This demonstrates the resilience of the WGRM framework across different asset universes. Furthermore, compared to the tech-heavy NASDAQ 100, the broader sectoral coverage of the S&P 500 inherently introduces more defensive and value-oriented stocks. This expanded asset base provides more options for diversification, and also confirms that the WGRM method’s structural robustness is not asset-specific, highlighting its superior adaptability to diverse market segments.

Recession regime Expansion regime Portfolio Two-month return Sharpe ratio Sortino ratio Two-month return Sharpe ratio Sortino ratio Panel A: Benchmark case Analyst 1 -1.84% -0.839 -1.089 4.28% 2.409 4.745 Analyst 2 -0.06% -0.430 -0.704 3.20% 1.212 2.196 Analyst 3 -2.11% -1.461 -2.023 7.86% 4.332 5.640 Analyst 4 -4.20% -1.893 -3.147 4.39% 1.876 3.361 Manager 0.44% -0.144 -0.186 3.44% 1.427 3.011 Panel B: Change time window to Analyst 1 1.03% 0.163 0.237 7.55% 2.923 4.936 Analyst 2 -1.04% -3.781 -6.903 10.76% 4.608 7.351 Analyst 3 -0.90% -0.571 -0.905 7.86% 4.332 5.640 Analyst 4 -10.43% -2.578 -4.340 8.28% 2.750 4.637 Manager 0.09% -0.429 -0.529 8.73% 4.934 7.010 Panel C: Change time window to Analyst 1 0.67% 0.038 0.055 3.14% 1.278 1.881 Analyst 2 -1.99% -1.556 -2.499 1.39% 0.378 0.769 Analyst 3 -0.14% -0.336 -0.497 5.55% 3.139 4.103 Analyst 4 -2.03% -1.407 -2.443 4.37% 2.037 4.150 Manager -0.19% -0.401 -0.662 3.65% 1.724 4.287 Panel D: Change level to Analyst 1 -1.84% -0.839 -1.089 4.28% 2.409 4.745 Analyst 2 -0.06% -0.430 -0.704 4.71% 1.856 3.117 Analyst 3 -2.11% -1.461 -2.023 7.86% 4.332 5.640 Analyst 4 -4.20% -1.893 -3.147 3.98% 2.009 4.771 Manager 0.64% 0.069 0.088 3.88% 1.919 4.769 Panel E: Change level to Analyst 1 -1.84% -0.839 -1.089 4.28% 2.409 4.745 Analyst 2 -0.06% -0.430 -0.704 3.20% 1.212 2.196 Analyst 3 -2.11% -1.461 -2.023 7.86% 4.332 5.640 Analyst 4 -4.20% -1.893 -3.147 4.39% 1.876 3.361 Manager 0.44% -0.144 -0.186 2.48% 0.893 1.566 Panel F: Change target return to Analyst 1 -1.84% -0.839 -1.089 7.38% 2.843 5.052 Analyst 2 -0.06% -0.430 -0.704 2.19% 0.504 0.722 Analyst 3 -2.03% -1.367 -1.903 4.85% 2.335 3.202 Analyst 4 -4.20% -1.893 -3.147 3.04% 0.837 1.174 Manager -2.20% -1.548 -2.140 6.27% 1.664 3.766 Panel G: Change target return to Analyst 1 -1.84% -0.839 -1.089 2.35% 1.238 2.270 Analyst 2 -0.06% -0.430 -0.704 6.17% 2.744 6.208 Analyst 3 -2.11% -1.461 -2.023 7.86% 4.332 5.640 Analyst 4 -4.20% -1.893 -3.147 3.70% 1.556 3.736 Manager 1.58% 0.739 0.947 3.30% 1.417 3.635

In summary, our empirical findings confirm that WGRM-based portfolios exhibit greater conservatism and robustness. While this framework may not generate outstanding raw returns in expansion regimes due to its inherent focus on downside protection, it consistently delivers superior resilience during recessions. Most crucially, it acts as a structural buffer, neutralizing the idiosyncratic risk of isolated misjudgments and preventing the severe consequences of over-relying on a single, flawed market outlook.

Acknowledgements

YL acknowledges financial support from the National Natural Science Foundation of China (Grant No. 12401624), The Chinese University of Hong Kong (Shenzhen) University Development Fund (Grant No. UDF01003336) and Shenzhen Science and Technology Program (Grant No. RCBS20231211090814028, JCYJ20250604141203005, 2025TC0010) and is partly supported by the Guangdong Provincial Key Laboratory of Mathematical Foundations for Artificial Intelligence (Grant No. 2023B1212010001). YW acknowledges financial support from the Natural Sciences and Engineering Research Council of Canada (RGPIN-2023-04674, DGECR-2023-00454), and the start-up fund at Carleton University. YW thanks The Chinese University of Hong Kong (Shenzhen) for the kind hospitality during her visit in 2025.

References

- CoVaR. American Economic Review 106 (7), pp. 1705–41. External Links: Document, Link Cited by: §1.2.

- A note on natural risk statistics. Operations Research Letters 36 (6), pp. 662–664. External Links: ISSN 0167-6377, Document, Link Cited by: §2.2.

- Coherent measures of risk. Mathematical Finance 9 (3), pp. 203–228. External Links: Document, Link, https://onlinelibrary.wiley.com/doi/pdf/10.1111/1467-9965.00068 Cited by: §1.1.

- Minimum capital requirements for market risk. Standard Bank for International Settlements, Basel, Switzerland (en). External Links: Link Cited by: Example 1, Example 2.

- Disclosure risk assessment with bayesian non-parametric hierarchical modelling. Statistics and Computing 35 (5), pp. 158. External Links: ISSN 1573-1375, Document, Link Cited by: §1.2.

- Optimizing mean conditional value-at-risk portfolios through deep neural network stock prediction. Engineering Applications of Artificial Intelligence 161, pp. 112198. External Links: ISSN 0952-1976, Document, Link Cited by: Example 2.

- Risk management with expectiles. European Journal of Finance 23 (6), pp. 487–506. External Links: Document, Link, https://doi.org/10.1080/1351847X.2015.1052150 Cited by: §1.2.

- Robust distortion risk measures. Mathematical Finance 34 (3), pp. 774–818. External Links: Document, Link, https://onlinelibrary.wiley.com/doi/pdf/10.1111/mafi.12414 Cited by: §1.2.

- Convolution bounds on quantile aggregation. Operations Research 73 (5), pp. 2761–2781. Cited by: §1.2.

- A theory for combinations of risk measures. arXiv e-prints, pp. arXiv:1807.01977. External Links: Document, 1807.01977 Cited by: §1.2.

- Distributionally robust optimization under distorted expectations. Operations Research 73 (2), pp. 969–985. External Links: Document, Link, https://doi.org/10.1287/opre.2020.0685 Cited by: §1.2.

- Star-shaped risk measures. Operations Research 70 (5), pp. 2637–2654. External Links: Document, Link, https://doi.org/10.1287/opre.2022.2303 Cited by: §1.2.

- Ordering and inequalities of mixtures on risk aggregation. Mathematical Finance 32 (1), pp. 421–451. Cited by: §1.2.

- Robustness and sensitivity analysis of risk measurement procedures. Quantitative Finance 10 (6), pp. 593–606. External Links: Document, Link, https://doi.org/10.1080/14697681003685597 Cited by: §1.1.

- Aggregation-robustness and model uncertainty of regulatory risk measures. Finance and Stochastics 19 (4), pp. 763–790. External Links: Document, Link Cited by: §1.1.

- A framework for measures of risk under uncertainty. Finance and Stochastics 28 (2), pp. 363–390. External Links: ISSN 1432-1122, Document, Link Cited by: §1.1, §1.1, §1.1, §1.2, §2.1.

- Sensitivity measures based on scoring functions. European Journal of Operational Research 307 (3), pp. 1408–1423. External Links: ISSN 0377-2217, Document, Link Cited by: §1.2.

- Convex measures of risk and trading constraints. Finance and Stochastics 6 (4), pp. 429–447. External Links: ISSN 0949-2984, Document, Link Cited by: §1.2.

- Putting order in risk measures. Journal of Banking & Finance 26 (7), pp. 1473–1486. External Links: ISSN 0378-4266, Document, Link Cited by: §1.2.

- Maxmin expected utility with a non-unique prior. Journal of Mathematical Economics 18, pp. 141–153. Cited by: §1.2.

- Multi-period portfolio selection with interval-based conditional Value-at-Risk. Annals of Operations Research. External Links: ISSN 1572-9338, Document, Link Cited by: §1.2.

- Measuring model risk in financial risk management and pricing. International Journal of Theoretical and Applied Finance 23 (02), pp. 2050012. External Links: Document, Link, https://doi.org/10.1142/S0219024920500120 Cited by: §1.2.

- Law invariant risk measures have the fatou property. In Advances in Mathematical Economics, pp. 49–71. External Links: ISBN 978-4-431-34342-4, Document, Link Cited by: Proof of Theorem 2., §2.3.

- A smooth model of decision making under uncertainty. Econometrica 73 (3), pp. 1849–1892. Cited by: §1.2.

- External risk measures and basel accords. Mathematics of Operations Research 38 (3), pp. 393–417. External Links: Document, Link, https://doi.org/10.1287/moor.1120.0577 Cited by: §1.2, §2.2.

- On the measurement of economic tail risk. Operations Research 64 (5), pp. 1056–1072. External Links: Document, Link, https://doi.org/10.1287/opre.2016.1539 Cited by: §1.1, §1.2, §2.2.

- Distributionally robust multiobjective optimization with application to risk measure theory. Annals of Operations Research. External Links: ISSN 1572-9338, Document, Link Cited by: §1.2.

- A theory for measures of tail risk. Mathematics of Operations Research 46 (3), pp. 1109–1128. External Links: Document, Link, https://doi.org/10.1287/moor.2020.1072 Cited by: §1.2.

- Quantitative risk management: concepts, techniques and tools. Revised edition edition, Princeton series in finance, Princeton University Press, Princeton Oxford (eng). External Links: ISBN 9780691166278 Cited by: Example 1.

- The fundamental risk quadrangle in risk management, optimization and statistical estimation. Surveys in Operations Research and Management Science 18 (1), pp. 33–53. External Links: ISSN 1876-7354, Document Cited by: Figure 1, Figure 1, §1.1, §3.2, §3.

- Convex analysis. Princeton University Press, Princeton. External Links: Link, Document, ISBN 9781400873173 Cited by: Proof of Theorem 2., Proof of Theorem 1..

- Prospect theory: for risk and ambiguity. Cambridge University Press. Cited by: §1.2.

- Scenario-based risk evaluation. Finance and Stochastics 25 (4), pp. 725–756. External Links: ISSN 1432-1122, Document, Link Cited by: §1.1, §1.2.

- An axiomatic foundation for the expected shortfall. Management Science 67 (3), pp. 1413–1429. External Links: Document, Link, https://doi.org/10.1287/mnsc.2020.3617 Cited by: §1.2.

- Worst-case conditional value-at-risk with application to robust portfolio management. Operations Research 57 (5), pp. 1155–1168. External Links: Document, Link, https://doi.org/10.1287/opre.1080.0684 Cited by: §1.2, Example 2.

- Worst-case value at risk of nonlinear portfolios. Management Science 59 (1), pp. 172–188. External Links: ISSN 00251909, 15265501, Link Cited by: §1.2.

Appendix: Proofs

Proof of Theorem 1.

The “if” statement can be checked directly. We only focus on the “only if” statement.

(1) Step 1: Dual representation via an auxiliary convex function. We first define an auxiliary function:

| (22) | ||||

| (23) |

Obviously, on . Since satisfies (B1)-(B2), it is easy to verify that also satisfies positive homogeneity, translation invariance, and monotonicity. Moreover, we can further verify that is also sub-additive, i.e., , for any . Note that if , then the inequality is valid by the comonotonic sub-additivity of . If or , then the right-hand side of Eq.(22) goes to infinity due to . The positive homogeneity and sub-additivity indicate convexity of . Furthermore, since , we have , i.e., is proper. From the fact that is Lipschitz continuous with respect to the maximum-norm and is a closed convex set, is lower semi-continuous (l.s.c.). By Fenchel-Moreau Biconjugation Theorem (Chapter 12, Rockafellar (1970)), it holds that

| (24) |

where , , for , is the dual function of .

Step 2: Structure of the conjugate and characterization of the weight set. Next we investigate the characteristic of . First, since , , by translation invariance, we have

If , i.e., , we have . Alternatively, if , i.e., , we have , since is arbitrary. This indicates that is non-negative and that . Second, by positive homogeneity,

for arbitrary . This indicates that if , it must hold that . Combining the above two claims, we can conclude that

| (25) |

where the second equation of (25) yields from the fact that, when , we have , implying that .

Define the set of maximizers at of Eq.(24) as , i.e., . It can be shown that , . Now, fix any and let . From Eq.(25), we know that holds. Let be the canonical basis of . Since , for each , there exists an small enough such that . Note that is an element of , but it does not necessarily indicate as well. Therefore, we have

| (26) |

where the second inequality of (26) results from monotonicity of . Equivalently, , i.e., , , which indicates that all coordinates of are non-negative. Since is l.s.c. (as is l.s.c.), the set is closed and convex. To sum up, so far we have obtained that

Step 3: Extension to the boundary and final representation. For any boundary point of , we could choose a sequence converging to . Then by the Lipschitz continuity of and the fact that on , we have . Finally, since is permutation invariant and for every , we have

(2) Since now is assumed to be sub-additive, it is directly convex along with properties of positive homogeneity, translation invariance, and monotonicity. From Part (1), we immediately have

where

and . We first note that for any , and , there exists a unique inverse permutation (since permutations are bijections) for permuted such that . Therefore, it is evident that

| (27) |

The second equality of (27) is valid due to the permutation invariance of , i.e., . The above relationship implies that is also permutation invariant. Moreover, since , where is non-decreasingly ordered, the Rearrangement Inequality implies that the supremum would be attained when is also non-decreasingly ordered. Therefore, . ∎

Proof of Proposition 1.

The “if” statement is direct. We only focus on the “only if” statement.

(1) Proof for satisfying (B1), (B2), (B6). Since satisfies (B1) positive homogeneity and translation invariance, setting and yields . Note that the intersection of and its negative cone satisfies . For any , the constant vectors and are comonotonic. Then by (B6) comonotonic additivity, it holds that . Combined with (B1) positive homogeneity, is fully homogeneous over on . Since is a convex cone and satisfies comonotonic additivity and full homogeneity, is linear on . By the Hahn-Banach Extension Theorem, there exists a unique linear extension such that for all . By the Riesz Representation Theorem, there exists a unique vector such that for all ; hence for all . Finally, (B1) translation invariance enforces , and (B2) monotonicity requires for all . Thus, we have .

(2) Proof for satisfying (B1), (B2), (B4), (B6). From Part (1), for any ordered risk vector , there exists a unique such that . For any unordered risk vector , (B4) permutation invariance guarantees that for any permutation . By definition, there exists a permutation such that , where is the non-decreasingly sorted version of . Thus, it holds that The uniqueness of follows directly from Part (1).

(3) Proof for satisfying (B1), (B2), (B6’). (B6’) additivity and (B1) positive homogeneity imply that is a linear functional on . By the Riesz Representation Theorem, there exists a unique such that for all . As in Part (1), translation invariance and monotonicity enforce .

(4) Proof for satisfying (B1), (B2), (B4), (B6’). From Part (3), we have for all , with . (B4) permutation invariance requires that for any permutation and any , it holds that Rewriting the right-hand side using permutation properties yields , where denotes the weight vector obtained by permuting with the inverse permutation . For this equality to hold for all , it is necessary that for all . The only permutation-invariant vector in is the uniform weight vector, i.e.,

∎

Proof of Theorem 2.

The “if” statement can be checked directly. We only focus on the “only if” statement.

(1) Step 1: Dual representation via an auxiliary convex function. Let be a cone of monotone functions. For any , its quantile function clearly belongs to . We first define an auxiliary function via:

The properness and convexity of can be established similarly to the discrete case. To establish the -lower semi-continuity of , which is equivalent to the Fatou property, we consider a uniformly bounded sequence such that . We aim to show . If , the inequality holds trivially. Otherwise, if , then there exists a subsequence such that . Since is closed under almost everywhere convergence (taking the left-continuous modification), the limit also belongs to . Thus, it suffices to show that , which is ensured by (C5).

Remark 8.

We emphasize the condition rather than convergence in the -norm to ensure the functional is compatible with the topology. This continuity requirement forces the dual representation to lie strictly within , thereby eliminating the singular components (purely finitely additive measures) that are otherwise inherent in the general dual space .

Since is proper, convex and l.s.c., by the Fenchel-Moreau Biconjugation Theorem (Chapter 12, Rockafellar (1970)), it holds that

where

Step 2: Structure of the conjugate and characterization of the weight set. Similar to the discrete case, we investigate the characteristic of . First, for any , the constant function . By (C1) affine invariance, we have

If , then we have . Otherwise, if , then . This indicates . Moreover, (C1) affine invariance also indicates

which indicates that if , it must hold that . That is, if , we have . By the above claims, it is evident that

We next go on to prove that for each valid , it holds that almost everywhere. Since is proper, convex and l.s.c., for any , it is easy to verify the non-emptiness of its subdifferential, i.e., . This indicates that for any , there exists such that

| (28) |

We first define another auxiliary set

which consists of strictly increasing functions with a uniform positive lower bound on the slope. We proceed by arising two lemmas.

Lemma 1.

Let with . Let be a smooth function satisfying

(1) on ,

(2) is supported on the interval ,

(3) for some constant .

Then for all , the function belongs to .

Proof.

For any , . Since by property (3) and by definition, it holds that

when . Hence is strictly increasing, and therefore . ∎

Lemma 2.

For any and any , we have a.e.

Proof.

Let with minimum slope . Fix any interval , and let be a smooth function supported on with . For , we define . By Lemma 1, we have . Since , the subdifferential inequality in (28) gives

Since and , by (C2) pointwise monotonicity, we have . Combining the above claims yields

which implies , i.e., . Since this relationship holds true for any smooth function supported on any interval , we conclude that holds almost everywhere on , and hence almost everywhere on . ∎

Step 3: Extension to the boundary and final representation. Since is l.s.c. (as is -lower semi-continuous), the set is closed and convex. By Lemma 2, we immediately have

| (29) |

For any function outside , i.e., , we can always choose a sequence converging to . For example, choosing for , where is always valid. Note that for identity map , , it holds that . Then by the fact that

we have when . Then the relationship Eq.(29) is valid in the entire .

Finally, by the (C4) strong permutation invariance, we can extend the result outside :

(2) The idea is very similar as in the discrete case. By assumptions, it is straightforward to check that is proper and convex. The lower semi-continuity of is a corollary of Theorem 2.2 in Jouini et al. (2006). Then from the above proof, we have

where

and . Note that for any measure-preserving transformations , and , there must exist an inverse measure-preserving transformations such that , which directly implies that

The second equality is valid due to the strong permutation invariance of . The above relationship implies that also satisfies strong permutation invariance. Thus it is reasonable to restrict .

∎

Proof of Proposition 3.

The “if” statement is direct. We only focus on the “only if” statement.

(1) Proof for satisfying (D1), (D2), (D3), and (D5). By (D3) comonotonic additivity, we have for any .

Define , the linear span of . For any with , we define . To verify that is well-defined, suppose , i.e., . By (D3) comonotonic additivity, we have

which implies . Thus, is uniquely defined on . By definition, is linear on . With (D5) -continuity, we have

confirming that is bounded (hence continuous) on .

A critical observation is that by the Jordan Decomposition Theorem, any function of bounded variation can be expressed as the difference of two non-decreasing functions. Thus, the set of bounded variation functions is a subset of . Since step functions (dense in ) are of bounded variation, we know is dense in , i.e., .

As a continuous linear functional on a dense subspace, admits a unique continuous linear extension . By the Riesz Representation Theorem for Spaces, there exists a unique such that . Restricting to , we have .

Finally, (D1) affine invariance implies , so . For any , implies by (D2) Pointwise monotonicity, and hence . The arbitrariness of and ensures a.e. on .

(2) Proof for satisfying (D1), (D2), (D3), (D4), and (D5). For any , there exists a Lebesgue measure-preserving transformation such that . By (D4) strong permutation invariance, we have Combining with the result from (1), we obtain Uniqueness of follows from (1).

(3) Proof for satisfying (D1), (D2), (D3’), and (D5). (D1) affine invariance and (D3’) additivity directly imply is a linear functional on . By (D5) -continuity, is bounded (i.e., ). The Riesz Representation Theorem guarantees a unique such that , Normalization () and non-negativeness ( a.e.) follow from (D1) and (D2), respectively, as shown in (1).

(4) Proof for satisfying (D1), (D2), (D3’), (D4), and (D5). By Part (3) we know holds for any . For any and any measure-preserving transformation , by (D4) strong permutation invariance, we have . Note that for the measure-preserving transformation , there must exist an inverse transformation such that , whcih further implies that . Hence, we conclude that for a.e. and any measure-preserving , which implies that is constant almost everywhere. The normalization of forces the constant to be , i.e., a.e.

∎

Proof of Theorem 3.

Then we move on Eqs.(15) and (16). We observe that

For each , the term attains its minimum if and only if , where denotes the statistic of under probability measure . By the monotonicity of the integral operation under a fixed , we have

with equality if and only if for all . Combining this with the constraint , we immediately obtain:

which further implies that .

Similarly, for the term, we have

By the same logic, for each , attains its minimum if and only if . From this, we can immediately derive that , where equality holds if and only if for all ; this also implies .

Next, if each paired is regular, then it is straightforward to check that the corresponding is also regular.

∎