Two-grid Penalty Approximation Scheme for Doubly Reflected BSDEs

Abstract

We study penalization coupled with time discretization for decoupled Markovian doubly reflected BSDEs with obstacles . The DRBSDE is approximated by a penalized BSDE with parameter and discretized by an implicit Euler scheme with step . A key difficulty is that the forward approximation used to evaluate the obstacles generates an error term that is amplified by . In the single-obstacle case this amplification can be removed by the shift , but no analogous transformation eliminates both obstacles simultaneously; this motivates simulating the forward SDE on a finer grid and projecting onto the backward grid (two-grid scheme). Under structural assumptions motivated by financial barriers we sharpen penalization rates and obtain a uniform bound for the value process. We derive an explicit error bound in and tuning rules; for -independent drivers, with yields the target rate. Nonsmooth barriers/payoffs are handled via a multivariate Itô–Tanaka and local-time-on-surfaces argument. We also provide numerical experiments for a one-dimensional game put under the Black–Scholes model. The observed grid-refinement errors are consistent with the predicted behavior, while the penalty sweep indicates that the tested regime remains pre-asymptotic with respect to the penalty parameter.

Keywords: doubly reflected BSDEs, Dynkin games, penalization, time discretization, implicit Euler scheme, two-grid scheme, local time on surfaces, game options

1 Introduction

Backward stochastic differential equations (BSDEs) with reflection arise naturally in stochastic control, mathematical finance, and game theory. Reflected BSDEs with a single barrier provide probabilistic representations for optimal stopping problems and obstacle partial differential equations. Doubly reflected BSDEs (DRBSDEs), which are subject to two barriers, are closely connected to Dynkin games, variational inequalities with two obstacles, and the valuation of game-type contingent claims such as callable, putable, and convertible securities; see, for example, [1, 3, 4].

This paper studies an approximation method for DRBSDEs. We consider the decoupled Markovian DRBSDE

| (1.1) |

subject to the double obstacle constraint

A classical approach to approximating reflected BSDEs is the penalization method, in which the reflection terms are replaced by large penalty terms whenever the solution exits the admissible region. In this setting, the DRBSDE (1.1) is approximated by the penalized BSDE

| (1.2) |

where

It was shown in [16] that the penalized solutions converge to the solution of the original DRBSDE, with penalization error of order as .

In practice, the penalized BSDE is numerically solved by time discretization. Unlike the standard discretization schemes, which is based on a single partition of , we employ two nested partitions

of , with coarse and fine step sizes

respectively. More precisely, we discretize the penalized DRBSDE (1.2) on the coarse grid , while the forward process is simulated on the finer grid by the Euler–Maruyama scheme and then evaluated at the coarse-grid times. With , the scheme is given by

for .

However, several issues arise naturally in implementing this procedure: (i) how the penalty parameter interacts with the time discretization, (ii) which choice of and leads to an efficient implementation, and (iii) what convergence rate is achieved by the resulting approximation. This paper addresses these questions.

Contributions. The main contributions of this paper can be summarized as follows.

-

1.

Improved penalization error under structural assumptions. Building on a PDE comparison/viscosity argument in the spirit of [13] and under additional assumptions tailored to financial barriers, we improve the pure penalization bound and obtain

uniformly in , improving the bound in [16]. This sharper penalization rate is essential for balancing the total approximation error in Corollary 4.7.

-

2.

Two-grid forward simulation for double barriers. We propose a two-grid discretization that restores the standard convergence behavior of the value approximation with respect to the backward time step, without requiring the backward scheme itself to be run on a fine grid. The method simulates the forward SDE on a finer grid and discretizes the penalized backward equation on a coarser grid . This separation is essential in the double-barrier case, because the error incurred in evaluating the barriers and along the forward approximation appears multiplied by the penalty parameter . By refining only the forward simulation, the scheme controls this amplified error at relatively low cost, while preserving a cheaper coarse-grid backward recursion.

-

3.

Explicit error rates with parameter coupling. We derive quantitative error bounds for the full penalization–discretization approximation , with explicit dependence on the coarse and fine step sizes and , and on the penalty parameter . In the general Lipschitz case, allowing -dependence in the driver, we prove the mean-square estimate

under the natural terminal approximation, so that the balancing choice yields the rate for the value process. When the driver is independent of , we further obtain the absolute-error bound

which exhibits the two-grid coupling explicitly. In particular, choosing together with recovers the target rate

These results extend the single-obstacle analysis of [13] to the double-barrier setting. In contrast to [13], which treats drivers linear in and independent of , our framework allows drivers that are Lipschitz in both and .

-

4.

Nonsmooth payoffs and barriers via multivariate Itô–Tanaka. Financial barriers such as basket calls and puts are typically not globally . We allow barrier functions that are away from a finite union of hypersurfaces. The analysis uses Tanaka-type arguments together with the change-of-variable formula with local time on surfaces (Peskir, 2007), which allows us to handle kink-type singularities while still deriving quantitative bounds compatible with penalization and discretization.

-

5.

Numerical validation and finite-sample behavior. We complement the theoretical analysis with numerical experiments for a one-dimensional game put under the Black–Scholes model. The grid-refinement experiment, performed under the theoretically motivated coupling , exhibits relative errors consistent with an decay. A second penalty sweep at fixed shows that, over the tested range, the error continues to decrease as increases, indicating that the computations remain in a pre-asymptotic regime in which the asymptotic balancing effect is not yet sharply resolved.

Organization. Section 2 introduces the DRBSDE framework and basic assumptions, together with existence and uniqueness results. Section 3 establishes the penalization error and the improved bound. Section 4 presents the two-grid numerical scheme and derives explicit discretization error bounds, together with parameter couplings that yield the rate. Section 5 reports numerical experiments for a game put example under the Black–Scholes model. Section 6 concludes.

2 Doubly reflected BSDEs: setting and preliminaries

We now describe the framework and introduce Markovian doubly reflected BSDEs under suitable assumptions. Let us fix a time horizon and consider a filtered probability space

Let be a standard -valued Brownian motion defined on the above probability space.

For and , we use the following notations.

-

•

is the space of all -measurable -valued random variables such that

-

•

is the space of all -valued progressively measurable processes such that

-

•

is the space of all adapted continuous processes such that

-

•

is the space of real-valued non-decreasing continuous predictable processes with . We also define

We are now ready to define doubly reflected BSDEs along with our assumptions. For , we study BSDEs of the form

| (2.1) |

under the following assumptions on coefficients.

Assumption 2.1.

-

(i)

The maps , are -Hölder continuous in the first argument. That is, there exist constants such that

for all and . Also, and are Lipschitz continuous in the second argument, i.e., there exist constants such that

for all and .

-

(ii)

There exists a constant such that, for all and all ,

-

(iii)

The function is Lipschitz continuous, i.e., there exists a constant such that

for all

-

(iv)

There exist constants such that the function satisfies

for all . Also,

and there exists a constant such that

for all .

-

(v)

The functions are -Hölder continuous in the first argument with Hölder constants , respectively, and Lipschitz-continuous in the second arguments with Lipschitz constants , respectively.

-

(vi)

We have and for all and .

With Assumption 2.1, we can establish the following theorem of uniqueness and existence of solution to (2.1) as a straightforward corollary to Theorem 3.7 of [8].

Furthermore, it is well known that (2.1) has a connection to the free-boundary PDE for given by

| (2.2) |

where

Specifically, we have the following well known result, as can be checked in [5].

Theorem 2.3.

For our method, we also consider the following penalized BSDE which approximates (2.1) as :

| (2.3) |

Here, and is defined by

We aim to calculate the error bound of the discretization scheme for the penalized BSDE (2.3). Again, if Assumption 2.1 holds, we have the following uniqueness and existence result. (See, e.g., [10]).

Let us now discuss the partial differential equation (PDE) corresponding to (2.3). Specifically, for , we consider the PDE

| (2.4) | ||||

It is well known that, under suitable conditions, the solution to the BSDE (2.3) can be expressed in terms of the solution to the PDE (2.4). Specifically, we have the following result (See, e.g., [11].)

Assumption 2.5.

-

(i)

is uniformly elliptic on .

-

(ii)

and are in the second argument.

3 Penalty error

For analyzing error from penalization, we first make the following additional assumptions on the payoff functions and the initial condition of the forward process.

Assumption 3.1.

There exist hypersurfaces such that for some with , satisfying the following conditions. We set and .

-

(i)

We have and . Moreover, for each and each of , the one-sided normal derivatives exist for , where .

-

(ii)

There exists such that for each and each ,

where

-

(iii)

There exist and such that for each ,

-

(iv)

We have and , where

and

Example 3.2.

Consider a put option where the holder may exercise early while the writer may also cancel early by paying an additional penalty. The underlying consists of assets. Under a risk-neutral measure, the asset dynamics are given by the Black–Scholes SDE

| (3.1) |

The holder’s exercise payoff is the arithmetic-basket put

and the writer’s cancellation payoff is defined by adding a time-dependent penalty

| (3.2) |

so that for all and .

The following proposition is analogous to Proposition 1 of [13].

Proposition 3.3.

Proof.

We prove the first inequality. The second one is proved analogously.

Let and choose large enough to satisfy

| (3.3) |

for all .

Also, for , we define

Since and have at most linear growth whereas has superlinear growth, there exists a compact set

such that on .

If on , then

and letting yields the conclusion. We may therefore assume that is positive somewhere, and hence attains a maximum on .

We now distinguish two cases.

Case 1. We assume that attains a positive maximum at some

Since , the function is in a neighborhood of .

We set

Then

and the maximality of at gives

for near . Thus has a local minimum at , and the viscosity supersolution property of yields

| (3.4) |

From

we obtain

Since , we also have

Substituting these relations into (3.4), we obtain

| (3.5) | ||||

Furthermore, the Lipschitz continuity of in gives

Substituting this into (3.5), we arrive at

By (3.3) and the definition of , this yields

Since for all , we obtain

By letting , we conclude that

Case 2. We now assume that every maximizer of lies on .

Since has empty interior and is continuous, there exists with such that

for any .

Applying Ekeland’s variational principle [6] to the continuous function on the complete metric space , we conclude that for every , there exists such that

and such that

attains its maximum over at .

Choosing , we have , and hence is in a neighborhood of .

Let

and

then since

and has a local minimum at , the viscosity supersolution property yields

Since , we have , and thus

Letting yields

Since we assumed attains it’s global maximum on , we conclude

Again, letting yields

This proves the first inequality.

For the second inequality, one argues in the same way with

replacing positive maxima by negative minima throughout. This completes the proof. ∎∎

Corollary 3.4.

Theorem 3.5.

Proof.

For brevity, we write

Note that for , we have and .

We first prove the upper bound inequality

Let

then, it is sufficient to show that is a viscosity supersolution of

| (3.7) |

Let be such that attains a local minimum at , and set

Then attains a local minimum at .

We consider the following two cases.

Case 1. If , then the supersolution condition for (3.7) is immediate since the second entry in the outer maximum is nonnegative.

Case 2. Assume that . The estimate of Proposition 3.3,

implies that

or equivalently,

Since , one has

In this case, verifying the supersolution condition reduces to proving

Since is a viscosity supersolution of the penalized PDE, we have

| (3.8) |

Also, since and depends only on , it follows that

| (3.9) |

Furthermore, the inequality gives us

and hence

Thus, we arrive at

| (3.10) |

Combining (3.8), (3.9), and (3.10), we obtain

Because and , the Lipschitz continuity of in the -variable gives

Hence

Since , the right-hand side is equal to . This proves that is a viscosity supersolution of (3.7).

The terminal condition satisfies

and hence applying the comparison principle gives us

which implies the desired conclusion.

The lower bound can also be proven similarly. ∎∎

For the total penalty error, we define increasing finite variation processes and by

Then the backward equation of penalized BSDE (2.3) can be rewritten as

in differential form.

Theorem 3.6.

Proof.

First, we have

from Theorem 3.5. Now, let us denote and . Then, we have

Thus, applying the Itô formula to , we obtain

| (3.11) | ||||

By Young’ inequality and the Lipschitz property of , we have

| (3.12) | ||||

Next, note that

| (3.13) | ||||

and

| (3.14) | ||||

Plugging in (3.12), (3.13), and (3.14) into (3.11), and then taking expectaion of absolute values of both sides, we arrive at

| (3.15) | ||||

Also, since we have . Thus, applying the Cauchy–Schwarz inequality yields

Plugging these estimates into (3.15), we conclude that

∎∎

4 Numerical scheme and error analysis

We describe the numerical scheme and derive an error bound of our method. From here on, we denote by any constant depending only on the data of the BSDE (2.1): , , , , , , , and . Note that the constant does not depend on the penalty parameter .

4.1 Numerical scheme

We describe the numerical scheme of our approximation method. First, we fix two time grids and on and write and . Note that , , and the generic constant does not depend on the resolution nor on .

The solution to the forward equation is approximated by the Euler–Maruyama scheme , with values on the finer grid given inductively as

| (4.1) |

for .

Then, on the coarser grid , we consider the discretization scheme

| (4.2) |

with terminal condition

| (4.3) |

where , to approximate the penalized BSDE solution associated with the forward Euler approximation of .

4.2 A priori estimates

Before obtaining error bounds, we derive a priori estimates. The following bound on the norms of the solutions to (2.3) can be obtained by applying previous results to alter proofs of well known results, such as Lemmata 1.5.1 and 1.5.2 of Part II of [7].

Proposition 4.1.

Proof.

We first divide into intervals with . For any , we have

Taking conditional expectations on both sides leads to

Thus, for we obtain

Thus, by Doob and Jensen’s inequality, we obtain

| (4.9) | ||||

Next, we apply the Burkholder–Davis–Gundy inequality to the martingale

to obtain

| (4.10) | ||||

Thus, putting together (4.9) and (4.10) yields

We then apply the continuity properties of , inequality (4.7), and Corollary 3.4 to obtain

Choosing , we arrive at

| (4.11) | ||||

Therefore, applying Grönwall’s lemma yields

Thus, follows from induction, the Lipschitz property of , and (4.7). Plugging this into (4.11) and using induction yields as well, and the desired conclusion follows. ∎∎

Remark 4.2.

The intervals introduced in the proof of Proposition 4.1 is irrelevant to the partition of the discretization scheme of our method.

Corollary 4.3.

4.3 Square error bound

We now derive the total square error bound of our scheme.

Theorem 4.4.

Proof.

Thus, combining (4.2) and (4.12) yields

Let

and , where

and

Then, by Lipschitz continuity, and we obtain

| (4.13) | |||

Thus, squaring both side of (4.13) and taking expectation, and then using Itô isometry yields

| (4.14) | ||||

Since , applying Young’s inequality to the right hand side of (4.14) gives us

| (4.15) | ||||

By the continuity property of and Young’s inequality, we have

| (4.16) | ||||

We now bound each terms on the righthand side of (4.16). First, applying the Cauchy–Schwartz inequality, Young’s inequality, and (4.5), we have

| (4.17) | ||||

For the second term, we find

| (4.18) |

We apply the Cauchy–Schwartz inequality to the third term to obtain

| (4.19) | ||||

Plugging in (4.17), (4.18), and (4.19) into (4.16) yields

| (4.20) | ||||

Thus, (4.20), (4.15), and gives us

| (4.21) | ||||

Since for , induction on (4.21) gives us

| (4.22) | ||||

Therefore, applying Proposition 4.1 and Grönwall’s inequality to (4.22) yields

| (4.23) | ||||

Also, applying Young’s inequality, continuity properties of , Proposition 4.1, and Corollary 4.3, we calculate

| (4.24) | ||||

Using (4.8) and applying Young’s inequality, Cauchy–Schwartz inequality, and Corollary 4.3, we have

| (4.25) | ||||

Also, by Proposition 4.3 and the Cauchy–Schwartz inequality, we find that

| (4.26) | ||||

By the same argument, we also have

| (4.27) |

Combining the penalty error from Theorem 3.6 and discretization error from Theorem 4.4, we obtain the total error as follows.

Corollary 4.5.

In particular, if , we obtain the minimal error rate

for the value process. This is suboptimal compared to the error rate of for conventional approximation schemes.

4.4 Absolute error bound for Z-independent driver

We consider the case in which the driver is not dependent on , and obtain the absolute error bound for the value process. It follows that optimal error rate of can be obtained with choices and for .

As before, we work under Assumptions 2.1,2.5, and 3.1. For each , let be the signed distance to on a tubular neighborhood and define

where denotes the symmetric semimartingale local time at . For define

with . It is standard that we have

| (4.30) |

The following is the extended version of Theorem 2 of [13].

Theorem 4.6.

Proof.

We use the same notations as in the proof of Theorem 4.4. Taking conditional expectation of both sides of (4.13) and then taking absolute values, we obtain

| (4.31) |

Since , we find that

| (4.32) |

Now, note that

| (4.34) | ||||

Then, we have

| (4.35) | ||||

Also, applying Tanaka’s formula together with the change-of-variable formula with local time on surfaces [15, 14], we calculate that for ,

where . Moreover, by Peskir’s formula we have

Thus, using , we obtain

Taking conditional expectations eliminates the stochastic integral, hence

Thus, by Proposition 4.1, continuity properties of , polynomial growth of , Corollary 3.4, and (4.7), we have

| (4.36) | ||||

Here denotes the total variation process of , and we used that by the bounded jump condition (Assumption 3.1(ii)) on .

By the same argument, we also have

| (4.37) | ||||

where and denotes the total variation process of .

Summing up, we obtain

| (4.40) | ||||

Note that, by Tanaka’s formula and Peskir’s change-of-variable formula,

Thus,

where we used Proposition 4.1, and Corollary 3.4. Similarly, , and hence

| (4.41) |

Moreover, it follows from (4.30) that

| (4.42) |

Corollary 4.7.

It is easy to see that the optimal error rate of is achieved with and for .

Remark 4.8.

In the bound of Corollary 4.7, the leading terms are

To obtain the target rate , the auxiliary time step must be chosen so that

Under this coupling, choosing yields

5 Experimental results

Problem setup and DRBSDE.

We work under the risk-neutral Black–Scholes model

with parameters and . We consider a one-dimensional Dynkin game (Israeli/game put): the holder may exercise to receive the put payoff, while the writer may cancel by paying an additional time-dependent premium. In the DRBSDE formulation, we solve for adapted processes such that

where and are nondecreasing processes with , together with the obstacle condition

and the Skorokhod reflection conditions

Here

with strike and . The quantity of interest is the initial value .

Experimental procedure and parameter sweeps.

We compare our penalized implicit discretization, implemented with LSMC regression for conditional expectations, against a penalty-free reference computed by a CRR binomial Dynkin-game recursion. The CRR baseline uses a recombining tree with a large number of steps, here , yielding the reference value

For our method, we simulate sample paths of , repeat the experiment over three random seeds, and report the mean estimate of together with the absolute and relative errors

Since the forward process is sampled exactly under the Black–Scholes model, no additional fine-grid approximation is needed in the forward simulation, and hence the auxiliary parameter does not appear in the experiments.

We perform two parameter sweeps.

-

1.

Time-step sweep. We vary the number of backward time steps

and choose the penalty parameter according to the theoretically motivated scaling

Since Corollary 4.7 predicts an convergence rate in the -independent case under the coupling , this experiment tests whether the observed error behaves like . In addition to the measured errors, we fit a curve of the form to the observed relative errors.

-

2.

Penalty sweep at fixed . Fixing , we vary the penalty parameter according to

for several values of . Although the asymptotic error analysis suggests as the natural balancing choice, this second experiment is intended to assess the finite-resolution sensitivity of the method to the penalty level and to determine whether the asymptotic balancing regime is already visible at the tested resolutions.

Results.

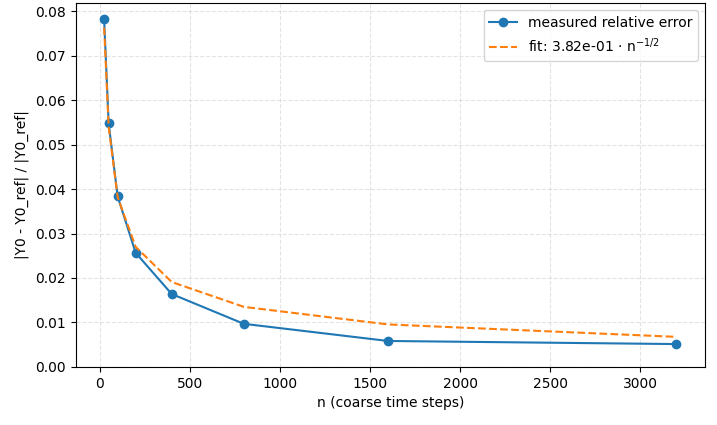

Table 1 and Figure 1 summarize the time-step sweep with

The observed relative error decreases steadily as increases. Moreover, the graph closely follows the fitted profile

over the first four grid levels, and for the finer grid levels the measured error falls slightly below the fitted curve. This behavior is fully consistent with the theoretical prediction.

Table 2 and Figure 2 display the penalty sweep at fixed . Over the tested range, the relative error decreases monotonically as increases. This behavior does not contradict the theory. Rather, it indicates that the experiment remains in a pre-asymptotic regime in which stronger penalization continues to improve the approximation, while the balancing effect underlying the asymptotically optimal scaling is not yet sharply visible at the present resolution. Accordingly, the penalty sweep should be interpreted as a finite-sample sensitivity study rather than as a direct numerical identification of the asymptotic balancing point.

| abs. error | rel. error | ||||

| 25 | 1.7534011957 | ||||

| 50 | 1.7153466906 | ||||

| 100 | 1.6886314368 | ||||

| 200 | 1.6679777902 | ||||

| 400 | 1.6529172189 | ||||

| 800 | 1.6420117424 | ||||

| 1600 | 1.6357353240 | ||||

| 3200 | 1.6346008394 |

| abs. error | rel. error | |||

| 0 | 1.6708014595 | |||

| 0.25 | 1.6685825388 | |||

| 0.5 | 1.6679777902 | |||

| 0.75 | 1.6678159132 | |||

| 1 | 1.6677727926 | |||

| 1.5 | 1.6677582704 | |||

| 2 | 1.6677572434 | |||

| 4 | 1.6677571652 |

6 Conclusion

We analyzed a penalty approximation of a decoupled Markovian doubly reflected BSDE in the computational regime where penalization is coupled with time discretization. The central difficulty in the two-barrier setting is that the error produced by evaluating the obstacles along an approximated forward process enters multiplied by the penalty parameter , and unlike in the single-barrier case, no simple transformation removes this amplification for both obstacles simultaneously. This motivates the two-grid construction, in which the forward process is resolved separately from the backward discretization.

Under additional structural assumptions motivated by typical financial barriers, we sharpened the penalization error and obtained a uniform bound for the value process. Combining this with the fully discrete scheme yields explicit error bounds in and transparent parameter-coupling rules. In particular, in the -independent case, choosing

recovers the target rate for the value process.

The numerical experiments support this picture. In the grid-refinement experiment, performed under the theoretically motivated scaling , the observed relative error follows the predicted behavior closely. In the penalty sweep at fixed resolution, the error continues to decrease as increases over the tested range, suggesting that the computations remain in a pre-asymptotic regime in which stronger penalization still improves the approximation and the asymptotic balancing effect is not yet sharply visible.

Several directions remain open. On the theoretical side, it would be natural to extend the analysis beyond the decoupled Markovian setting, and to investigate whether comparable quantitative results can be obtained for more general obstacle geometries or less regular coefficients. On the numerical side, it would be interesting to combine the present error analysis with more flexible regression or deep-learning-based solvers in higher dimensions.

Acknowledgments

Hyungbin Park was supported by the National Research Foundation of Korea (NRF) grants funded by the Ministry of Science and ICT (Nos. 2021R1C1C1011675 and 2022R1A5A6000840). Financial support from the Institute for Research in Finance and Economics of Seoul National University is gratefully acknowledged.

References

- [1] (2009) Valuation and hedging of defaultable game options in a hazard process model. Journal of Applied Mathematics and Stochastic Analysis 2009, pp. 695798. External Links: Document Cited by: §1.

- [2] (2008) Discrete-time approximation of decoupled forward-backward SDEs with jumps. Stochastic Processes and their Applications 118 (1), pp. 53–75. External Links: Document Cited by: §4.1.

- [3] (1996) Backward stochastic differential equations with reflection and Dynkin games. The Annals of Probability 24 (4), pp. 2024–2056. External Links: Document Cited by: §1, Example 3.2.

- [4] (2016) Numerical approximation of doubly reflected BSDEs with jumps and RCLL obstacles. Journal of Mathematical Analysis and Applications 442 (1), pp. 206–243. External Links: Document Cited by: §1.

- [5] (2016) Generalized Dynkin games and doubly reflected BSDEs with jumps. Electronic Journal of Probability 21, pp. 1–32. External Links: Document Cited by: §2.

- [6] (1974) On the variational principle. Journal of Mathematical Analysis and Applications 47 (2), pp. 324–353. External Links: Document Cited by: §3.

- [7] (2006) Contrôle stochastique et méthodes numériques en finance mathématique. Ph.D. Thesis, Université Paris-Dauphine. Cited by: §4.2.

- [8] (2005) BSDEs with two reflecting barriers: the general result. Probability Theory and Related Fields 132 (2), pp. 237–264. External Links: Document Cited by: §2.

- [9] (1992) Numerical solution of stochastic differential equations. Applications of Mathematics, Vol. 23, Springer, Berlin. Cited by: §4.1.

- [10] (1999) Forward-backward stochastic differential equations and their applications. Springer. Cited by: §2.

- [11] (2002) Representation theorems for backward stochastic differential equations. The Annals of Applied Probability 12 (4), pp. 1390–1418. External Links: Document Cited by: §2.

- [12] (2003) Stochastic differential equations: an introduction with applications. 6 edition, Universitext, Springer, Berlin. Cited by: §4.1.

- [13] (2024) Deep penalty methods: a class of deep learning algorithms for solving high dimensional optimal stopping problems. External Links: 2405.11392, Document Cited by: item 1, item 3, §3, §4.4.

- [14] (2007) A change-of-variable formula with local time on surfaces. In Séminaire de Probabilités XL, Lecture Notes in Mathematics, Vol. 1899, pp. 69–96. External Links: Document Cited by: §4.4.

- [15] (1999) Continuous martingales and brownian motion. Grundlehren der mathematischen Wissenschaften, Vol. 293, Springer, Berlin, Heidelberg. External Links: Document Cited by: §4.4.

- [16] (2011) Numerical algorithms and simulations for reflected backward stochastic differential equations with two continuous barriers. Journal of Computational and Applied Mathematics 236 (5), pp. 1137–1154. External Links: Document Cited by: item 1, §1.