XXX\EquationsNumberedThrough

Zang et al

How bad is time variability for users?

How bad is time variability for users in mobility services?

Zhaoqi Zang, David Z.W. Wang*

\AFFSchool of Civil and Environmental Engineering, Nanyang Technological University, 50 Nanyang Avenue, Singapore 639798, Singapore,

\EMAIL* Corresponding author. zhaoqi.zang@ntu.edu.sg; wangzhiwei@ntu.edu.sg

Xiangdong Xu \AFFCollege of Transportation, Tongji University, Shanghai, China, \EMAILxiangdongxu@tongji.edu.cn

Shaojun Liu \AFFSchool of Civil and Environmental Engineering, Nanyang Technological University, 50 Nanyang Avenue, Singapore 639798, Singapore, \EMAILshaojun.liu@ntu.edu.sg

Time variability is a pervasive feature of mobility services and a major source of welfare loss for users. Although a substantial literature has quantified the cost of time variability (COTV), it remains theoretically unclear how bad time variability can be for users in the worst case. In the absence of such a benchmark, quantified variability costs lack a principled reference for assessing whether they are economically meaningful or negligible. Meanwhile, such a benchmark is critical for strategic prioritization in transport appraisal, service design, and pricing—particularly in early-stage decision making, where detailed valuation is often infeasible. To fill this gap, this paper develops an expected utility (EU) framework to quantify the cost of time (COT) and the COTV, and to establish theoretical upper bounds on the ratio of COTV to COT. For users with quadratic utility, we show that , where is the coefficient of variation of service time. When the service process follows a Poisson process, a common adopted assumption, this bound simplifies to , implying that the total cost of a mobility service with stochastic service time is at most 1.5 times that of an otherwise identical deterministic service. In more general settings, the ratio depends on three interpretable factors: and users’ second- and third-order risk preferences, captured by relative risk aversion (RRA) and relative prudence (RP). We identify benchmark values of RRA and RP that characterize users’ preferences over mean-, variance-, and skewness-related reductions. Our analysis is further extended to non-EU frameworks, including dual theory and rank dependent utility, showing that the key structural insights remain robust despite differences in how time variability and users’ preferences are modeled. By quantifying the cost induced by time variability and the ratio of COTV to COT, this study provides a data-light benchmark for early-stage decision making and a principled upper bound on users’ willingness to pay for reliability improvements, informing the pricing and design of reliability-oriented services. \KEYWORDScost of time variability; risk aversion; prudence; expected utility; dual theory; rank dependent utility

1 Introduction

The economic costs of time variability—the inconsistency or unpredictability of transport or mobility service times—are profound (Winston 2013). For U.S. motorists, truckers, and shippers, increased delays due to time variability resulted in a $45 billion welfare loss (Langer et al. 2008), while in U.S. domestic air travel, arrival delay variability doubled users’ expected costs (Koster et al. 2016). Moreover, time variability significantly affects users’ satisfaction and loyalty across various mobility services and systems, including public transport, online delivery or ridesourcing, and tolling or charging services (e.g., Yin and Lou 2009, Jung et al. 2014, Ansari Esfeh et al. 2021, Xu et al. 2021, Yu et al. 2022). Recognizing the inevitability of time variability, users are willing to pay to reduce it (see Carrion and Levinson (2012)), prompting service providers to improve reliability and regulators to require the inclusion of time variability costs in project appraisals (NZTA 2010, de Jong and Bliemer 2015). Consequently, quantifying the cost of time variability (COTV) is of interest to all stakeholders, including users, service providers, regulators, and the society. Accordingly, a wide range of empirical and theoretical methods have been therefore developed to quantify COTV (see reviews e.g., Li et al. 2010, Carrion and Levinson 2012, Zang et al. 2022). Together, these studies have substantially advanced our understanding of how variability affects user’ behavior.

However, quantifying COTV alone, often referred to as the value of reliability (VOR) in the literature, only addresses the question of How much does it cost users due to time variability. In other words, the VOR studies do not answer another fundamental question: How bad can time variability be for users in the worst case? Without a theoretical benchmark, the estimated COTVs lack an interpretable scale: while they indicate how much users are willing to pay for reliability, they do not reveal whether an estimated variability cost is economically meaningful or negligible. This limitation is especially consequential in early-stage decision-making, where reliability improvement investments (such as increasing road capacity and building dedicated lanes or a new road) must be screened and prioritized before a detailed evaluation is feasible.

This paper fills this gap by developing a framework to evaluate how large the economic inefficiency induced by time variability can be, relative to the cost users already incur from mean time. Specifically, we first model how users respond to time variability using risk premium approach. We then adopt the expected utility (EU) framework to estimate the cost of time variability (COTV) relative to the cost of time (COT), where the latter represents users’ cost under an otherwise identical deterministic service. The ratio of the COTV to COT is used as a normalized measure of the severity of time variability. Furthermore, we study marginal benefits by comparing the returns to reductions in time variability and mean service time via the ratio of the value of time variability to the value of time, capturing how users value a unit decrease in variability relative to a unit decrease in mean service time.

We show that under a commonly adopted setting for mobility services, where users’ utility function is quadratic, and its service process follows a Poisson process, the COTV is at most of the COT. Consequently, the total cost for users under time variability is bounded by 1.5 times that of an otherwise identical deterministic service. This simple yet powerful bound provides the first theoretical “worst-case” benchmark for COTV. More generally, if we relax the Poisson process assumption and retain only the quadratic utility assumption, the ratio satisfies where is the coefficient of variation of service time. This bound is appealing as it depends linearly only on readily observable characteristics of time variability (i.e., ) for arbitrary risk preference parameters. As such, it is particularly useful for the early-stage decision-making related to strategic prioritization in transport appraisal, service design, and pricing.

In an even more general setting where users’ utility functions are only assumed to be differentiable, we show that the ratio of COTV to COT depends on three interpretable factors: the degree of time variability (captured by CV), users’ second-order risk preference (captured by relative risk aversion, RRA), and third-order risk preference (captured by relative prudence, RP). We identify benchmark values of RRA and RP that classify users according to their preferences for reducing the mean, variance, and skewness of random mobility service times. Intuitively, reduction in mean time makes trips faster, reduction in variance decreases spread of travel times around mean, and reduction in skewness protects users against rare but severe delays. This preference-based classification is of clear practical relevance, as identifying user types is essential for effectively managing time variability in service systems (Yu et al. 2018).

Finally, recognizing the well-known limitations of expected utility (EU) models, such as common-ratio and framing effects, we extend our analysis to non–EU frameworks, including dual theory (DT; Yaari (1987)) and rank-dependent utility (RDU; Quiggin (1982)). Although these frameworks differ in their modeling primitives, the structural form of the COTV–COT ratio remains unchanged, continuing to depend on the degree of time variability and users’ risk preferences. The distinction lies in representation: under EU, variability and preferences are characterized in the payoff (i.e., mobility service time) plane via space through moments of time and derivatives of the utility function, whereas under non-EU models they are captured in the probability plane through dual moments and probability-weighting derivatives.

In summary, the main contribution of this paper is to provide a theoretical answer to how bad time variability can be for users. We show that the economic impact of time variability is inherently bounded and depends on both the degree of variability and users’ risk preferences, thus placing variability costs within a clear and interpretable benchmark relative to time costs. Taken together, these results complement existing valuation methods by offering a data-light benchmark for early-stage decision-making, as well as practical guidance for transport appraisal, reliability-oriented pricing, and the design of mobility services under uncertainty.

The remainder of this paper is organized as follows. Section 2 reviews time variability and its quantification. Section 3 models users’ response to time variability under EU framework. Section 4 quantifies the COTV and defines the ratios to assess how bad time variability can be. Section 5 gives theoretical results and discussions. Section 6 extends the analysis to non–EU frameworks. Section 7 concludes the paper.

2 Literature review

This section first reviews extensive evidence on the importance and consequences of time variability, and then introduces methods for evaluating the cost of time variability.

2.1 Time variability in mobility service systems

There are many forms of time variability in mobility service systems, most notably variability in travel times, waiting times, and queuing or service times.

Travel time variability (TTV) has long been recognized as an important topic since Herman and Lam (1974). Moreover, the rare events included in TTV may cause much more serious delays as expected by travelers, which is at most five times than that of common condition (Van Lint et al. 2008). Reducing the TTV can therefore generate substantial benefits, often comparable to reducing travel time, as reported by many studies (Franklin and Karlstrom 2009, Carrion and Levinson 2012, Devarasetty et al. 2012, Zang et al. 2026). This underscores the need to quantify the cost of TTV (NZTA 2010, de Jong and Bliemer 2015, Zang et al. 2024). Waiting time variability plays a critical role in shaping the attractiveness and perceived service quality of mobility service in transport systems, including public transit (Cats and Gkioulou 2017, Ansari Esfeh et al. 2021), airports (Gkritza et al. 2006), and online delivery or ride-sourcing platforms (Xu et al. 2021, Yu et al. 2022, Cui et al. 2024). For instance, Fan et al. (2016) reported that passengers’ perceived waiting time was on average 1.21 times their actual waiting time. Consequently, waiting time is often regarded as the dominant component of generalized cost in public transport (Ansari Esfeh et al. 2021), and thus serves as a key performance indicator of service attractiveness (Esfeh et al. 2022). Queuing and service time variability typically emerges when demand persistently exceeds service capacity of transport systems. An example is severe congestion at corridor bottlenecks—such as toll stations—during peak hours (Moghaddam et al. 2017), where long and uncertain queues significantly reduce operational efficiency. Beyond road networks, electric vehicle users often experience substantial and unpredictable queuing delays at urban public charging stations (Jung et al. 2014), exacerbating their range anxiety (Noel et al. 2019).

The widely existing time variability and its significant effects highlight the necessity of understanding users’ behavioral responses to variability and further evaluating its cost for users or systems.

2.2 Modeling the cost of time variability

A notable theoretical achievement for modeling the time variability of transportation systems is the bottleneck model developed by Vickrey (1969). Small (1982) introduced the schedule cost into the bottleneck model and proposed the expected utility model, which assumes that travelers aims to maximize their trip utility in their trip scheduling and their disutility comes from not arriving at the preferred arrival time on time. Specifically, under this schedule delay framework, the concept of the monetary value of travel time reliability, namely the VOR, and reliability ratio approach have been developed to quantitatively assess the cost of travel time variability (TTV) (Small 1982, Noland and Small 1995, Bates et al. 2001, Fosgerau and Karlström 2010, Jenelius 2012, Li et al. 2012, Engelson and Fosgerau 2016, Zang et al. 2024). This line of research is rooted in schedule-based travel behavior and variability causes cost because it generates earliness and lateness penalties, so we often refer to it as the scheduling delay approach.

Another line of research on modeling the cost of time variability (COTV) is the Bernoulli approach. The Bernoulli approach is also grounded in expected utility theory, but it explicitly attributes disutility to variability itself. Under this framework, travelers dislike time variability because they are risk-averse toward uncertain travel times, implying that greater risk aversion leads to higher cost of variability. Specifically, with the theoretical foundation of the so-called safety margin provided by Gaver Jr (1968) and Knight (1974), Jackson and Jucker (1982) successfully used mean-variance preferences over random travel times to explain the choice among risky trips. In the context of a general travel choice model, Senna (1994) further made notable advances in deriving measures of both the value of time and the value of travel time variability. Recently, Beaud et al. (2016) and Zang et al. (2026) used the Bernoulli approach to model the cost of travel time variability and explored the impact of travel time variability and travelers’ risk attitudes on it.

Since our goal is to quantify how much users suffer from time variability, we focus on the cost generated by variability itself. Accordingly, we adopt the Bernoulli approach to model the COTV. To the best of our knowledge, the current literature in quantifying the COTV has focused mainly on deriving its formulations and examining the factors influencing it (See reviews e.g., Carrion and Levinson 2012, Zang et al. 2022). However, no studies have ever established an upper bound on the ratio of COTV to COT. As a result, how severe time variability can be for users remains an open question. The studies most closely related to our work are those on the VOR and the reliability ratio, from which our focus differs in several respects. First, the reliability ratio captures the marginal value of reducing travel time variability per unit of travel time, whereas we study the total cost attributable to time variability. Second, recent advances in the VOR mainly express it as a function of users’ preferences and a variability measure, and then estimate it empirically using stated- or revealed-preference data; see the reviews in Li et al. (2010) and Carrion and Levinson (2012). Such empirical quantification, however, lacks a theoretical benchmark for assessing whether a quantified variability cost is economically large or negligible. In other words, while VOR indicates users’ willingness to pay for reliability, it does not reveal how severe time variability can be relative to mean time in worst-case scenarios. In contrast, a theoretical benchmark, specifically an upper bound on the ratio of COTV to COT, is particularly valuable for early-stage decision-making. For example, it benefits screening and prioritizing reliability-improvement options (e.g., capacity expansions or constructing a new road) before detailed project-level appraisal is feasible. Finally, most current VOR studies are based on the EU framework, which has well-known limitations (e.g., common-ratio and framing effects), whereas we extend our analysis to non-EU frameworks.

3 A theoretical framework for modeling users’ responses to time variability

This section introduces mobility service users’ utility function of time and their risk attitudes, and models their responses to time variability, thereby providing a theoretical foundation for the subsequent analysis.

For a transport or mobility service, we use lowercase to represent its service time11endnote: 1Note that can represent various realistic duration time involved in the mobility services; its specific terminology depends on specific contexts, e.g., travel time, waiting time, queuing time, and service time. and uppercase to represent a constant value of . Let , , , and denote its mean, standard deviation, probability density function (PDF), and cumulative distribution function (CDF), respectively. Throughout this paper, we refer to the single as an instance without time variability with utility ; the triple referred to as an instance with time variability and and its expected utility is denoted as . For notational convenience, we use to denote the instance when no ambiguity arises.

3.1 Utility function of time and risk attitudes

In the context of economic risks, individuals generally prefer larger amounts of wealth because it typically yields positive utility to them. Therefore, the utility function of wealth, denoted by , is assumed to be a non-decreasing function, i.e., . In contrast, as transport demand is derived from the need to move people or goods, time spent for mobility services typically generates negative utilities; users therefore dislike long service times. For example, passengers generally dislike longer waiting times for buses. As a result, the utility function of time is a non-increasing function, i.e., for .

Building seminar works on risk attitudes (Pratt 1964, Arrow and others 1965, Kimball 1990), Definition 3.1 formalizes the second-order risk preference (i.e., Pratt-Arrow risk aversion) and the third-order risk preference (i.e., prudence) for mobility service users with differentiable utility function. Interested readers can further refer to Gollier (2001) and Eeckhoudt and Schlesinger (2006) for understanding risk aversion and prudence.

Definition 3.1 (Risk attitudes)

Given a mobility service user with a differentiable utility function of service time, the user is (i) risk-averse if and only if the utility function is concave and (ii) prudent if and only if the marginal utility function is convex.

Definition 3.1 implies that, mathematically, risk aversion is equivalent to , which in turn implies . For this reason, risk aversion is referred to as a second-order risk preference. Prudence is equivalently characterized by , i.e., , and therefore is termed as a third-order risk preferenceThis paper follows the original meaning of prudence introduced in economic risks (Eeckhoudt and Schlesinger 2006): agents raise savings for uncertainty in future incomes. That is, prudent users of mobility services prepare to pay additional time for variability in their service times. This is different with Beaud et al. (2016) that defined prudence by under context of travel time variability from the perspective of disliking upside variability.. In the context of time variability, risk aversion reflects users’ dislike of variability and their desire to avoid it whenever possible, whereas prudence captures users’ propensity to prepare for and protect themselves against rare but severe unfavorable realizations of random service time.

3.2 Modeling users’ responses to time variability

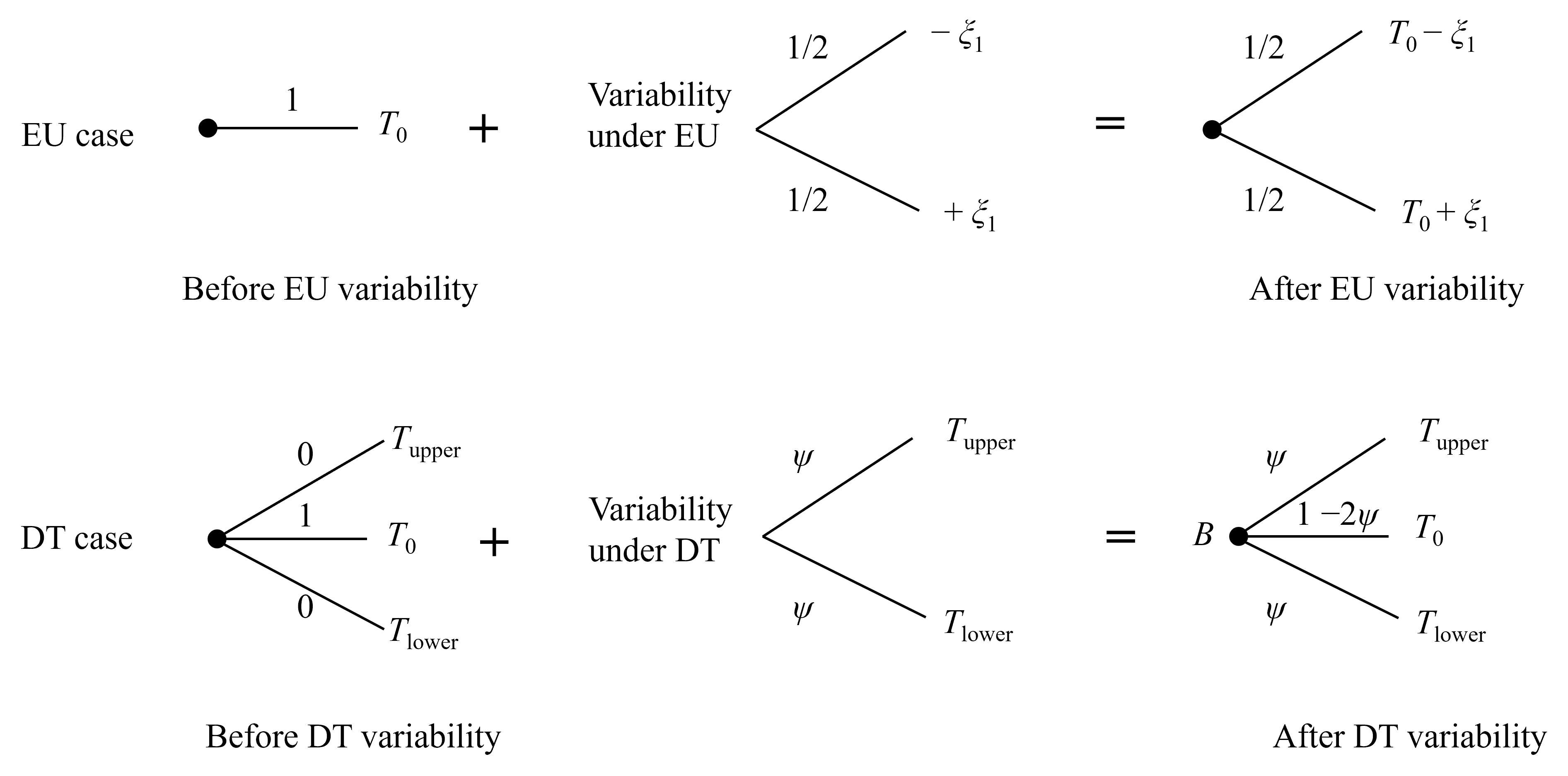

For a given mobility service, consider two instances: one determinstic benchmark without time variability and one stochastic instance with time variability by adding a zero-mean time variability into . Figure 1 shows these two instances by using a discrete representation of the variability for illustrative clarity; the analysis readily extends to continuous representations as . Throughout the paper, values shown along the lines (at the right end) in all figures represent probabilities (outcomes).

For users who prefer certainty to variability, a common behavioral practice is to reserve additional time beyond to eliminate the impact of time variability. This practice corresponds to safety margin hypothesis of how users manage time variability, which has been widely recognized in both empirical and theoretical studies (e.g., Gaver Jr 1968, Lo et al. 2006, Zang et al. 2026). Given that the utility function of time is non-increasing, the maximum should satisfy . We can find that identifies a utility-equivalent deterministic instance that is indifferent to the instance with time variability . Besides, and are the mean and variance of the random variable , namely and . Therefore, we formally define such as variability premium in Definition 3.2, as our focus here is on mobility service time variability . This definition is consistent with the classical notion of risk premium in economic theory with focus on risks (Pratt 1964, Arrow and others 1965). Specifically, for a given mobility service, users are indifferent between the instance with time variability and the newly identified equivalent instance without variability , as shown by Figure 2.

Definition 3.2 (Variability premium)

The variability premium measures the amount of additional time a user is willing to pay beyond the expected time to eliminate the impact of time variability in a service, which mathematically satisfies .

Let , where is a standardized time variable with zero mean and . Following the terminology of Pratt (1964) in economics, can be viewed as the actuarially neutral variability, while the parameter serves as a scale parameter capturing the magnitude of this variability. Proposition 3.3 formalizes the concept of the variability premium in the context of time variability, building on the seminal works of Pratt (1964) and Arrow and others (1965), as well as subsequent developments in the transportation literature (Batley 2007, Beaud et al. 2016, Zang et al. 2026).

Proposition 3.3

Consider a service whose service time is a random variable with mean and variance . For a user with utility function of , the variability premium is given by

Proof 3.4

Proof. Since is developed to quantify the cost of time variability and is a measure of the variability, it is natural to posit a functional relationship between and , i.e., . Then,

Differentiating it with respect to once and twice yields, respectively

| (1) | |||

| (2) |

Since the absence of time variability implies zero variability premium, so when ,. Moreover, recalling that , it has following from Eq. (1); and we further drive by evaluating Eq. (2) at . Using second-order Taylor expansion, we obtain

This completes the proof.

It is worth to point out the term in Proposition 3.3 corresponds to the coefficient of absolute risk aversion (ARA) at time , which characterizes users’ intensity of risk aversion. Another typical measure of the intensity of risk aversion is the coefficient of relative risk aversion (RRA). Let and denote ARA and RRA wherein the subscript 2 represents the 2nd-order risk preference, respectively, then and are slightly different to their counterparts in the context of economic risks where , and . The negative sign in and is used to keep them positive as a risk averse customer has and . But under time variability, a risk averse user has and . So, there is no need of a negative sign.

| (3) |

Therefore, Proposition 3.3 provides an insightful decomposition of the variability premium, showing that the amount of additional time users are willing to pay to eliminate time variability depends on the first two moments (i.e., expected value and variance) of times and the absolute risk aversion (ARA). For a given service within a fixed period, different users usually experience the same mean and variance; consequently, heterogeneity in the variability premium arises primarily from differences in users’ risk-aversion intensities. Besides, though not explicitly captured in Proposition 3.3, prudence also plays an important role in shaping the variability premium as it reflects users’ propensity to allocate additional time as a precaution against time variability. The intensity of prudent preference is typically characterized by the coefficients of absolute prudence (AP) or relative prudence (RP) coefficient (Gollier 2001, Eeckhoudt et al. 2009). Similarly, let and denote AP and RP where the subscript represents the 3rd-order risk preference, then

| (4) |

where the negative sign in and is introduced to ensure that these measures remain positive. The above coefficients of (relative) risk aversion and prudence play important roles in quantifying users’ costs associated with time variability in mobility services, to be shown later in this paper. Up to this point, variability premium and its approximation have enabled us to quantify how users behaviorally respond to time variability and to quantify the costs that mobility service users incur due to time and its variability.

4 Bounding the inefficiency of time variability relative to no variability

When using mobility services, users typically incur a service cost. Accordingly, the users’ utility and expected utility from using a mobility service with random time can be expressed by:

| (5) | |||

| (6) |

where denotes the mobility service cost (e.g., ticket fare or booking fee) and is marginal utility of wealth.

4.1 The costs of time and time variability

4.1.1 The cost of time

With reference to Eq. (5), if is marginally increased from to , the resulting utility would be . Consequently, we can define the monetary value of time (VOT) at time as follows:

| (7) |

Based on the monetary VOT at time defined in Eq. (7), we can further obtain the (average) VOT, which quantifies the monetary value users place on time savings per time unit (Li et al. 2010). Namely,

| (8) |

Then, it is straightforward to compute the cost of time (COT) as

| (9) |

We note that in some studies the terms , and are used interchangeably. In this paper, however, we deliberately distinguish among these three concepts. Although they are closely related, they represent different quantities, and their relationships are clarified in Remark 4.1.

Remark 4.1 (Differences and relationship among , , and )

is the instantaneous monetary value of time evaluated at time ; represents the average monetary value that users place on time savings per unit of time; and denotes the total monetary amount users are willing to pay for the entire duration of the mobility service. Therefore, the is obtained by aggregating over time to be shown in Eq. (15); and is computed as the product of and the expected time spent for a mobility service, i.e., .

4.1.2 The cost of time variability

Based on Eqs. (5) and (6), we can use the following equation (10) to compute the additional monetary cost required to compensate for the utility loss induced by time variability, which is referred to as the cost of time variability (COTV).

| (10) |

By solving Eq. (10), we can obtain the expression of COTV, summarized in Lemma 4.2. The result is obtained by directly combining Eqs. (5) and (6) into Eq. (10).

Lemma 4.2

The cost of time variability can be calculated by:

So far, we have quantified the cost of using a mobility service without time variability (i.e., the ) and the additional cost incurred by time variability (i.e., the ). These two measures provide a solid foundation for examining the impact of time variability on users, thereby enabling us address our central question: how bad is time variability for users of mobility services?

4.2 The ratios

4.2.1 The ratio of the COTV to the COT

To quantify the extent to which time variability amplifies the cost experienced by users, we define as the ratio of the COTV to the COT:

| (11) |

Based on Eqs. (7), (9), and (10), together with Proposition 1, we can derive the mathematical expression for the ratio . The result is summarized in the following Proposition 4.3.

Proposition 4.3

For a mobility service with random time and a user with utility function , the ratio of the COTV to the COT can be approximated by

| (12) |

Proof 4.4

Proof. We first derive the formulation of . Combining three equations of (5), (7), and (8) gives

| (13) |

Then, by rearranging terms and based on , we can have

| (14) |

This implies that can be viewed as a function of ; denote . Then, the -th derivative of the function is expressed by . Using second-order Taylor series expansion to around yields:

| (15) |

where the is the defined VOT at time . Finally, it is straightforward to compute the COT as

| (16) |

Then, we derive the formulation of . Since , we have where . This representation allows us to view the as a function of , i.e., . Equivalently, we have . Then, the -th derivative of can be expressed by

| (17) |

Using the second-order Taylor expansion, we can obtain an approximation of as follows.

| (18) |

According to Eq. (7), we know . Finally, combining Eqs. (16) and (18) can obtain:

This completes the proof.

Two observations immediately follow from Proposition 4.3 and its proof. First, Eq. (18) provides a straightforward way to monetize the time unit-based variability premium into monetary cost. Namely, we offer an alternative estimation method of the based on the proposed variability premium and the at time as given by Eq. (7). This approach is particularly useful for incorporating the cost of time variability into cost–benefit analyses in transport project appraisal. For more details, please refer to Zang et al. (2026). Second, the result of depends critically on the derivatives of the utility function of time. As shown in Definition 3.1, users’ risk attitudes are characterized by these derivatives. In other words, risk attitudes play a central role in determining the magnitude of the ratio. Accordingly, when deriving the theoretical results in Section 5, we first examine the most widely used utility function in pioneering empirical and theoretical transportation studies, i.e., the quadratic utility function, and then extend the analysis to a general setting in which the utility function of time is assumed to be differentiable.

4.2.2 The ratio of the VOTV to the VOT

We note that the ratio captures the overall cost imposed on users by service time variability. However, in many practical settings, it is also important to consider the rate of return, in order to balance improvements in efficiency against efforts to eliminate variability. This consideration arises because demand for mobility services is derived demand; consequently, users typically face a limited time budget for mobility services. Motivated by this observation, we further examine the rate of return per unit of additional cost that users incur when hedging against time variability. This perspective allows us to compare the relative importance users attach to a marginal reduction in time variability versus a marginal reduction in mean time. We can notice that if we use variability premium as the valuation measure, Eq. (18) provides us a simple way to derive the value of time variability (VOTV), which quantifies the monetary value users place on a unit of reduction in time variability. That is, we have . Then, the ratio of the VOTV to VOT, which focuses on the rate of return, is given by is consistent with the so-called reliability ratio in existing valuation studies of travel time reliability (See e.g., Jackson and Jucker 1982, Fosgerau and Karlström 2010, Taylor 2017, Zang et al. 2022).:

| (19) |

5 Theoretical results

This section first derives the ratios under quadratic utility functions and then extends the analysis to more general settings with arbitrary differentiable utility functions..

5.1 Results under quadratic utilities

In the literature, the utility function of time in mobility service systems is typically assumed to be quadratic, as it provides analytical tractability while capturing second-order risk preferences commonly assumed in transport economics (See e.g. Jackson and Jucker 1982, Senna 1994, Yin et al. 2004, Beaud et al. 2016, Zang et al. 2022). Under this assumption, users’ decision making depends on no more than second-order information of time variability, and Remark 5.8 in next Section 5.2.1 will provide theoretical analysis for this. This is reasonable in practice. Indeed, even the second moment of time distribution, i.e., variance, are already difficult for users to understandAlthough variance is a commonly used measure in the mentioned VOR studies, it is challenging to communicate the extent of TTV clearly and simply to the public and thus there have been considerable efforts to design stated preference questionnaires to communicate the concept of TTV as straightforwardly as possible. See Li et al. (2010) and Carrion and Levinson (2012) for details. (FHWA 2006, Nevers and others 2014), let alone the higher moment information (e.g., skewness) of time variability. If users’ utility function is quadratic, we have and the ratio would reduces to

| (20) |

where . Here, the ratio depends linearly on the degree of users’ second-order risk preference, i.e., , and the degree of time variability, i.e., . To derive an upper bound for the ratio, we first consider a commonly assumed service process in both theoretical and practical studies of mobility service systems, i.e., the Poisson process; and then extend the analysis to other arbitrary service processes.

5.1.1 An upper bound of the ratio for mobility service under Poisson processes

Generally, mobility service operates as a stochastic process which usually involves queuing process of users due to its limited capacity. Consequently, service process in various mobility systems is typically modeled as the Poisson process, under which the service duration or service time of users follows the exponential distribution. For example, exponential distribution is widely used to theoretically and empirically model travel time of private cars, taxi, and bus or transit (e.g., Jackson and Jucker 1982, Noland and Small 1995, Yin and Ieda 2002, Benezech and Coulombel 2013, Qian et al. 2021), departure or arrival delay of bus or train or railway (e.g., Cai and Zhou 2014, Harrod et al. 2019), and waiting or queuing time in offline mobility services such as charging or tolling services and online mobility services such as ridesourcing or delivery (e.g., Guo and Zipkin 2007, Allon and Bassamboo 2011, Sá et al. 2019, Lin et al. 2023). In particular, Proposition 5.1 states that, if the mobility service follows a Poisson process, users with quadratic function will incur at most times more additional cost due to the existence of time variability. In other words, the total cost of mobility service under time variability is at most times that under the setting with no time variability. Furthermore, such upper bound is tight as the bound is attained when the utility function is pure quadratic (i.e., ). Namely, . To the best of our knowledge, this simple yet insightful upper bound has not been previously established in the literature.

Proposition 5.1

An expected-utility (EU) user with quadratic utility function will pay at most 1/2 of the cost of time as additional cost due to time variability in mobility systems whose service follows the Poisson process. Formally, , with equality attained for a pure quadratic utility function.

Proof 5.2

Proof. If users have a quadratic utility function of time, then it can be written as in which . According to Lemma 3.3 and noting that , the ratio can be simplified as

| (21) |

As introduced in Section 3.1, for , should be a non-increasing function. This implies that and or equivalently, and . Consequently, the maximum value of ratio based on Eq. (21) can be derived as follows

| (22) |

If the service of mobility systems follows a Poisson process, then the time of users involving in the service process will follow an exponential distribution. One key property of exponential distribution is that it has the same mean and standard deviation, implying . Therefore, we have . For a pure quadratic utility function, i.e., , the equality holds. This completes the proof.

5.1.2 An upper bound of the ratio for general mobility service

If no specific assumption is imposed on the service process of the mobility systems, we can derive a general result for the ratio under an arbitrary random service process, which is summarized in Corollary 5.3. Its proof follows directly from that of Proposition 5.1 and is therefore omitted.

Corollary 5.3

For an EU user with quadratic utility function, ; particularly, for a pure quadratic utility function, equality holds, i.e., .

Corollary 5.3 indicates that, for a risk-averse user, the COTV is at most times the COT. In other words, the upper bound of is exactly . Furthermore, such upper bound is tight as the equation is attained when the utility function is purely quadratic (i.e., ). Section 5.1.4 will discuss the underlying implications of Corollary 5.3.

5.1.3 Users value time variability reductions as much as time reductions

With respect to the benefits from time variability reduction and mean service time reduction, Corollary 5.4 shows that users obtain the same benefit per unit of time saved as the amount that they pay per unit of time variability reduced. Its proof is straightforward: when the utility function is quadratic, the ratio defined in Eq. (19) would be 1, since .

Corollary 5.4

For risk-averse EU users with quadratic utility function, the value of time variability equals the value of time. Namely, .

The result given by Corollary 5.4 actually provides a theoretical support for a commonly stated claim in the literature (see e.g., Chen et al. 2023, Zang et al. 2026) highlighting the importance of accounting for the COTV: users value time variability reductions as much as, if not more than, time savings. In addition, it also lends theoretical justification to the prevalent practice in reliability-based network design problem, where the same assumed VOT coefficient is directly used to transfer the additional time for hedging against time variability to monetary costs (e.g., Yan et al. (2013)). For more details, please see a review paper of Chen et al. (2011). Remark 5.8 in 5.2.1 elaborates on the underlying theoretical implications of adopting a quadratic utility specification for users in mobility service systems.

5.1.4 Implications of special results of and

According to Wardman et al. (2016), the congestion multiplier in travel time valuation is the ratio of the VOT with congestion to the VOT without congestion. Many empirical studies report 1.5 as the central value of the congestion multiplier (Wardman et al. 2016) and this parameter plays a pivotal role in transport project. Thus, recalling the definition of , we can find is quite close to the congestion multiplier. The consistency between our theoretical result of and empirical value of implies that, for most mobility services or project appraisals involving a group of users, it is reasonable to assume that (1) the service process of transport systems can be approximated by a Poisson process and (2) the intensity of users’ risk aversion satisfies , as formalized in Lemma 5.7 in next section, which implies users make decisions with consideration of no more than first two moments, i.e., mean and variance. Equivalently, these users treat time variability as a small risk in everyday travel decisions. They therefore favor routes with lower variability, but are willing to tolerate moderate variability when its elimination requires disproportionate cost. However, for a specific user, higher-order risk preference may be important for various reasons, such as greater variability inherent in the mobility service under special events (e.g., disasters) or the importance of the purpose of travel (e.g., business travel). In such scenarios, users may exhibit and large for users, which corresponds to the general result given in Eq. (20). This explains why premium service prices in practice can be several times higher than those of regular service, such as the price differentials between regular trains and high-speed trains, or between bus rapid transit service and regular buse service.

5.2 General results for users with differentiable utility functions

In this section, we consider a general setting where users’ utility functions are assumed only to be differentiable. That is, we relax the assumptions on both the functional form of the utility and service process. Proposition 5.5 shows that the ratio generally depends on coefficient of variation (CV), RRA coefficient, and RP coefficient. Note that RRA coefficient, and RP coefficient are defined by derivatives of utility functions of time as introduced in Section 3.1.

Proposition 5.5

Suppose users are risk-averse under the EU framework for the service instance , then

where and are coefficients of RRA and RP, respectively.

Proof 5.6

Proof. By rearranging terms and substituting for using the Lemma 3.3, we have

Since we have defined RRA coefficient and RP coefficient , the ratio is

This completes the proof.

For a service in a certain period, its is an objective measure and thus can be viewed as a fixed value for all users. Consequently, the magnitude of the ratio for a specific service primarily depends on users’ intensity of risk preferences. Importantly, benchmark values of the coefficients of relative risk aversion (RRA) and prudence (RP) can be identified to categorize the intensity of users’ risk preferences. These benchmark values serve as thresholds that distinguish how users trade off reductions associated with different moments of the time distribution. Particularly, reductions in mean, variance, and skewness respectively reflect users’ preferences for shorter average times, lower dispersion of outcomes, and reduced exposure to extreme delays. Table 1 summarizes the moment reductions in time variability and interpret them in terms of distributional change, user concern, and risk preference.

| Moment reduced | Distributional change | User concern | Risk preference |

|---|---|---|---|

| Mean | Leftward shift of the time distribution | Lower average time | Risk neutral |

| Variance | Contraction of the distribution around the mean | Lower dispersion or volatility of outcomes | Second-order risk preference (risk aversion) |

| Skewness | Reduction in the right-tail mass | Lower exposure to extreme delays | Third-order risk preference (prudence) |

5.2.1 Benchmark value of RRA coefficient and its interpretation

Lemma 5.7 provides the benchmark value, i.e., , to partition risk-averse users into different groups according to the degree of RRA. Its proof follows directly from Eeckhoudt et al. (2009) and Eeckhoudt et al. (2009).

Lemma 5.7 (Gollier (2001) and Eeckhoudt et al. (2009))

For an EU risk-averse user, the benchmark value of RRA coefficient governing the trade-off between time reductions and variance reductions is .

In practice, such benchmark value of 1 serves as a natural threshold value for distinguishing how users trade off mean time savings against variance reductions. Based on Lemma 5.7, two cases can be considered. When , we have , indicating a higher intensity of risk aversion. In this case, the marginal benefit of reducing second moment (i.e., variance) exceeds that of reducing the first moment (i.e., mean). Conversely, means , indicating that users prefer first moment reductions to second moment reductions. Indeed, the case of corresponds exactly to the users with quadratic utility functions in Section 5.1. Based on these observations, Remark 5.8 further elucidates the implications of quadratic utility function for risk-averse users in terms of risk and moments reduction preferences.

Remark 5.8 (users’ risk preferences under quadratic utility function)

Consider the vertex form of quadratic utility function: where and are coordinates of the vertex. We assume and . Based on the vertex form, the expected utility can be expressed as a function of mean and variance of time as follows:

| (23) |

If we ignore the term in the right-hand side of Eq. (23), we can clearly see that the changes of mean and variance affect values symmetrically, which corresponds to the case of . However, as we all know, the shift of in Eq. (23) can change the mean value but has no effects on the variance . This asymmetry explains why we have for general quadratic utility function, which in turn underlies the results in Proposition 5.1 and Corollary 5.3. In other words, although users with quadratic utility functions dislike time variability, they tend to prioritize mean time savings over variability reductions.

5.2.2 Benchmark value of RP coefficient and its interpretation

Proposition 5.9 establishes 2 as the benchmark value of RP coefficient and its proof is based on the idea of using multiplicative lotteries and the principle of harm dis-aggregation (Eeckhoudt et al. 2009).

Proposition 5.9

For an EU risk-averse and prudent user, the benchmark value of RP coefficient governing the trade-off between reducing second moment and reducing third moment is .

Proof 5.10

Proof. Consider a user facing the choice of two instances and , as shown in Figure 3, for a mobility service. In Figure 3, is the initial time of this service with no time variability; represents a deterministic time and is a zero-mean variability with . By construction, and have the same expected service time, while has lower variance but higher skewness than .

If one user prefers to , then it means:

Namely, we have

Denoting , we have to show for all . So, its partial derivative in terms of should be non-positive, namely

By rearrangement, we have . Now, let us define , then it implies . In other words, should be a convex function with respect to .

By rearrangement, we can further have the following inequality:

Let , then we have . This completes the proof.

Proposition 5.9 and its proof show that, if RP coefficient , for the same expected time, users prefer an alternative choice with a lower skewness, even it has higher variance. On the contrary, if , users prefer an alternative choice with a higher variance even it has lower skewness. Consequently, serves as a benchmark value for the balance between reducing second moment and reducing third moment. Although skewness-related behavior received limited attention in theoretical transport studies, it has been recognized by empirical studies, such as Van Lint and van Zuylen (2005) and Van Lint et al. (2008). Furthermore, extensive studies have reported the right-skewed tail of travel time distributions in the literature (e.g., Van Lint and van Zuylen 2005, Susilawati et al. 2013, Zang et al. 2024). The benchmark values of RRA and RP provide a useful baseline for characterizing the intensity of different risk attitudes. In particular, empirically estimated ratios, such as those obtained from stated-preference surveys, can be compared against these benchmark values to facilitate interpretation. As discussed in Zang et al. (2022), a wide range of models requires users’ risk parameters as inputs, including the preference parameters in VOR models, the probabilities needed for reliability measures, and the risk parameters in route choice models. However, specifying these values ex ante is challenging, and in many cases it is even impractical to gather each user’s parameters through surveys, as users may not even be aware of their precise values and also these parameters may vary rather than remain fixed. The proposed benchmark provides a practical reference point, enabling the identifications of users’ risk preferences through long-term and large-scale individual-level datasets collected through non-survey-based approaches, such as GPS and cellular data.

5.2.3 The rate of return from reducing time variability

With general differentiable utility functions, the reliability ratio can be expressed as follows:

We can thus derive Corollary 5.11, which shows that higher-order risk preference is associated with diminishing marginal benefits from reducing time variability. Specifically, although stronger higher-order risk preferences lead users to incur larger additional time costs to hedge against variability, the marginal benefit of further reductions in time variability becomes smaller. This result is intuitive: as mobility services represent the derived demand undertaken to achieve other objectives, consuming the service itself does not generate intrinsic utility. In addition, such a diminishing marginal effect is widely observed in other related scenarios. For example, in studies of the value of travel time and travel time reliability, Metz (2008) found that the additional benefit derived from further travel time savings tends to diminish, while Zang et al. (2024) found that the additional benefit derived from further improving travel time reliability also becomes diminishing. Furthermore, within the framework of reliable network design, Xu et al. (2014) identified a diminishing marginal effect of improving network reliability performance relative to the construction budget.

Corollary 5.11

For risk-averse and prudent EU users, the marginal benefit of reducing time variability is at most times that of the marginal benefit of reducing time. Namely, .

Proof 5.12

Proof. If users dislike longer time, then by definition we have . It follows from Eq. (15) that . Namely,

where the second inequality and the third inequality are implied by and , respectively. With the definition of RRA coefficient and RP coefficient, we could have

That is, we have and therefore . This completes the proof.

6 Extensions to non-expected utility models

This section extends the proposed framework to non-expected utility models. We first examine the dual theory (DT; Yaari (1987)), which captures users’ perceptions of probabilities, and then consider the more general rank-dependent utility (RDU; Quiggin (1982)). Note that the RDU encompasses both EU and DT as special cases and forms the basis of prospect theory (Tversky and Kahneman 1992). Below we first introduce dual moments, which play a vital role in generalizing the results derived under EU models to non-EU model settings, as will be demonstrated in Sections 6.2 and 6.3.

6.1 Dual moments

For time with CDF , its first and second moments, and , can be written by

Following Eeckhoudt and Laeven (2022), if we treat as a primal moment, the associated dual moment can be written as

| (24) |

Therefore, a more precise terminology for is the second dual moment about the meanEeckhoudt and Laeven (2022) termed such dual moment as the maxiance in the vein of the variance as represents the expected best outcome obtained from two independent draws of random times. of . Note that is the CDF of maximum of independent and identically distributed random time. If we only consider and as two independent copies of , the dual moment can be also written as

| (25) |

Eq. (25) shows that admits an order-statistic interpretation: it equals the expected value of the largest outcome from two independent draws of the risk. For more details of mean order statistics in the statistics literature, we refer the readers to David and Nagaraja (2004). Similarly, the second dual moment about the variance of should be computed as

| (26) |

Consider two independent copies and of again, we have . Specifically, if we only consider the zero mean variability in random time, to be shown in next section, then we have

6.2 Results under dual theory

Under EU framework, random service time is characterized by its probability distribution, specified by the the PDF and the CDF . In practice, however, users often perceive event probabilities only; they may overestimate some probabilities while underestimating others. To capture this behavior, dual theory (DT) replaces the CDF with where the probability weighting function : satisfies the following conditions: . Then, the utility representation of a user for random time under DT is

| (27) |

where strict concavity, i.e., , implies aversion to mean-preserving spreads, which is analogous to the risk aversion in EU framework (i.e., ).

6.2.1 Dual moments and variability premium

Under DT, variability is introduced through probability (i.e., small probabilities attached to fixed payoffs), which is dual to the case of EU in which variability arises from random payoffs with equal probability. For illustration purpose, Figure 4 presents illustrative examples of binary variability under EU and DT cases, highlighting their differences and underlying relationships for the same certain instance .

Let us consider a more general instance, in which there are possible outcomes. Specifically, we have with probability , with probability , with probability , and all other outcomes with 0 as probability. Then, dual zero mean n-state variability is added into instance. Specifically, possible outcomes are in ascending order, i.e., ; is assumed to be and we assume each of possible outcomes occur with the equal probability of .The service change due to dual variability is illustrated in Figure 5. As we allow adjacent states to be the same, such variability can be viewed as variability with unequal state probability as well. In addition, though we use discrete representations, it naturally extends to continuous representations if . Specifically, if , it will be completely the same as instances illustrated in Figure 1; this is how we can generalize the following analysis to add variability to all probability. From the perspective of DT, it is conceptually more appropriate to formulate the analysis in terms of changes affecting only a portion of the probability distribution, rather than uniformly perturbing all probabilities.

According to definitions and formulations of dual moments introduced in Section 6.1 (i.e., mainly Eq. (24)), the dual moment of variability can be given by

| (28) |

Then, as illustrated by Figure 6, the variability premium under dual theory is defined such that users are indifferent between risky instance and the corresponding certain instance. Proposition 6.1 gives the formulation of under DT.

Proposition 6.1

For a service with random service time , the variability premium of a DT user with probability weighting function can be approximated by

Proof 6.2

Proof. If DT users are indifferent between risky instance and certain instance as shown in Figure 6, it indicates that

| (29) |

By solving this equation, we can derive

Applying second-order Taylor expansion to and at , we can obtain the following expression:

Similarly, we have by invoking second-order Taylor expansion at . Consequently, is given by

where is the dual moment about the mean of risk . Now, we consider adding dual variability to all possible times, and thus we have . As a result, . This completes the proof.

As shown by Proposition 3.2, the primal moment, variance, plays a fundamental measure of time variability under EU. In contrast, Proposition 6.1 shows that the second dual moment plays an analogous role under the dual theory, standing on equal footing with variance as the fundamental measure of time variability (Eeckhoudt and Laeven 2022).

6.2.2 COT, COTV, and the ratio under dual theory

As the utility function of DT is linear, so the key difference between and is that in is replaced by in . Thus, based on Eq. (6), the expected utility of DT is given by

| (30) |

and thus the VOT and COTV can be calculated by and . Based on the above results, Proposition 6.3 gives the formulation of the ratio of the COTV to COT.

Proposition 6.3

For DT risk-averse users, the ratio depends on CV of random times and dual risk aversion parameters only:

Proof 6.4

Interestingly, the result of is quite similar to that under EU framework with quadratic utility function in Eq. (20) of Section 5.1. Namely, under DT framework, the ratio also depends on the degree of time variability and users’ second-order preference of risk. Specifically, for a DT risk-averse user, the second dual moment is as significant as the variance in measuring COTV for mobility services. Based on the modeling rationality of EU and DT, we can find that the variance quantifies time variability in terms of “payoff plane” (i.e., time), the second dual moment represents a measure of time variability in terms of “probability plane” (i.e., perceived probability). With respect to quantifying users’ preference, EU measures it through second-order risk preference embodied in utility function, while DT characterize them through second-order “weighting” of perception about probability.

6.3 Results under rank dependent model

Although the dual theory (DT) is able to address the common ratio effect, it lacks coherence. A more general and behaviorally realistic framework is the rank dependent utility (RDU) model. The key distinction between RDU and DT lies in the treatment of utility: RDU replaces the linear utility in DT with a general utility function. Accordingly, the expected utility under RDU is written as

| (33) |

Proposition 6.5 gives the formulation of under RDU, which makes users indifferent between risky instance and the corresponding certain instance.

Proposition 6.5

For a mobility service with random service time , the variability premium of an RDU user with probability weighting function can be approximated by

| (34) |

Proof 6.6

Proof. If RDU users are indifferent between the risky instance (as in Figure 6) and a newly corresponding certain instance, it means

| (35) |

Following Eeckhoudt and Laeven (2022), we apply second-order Taylor expansion to at , and at , and at , and first-order Taylor expansion to at . Then, we can obtain the solution to the above equation as

After simplification (see Appendix for the detailed derivations), we can have:

where , and are primal second moment, second dual moment about mean, and second dual moment about variance defined in Section 6.1. Now, we consider adding variability to all possible times, and thus we have . Then, the resulting expression is given in Eq. (34).

Note that and under RDU can be estimated by following the same process used to estimate and under EU in Section 4. Consequently, we have Proposition 6.7.

Proposition 6.7

For RDU risk-averse users, the ratio depends on CV of random times and dual risk aversion parameters only:

where is the parameter of the to the .

Proof 6.8

Proof. For random times under RDU framework, we let where and are mean and variance under . Then, according to the proof of Proposition 4.3, we have

Note that is right-hand side of Eq. (35). By invoking first order Taylor expansion, the COTV is further written as

Let be the parameter of the to the . The ratio of under RDU can be reformulated as

This completes the proof.

Proposition 6.7 demonstrates that, for a RDU risk-averse user, the result of is also structurally similar to that under EU framework. In particular, it depends on the degree of time variability and users’ preferences. Specifically, both the first and second primal moments and the first and second dual moments jointly determine the COTV for mobility services. Accordingly, both users’ preference in terms of utility function and “weighting” function of perception about probability are important. We can thus observe the relationship among the results of the ratio between EU, DT and RDU frameworks according to Propositions 5.5, 6.3 and 6.7. For RDU users characterized by Eq. (33), if we use to replace , then RDU would reduce to EU model. Accordingly, the result in Proposition 6.7 reduces to Proposition 5.5. Alternatively, if we use to replace in Eq. (33), then RDU would reduce to DT model. Accordingly, the result in Proposition 6.7 reduces to Proposition 6.3. In short, in either DT or EU model, the last term in Proposition 6.7 under RDU framework, which captures the intersection of DT and EU in measuring time variability and users’ preference, vanishes.

7 Conclusion

This paper investigates the economic consequences of time variability in mobility services, with the aim of clarifying how users are affected by uncertainty in service times. Our analysis shows that time variability does not affect users arbitrarily: its economic impact follows a structured and predictable pattern jointly shaped by service time variability and behavioral attitudes toward risk. In a commonly adopted special case—quadratic utility combined with a Poisson service process—we showed that the total user cost under time variability does not exceed of the deterministic benchmark. More generally, without assumptions on the service process, variability costs scale with relative to time costs. These results indicate that substantial welfare losses arise primarily when variability is large relative to mean service time, whereas moderate variability leads to proportionate and predictable impacts. Under quadratic utility, we further found that the marginal benefit of reducing variability is equal to that of reducing mean time. This finding provides theoretical support for the claim commonly used in the literature (see e.g., Chen et al. 2023, Zang et al. 2026) highlighting the importance of considering the COTV: users value time variability reductions as much as, if not more than, they value time savings. Beyond this special case, we show that the ratio of COTV to COT depends on the coefficient of variation (CV) of times and on users’ higher-order risk preferences, captured by relative risk aversion (RRA) and relative prudence (RP). Benchmark values of these parameters provide a useful basis for distinguishing how users trade off reductions in mean, variance, and skewness. When sensitivity to higher-order risk becomes pronounced, diminishing marginal effects emerge: for risk-averse and prudent users, the marginal benefit of reducing time variability is bounded by of the marginal benefit of reducing mean time. Finally, extending the analysis to non–EU models, including DT and RDU, shows that these insights are robust across alternative behavioral representations. Although variability and preferences are modeled differently, the structural dependence of variability costs on relative dispersion and risk attitudes remains intact. From a practical standpoint, characterizing the maximum economic loss associated with time variability offers a useful complement to existing valuation methods, particularly in settings where detailed data are limited and decisions must be made at an early stage. Moreover, the derived bounds provide a principled upper limit on users’ willingness to pay for reliability improvements, offering guidance for investment prioritization and the pricing and design of reliability-oriented mobility services.

Appendix

Acknowledgement

This research is supported by the National Research Foundation, Singapore under its AI Singapore Pro- gramme (AISG Award No:AISG3-RP-2022-031).

References

- The impact of delaying the delay announcements. Operations Research 59 (5), pp. 1198–1210. Cited by: §5.1.1.

- Waiting time and headway modelling for urban transit systems–a critical review and proposed approach. Transport Reviews 41 (2), pp. 141–163. Cited by: §1, §2.1.

- Aspects of the theory of risk-bearing. Helsinki: Yrjö Jahnssonin Säätiö. Cited by: §3.1, §3.2, §3.2.

- The valuation of reliability for personal travel. Transportation Research Part E: Logistics and Transportation Review 37 (2-3), pp. 191–229. Cited by: §2.2.

- Marginal valuations of travel time and scheduling, and the reliability premium. Transportation Research Part E: Logistics and Transportation Review 43 (4), pp. 387–408. Cited by: §3.2.

- The impact of travel time variability and travelers’ risk attitudes on the values of time and reliability. Transportation Research Part B: Methodological 93, pp. 207–224. Cited by: §2.2, §3.1, §3.2, §5.1.

- The value of service reliability. Transportation Research Part B: Methodological 58, pp. 1–15. Cited by: §5.1.1.

- Optimal policies for perishable products when transportation to export market is disrupted. Production and Operations Management 23 (5), pp. 907–923. Cited by: §5.1.1.

- Value of travel time reliability: a review of current evidence. Transportation Research Part A: Policy and Practice 46 (4), pp. 720–741. Cited by: §1, §2.1, §2.2, §5.1.

- Modeling the impacts of public transport reliability and travel information on passengers’ waiting-time uncertainty. EURO Journal on Transportation and Logistics 6 (3), pp. 247–270. Cited by: §2.1.

- Transport network design problem under uncertainty: a review and new developments. Transport Reviews 31 (6), pp. 743–768. Cited by: §5.1.3.

- A conservative expected travel time approach for traffic information dissemination under uncertainty. Transportmetrica B: Transport Dynamics 11 (1), pp. 211–230. Cited by: §5.1.3, §7.

- Sooner or later? promising delivery speed in online retail. Manufacturing & Service Operations Management 26 (1), pp. 233–251. Cited by: §2.1.

- Order statistics. John Wiley & Sons. Cited by: §6.1.

- On including travel time reliability of road traffic in appraisal. Transportation Research Part A: Policy and Practice 73, pp. 80–95. Cited by: §1, §2.1.

- The value of travel time and reliability-evidence from a stated preference survey and actual usage. Transportation Research Part A: Policy and Practice 46 (8), pp. 1227–1240. Cited by: §2.1.

- The values of relative risk aversion and prudence: a context-free interpretation. Mathematical Social Sciences 58 (1), pp. 1–7. Cited by: §3.2, §5.2.1, §5.2.2, Lemma 5.7.

- Dual moments and risk attitudes. Operations Research 70 (3), pp. 1330–1341. Cited by: §6.1, §6.1, §6.2.1, Proof 6.6.

- Putting risk in its proper place. American Economic Review 96 (1), pp. 280–289. Cited by: §3.1, §3.1.

- The cost of travel time variability: three measures with properties. Transportation Research Part B: Methodological 91, pp. 555–564. Cited by: §2.2.

- Waiting time and headway modeling considering unreliability in transit service. Transportation Research Part A: Policy and Practice 155, pp. 219–233. Cited by: §2.1.

- Waiting time perceptions at transit stops and stations: effects of basic amenities, gender, and security. Transportation Research Part A: Policy and Practice 88, pp. 251–264. Cited by: §2.1.

- Travel time reliability: making it there on time, all the time. Technical report Federal Highway Administration, US Department of Transportation, Washington, D.C. External Links: Link Cited by: §5.1.

- The value of reliability. Transportation Research Part B: Methodological 44 (1), pp. 38–49. Cited by: §2.2, §4.2.2.

- Travel time reliability for stockholm roadways: modeling mean lateness factor. Transportation Research Record 2134 (1), pp. 106–113. Cited by: §2.1.

- Headstart strategies for combating congestion. Transportation Science 2 (2), pp. 172–181. Cited by: §2.2, §3.2.

- Airport security screening and changing passenger satisfaction: an exploratory assessment. Journal of Air Transport Management 12 (5), pp. 213–219. Cited by: §2.1.

- The economics of risk and time. MIT press. Cited by: §3.1, §3.2, Lemma 5.7.

- Analysis and comparison of queues with different levels of delay information. Management Science 53 (6), pp. 962–970. Cited by: §5.1.1.

- A closed form railway line delay propagation model. Transportation Research Part C: Emerging Technologies 102, pp. 189–209. Cited by: §5.1.1.

- Trip time characteristics of journeys to and from work. Transportation and traffic theory 6, pp. 57–86. Cited by: §2.1.

- An empirical study of travel time variability and travel choice behavior. Transportation Science 16 (4), pp. 460–475. Cited by: §2.2, §4.2.2, §5.1.1, §5.1.

- The value of travel time variability with trip chains, flexible scheduling and correlated travel times. Transportation Research Part B: Methodological 46 (6), pp. 762–780. Cited by: §2.2.

- Stochastic dynamic itinerary interception refueling location problem with queue delay for electric taxi charging stations. Transportation Research Part C: Emerging Technologies 40, pp. 123–142. Cited by: §1, §2.1.

- Precautionary saving in the small and in the large. Econometrica 58, pp. 53–73. Cited by: §3.1.

- An approach to the evaluation of changes in travel unreliability: a “safety margin” hypothesis. Transportation 3 (4), pp. 393–408. Cited by: §2.2.

- The user costs of air travel delay variability. Transportation Science 50 (1), pp. 120–131. Cited by: §1.

- Toward a comprehensive assessment of road pricing accounting for land use. Brookings-Wharton Papers on Urban Affairs, pp. 127–175. Cited by: §1.

- Willingness to pay for travel time reliability in passenger transport: a review and some new empirical evidence. Transportation Research Part E: Logistics and Transportation Review 46 (3), pp. 384–403. Cited by: §1, §2.2, §4.1.1, §5.1.

- Embedding risk attitudes in a scheduling model: application to the study of commuting departure time. Transportation science 46 (2), pp. 170–188. Cited by: §2.2.

- Wait time–based pricing for queues with customer-chosen service times. Management Science 69 (4), pp. 2127–2146. Cited by: §5.1.1.

- Degradable transport network: travel time budget of travelers with heterogeneous risk aversion. Transportation Research Part B: Methodological 40 (9), pp. 792–806. Cited by: §3.2.

- The myth of travel time saving. Transport reviews 28 (3), pp. 321–336. Cited by: §5.2.3.

- Smart charging strategy for electric vehicle charging stations. IEEE Transactions on Transportation Electrification 4 (1), pp. 76–88. Cited by: §2.1.

- Guide to establishing monitoring programs for travel time reliability. Transportation Research Board. Cited by: §5.1.

- Fear and loathing of electric vehicles: the reactionary rhetoric of range anxiety. Energy Research & Social Science 48, pp. 96–107. Cited by: §2.1.

- Travel-time uncertainty, departure time choice, and the cost of morning commutes. Transportation Research Record 1493, pp. 150–158. Cited by: §2.2, §5.1.1.

- Economic evaluation manual. Wellington: New Zealand Transport Agency. Cited by: §1, §2.1.

- Risk aversion in the small and in the large. Econometrica 32 (1/2), pp. 122–136. Cited by: §3.1, §3.2, §3.2.

- Scaling of contact networks for epidemic spreading in urban transit systems. Scientific Reports 11 (1), pp. 4408. Cited by: §5.1.1.

- A theory of anticipated utility. Journal of Economic Behavior & Organization 3 (4), pp. 323–343. Cited by: §1, §6.

- Dynamic hospital competition under rationing by waiting times. Journal of Health Economics 66, pp. 260–282. Cited by: §5.1.1.

- The influence of travel time variability on the value of time. Transportation 21 (2), pp. 203–228. Cited by: §2.2, §5.1.

- The scheduling of consumer activities: work trips. The American Economic Review 72 (3), pp. 467–479. Cited by: §2.2.

- Distributions of travel time variability on urban roads. Journal of Advanced Transportation 47 (8), pp. 720–736. Cited by: §5.2.2.

- Fosgerau’s travel time reliability ratio and the burr distribution. Transportation Research Part B: Methodological 97, pp. 50–63. Cited by: §4.2.2.

- Advances in prospect theory: cumulative representation of uncertainty. Journal of Risk and Uncertainty 5, pp. 297–323. Cited by: §6.

- Travel time unreliability on freeways: why measures based on variance tell only half the story. Transportation Research Part A: Policy and Practice 42 (1), pp. 258–277. Cited by: §2.1, §5.2.2.

- Monitoring and predicting freeway travel time reliability: using width and skew of day-to-day travel time distribution. Transportation Research Record 1917 (1), pp. 54–62. Cited by: §5.2.2.

- Congestion theory and transport investment. The American Economic Review, pp. 251–260. Cited by: §2.2.

- Values of travel time in europe: review and meta-analysis. Transportation Research Part A: Policy and Practice 94, pp. 93–111. Cited by: §5.1.4.

- On the performance of the us transportation system: caution ahead. Journal of Economic Literature 51 (3), pp. 773–824. Cited by: §1.

- Modeling distribution tail in network performance assessment: a mean-excess total travel time risk measure and analytical estimation method. Transportation Research Part B: Methodological 66, pp. 32–49. Cited by: §5.2.3.

- Longer waiting, more cancellation? empirical evidence from an on-demand service platform. Journal of Business Research 126, pp. 162–169. Cited by: §1, §2.1.

- The dual theory of choice under risk. Econometrica: Journal of the Econometric Society, pp. 95–115. Cited by: §1, §6.

- Robust optimization model of bus transit network design with stochastic travel time. Journal of Transportation Engineering 139 (6), pp. 625–634. Cited by: §5.1.3.

- Optimal improvement scheme for network reliability. Transportation Research Record 1783 (1), pp. 1–6. Cited by: §5.1.1.

- New technology and the modeling of risk-taking behavior in congested road networks. Transportation Research Part C: Emerging Technologies 12 (3-4), pp. 171–192. Cited by: §5.1.

- Dynamic tolling strategies for managed lanes. Journal of Transportation Engineering 135 (2), pp. 45–52. Cited by: §1.

- Managing customer expectations and priorities in service systems. Management Science 64 (8), pp. 3942–3970. Cited by: §1.

- Delay information in virtual queues: a large-scale field experiment on a major ride-sharing platform. Management Science 68 (8), pp. 5745–5757. Cited by: §1, §2.1.

- Reliability premium: a generic conceptual framework for evaluating the cost of travel time variability. Transportation Research Part B: Methodological 205, pp. 103408. Cited by: §2.1, §2.2, §3.2, §3.2, §4.2.1, §5.1.3, §7.

- On the value of distribution tail in the valuation of travel time variability. Transportation Research Part E: Logistics and Transportation Review 190, pp. 103695. Cited by: §2.1, §2.2, §5.2.2, §5.2.3.

- Travel time reliability in transportation networks: a review of methodological developments. Transportation Research Part C: Emerging Technologies 143, pp. 103866. Cited by: §1, §2.2, §4.2.2, §5.1, §5.2.2.