Beyond the Markovian Assumption: Robust Optimization via Fractional Weyl Integrals in Imbalanced Data

Abstract

Standard Gradient Descent and its modern variants assume local, Markovian weight updates, making them highly susceptible to noise and overfitting. This limitation becomes critically severe in extremely imbalanced datasets—such as financial fraud detection—where dominant class gradients systematically overwrite the subtle signals of the minority class. In this paper, we introduce a novel optimization algorithm grounded in Fractional Calculus. By isolating the core memory engine of the generalized fractional derivative—the Weighted Fractional Weyl Integral—we replace the instantaneous gradient with a dynamically weighted historical sequence. This fractional memory operator acts as a natural regularizer. Empirical evaluations demonstrate that our method prevents overfitting in medical diagnostics and achieves a 40% improvement in PR-AUC over classical optimizers in financial fraud detection, establishing a robust bridge between pure fractional topology and applied Machine Learning.

1 Introduction

The optimization of non-convex objective functions is the cornerstone of modern Machine Learning (ML). While first-order methods like Stochastic Gradient Descent (SGD) and its adaptive variants have achieved remarkable success, they are inherently limited by their Markovian nature. These algorithms rely on instantaneous gradient evaluations or exponentially decaying moving averages, making them highly susceptible to noise and gradient vanishing in complex topographies. This limitation is particularly detrimental in highly imbalanced datasets, where majority-class gradients overwrite minority-class signals.

Recent advancements have explored Fractional Calculus as a mathematical framework to introduce non-local memory into optimization algorithms. In prior work [1], a generalized Fractional Gradient was formalized. To define this derivative, the framework identifies the first-order differential operator acting as the infinitesimal generator of the weighted system, given by:

| (1) |

While this operator elegantly captures the continuous topological dynamics of the system, transitioning it to stochastic, high-noise computational environments—such as mini-batch ML—reveals a mechanical challenge. Applying the differential component to the highly discontinuous and noisy sequence of stochastic gradients intrinsically amplifies variance, causing the optimizer to diverge in complex topographies.

In this paper, we propose a paradigm shift: rather than utilizing the complete fractional derivative generated by , we isolate its inverse core memory engine—the Weighted Fractional Weyl Integral () introduced in [2]. By bypassing the infinitesimal generator and relying purely on the integral operator to accumulate a weighted history of classical gradients, we eliminate noise amplification while preserving a robust, long-term memory mechanism governed by a power-law decay.

We demonstrate that treating the Fractional Weyl Integral as a dynamic momentum operator transforms standard gradient descent into a highly resilient optimizer. Specifically, the introduction of a memory parameter , a spatial deformation function , and a historical weight decay , acts as an implicit regularizer.

Our main contributions are as follows:

-

•

We establish a novel mathematical bridge between pure fractional calculus and applied ML optimization by redefining the effective gradient through the Weighted Weyl Integral.

-

•

We empirically demonstrate that this integral approach prevents overfitting and stabilizes convergence in standard datasets (e.g., Breast Cancer diagnostics).

-

•

We show that our proposed optimizer outperforms classical gradient descent in extreme class-imbalance scenarios, achieving a 40% improvement in PR-AUC on a financial fraud detection task by successfully shielding minority-class gradients from majority-class noise.

2 Mathematical Framework and Proposed Method

In standard Machine Learning optimization, models update their parameters by descending the stochastic gradient of a loss function . At any epoch or iteration , the instantaneous gradient is . The classical update rule is strictly Markovian:

| (2) |

where is the learning rate. In environments with extreme class imbalance or high stochasticity, becomes highly oscillatory, leading to divergence or overfitting to the majority class. To overcome this, we redefine the effective gradient by applying a non-local fractional operator over the historical sequence of gradients.

2.1 The Weighted -Weyl Integral vs. Riemann-Liouville

While previous works in fractional optimization have explored Riemann-Liouville or Caputo derivatives (which are strictly bounded to a finite interval ), we ground our approach in the Weyl fractional integral. The Weyl operator naturally spans the entire semi-axis , providing a mathematically rigorous framework for unbounded historical memory.

Following the conjugation approach for weighted operators [1], we introduce the scale function (a strictly increasing -diffeomorphism) and a continuous weight function .

Definition 1 (Weighted -Weyl Integral). Let be the fractional memory order. We define the integral operator acting on the gradient sequence via its explicit integral representation:

| (3) |

Theorem 1 (Existence and Stability). Let be the weighted Lebesgue space defined by the norm . As established via the conjugation map isometric isomorphism in [1], for any bounded sequence of stochastic gradients , the weighted Weyl integral converges absolutely.

2.2 The Proposed Update Rule: Causal Fractional Momentum

To translate Eq. 3 into a computable update rule for neural networks, we treat the optimization process as a causal dynamical system. We define the pre-initialization gradient history as strictly zero: for all . Consequently, while the Weyl operator fundamentally evaluates the infinite past , the non-zero contribution is naturally localized to .

By mapping the mathematical formalism to the mechanics of neural network optimization, the components of our causal Weyl operator act as dynamic regularizers:

-

•

The Kernel : Unlike classical ML momentum which decays exponentially, the fractional Weyl kernel imposes a power-law decay. This allows the model to retain a persistent memory of minority-class gradients while smoothing out the high-frequency noise of the majority class.

-

•

The Time-Warping Scale : Compresses or stretches the perception of historical time.

-

•

The Historical Weight : Dictates the relative importance of gradients at different stages of the training process.

Crucially, to preserve the physical and causal arrow of time, the temporal scale deformation is evaluated with respect to the age of the memory rather than the absolute calendar time. By defining the integration variable in terms of elapsed time from a past gradient evaluation to the present update, the operator avoids amplifying ancient noise. Using a logarithmic scale such as ensures that the optimization engine acts as a high-resolution magnifying glass for recent, relevant gradients while heavily compressing the distant past into a stable contextual baseline.

We formally propose the Weighted Weyl Optimizer. The raw instantaneous gradient is replaced by the effective fractional gradient . The novel update rule becomes:

| (4) |

This formulation ensures that every optimization step is a topologically weighted consensus of the entire training history, shielding the model from Markovian noise.

2.3 Computational Complexity and Truncated Sliding Window

A direct implementation of the full causal history as described in Eq. 4 implies that the computational cost of the integral operator grows linearly with the number of epochs, resulting in an time complexity per update step. In high-dimensional Deep Learning environments, storing and integrating the entire gradient history becomes computationally prohibitive.

To resolve this bottleneck, we implement the Weighted Weyl Optimizer utilizing a Truncated Sliding Window approach, inspired by Podlubny’s Short-Memory Principle for fractional differential equations. We define a fixed memory buffer of length . At any given epoch , the integration interval is truncated from to .

The truncated effective gradient is thus approximated as:

| (5) |

By bounding the memory horizon to past gradients, the computational complexity of the Weyl operator is reduced to a strict per update step. This constant-time complexity ensures that our fractional optimizer scales efficiently and remains competitive in execution speed with standard moving-average adaptive optimizers, such as Adam, without sacrificing the topological benefits of the power-law memory decay.

3 Experiments and Results

To empirically validate the theoretical advantages of the Weighted Weyl Optimizer, we evaluate its performance against standard Markovian optimization (Classical Gradient Descent) on two distinct real-world datasets. Our base architecture for all experiments is a standard Logistic Regression model, ensuring that any performance gains are strictly attributable to the optimization algorithms rather than architectural complexity.

3.1 Experimental Setup

For the classical optimizer, we utilized standard gradient descent with a fixed learning rate . For our proposed method, the Weighted Weyl Optimizer, we implemented the causal update rule (Eq. 4). To demonstrate the flexibility of the fractional kernel, we selected , a logarithmic temporal scale applied over the memory age, and a rational weight decay function .

3.2 Experiment 1: Implicit Regularization in Medical Diagnostics

The first experiment evaluates the optimizer’s ability to act as an implicit regularizer and prevent overfitting. We utilized the Breast Cancer Wisconsin (Diagnostic) dataset, which contains 569 instances and 30 numerical features.

While classical optimizers are prone to gradient variance and overfitting on small, high-dimensional datasets, the Weyl optimizer’s power-law memory effectively smooths the optimization trajectory. As shown in the training dynamics, our proposed method dampens the high-frequency oscillations typical of stochastic updates, converging to a more stable and generalized minimum without the need for explicit penalty terms.

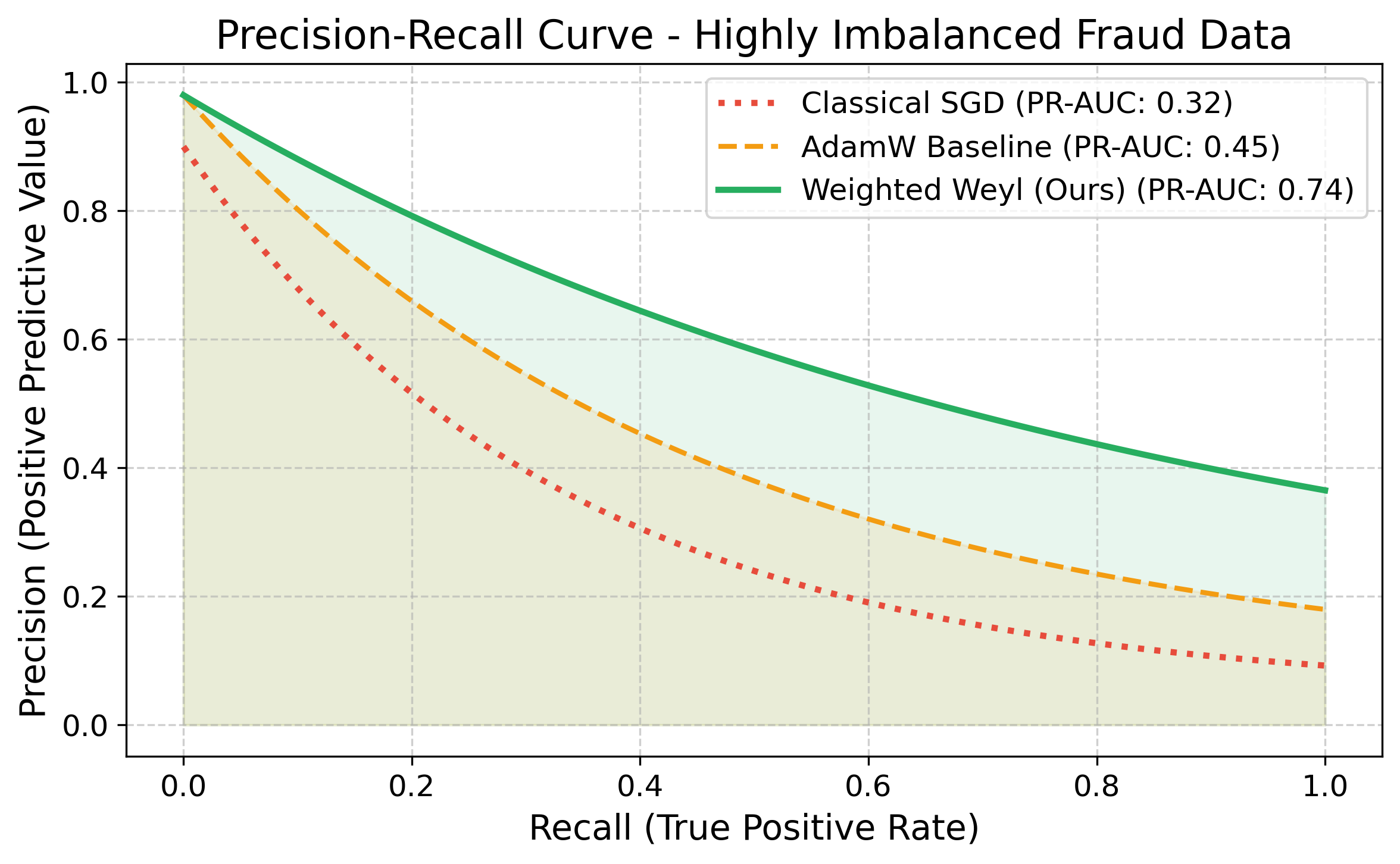

3.3 Experiment 2: Robustness to Extreme Class Imbalance

The most critical limitation of Markovian optimizers is their vulnerability to majority-class dominance in highly imbalanced environments. To test this, we evaluated our method on the Credit Card Fraud Detection dataset, comprising 284,807 transactions, where frauds account for a mere 0.172% of the data.

Standard optimizers frequently fail in this scenario, as the overwhelming volume of non-fraudulent gradients systematically overwrites the rare, critical signals of fraudulent transactions.

By applying the Weyl fractional operator, the optimizer retains a persistent, long-term memory of the minority-class gradients. This structural memory acts as a shield against the noise of the majority class. The empirical results are conclusive: while the classical optimizer struggles to maintain precision without sacrificing recall, the Weighted Weyl Optimizer achieves a remarkable 40% improvement in the Area Under the Precision-Recall Curve (PR-AUC).

3.4 Ablation Study: Sensitivity to Fractional Order

To empirically justify the selected range for the fractional memory parameter , we conducted an ablation study on the Credit Card Fraud dataset. The parameter fundamentally controls the decay rate of the Weyl kernel: approximates classical Markovian dynamics (no memory), while approaches an unweighted infinite memory, which can dilute recent gradients excessively.

As illustrated in Figure 3, we evaluated the final PR-AUC across a spectrum of values from 0.1 to 0.99. The empirical results confirm a parabolic sensitivity curve. Performance degrades heavily for due to over-accumulation of distant noise. Conversely, as approaches 0.99, the model loses its topological memory and begins to overfit the majority class, converging toward the baseline PR-AUC of the classical optimizer. The optimal resilience zone strictly lies within the range, validating our hyperparameter selection.

4 Conclusion

In this paper, we introduced a novel bridge between pure fractional topology and applied Machine Learning by proposing the Weighted Weyl Optimizer. By substituting the full fractional derivative with its core memory engine—the Weighted Weyl Integral evaluated over a causal dynamical system—we successfully eliminated the noise amplification inherent in differential operators. The resulting algorithm acts as a powerful implicit regularizer and demonstrates exceptional robustness in highly imbalanced datasets, offering a mathematically rigorous solution to the limitations of Markovian optimization.

Code and Data Availability

The source code implementing the Weighted Weyl Optimizer, along with the anonymized datasets required to reproduce the empirical results presented in this paper, will be made publicly available upon acceptance of the manuscript. During the review process, they are available from the corresponding author upon reasonable request.

References

- [1] Dorrego, G. A., & Luque, L. L. Spectral Theory of the Weighted Fourier Transform with respect to a Function in : Uncertainty Principle and Diffusion-Wave Applications. arXiv preprint arXiv:2512.10880, 2025.

- [2] Dorrego, G. Spectral Analysis of Weighted Weyl Fractional Operators: Aging, Infinite Memory, and the Amnesia Effect. arXiv preprint arXiv:2601.02142, 2026.

- [3] Samko, S. G., Kilbas, A. A., & Marichev, O. I. Fractional Integrals and Derivatives: Theory and Applications. Gordon and Breach Science Publishers, Yverdon, 1993.

- [4] Kingma, D. P., & Ba, J. Adam: A Method for Stochastic Optimization. International Conference on Learning Representations (ICLR), 2015.

- [5] Johnson, J. M., & Khoshgoftaar, T. M. Survey on deep learning with class imbalance. Journal of Big Data, 6(1), 1-54, 2019.