inline]]

Asymptotic Separability of Diffusion and Jump Components

in High-Frequency CIR and CKLS Models

Abstract

This paper develops a robust parametric framework for jump detection in discretely observed CKLS-type jump–diffusion processes with high-frequency asymptotics, based on the minimum density power divergence estimator (MDPDE). The methodology exploits the intrinsic asymptotic scale separation between diffusion increments, which decay at rate , and jump increments, which remain of non-vanishing stochastic magnitude. Using robust MDPDE-based estimators of the drift and diffusion coefficients, we construct standardized residuals whose extremal behavior provides a principled basis for statistical discrimination between continuous and discontinuous components. We establish that, over diffusion intervals, the maximum of the normalized residuals converges to the Gumbel extreme-value distribution, yielding an explicit and asymptotically valid detection threshold. Building on this result, we prove classification consistency of the proposed robust detection procedure: the probability of correctly identifying all jump and diffusion increments converges to one under proper asymptotics. The MDPDE-based normalization attenuates the influence of atypical increments and stabilizes the detection boundary in the presence of discontinuities. Simulation results confirm that robustness improves finite-sample stability and reduces spurious detections without compromising asymptotic validity. The proposed methodology provides a theoretically rigorous and practically resilient robust approach to jump identification in high-frequency stochastic systems.

1 Introduction

Stochastic differential equations (SDEs) constitute a fundamental mathematical framework for modeling dynamically evolving systems subject to random perturbations. In financial econometrics, such models play a central role in the analysis of interest rate dynamics, asset prices, and volatility processes. Among the most prominent specifications, the Cox–Ingersoll–Ross (CIR) process, introduced by [undefh], has received considerable attention due to its ability to capture mean-reverting behavior while preserving strict positivity of the state variable. The CIR model arises as a special case of the more general Chan–Karolyi–Longstaff–Sanders (CKLS) model proposed by [undefg], which provides a flexible parametric family capable of accommodating empirically observed features such as state-dependent volatility, and heterogeneous diffusion elasticities.

The empirical relevance of mean–reverting diffusion processes in interest rate modeling is well established. Short-term interest rates exhibit a persistent tendency to revert toward a stochastic equilibrium level, reflecting macroeconomic fundamentals, monetary policy interventions, and market expectations. Such dynamics are naturally represented by continuous-time diffusion models, which provide a parsimonious and analytically tractable description of short-rate evolution. These models form the structural foundation of modern arbitrage-free term structure theory and have been systematically incorporated within general no-arbitrage frameworks; see, for example, [undefn] and [undefk]. Since derivative valuation, hedging, and risk management depend explicitly on the drift and diffusion coefficients governing the underlying rate dynamics, reliable statistical inference for discretely observed diffusions is essential. This has motivated extensive research on statistically efficient estimation procedures, most notably maximum likelihood estimation (MLE) and conditional least squares (CLS), which provide consistent and asymptotically normal estimators under high-frequency sampling schemes.

Early contributions to the statistical inference of the CIR process include the work of [undefx], who proposed CLS-type estimators and established their strong consistency under both discrete and continuous observation schemes. Subsequent investigations, including [undefa] and [undefb], demonstrated that likelihood-based methods generally exhibit superior finite-sample and asymptotic efficiency relative to CLS estimators, particularly under high-frequency sampling regimes. These studies established consistency, asymptotic normality, and improved efficiency properties of maximum likelihood estimators, especially in regimes where the process approaches boundary regions. Extensions to the more general CKLS framework were provided by [undefu], who derived asymptotic properties of CLS estimators under relaxed regularity conditions and more general diffusion structures. Alternative inferential paradigms, including Bayesian estimation procedures incorporating prior structural information, were developed by [undefl], offering enhanced inferential stability in small-sample environments.

Despite their widespread applicability, classical diffusion models rely fundamentally on the assumption that the underlying stochastic process evolves continuously over time. However, empirical evidence from high-frequency financial data unequivocally demonstrates the presence of discontinuities, or jumps, arising from macroeconomic announcements, liquidity shocks, institutional trading, and other structural market events. These observations have motivated the development of jump–diffusion models, which augment the continuous diffusion component with a discontinuous pure-jump process; see, for example, the seminal contributions of [undefv] and [undefj].

From a statistical standpoint, the presence of jumps introduces profound challenges for inference. Under high frequency asymptotics, diffusion-driven increments scale at rate , whereas jump-induced increments remain of order . This fundamental disparity in asymptotic scaling provides the theoretical basis for statistical discrimination between continuous and discontinuous components, and has motivated a substantial body of literature devoted to jump detection and decomposition of semimartingale dynamics.

Pioneering work by [undefd, undefe] introduced nonparametric jump detection procedures based on realized variation measures, exploiting the distinct asymptotic behavior of quadratic and bipower variation in the presence of jumps. These methods were further developed by [undefo] and [undef], who established rigorous limit theorems and consistent statistical tests for detecting discontinuities under general semimartingale models. A particularly influential contribution is the locally normalized jump detection statistic proposed by [undeft], which converges weakly to a standard Gaussian distribution in the absence of jumps while exhibiting divergent behavior in the presence of discontinuities. This framework provides a statistically tractable and asymptotically justified mechanism for identifying jump occurrences in high-frequency observations.

Notwithstanding these advances, most existing jump detection methodologies are formulated within a fully nonparametric framework and do not explicitly exploit the structural information inherent in parametric diffusion models. In many practical applications, parametric models such as the CIR and CKLS processes remain indispensable due to their interpretability, tractability, and relevance for structural and forecasting purposes. A common empirical strategy consists of applying nonparametric jump detection procedures as a preliminary filtering step, followed by parametric estimation based on the filtered sample. However, such two-stage procedures introduce additional stochastic variability and are inherently vulnerable to misclassification errors, which may propagate into the parameter estimation stage and degrade statistical efficiency.

A central inferential challenge arises from the intrinsic sensitivity of likelihood-based estimators to contamination by jump-induced increments. Classical likelihood and quasi-likelihood methods assign quadratic penalties to large deviations under Gaussian approximations, rendering them highly sensitive to atypical observations. Consequently, even a relatively small number of jumps may exert disproportionate influence on the resulting parameter estimates, leading to bias, inefficiency, and instability in inference. This phenomenon has been rigorously analyzed in the context of discretely observed diffusions; see, for example, [undefz], [undefq], and [undefy].

These limitations underscore the necessity of robust statistical methodologies capable of mitigating the influence of contamination while retaining asymptotic efficiency under the correctly specified model. A principled and theoretically well-founded approach is provided by divergence-based estimation methods, which replace the classical likelihood function with a discrepancy functional between the empirical and model-implied distributions. In particular, the minimum density power divergence estimator introduced by [undeff] provides a continuous interpolation between maximum likelihood estimation and highly robust procedures through a tuning parameter controlling the trade-off between efficiency and robustness.

Density power divergence estimators possess several desirable theoretical properties, including consistency, asymptotic normality, and bounded influence functions, rendering them particularly suitable for inference in the presence of contamination or model misspecification. Their statistical properties have been extensively investigated in both independent and dependent data settings; see, for example, [undefm] and [undefs]. In the context of discretely observed diffusion processes, divergence-based methods provide a natural and theoretically justified mechanism for attenuating the influence of jump-induced increments, which manifest as localized deviations from the continuous diffusion dynamics.

Motivated by these considerations, the present paper develops a unified parametric framework for robust jump identification and parameter estimation in CKLS-type diffusion models. The proposed methodology integrates robust divergence-based estimation with a statistically principled jump identification mechanism derived from the asymptotic behavior of locally normalized residuals. This approach provides a coherent inferential framework that simultaneously achieves robust parameter estimation and consistent jump detection within a fully parametric setting.

The remainder of the paper is organized as follows. Section 2 reviews the parametric CKLS model and summarizes existing results on consistency and asymptotic normality of classical estimators. Section 2.1 introduces the proposed robust estimation framework and establishes its asymptotic properties. Section 3 develops a statistically rigorous jump detection procedure and derives the associated asymptotic critical thresholds. Section 4 presents simulation studies illustrating the finite-sample performance of the proposed methodology. Concluding remarks are provided in Section 5. All technical proofs and auxiliary results are deferred to Appendix A, with additional simulation results provided in the Supplementary Material.

2 Theoretical Background and Illustration

This section summarizes the probabilistic framework and classical asymptotic results that form the benchmark for the robust methodology developed later. All statements are standard and included only to fix notation and clarify the reference model. Detailed derivations can be found in the cited literature.

We consider the CKLS diffusion process introduced by [undefg],

| (1) |

where and is a standard Brownian motion.Throughout the paper we impose the following standing conditions.

Assumption 1.

The parameters satisfy , , and , and the initial condition satisfies .

The ergodic and boundary properties of (1) are well understood; see [undefg], [undefp], and [undefc]. Under Assumption 1, the process admits a unique stationary distribution. The boundary at zero is unattainable for , while in the boundary case unattainability holds provided . The stationary density takes the form

| (2) |

where is determined by the scale and speed measures.

To motivate the estimation framework, consider first the CIR specification (),

| (3) |

introduced by [undefh]. Let denote observations on an equidistant grid with mesh . The Euler–Maruyama approximation ([undefr]) yields

Define

Then the discretized model admits the linear representation

| (4) |

which forms the basis for classical inference in discretely observed diffusions; see [undefq] and [undefi]. Let denote the OLS estimator associated with (4), and let denote the corresponding residual variance estimator.

We consider the high-frequency asymptotic regime

| (5) |

under which the observation grid becomes increasingly dense as the sample size grows. This framework corresponds to an infill asymptotic scheme, where the time discretization is progressively refined while the observation horizon diverges.

Under (5), standard martingale arguments imply consistency and asymptotic normality of the estimators.

Result 1 (Consistency).

Result 2 (Asymptotic normality).

where depends on moments of the stationary distribution; see [undefq].

For the CIR case,

while for the general CKLS model,

Under infill asymptotics, both the ordinary least squares estimator and the Gaussian quasi–maximum likelihood estimator are consistent for the same true parameter vector; see [undefi] and [undefw]. Since both estimators converge in probability to the identical deterministic limit, their difference must vanish asymptotically. Consequently, the preceding results apply equally to the likelihood-based estimator.

The preceding asymptotic analysis is derived under the Gaussian increment structure implied by the pure diffusion specification. This structure ensures local quadratic approximation of the likelihood and yields the standard quasi-likelihood estimating equations. In empirical applications, however, high-frequency financial series often display excess kurtosis and abrupt movements incompatible with the Gaussian benchmark. Since least squares and Gaussian quasi-likelihood estimators weight all increments equally, their finite-sample behavior may be adversely affected by atypically large increments. This consideration motivates an alternative estimating framework that retains consistency under the diffusion model while reducing the influence of extreme observations.

2.1 Robust Estimation via Density Power Divergence

To formalize robustness, we replace the Gaussian quasi-likelihood criterion by a density power divergence objective in the sense of [undeff]. Let denote the working Gaussian increment density. For , the density power divergence between the empirical distribution and yields the estimating criterion

with the usual likelihood recovered at .

The resulting minimum density power divergence estimator (MDPDE) downweights increments with small model-implied density and therefore limits the influence of extreme observations while preserving consistency under correct specification.

Let denote the vector of unknown parameters, and consider the Gaussian conditional density associated with the Euler discretization of the diffusion process,

where denotes the available conditioning information at time and are the corresponding regressors. This Gaussian approximation serves as a working model for the conditional distribution of the increments and constitutes the basis for both classical and robust inference.

For a robustness tuning parameter , the empirical density power divergence objective function is defined as

The first term acts as a normalization component that depends only on the model, while the second term downweights observations that are unlikely under the postulated conditional density. As , the criterion converges to the negative log-likelihood, and the corresponding estimator reduces to the classical maximum likelihood estimator.

The MDPDE is then defined as

where denotes the parameter space. The tuning parameter controls the trade-off between robustness and efficiency, with larger values of yielding increased resistance to outliers at the cost of some loss in efficiency under the correctly specified Gaussian model.

Result 3 (Asymptotic properties of the MDPDE).

Suppose the regularity conditions of [undefs] hold and the sampling scheme satisfies the infill asymptotic regime (5). If in addition, holds, then the minimum density power divergence estimator satisfies

where denotes the true parameter value. Furthermore, if the estimator is asymptotically normal with covariance matrix given explicitly in [undefs].

Remark 1.

A fundamental property of the minimum density power divergence estimator is its bounded influence function, which ensures stability in the presence of atypically large observations. In discretely observed diffusion models, unusually large increments may arise from unmodeled jump components or mild departures from the pure diffusion specification. Unlike classical likelihood-based estimators, whose influence functions are unbounded, the MDPDE automatically downweights such increments and prevents them from dominating the estimating equations. As a result, systematic discrepancies between classical and robust estimators provide a natural diagnostic signal of structural misspecification, including the presence of jumps.

This distinction is particularly relevant in high-frequency settings. Diffusion sample paths are almost surely continuous, and their increments vanish at the rate as , whereas jump-induced increments remain of finite magnitude. Consequently, jump increments appear as local outliers relative to the continuous diffusion dynamics and may exert disproportionate influence on likelihood-based procedures, often leading to biased or unstable estimates. Robust divergence-based estimators mitigate this effect by limiting the contribution of extreme observations and thereby preserving stability and interpretability of the fitted model.

An additional advantage arises in constrained parametric models, where extreme increments may drive likelihood-based estimates toward the boundary of the parameter space, potentially violating structural conditions such as positivity or ergodicity. By attenuating the influence of atypical observations, robust estimation maintains numerical stability and ensures that the estimated parameters remain within economically and statistically meaningful regimes.

Motivated by these considerations, we consider the CKLS diffusion augmented by a jump component. Specifically, for known elasticity parameter , we study the jump–diffusion model

| (6) |

where is a pure-jump process independent of . Such models are widely used in interest rate and volatility modeling to capture abrupt market movements. The classical Cox–Ingersoll–Ross model arises as the special case .

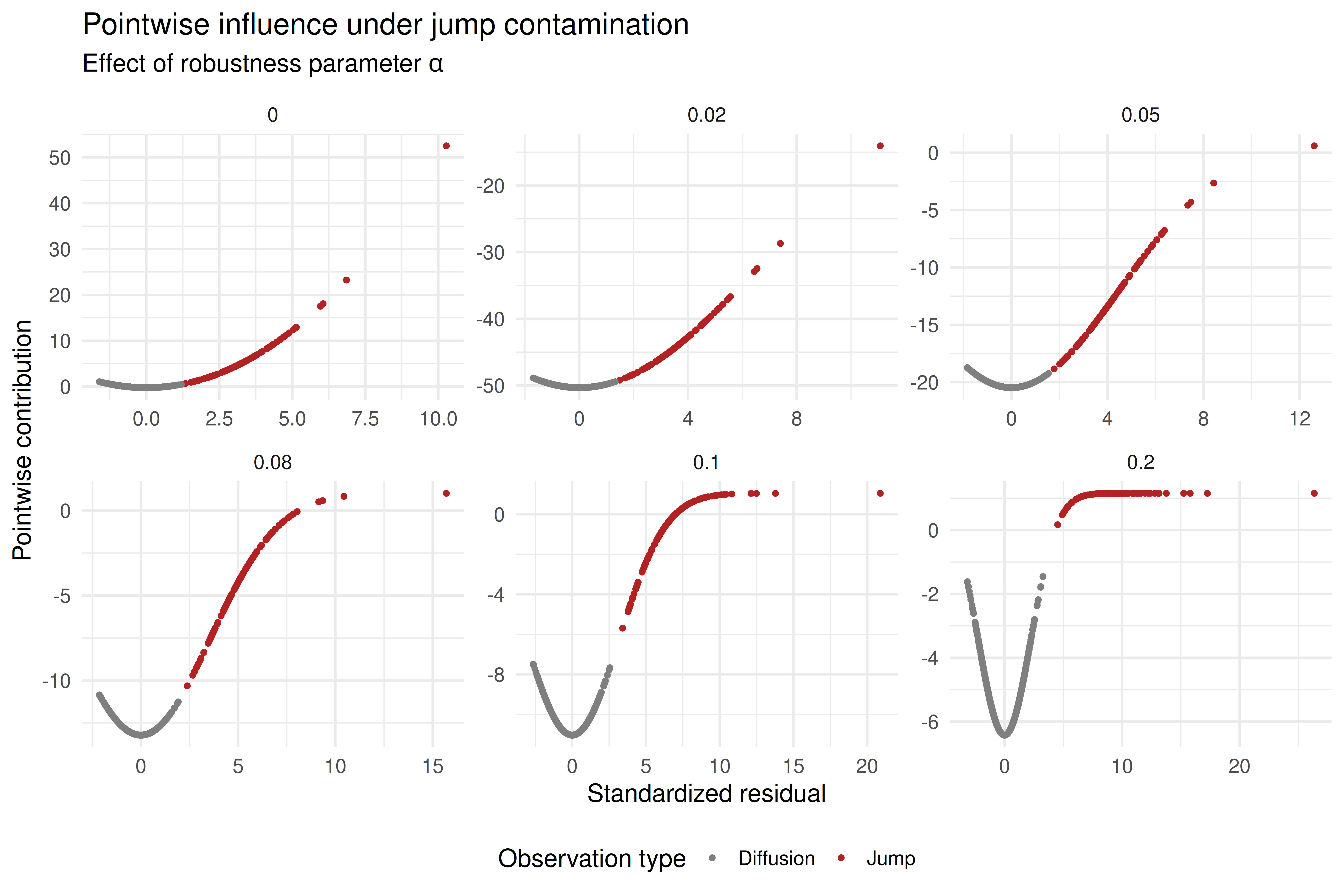

Figures 1(a) and 1(b) illustrate the effect of robustness on the pointwise contribution of standardized increments. When , corresponding to Gaussian likelihood estimation, the influence of extreme increments is unbounded, and jump observations may dominate the estimating equations. As the robustness parameter increases, the influence function becomes bounded, and the contribution of jump-induced increments is progressively attenuated, while diffusion-driven increments remain largely unaffected. This behavior reflects the intrinsic robustness of the MDPDE and its ability to isolate the continuous diffusion structure from jump contamination.

Taken together, these considerations highlight a fundamental advantage of divergence-based estimation in high-frequency diffusion models. By exploiting the distinct scaling behavior of diffusion and jump increments, the MDPDE provides stable parameter estimates and offers a principled basis for detecting departures from the pure diffusion assumption. This diagnostic capability will play a central role in the development of the robust parametric jump detection methodology presented in subsequent sections.

3 Proposed Test for Jump

Let denote discrete observations of the process introduced above equation (6), recorded at equidistant times over a fixed time horizon, where . Denote the increments by

and the jump increment be defined as

| (7) |

where the presence of a jump at index corresponds to the event . Let denote consistent estimators of the model parameters satisfying

We define the normalized increment statistic

| (8) |

This normalization removes the estimated drift and rescales the increment by the estimated local diffusion magnitude. Consequently, increments generated by the continuous martingale component are brought to a unit Gaussian scale, whereas jump-induced increments remain asymptotically separated due to their larger order. This separation forms the foundation of the parametric jump detection procedure developed in the sequel.

The following theorem establishes the asymptotic decomposition of the normalized increment statistic into its continuous martingale and jump components.

Theorem 1.

Suppose the parameter estimators are consistent. Then, for each fixed index ,

| (9) |

Consequently, if , then

whereas if and the jump magnitude is nondegenerate,

Theorem 1 formalizes the pointwise asymptotic separation between the continuous and discontinuous components. After normalization, diffusion-driven increments remain stochastically bounded, while jump-induced increments diverge at rate .

We next characterize the maximal fluctuation of the statistic over intervals free of jumps, which determines the natural detection boundary.

Theorem 2.

Let

Under consistency of the parameter estimators,

and more precisely,

where

and denotes the standard Gumbel distribution.

This extreme-value characterization determines the intrinsic growth rate of the continuous-path maximum and provides a principled basis for threshold selection.

Corollary 1.

Under the same assumptions,

Corollary 1 establishes uniform asymptotic separation between the continuous and jump components, ensuring that a threshold of order asymptotically discriminates between the two regimes.

Theorem 3 (Consistency of parametric jump detection).

and, for any index such that ,

Consequently,

Reliable separation requires stable estimation of the diffusion scale parameter. Classical likelihood-based estimators may be severely distorted by jump-induced contamination, compromising the normalization. To address this issue, we employ robust estimators based on the minimum density power divergence.

Let denote the robust estimators, and define the corresponding normalized statistic

| (10) |

By consistency of the robust estimators, the asymptotic expansion (9) and the extreme-value result of Theorem 2 remain valid for , while providing enhanced stability under contamination.

We formulate jump identification at index as the testing problem

Under ,

whereas under with nonvanishing jump magnitude,

Thus, the continuous and discontinuous regimes become asymptotically distinguishable through the magnitude of the standardized statistic. Motivated by Theorem 2, we introduce the detection threshold

and declare a jump at time whenever

| (11) |

Define the true and estimated jump index sets by

| (12) |

Combining the consistency of the robust parameter estimator with Theorem 3 implies

Consequently, conditional on consistent identification of the jump indices, the jump magnitude at detected times is estimated by

The preceding result establishes asymptotic separation between the continuous diffusion component and the jump component. Specifically, the extreme–value growth of the maximal standardized diffusion increment determines the appropriate detection boundary, whereas the divergence of the statistic in the presence of jumps ensures consistent identification of discontinuities. The robust parametric normalization further stabilizes scale estimation, thereby enhancing reliability under jump contamination and mild model misspecification.

4 Simulation Study

We conduct a simulation study to examine the finite-sample behavior of the proposed robust parameter estimation and jump detection procedure. The data generating process is given by (6). The jump component is specified as a compound Poisson process

| (13) |

where is a Poisson process with intensity , and the jump sizes are independent and identically distributed with

The process is observed at equidistant time points with sampling interval corresponding to a high-frequency asymptotic regime in which as . The underlying diffusion parameters are set to , , , and .

The simulation study considers the following configurations for the sample size and jump component parameters:

| (14) |

in order to evaluate the performance of the proposed robust procedure for jump isolation and detection.

We first examine performance through a visual comparison between true and detected jump locations. For illustration, a representative trajectory is generated under the configuration . Using this fixed sample path, jump classification is performed for robustness parameters

where parameter estimation is carried out via the robust procedure and the resulting estimates are used to classify increments as jump or diffusion driven. The case corresponds to the classical least-squares estimator, providing a non-robust benchmark.

Figure 2 presents the jump detection results for the values of the robustness parameter specified above. Rather than displaying the sample path itself, we plot the first-order increments to highlight discontinuities directly. The detection threshold obtained from Theorem 2 is . True jump times are indicated by blue markers, while detected jumps based on the thresholded standardized statistic are shown in red.

When , corresponding to the classical OLS estimator, the procedure fails to identify several clearly separated jumps. As increases, detection improves substantially, reflecting the stabilizing effect of robust normalization. The detection rate increases rapidly for small positive values of and stabilizes around , beyond which all true jumps are consistently identified.

These results illustrate the role of the robustness parameter in controlling the trade-off between sensitivity and stability. Small values of leave the normalization susceptible to diffusion-driven extreme increments, leading to missed or unstable detections, whereas moderate values attenuate this influence and reduce spurious classifications while preserving detection power.

To provide a more comprehensive assessment of the proposed procedure, we summarize performance over the parameter configurations specified in (14) for robustness levels . Performance is evaluated using classification accuracy and parameter recovery metrics, namely the F1-score and a scaled estimation error.

Let and denote the true and estimated jump sets, respectively, as defined in (12). We define the classification counts

The corresponding performance measures are

| Precision | |||

| F1-score |

Although the jump intensity parameter is fixed in simulation, the realized number of jumps varies across trajectories. Consequently, evaluation based on the theoretical parameters may be misleading in finite samples. We therefore compare estimators with the realized jump characteristics. Define the realized jump mean and intensity as

| (15) |

The corresponding estimators based on detected jumps are

| (16) |

When both the sampling size and the jump intensity are moderate, the number of realized jumps may be small, preventing reliable convergence toward theoretical parameters. For this reason, estimation accuracy is assessed relative to realized quantities rather than population values. We measure the discrepancy via the scaled error metric

which jointly evaluates the accuracy of estimated jump magnitude and frequency.

Accordingly, detection performance and estimation accuracy are evaluated jointly through the F1-score and the scaled error metric defined above. The F1-score takes values in , with larger values indicating improved classification performance; in particular, values closer to one correspond to more accurate identification of jump indices. While the F1-score assesses detection accuracy through correct classification counts, the metric quantifies the discrepancy between estimated and realized jump characteristics. is scale-free and equals zero if and only if the estimated quantities coincide with their realized counterparts, that is, and . Consequently, smaller values of indicate greater estimation accuracy, whereas larger values reflect increasing deviation from the realized jump structure and hence reduced reliability of both parameter estimation and detection. In this sense, the F1-score captures classification performance, while measures parametric divergence, providing complementary perspectives on the effectiveness of the proposed procedure.

Figure 3 reports the F1-score across the parameter configurations defined in (14). The results show a clear improvement in detection performance as the jump mean increases. Moving from left to right in the figure, corresponding to larger values of , the F1-score increases monotonically and approaches one, indicating nearly perfect recovery of the jump indices. A similar improvement is observed when the sample size increases (top to bottom panels). Larger samples lead to a faster convergence of the F1-score toward one as the robustness parameter increases.

For small sample sizes and higher jump intensities (large ), the number of jumps is relatively large compared with the available observations, which reduces the power to correctly identify all true jumps. Nevertheless, relative to the case (corresponding to the OLS estimator), the detection accuracy improves substantially for , demonstrating the advantage of the proposed robust normalization. These findings are consistent with the theoretical result in Theorem 3, which implies that diffusion increments remain of stochastic order while jump-induced increments diverge, yielding increasing separation as .

A similar pattern is observed in the jump-parameter estimation results shown in Figure 4. As the separation between the diffusion increments and the realized jump mean increases (again moving from left to right), the proposed metric converges more rapidly toward zero, indicating improved estimation accuracy. When the jump intensity is very small (), the performance of the OLS estimator is nearly indistinguishable from that of the robust estimator with . In contrast, for higher jump intensities and small samples, the discrepancy between the estimated and realized parameters becomes more pronounced. Increasing the sample size substantially reduces this discrepancy, and the metric declines more steeply toward zero, reflecting improved estimation precision.

Overall, the simulation results provide empirical support for the theoretical separation mechanism underlying the proposed detection procedure. The robust parametric normalization preserves the asymptotic divergence of jump-induced increments while stabilizing the estimation of the diffusion scale. As a consequence, the resulting procedure achieves reliable identification of discontinuities across a broad range of jump intensities and magnitudes, maintaining stable performance even under moderate contamination through jumps.

5 Conclusion

This paper develops a robust estimation and jump detection framework for discretely observed CKLS jump–diffusion processes under high–frequency asymptotics. The methodology combines a density power divergence–based estimator for drift parameters with an extreme–value–theoretic jump detection rule derived from standardized residuals. The proposed approach is designed to retain asymptotic validity under the diffusion benchmark while mitigating the influence of atypical increments arising from jumps or other departures from Gaussianity.

On the theoretical side, we establish consistency and asymptotic normality of the robust estimator under infill asymptotics and show that the associated residual normalization yields a detection statistic whose extremal behavior permits asymptotically valid separation of continuous and discontinuous components. The analysis demonstrates that robustness regularizes the normalization without altering the asymptotic classification boundary, thereby preserving identifiability of the jump component.

The finite–sample experiments corroborate the theoretical findings. The results show that moderate robustness improves stability of both parameter estimation and jump identification, particularly in regimes where jump magnitudes are small or sample sizes are limited. As the sampling frequency increases, detection performance approaches the asymptotic regime, confirming the theoretical scale separation between diffusion and jump increments.

Overall, the proposed framework provides a unified and theoretically grounded approach to robust inference in jump–diffusion models. It achieves reliable jump detection and stable parameter estimation across a broad range of regimes, while remaining consistent with classical likelihood–based inference under the pure diffusion specification. These results support the use of robustness as a principled mechanism for improving finite–sample performance without compromising asymptotic efficiency.

Acknowledgments

The author would like to express special thanks to Prof. Diganta Mukherjee 111Professor, Indian Statistical Institute for his valuable guidance and insightful suggestions throughout this research. The author is also grateful to Prof. Indranil Sengupta222Professor, City University of New York for his assistance and support during the development of this work. Their contributions have been instrumental in shaping the final outcome of this paper.

1 1 1 1 1 1 2 3 2 2 1 1 1 1 1 1 1 3 1 3 1 1 1 1 1 1 1

References

- [undef] Yacine Aït-Sahalia and Jean Jacod “Testing for Jumps in a Discretely Observed Process” In The Annals of Statistics 37.1 Institute of Mathematical Statistics, 2009, pp. 184–222 DOI: 10.1214/07-AOS568

- [undefa] Mohamed Ben Alaya and Ahmed Kebaier “Parameter Estimation for the Square-Root Diffusions: Ergodic and Nonergodic Cases” In Stochastic Models 28.4 Taylor & Francis, 2012, pp. 609–634 DOI: 10.1080/15326349.2012.726042

- [undefb] Mohamed Ben Alaya and Ahmed Kebaier “Asymptotic Behavior of the Maximum Likelihood Estimator for Ergodic and Nonergodic Square-Root Diffusions” In Stochastic Analysis and Applications 31.4 Taylor & Francis, 2013, pp. 552–573 DOI: 10.1080/07362994.2013.798175

- [undefc] Leif Andersen and Vladimir Piterbarg “Moment Explosions in Stochastic Volatility Models” In Finance and Stochastics 11, 2007, pp. 29–50 DOI: 10.1007/s00780-006-0011-7

- [undefd] Ole E. Barndorff-Nielsen and Neil Shephard “Power and bipower variation” In Journal of Financial Econometrics, 2004

- [undefe] Ole E. Barndorff-Nielsen and Neil Shephard “Econometrics of Testing for Jumps in Financial Economics Using Bipower Variation” In Journal of Financial Econometrics 4.1 Oxford University Press, 2006, pp. 1–30 DOI: 10.1093/jjfinec/nbi022

- [undeff] Ayanendranath Basu, Ian R. Harris, Nils L. Hjort and Michael C. Jones “Robust and Efficient Estimation by Minimising a Density Power Divergence” In Biometrika 85.3, 1998, pp. 549–559 URL: http://www.jstor.org/stable/2337385

- [undefg] K.. Chan, G. Karolyi, Francis A. Longstaff and Anthony B. Sanders “An Empirical Comparison of Alternative Models of the Short-Term Interest Rate” In The Journal of Finance 47.3, 1992, pp. 1209–1227 DOI: https://doi.org/10.1111/j.1540-6261.1992.tb04011.x

- [undefh] John C. Cox, Jonathan E. Ingersoll and Stephen A. Ross “A Theory of the Term Structure of Interest Rates” In Econometrica 53.2 [Wiley, Econometric Society], 1985, pp. 385–407 URL: http://www.jstor.org/stable/1911242

- [undefi] Olena Dehtiar, Yuliya Mishura and Kostiantyn Ralchenko “Two Methods of Estimation of the Drift Parameters of the Cox–Ingersoll–Ross Process: Continuous Observations” In Communications in Statistics – Theory and Methods 51.19 Taylor & Francis, 2022, pp. 6818–6833 DOI: 10.1080/03610926.2020.1866611

- [undefj] Darrell Duffie, Jun Pan and Kenneth Singleton “Transform Analysis and Asset Pricing for Affine Jump-Diffusions” In Econometrica 68.6 Wiley, 2000, pp. 1343–1376 DOI: 10.1111/1468-0262.00164

- [undefk] Darrell Duffie and Kenneth J. Singleton “Simulated Moments Estimation of Markov Models of Asset Prices” In Econometrica 61.4, 1993, pp. 929–952

- [undefl] Xiaoxia Feng and Dejun Xie “Bayesian Estimation of CIR Model” In Journal of Data Science 10.2 School of Statistics, Renmin University of China, 2022, pp. 271–280 DOI: 10.6339/JDS.2012.10(2).746

- [undefm] Abhik Ghosh, Ayanendranath Basu and Leandro Pardo “Generalized Density Power Divergence and Robust Estimation” In Journal of Statistical Planning and Inference 143.7, 2013, pp. 1100–1114

- [undefn] David Heath, Robert Jarrow and Andrew Morton “Bond Pricing and the Term Structure of Interest Rates: A New Methodology” In Econometrica 60.1, 1992, pp. 77–105

- [undefo] Jean Jacod “Asymptotic properties of realized power variations” In Annals of Probability, 2008

- [undefp] Samuel Karlin and Howard Edward Taylor “A second course in stochastic processes”, 1981 URL: https://api.semanticscholar.org/CorpusID:118412345

- [undefq] Mathieu Kessler “Estimation of an Ergodic Diffusion from Discrete Observations” In Scandinavian Journal of Statistics 24.2, 1997, pp. 211–229

- [undefr] Peter E. Kloeden and Eckhard Platen “Numerical Solution of Stochastic Differential Equations” 23, Stochastic Modelling and Applied Probability Berlin, Heidelberg: Springer, 1992

- [undefs] Sangyeol Lee and Junmo Song “Minimum Density Power Divergence Estimator for Diffusion Processes” In Annals of the Institute of Statistical Mathematics 65.2, 2013, pp. 213–236 DOI: 10.1007/s10463-012-0366-9

- [undeft] Suzanne S. Lee and Per A. Mykland “Jumps in Financial Markets: A New Nonparametric Test and Jump Dynamics” In The Review of Financial Studies 21.6 Oxford University Press, 2008, pp. 2535–2563 DOI: 10.1093/rfs/hhm056

- [undefu] Zenghu Li and Chunhua Ma “Asymptotic properties of estimators in a stable Cox-Ingersoll-Ross model”, 2013 arXiv: https://arxiv.org/abs/1301.3243

- [undefv] Robert C. Merton “Option Pricing When Underlying Stock Returns Are Discontinuous” In Journal of Financial Economics 3.1–2 Elsevier, 1976, pp. 125–144 DOI: 10.1016/0304-405X(76)90022-2

- [undefw] Yuliya Mishura, Kostiantyn Ralchenko and Olena Dehtiar “Parameter estimation in CKLS model by continuous observations” In Statistics & Probability Letters 184.C, 2022 DOI: 10.1016/j.spl.2022.109391

- [undefx] Ludger Overbeck “Estimation for Continuous Branching Processes” In Scandinavian Journal of Statistics 25.1 [Board of the Foundation of the Scandinavian Journal of Statistics, Wiley], 1998, pp. 111–126 URL: http://www.jstor.org/stable/4616488

- [undefy] Masayuki Uchida and Nakahiro Yoshida “Adaptive estimation of an ergodic diffusion process based on sampled data” In Stochastic Processes and their Applications 122, 2012, pp. 2885–2924

- [undefz] Nobuaki Yoshida “Asymptotic behavior of M-estimator and related random field for diffusion processes” In Annals of the Institute of Statistical Mathematics 40.2, 1988, pp. 271–296 DOI: 10.1007/BF00052393

Appendix A Appendix

Proof of the theorem 1.

Proof of Theorem 2.

Let

By consistency of the parameter estimators,

uniformly over , where are independent variables. Since , it follows that

Thus, for any ,

Define the normalizing sequences

and let . Using the Gaussian tail expansion

we obtain

Consequently,

which establishes convergence to the standard Gumbel law.

Finally, since and ,

∎

Proof of Theorem 3.

Let

denote the sets of continuous and jump increments, respectively, and define the threshold

where are given in Theorem 2 and is the Gumbel quantile function.

We first control false detections. By Theorem 2,

where has the standard Gumbel distribution. Hence,

Since may be chosen arbitrarily small, false detections vanish asymptotically.

Next, consider detection under the alternative. For any fixed , Theorem 1 yields

Since , it follows that

so each jump is detected with probability tending to one.

Finally, define the estimated jump set

The preceding bounds imply

which establishes consistency of the classification. ∎