remarkRemark \newsiamremarkhypothesisHypothesis \newsiamthmclaimClaim \newsiamthmassumptionAssumption \newsiamremarkfactFact \newsiamremarkillustrationIllustration \headersSolving LQ Stochastic Control Problems with SignaturesA. Aqsha, P. Bank, and L. Sánchez-Betancourt

Solving Linear-Quadratic Stochastic Control Problems with Signatures ††thanks: Funding: We are grateful for support from Berlin-Oxford IRTG 2544 and the Oxford-Man Institute of Quantitative Finance. AA’s research is supported by the Oxford-Man Institute of Quantitative Finance through the EPSRC Centre for Doctoral Training in Mathematics of Random Systems: Analysis, Modelling and Simulation (EPSRC Grant EP/S023925/1). PB gratefully acknowledges funding by the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) – CRC/TRR 388 “Rough Analysis, Stochastic Dynamics and Related Fields” – Project ID 516748464. For the purpose of open access, the authors have applied a CC BY public copyright licence to any author accepted manuscript version arising from this submission. Acknowledgments: We are grateful to seminar participants at the Oxford-Princeton and Oxford-Berlin workshop for their comments and suggestions.

Abstract

We study a signature-driven numerical scheme to solve multi-dimensional linear-quadratic (LQ) stochastic control problems. Using that linear signature functionals are dense in the natural class of admissible controls, we show that our approach turns the original LQ problem into a deterministic convex quadratic polynomial optimisation. To underpin a numerical approach based on truncated signatures, we prove that the problem’s value function can be approximated by finite-dimensional polynomial approximations when the truncation levels are chosen sufficiently high. Remarkably, our numerical experiments show very decent accuracy already for small truncation levels. Key tools for our analysis are (i) the algebraic representation of controlled stochastic differential equations and the associated cost function as linear functionals of the path signatures of the driving noise, (ii) the convergence of the truncated linear functionals, and (iii) the density of signature controls.

keywords:

Signatures, stochastic control, linear-quadratic, numerical methods, truncation93E20, 93E03, 93E25

1 Introduction

Stochastic optimal control is classically approached by characterising the associated value function. In sufficiently regular Markovian settings, the dynamic programming principle leads to a Hamilton–Jacobi–Bellman (HJB) partial differential equation (PDE) [bensoussan2018estimation, pham2009continuous], alternatively, the Pontryagin maximum principle yields characterisations in terms of backward stochastic differential equations [yong1999stochastic, carmona2016lectures]. These routes are powerful but quickly become challenging in high dimensions, path-dependent settings, or with lack of regularity. Although there are results for optimal linear-quadratic (LQ) control problems driven by fractional Brownian motion [kleptsyna2003lqregulator, duncan2013linear, duncan2017stochastic], these often require fractional integrals to obtain the optimal controls.

Over the last decade, machine learning methods have brought renewed optimism for high-dimensional control, largely by targeting the HJB equation (or related PDE objects) through function approximation [sirignano2018dgm]. While these developments have produced impressive results in certain regimes, they still inherit the conceptual bottleneck of the HJB route: one approximates the value function first, and only then recovers the optimal control (or its approximation). This motivates complementary approaches that parametrize controls directly in a rich, high-dimensional feature space and solve the resulting optimisation problem without passing through a PDE.

In this paper, we pursue such an alternative by using signatures of the driving noise to parametrize admissible controls. The signature of a path, introduced by Chen [chen1954iterated] and developed systematically in rough path theory [lyons2007differential], is a collection of iterated integrals which provides a faithful and algebraically structured representation of the path [hambly2010uniqueness, boedihardjo2016uniqueness]. In particular, linear functionals of (time-augmented) signatures form an algebra [lyons2007differential] and enjoy strong approximation properties on suitable path spaces, making them a natural candidate for constructing expressive families of non-anticipative functionals. In stochastic analysis, iterated stochastic integrals underpin stochastic Taylor expansions [platen1980approx, platen1982taylor, kloeden1992stochastic], and signature theory consolidates these expansions into a unified algebraic framework in which truncation and polynomial structure can be handled systematically.

The idea of restricting to controls that are linear functionals of signatures (or expected signatures) has recently been explored in concrete stochastic optimisation tasks such as optimal execution [arribas2020optimal, cartea2022double]. A key theoretical step was taken in [bank2025stochastic], which proves convergence of value functions when the objective functions are bounded in a way that permits dominated convergence arguments. While this yields a clean theory and accommodates rougher drivers, the boundedness requirement rules out the canonical LQ setting, despite LQ problems being a standard benchmark class. Nevertheless, the LQ structure suggests that a signature approach should be feasible if one can represent both the controlled state and the cost in a tractable signature-based form. Thus, our goal in this paper is to develop a rigorous signature-driven numerical scheme for multi-dimensional LQ stochastic control.

Our starting point is that linear signature functionals are dense in the natural class of admissible controls for the LQ problem driven by Brownian noise, based on the recent density results in [ceylan2025universality]. This allows us to restrict attention to signature controls without losing optimality in the limit. The second ingredient is an algebraic representation viewpoint, inspired by ideas sketched in [arribas2020optimal]: by working with time-augmented signatures and their tensor algebra, we represent the controlled state process (at least for Brownian drivers) via an infinite-dimensional linear functional acting on the signature of the driving noise, and we express the quadratic cost functional in the same algebraic language. The last ingredient is the celebrated Fawcett formula which established a closed-form expression for the expected signature of Brownian motion [fawcett2003problems, lyons2004cubature, ni2012expected]. As a result, once the control is parameterised as a linear functional of the (truncated) signature, the original stochastic control problem reduces to a deterministic convex quadratic polynomial optimisation in finitely many parameters.

To support a practical numerical method, we truncate (i) the tensor representation of the state at some level , and (ii) the signature features used to parametrize controls up to level . A central theoretical question is whether such finite-dimensional truncations yield value convergence as . Here we leverage recent growth and convergence estimates for tensor/signature expansions (in particular the growth estimates developed in [jaber2024pathdependent]) to prove a rigorous consistency result: for high truncation levels, the value function of the truncated polynomial optimisation approximates the true LQ value function. Importantly, this provides a convergence statement at the level of value functions, not merely almost-sure approximation of candidate controls.

Our numerical experiments confirm that the method we propose converges to the known LQ solution and, strikingly, achieves good accuracy for small truncation levels. Finally, the methodology itself is not tied to Brownian drivers: it extends naturally to other signals such as fractional Brownian motion, where PDE methods are less directly applicable. Establishing a fully rigorous approximation theorem in such settings would require appropriate signature growth estimates for the chosen driver, which lies beyond the scope of the present paper. Nevertheless, our experiments indicate that the signature-driven optimisation remains effective in these non-Markovian regimes. In summary, we make the following contributions:

-

(i)

We develop a signature-driven numerical scheme for multi-dimensional LQ stochastic control by parametrizing controls as linear functionals of (time-augmented) path signatures.

-

(ii)

Using density of linear signature functionals in the admissible control class, we justify the signature-control as an asymptotically non-restrictive approximation.

-

(iii)

We show that, under signature truncation, the LQ problem reduces to a deterministic convex quadratic polynomial optimisation problem.

-

(iv)

Using tensor/signature convergence and growth estimates, we prove consistency of the finite-dimensional truncations and obtain value-function approximation results as truncation levels increase.

-

(v)

We provide numerical experiments demonstrating convergence to the known LQ solution with good accuracy at low truncation levels, and we discuss extensions beyond Brownian drivers (e.g. fractional Brownian motion).

Related literature

Signature-based approaches now appear in a growing range of stochastic optimization tasks. Examples include algorithmic trading [arribas2020optimal, cartea2022double], the optimal stopping problem [bayer2023optimal, bayer2025primal] (the latter used dynamically normalised robust signatures [chevyrev2022signature]), portfolio construction and trading [arribas2020sigsde, futter2023signature, futter2025kernel], non-Markovian control problems [hoglund2023neuralrde], and the pricing and hedging of derivatives [lyons2020non, jaber2024signature, jaber2025hedging, jaber2025signatureapproach]. On the theoretical side, robust signatures were introduced in [chevyrev2022signature], while global approximation and universality results for signature feature maps have been advanced in [cuchiero2025global, ceylan2025universality]. The present paper fits into this broader program by establishing theoretical results about the applicability of signature methods to solve LQ stochastic control problems.

The remainder of the paper proceeds as follows. Section 2 reviews the signature background used throughout. Section 3 introduces the control problem, the signature parametrization, and states our main theoretical results. Section 4 presents numerical experiments illustrating the performance of the proposed scheme.

2 Some notations for dealing with path signatures

Let us briefly present some concepts and notation from Lyons’s theory of path signatures; for further details, see for instance [arribas2020optimal, cass2024lecturenotesroughpaths, chevyrev2026aprimer].

2.1 Tensor algebra notations

Let , and be the standard basis of which induces the canonical dual basis . Consider the algebra of tensors

the space of truncated tensors

and the space of extended tensors

where “” denotes the tensor product.111The space is isomorphic to ; for example, we can rearrange the matrix elements of into a long vector in . We define , , and similarly by replacing with its dual . Moreover, for any , we write its projection onto the truncated space as , that is

| (2) |

For any , we define similarly.

Throughout the paper, we represent the canonical dual basis as letters and words with blue characters. A letter represents an element from the canonical basis of and an -word letter represents an element from the canonical basis of . Let us consider a set of letters with the convention that is the -th letter. We associate with , with , and so on until is represented by . With this, we identify the canonical basis of with the set of -letter words

| (3) |

For any , and , we denote as the coefficient resulting from the projection of to the coordinate associated with the word . We have that

We now define the Hilbert-Schmidt pairing as

| (4) |

where is the natural dual pairing induced from the dot product in . The above pairing is a finite summation as has only finitely-many nonzero components. For , we extend the pairing to

| (5) |

whenever the expression converges. Next, we define the seminorm of implied by the tensor as

| (6) |

where .

3 Problem formulation

In this section, our aim is to express, algebraically, and as a (potentially infinite) linear combination of coefficients involving the driving noise signatures: (i) the controlled multidimensional state process and (ii) the linear-quadratic cost functions. Afterwards, we propose a truncation method to approximate the controlled system and the associated cost with a finite sum. We will show that optimising for these finite-dimensional approximations is a good substitute to the actual infinite-dimensional problem.

3.1 Class of admissible tensor functionals

Let and be a filtered probability space satisfying the usual conditions. Let be a -dimensional continuous -progressively measurable process and be its time-extended signature up until time , that is

| (7) |

where “” denotes the Stratonovich integration. The signature lies on the space of extended tensors with the following coordinates: for any word with , we have

| (8) |

with the convention . From rough path theory, the definition of signature above is well-defined for any continuous process, e.g., Brownian motion and fractional Brownian motion. We then define the following subset of admissible tensors

| (9) |

It follows that as the sum in (6) turns into a finite sum. Moreover, if , then the Hilbert-Schmidt pairing ,

| (10) |

is a well-defined and progressively-measurable stochastic process.

It is well-known that the space of linear functionals acting on signatures forms an algebra under the so-called shuffle product “” (refer to e.g. [gaines1994thealgebra]; see [jaber2024pathdependent] for the extended version). In particular, from [jaber2024pathdependent] we have that if , then and

| (11) |

3.2 Algebraic expression of a controlled multidimensional linear SDE

We take the state to be -dimensional and the control to be -dimensional. Suppose that is a -progressively measurable process such that the system of stochastic differential equations (SDEs),

| (12) | ||||

| (13) |

admits a strong solution. For simplicity, all coefficients (, , , , for , , ) are constants.222This can be relaxed into deterministic polynomial-in-time coefficients

Throughout this paper, we use parentheses in the superscripts to refer to a particular element of a vector/matrix/tensor. For example, denotes the -th element of the -dimensional vector and denote the element of in coordinate . We include in the superscript of to draw attention to the dependence on the control.

We are particularly interested in controls which are given by linear functions of the signature:

| (14) | ||||

| (15) |

As we will see, these signature controls form a sufficiently rich class for linear quadratic optimization problems with the clear advantage that, conveniently for numerically purposes, it is parametrized by elements of the tensor algebra .

The main result of the present section will be that for signature controls also their induced state dynamics of (13) are of signature form, albeit with suitable elements from the extended tensor algebra which can be computed from . So, let us make the ansatz

Granted this ansatz works, we exploit the linearity of our system dynamics to express both sides of (13) using tensors

| (16) |

with

We are thus led to consider the system of tensor equations

| (17) |

Our first result deals with the existence and uniqueness of the solution to this system.

Proposition 3.1.

For any , , with , there exists a unique such that

| (18) |

Proof 3.2.

The problem is equivalent to solving the system of equations

| (19) |

parametrized by and arbitrary words . For , we have as , implying that

is the only choice. Next, assume that we have solved for for all and any . For , again we use the fact that and obtain

| (20) |

Thus, we would have solved for for all and word of length . By induction, we find a solution that satisfies Equation (18). The uniqueness follows directly from the algorithm for computing each element of .

From Proposition 3.1, the tensor equation (17) has a unique solution in . However in general, even if the extended tensor belongs in the space (which is not yet established at this point), it is not clear that the random process replicates the original controlled state . Moreover, it remains unknown that the pairing is integrable (either with respect to , , or both). Even if it is integrable, it does not follow automatically that one can move the expectation inside the pairing, i.e., .

All of the above complications are resolved when the driving noise is Brownian. The foundational work by [jaber2024pathdependent] provides a growth condition for the entries of such that random processes induced by the tensor and the Brownian signatures are integrable in some sense.

Lemma 3.3.

Define the set

| (21) |

The following statements hold.

-

1.

is a linear space that is closed under tensor and shuffle product, i.e. for any , , we have .

-

2.

If the driving noise is Brownian, for any , we have

-

(a)

and ,

-

(b)

-

(c)

-

(d)

-

(e)

-

(f)

and

-

(g)

for all ,

(22) (23)

-

(a)

Proof 3.4.

First, we will prove that the space is the same as the space of exponentially-dominated tensors introduced in [jaber2024pathdependent]. Let with the corresponding constant . Define and . From Proposition 2.3 in [jaber2024pathdependent] we have that

| (24) |

Thus, for any and , Conversely, if there exists such that for any word , then . We conclude that statements 1, 2a, and 2b directly follow from Proposition 3.12 in [jaber2024pathdependent]. For 2c, we have

| (25) | ||||

| (26) | ||||

| (27) |

Statement 2d follows similarly. Next, observe that

| (28) |

Thus, it follows that

| (29) | ||||

| (30) |

By applying the extended shuffle property (Proposition 3.1 in [jaber2024pathdependent]) and Cauchy-Schwarz inequality we have

| (31) | |||

| (32) | |||

| (33) |

Moreover, observe that . As such, by applying the extended shuffle product and Cauchy-Schwarz again, the second term in the right-hand side of (30) also converges to zero, proving 2e. Statement 2f follows from the extended shuffle product and 2e. Statement 2g follows from the fact that and from applying the extended shuffle product, statement 2d, and statement 2e.

The following lemma shows conditions under which the solution of (17) belongs to the space .

Lemma 3.5.

For , the solution , , of (17) is an element of the space .

Proof 3.6.

Let us define . Then, for all and , we have

| (34) | ||||

| (35) |

Recall that and are linear combinations of 1-letter words. Moreover, as lives in , so does . Thus, at some point, for long words, i.e. there exists such that for all , with . We define

| (36) |

and we take

By this construction, we have

| (37) |

for all words with length . Assume for all words with length , . Then for any letter ,

| (38) |

The lemma follows by induction.

Corollary 3.7.

In light of Lemma 3.5, we will assume the driving noise to be Brownian from this point forward. Later, we will discuss similar results for other processes (e.g. fractional Brownian motion) as well as the associated challenges involved.

The process is a -dimensional standard Brownian motion.

3.3 Linear-quadratic cost functional and its algebraic properties

Next, we are going to express the linear-quadratic cost function as a pairing with the driving noise signature. Additionally, we are also going to describe the algebraic and convexity properties of the cost function.

3.3.1 Tensor representation of the cost functional

For linear state dynamics as in (13), a widely used cost functional in stochastic control problems is the linear-quadratic criterion

| (39) | ||||

| (40) |

for continuous matrix valued mappings on and matrices such that are symmetric, positive semi-definite, is symmetric positive definite, and , for any .

As we seek to minimize these costs, it is natural to focus on admissible controls from

| (41) | ||||

| (42) |

It follows that as each entry of is square-integrable and the tensors defining signature controls have only finitely many non-zero entries.

By Stone-Weierstraß, we can uniformly approximate the continuous matrix functions with polynomials in . Thus, we are justified in considering the polynomial case when

| (43) | |||

| (44) |

where and are symmetric such that , for all . Under this assumption, it turns out that not only is the state process from a signature control of the signature form , , but also the induced cost can be described by a linear functional on the extended tensor algebra, albeit applied to the expected signature .

Proposition 3.8.

The costs incurred by a signature policy can be written in the form

| (46) |

where, for , is in with the following explicit expression,

| (47) | ||||

| (48) | ||||

| (49) | ||||

| (50) | ||||

| (51) |

and is a version of obtained by replacing with its truncated version .

The algebraic tensor representation in (46) is quite powerful: we have transformed the stochastic optimal control problem into a deterministic one. In practice, we cannot numerically compute fully as it involves infinite dimensional tensors . A sensible approximation in this situation is to truncate first at some level , then use this as a proxy for the full tensor and, finally, consider the approximate criterion where is determined by replacing with the truncated version . Observe that now lives in the space . As such, is a linear combination of finitely-many elements of and thus .

Proof 3.9 (Proof of Proposition 3.8).

From the extended shuffle product and the statements of Lemma 3.3, we are able to write the cost functional as follows:

| (52) | ||||

| (53) | ||||

| (54) | ||||

| (55) | ||||

| (56) | ||||

| (57) |

where is given by (47). As is a linear combination of finitely-many tensors in , the tensor also belong in this space. From Lemma 3.3 (statement 2f and 2g), we have

| (58) |

Next, we seek to investigate the algebraic properties of the cost function .

Lemma 3.10.

Let be mappings such that for , can be written as

| (59) |

for some , linear maps and with

| (60) |

Here is the projection map from to . It follows that:

-

1.

For every , , , and , the expression

is an affine function in terms of the coefficients of .

-

2.

For every , , , and linear map , the expression

is a quadratic polynomial in terms of the coefficients of .

Proof 3.11.

To prove statement 1, we have that by repeatedly iterating equation (59)

| (61) | ||||

| (62) |

However, we have . Thus,

| (63) |

As is a linear map acting on , it follows that is an affine function in terms of the coefficients of . As for statement 2, observe that is a linear functional over the coefficients of . However, those coefficients have the form

| (64) | |||

| (65) |

for any word . From the previous statement, it follows that and are affine functions of the coefficients of .

In light of our tensor equation (17) encoding the system dynamics, it is straightforward to see that the mapping satisfies the conditions of Lemma 3.10. As we can decompose into a finite sum of terms in the form of or , the expression is a quadratic polynomial. Additionally, Proposition 3.8 tells us that

so the actual cost functional is also a quadratic polynomial of the coefficients of .

Corollary 3.12.

Let be as in (47). Then, restricted to , the functions and are quadratic polynomials in terms of the tensor coefficients.

3.3.2 Strict convexity of the cost functional

The linear-quadratic cost function in (40) is strictly convex in the space of controls ; automatically, it is also convex in the subspace . As we are working with the tensor representation of the control, we will also need the cost function to be strictly convex in the space . To show this, we need the following lemma.

Lemma 3.13.

The empty word is the only such that for all , -almost surely.

Proof 3.14.

Let us define

| (66) |

Consequently, forms a sub-vector space of . Consider some . For a word , let us denote

| (67) |

Moreover, let us denote for . By Ito’s formula for pairings with Brownian signatures (see Theorem 3.3 in [jaber2024pathdependent] for the extended pairing)

| (68) | ||||

| (69) | ||||

| (70) |

Thus, if , then , , and for all . This implies that for all , which in turn implies that for any word . Let be the longest word such that . Then, we would have ; however, , implying , a contradiction. Thus, .

Using Lemma 3.13, we can show that the tensor representation of the cost functional inherits the strict convexity property from the original cost functional.

Lemma 3.15.

The cost functions and are strictly convex in .

Proof 3.16.

The convexity of follows from the convexity of the actual cost function and Lemma 3.13, so we only need to show the convexity of . Let us consider any such that . Define and . From Lemma 3.13, we have . Denote by and the controlled systems associated with and respectively and take , as their tensor respective representation, i.e. and . Let us take and define

Then for all . Denote by the controlled system associated with and as its tensor representation, i.e. . It follows that

By taking a truncation up to level , we have

From the linear-quadratic form of the performance criterion, we have

| (71) |

Moreover, as is continuous and strictly positive definite, the inequality above is strict if . Thus, is strictly convex.

3.4 Convergence of the truncated problem and density results

In this section, we will prove that minimising the cost functional over is the same as minimising it over the larger space . Moreover, we are going to propose a truncation method to approximate the infinite-dimensional optimisation problem by a finite-dimensional one while preserving convexity and consistency. The following theorem sums up the main findings in this section.

Theorem 3.17.

For sufficiently large truncation levels , the minimization of the truncated cost functional over is a proxy for the original linear quadratic optimization problem in the sense that

| (72) |

and

| (73) |

where denotes the minimizer of the truncated problem and is the optimal control in the linear quadratic optimization problem.

To prove Theorem 3.17, first we need the following result from [ceylan2025universality] on the -universality of linear functionals acting on Brownian signatures.

Theorem 3.18.

For every , there exists , , such that

| (74) |

Proof 3.19.

This follows directly from ([ceylan2025universality], Corollary 4.3.(i)). In fact, the density result still holds in the space of -integrable processes for .

Employing Theorem 3.18, we have the following corollary.

Corollary 3.20.

We have that

Proof 3.21.

Let us choose any . Then we can choose satisfying the statement of Theorem 3.18 and define by . Due to the linear drift and volatility of , we obtain

| (75) |

and thus from the linear-quadratic nature of the cost functional, we have . Thus, the set of real numbers is dense in , and the equality follows.

Now, we are ready to prove our main result.

Proof 3.22 (Proof of Theorem 3.17).

Let us fix . From Proposition 3.8, Lemma 3.12 and 3.15, if one restricts oneself to the space , the coefficients of the (strictly convex) quadratic polynomial converge for to those of the strictly convex quadratic polynomial . The same is then true also for the respective infima, i.e.

| (76) | ||||

| (77) |

In fact, when , it follows that even the minimiser of over converges to , the minimiser of over this domain.

Let us argue why converges weakly to , the minimiser of over . From the above, we deduce that . In particular, is bounded in . Thus, by the Banach-Alaoglu theorem, there exists a weak accumulation point and, by Mazur’s theorem, we can find , , converging to in the strong -sense. By standard stability results of linear SDEs, the cost functional is continuous with respect to the latter convergence and so

| (78) |

where the estimate is due to the convexity of . It follows that minimises over . By uniqueness of this minimiser, thus converges weakly in to the minimiser of over .

3.5 Beyond Brownian noise

Observe that the extended tensors (associated with the controlled state) and (associated with the cost function) do not depend on the driving noise . As such, heuristically, we may replace the driving noise in controlled linear systems (13) with a general process , such as a fractional Brownian motion, with signature and hope that a similar result to Theorem 3.17 would still hold, i.e.

| (79) |

Here, there are two main challenges to establish this broader result:

-

1.

It is now unclear whether the process is even well-defined; we need the truncated pairing to converge to the process in some sense, and the latter process also needs to have a proper meaning. But our result (Theorem 3.17) to this effect makes essential use of the Brownian motion and its signature.

-

2.

There is currently limited -universality result for linear functionals of classical signatures beyond Brownian motion. Such a result does exist for robust signatures (see [bayer2025primal]); however, we are not aware of a way to find a tensor such that for . Recently, there is a new -universality result by [chevyrev2026orthogonal] for linear functionals of a class of rough paths which includes Gaussian and Markovian rough paths.

4 Numerical experiments

In what follows, we study the one-dimensional case ( with two types of noise: (i) Brownian motion, and (ii) fractional Brownian motion with Hurst index . We also consider state truncation levels up to and control truncation levels up to ; as we will see, this is enough for our problem. To work with signatures, we employ the “iisignature” package by [iisignature] and source codes from [arribas2020optimal, cartea2022double]. Additionally, we utilise the “fbm” package to simulate fractional Brownian motion and the “differint” package by [adams2019differint] to perform fractional calculus operations.444The code is publicly available in muhammadalifaqsha’s GitHub.

4.1 Brownian noise

In the Brownian case, we set , , and the remaining model parameters of the state dynamics and cost functional to be one. By Fawcett’s formula (see [fawcett2003problems, lyons2004cubature]), we utilise the following closed-form equation for the expected Brownian signature,

| (80) |

Using the above formula, we are able to calculate all coefficients of the quadratic polynomial explicitly for the truncated problem. For , let us write

| (81) |

Suppose that we have a black-box function that evaluates . It is easy to check that

| (82) | ||||

| (83) | ||||

| (84) |

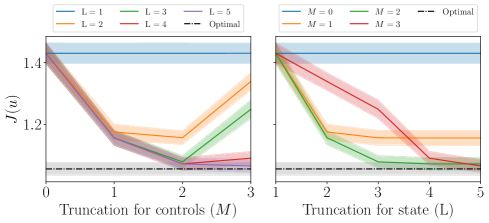

After obtaining the polynomial coefficients, we apply first-order condition to minimise , thus obtaining the coefficients of the minimizer . Afterwards, we simulate a total of times by partitioning the time horizon into equally-spaced intervals. As benchmark, we compute the actual optimal control (obtained by solving the HJB equation) and simulate the performance using the same randomness as in the signature approach. The performance of the strategies is reported in the first and second panel of Figure 1.

On the first and third panel of Figure 1 we observe that the level of state truncation () strongly influences the optimization results. If one were to choose a low , solving the truncated problem would produce a highly suboptimal cost, no matter how complex the control model (more complexity = higher truncation for the control). In fact, for a given , the cost value appears to decrease initially and then increase after around . This is due to the fact that in Equation (17), the coefficients of at a level appear only in the coefficients of at levels or higher. As the coefficients of at higher levels will not affect the coefficients of at lower levels, the procedure can be considered as an overfit, i.e. optimising a complex control model with less accurate target function. This is also reflected in our main result (Theorem 3.18) that we have an ordered limit where should be significantly larger than .

On the second and fourth panel of Figure 1 we observe that for each level of control truncation (), the cost value decreases as we increase the accuracy of the cost functional (more accuracy corresponds to higher level of state truncation ). The cost values seem to plateau to quantities above the actual optimal cost, but said quantities seem to converge to the optimal cost as the complexity of the controls () increases.

4.2 Fractional Brownian motion ()

In this case, we set , and the remaining model parameters of the state dynamics and cost functional to be one. The optimal control thus seeks to minimize the expected average squared control effort and distance from the origin of a geometric fractional Brownian motion whose drift is additively controlled.

First, we implement Monte-Carlo simulation ( sample path with time partitions) to approximate the expected fractional Brownian signature . Next, we apply the first-order condition to minimise as in the Brownian case to obtain the (approximate) minimizer . Afterwards, we simulate a total of times by partitioning the time horizon into equally-spaced intervals. As benchmark, we compute the optimal control from Corollary 3.4 in [duncan2013linear] and simulate the performance using the same randomness as in the signature approach. Note that this benchmark is also an approximate to the actual optimal control as we have to approximate several fractional integrals. The performance of the strategies is reported in Figure 2.

The above results show that we still obtain similar convergence trend as in the Brownian case. Showing that although the theoretical convergence guarantees are yet to be established, the numerical experiments produce encouraging results.

References