Zhu et al.

Huge-Scale Assortment Optimization with Customer Choice: A Parallel Primal-Dual Approach

Huge-Scale Assortment Optimization with Customer Choice: A Parallel Primal-Dual Approach

\ARTICLEAUTHORS

\AUTHORDonghao Zhu

\AFFThe Institute of Statistical Mathematics, Tokyo, Japan 190-0014,

The University of Tokyo Market Design Center, The University of Tokyo, Tokyo, Japan 113-0033,

\EMAILzhu@ism.ac.jp

\AUTHORHanzhang Qin

\AFF

Institute of Operations Research and Analytics, National University of Singapore, Singapore 117602,

Department of Industrial Systems Engineering and Management, National University of Singapore, Singapore 117576,

\EMAILhzqin@nus.edu.sg

\AUTHORChing-pei Lee

\AFF

The Institute of Statistical Mathematics, Tokyo, Japan 190-0014, \EMAILchingpei@ism.ac.jp

\AUTHORYuki Saito, Takahiro Kawashima

\AFF

ZOZO Next, Inc., Tokyo, Japan 263-0023, \EMAILyuki.saito@zozo.com, \EMAILtakahiro.kawashima@zozo.com

\AUTHORKenji Fukumizu

\AFF

The Institute of Statistical Mathematics, Tokyo, Japan 190-0014, \EMAILfukumizu@ism.ac.jp

We study huge-scale assortment optimization problems to maximize expected revenue under customer choice, addressing a fundamental challenge in industries such as transportation, retail, and healthcare. The choice-based linear programming (CBLP) formulation provides a powerful framework for optimizing sales allocations across customer segments, yet traditional approaches often fail to solve CBLPs of huge scale (involving millions of customer choices) due to the lack of algorithmic designs that exploit problem structure. To overcome this computational bottleneck, we propose a first-order primal–dual method, SPFOM, which requires only a small computational cost per iteration, achieves a provably near-optimal convergence rate, and can be readily extended to parallel computing environments. Computational experiments demonstrate the computational and practical superiority of SPFOM over state-of-the-art solvers for large-scale linear programs. The framework is extended to a multi-period assortment optimization setting with inventory constraints, where SPFOM estimates global shadow prices that enhance classical bid-price control policies compared with benchmark methods such as market segment decomposition. Numerical experiments and a case study using real-world data from the ZOZOTOWN platform validate the practical effectiveness of SPFOM, highlighting its advantages in improving revenue performance while maintaining balanced inventory levels.

Revenue management, Generalized attraction model, Discrete choice model, Primal-dual method, Large-scale optimization

1 Introduction

In the dynamic landscape of modern digital markets, effective revenue management (RM) is crucial for businesses to thrive. This paper investigates the computational challenges arising in huge-scale assortment optimization problems (i.e., extremely large-scale problems involving millions of customer choices and high-dimensional decision spaces) that aim to maximize expected revenue, with a particular focus on formulations based on choice-based linear programs (CBLPs) under the generalized attraction model (GAM). A central question in revenue management is how to incorporate demand dependencies into forecasting and optimization models. Specifically, suppliers must anticipate how consumer demand redistributes when the set of available products changes, since such substitution effects fundamentally determine the revenue-maximizing assortment. Modeling these interactions is critical for effective decision-making in large, dynamic markets where customer choices evolve in response to assortment updates and price adjustments. This modeling framework offers a substantial improvement over the traditional independent demand model (IDM), which relies on the simplifying assumption that the demand for each product is independent of the availability of other products. While the IDM allows for tractable computation, it fails to capture the cross-product substitution effects that are central to realistic demand systems.

In this paper, we focus on the discrete choice model and the associated optimization formulation developed by Gallego et al. (2015). Specifically, the GAM provides a closed-form representation of customer demand for any given choice set, capturing substitution effects across products. The parameters of the GAM can be efficiently estimated from abundant transaction data (Gallego et al. 2015), and are assumed to be given in this study. Under the GAM framework, the resulting revenue management problem can be formulated as a choice-based linear program (CBLP), which can be equivalently transformed into a sales-based linear program (SBLP) that is more amenable to large-scale computation and algorithmic analysis.

In modern digital markets, assortment optimization problems often involve an extraordinarily large number of decision variables, reflecting the complexity of coordinating millions of products, heterogeneous customer segments, and dynamic demand patterns. For instance, in the fashion e-commerce industry, platforms such as ZOZOTOWN, one of Japan’s largest online fashion retailers, handle tens of millions of product–customer interactions across thousands of brands and millions of active users daily (Saito et al. 2020). Similarly, Amazon recorded over 3 billion monthly online visits in 2023, illustrating the massive scale of customer activity in global digital markets (Amazon 2024). Managing such large-scale systems presents formidable computational challenges, as even basic full-dimensional vector operations become prohibitively expensive at realistic market scales. A common practical approach to mitigate this challenge is to decompose the problem by partitioning the product space into smaller, more manageable subsets (e.g., market segments), and making assortment or selling decisions separately for each subset (Aouad et al. 2023). However, while such decomposition strategies reduce the dimensionality of the product space, the number of customers and potential choice interactions entering the system typically remains prohibitively large. These characteristics make the development of computationally scalable optimization methods indispensable for practical large-scale assortment optimization. Hence, our central research question is: How can we design a computationally efficient method to solve assortment optimization problems when the number of customers is prohibitively large? To answer this question, the primary objective of this paper is to develop a computationally scalable framework that enables firms to determine more effective resource allocation and assortment (or product recommendation) strategies for large-scale digital markets, while maintaining minimal computational overhead.

1.1 Our Contributions

The core technical innovation of our work lies in the development of a novel primal–dual first-order method, termed the Sales-based Primal-dual First-Order Method (SPFOM), which efficiently exploits the structured coupling inherent in huge-scale assortment optimization problems and ensures rapid convergence to the optimal solution of the SBLP. The optimal solution of the SBLP can be equivalently transformed into that of the CBLP, thereby linking the sales-based and choice-based perspectives in a manner consistent with practical modeling considerations. We establish a global linear contraction in expected squared distance to the unique smoothed optimum, with an explicit rate that depends on the market size, batch size, and the spectral properties of the structured coupling matrix. This form of convergence is not implied by existing LP theory papers: these papers usually apply to deterministic full-information iterations and control residuals for the original LP, whereas our result quantifies how sampling noise, problem scale, and smoothing jointly determine contraction for a market-structured problem.

Moreover, from a computational perspective, SPFOM is inherently parallelizable, enabling substantial acceleration in distributed computing environments using GPUs. Our algorithm contributes to the growing literature on GPU-based linear programming, and our approach is more structured and scalable than general-purpose GPU-based LP methods, as it explicitly exploits the problem structure arising in huge-scale assortment optimization, as demonstrated in our numerical experiments. Our framework can also be extended to multi-period assortment optimization settings with inventory considerations, allowing it to adapt effectively to dynamically evolving retail environments.

The global shadow prices estimated by SPFOM can be directly incorporated into classical revenue management heuristics, such as bid-price control. In contrast to conventional approaches that repeatedly compute local shadow prices for smaller product subsets or market segments, SPFOM derives global shadow prices that more accurately capture product-level marginal profits, substitution effects, and future value potentials. This capability enables the system to avoid prematurely recommending products with higher long-term value, thereby improving both revenue performance and inventory balance over multiple periods. This framework can also be extended to network revenue management problems with bundle selling, in which bundle-level decisions interact through shared resource capacities. Using a real-world dataset from ZOZOTOWN, one of Japan’s largest online retail platforms, we demonstrate the scalability and empirical effectiveness of the proposed method in large-scale, dynamically evolving assortment and recommendation environments.

1.2 Organization of the Paper

Section 2 reviews the related literature. Section 3 introduces the model setup and problem formulations. Section 4 presents our methodological framework and theoretical analysis, together with numerical validation and discussion of parallel implementation. Section 5 extends the framework to a multi-period assortment optimization setting and shows how the resulting shadow prices improve bid-price control. Section 6 reports a real-world case study using data from ZOZOTOWN and evaluates computational performance across large-scale and multi-period settings. Section 7 concludes and outlines directions for future research.

2 Related Work

A choice-based deterministic linear program (CBLP) is a mathematical model for maximizing revenue through optimal inventory allocation across market segments while explicitly accounting for customer choice behavior (Liu and Van Ryzin 2008), and serves as a fundamental formulation for assortment optimization problems under customer choice. Unlike traditional models that treat product demands as independent, the CBLP incorporates the sale probability of each product within a market segment, capturing interactions among available alternatives and customer preferences. Its objective is to determine the optimal assortment of products and the fraction of time each assortment should be offered, thereby maximizing expected revenue over the planning horizon. This deterministic linear programming formulation provides an upper bound on achievable revenue while respecting inventory constraints and capturing customer choice dynamics. For a comprehensive overview of recent studies on choice-based revenue management and assortment optimization, readers are referred to the surveys by Feng et al. (2022), Heger and Klein (2024).

Extensive research has studied revenue management from both modeling and computational perspectives; for a comprehensive review, readers are referred to Strauss et al. (2018). Much of this literature focuses on developing rich optimization formulations to capture demand uncertainty, customer choice behavior, and inventory constraints, as well as tractable solution methods for the resulting models. Within this line of work, Gallego et al. (2015) introduced the sales-based linear program (SBLP), which is equivalent to the choice-based linear program (CBLP) but avoids the exponential number of variables inherent in the latter. Relatedly, Tong and Topaloglu (2014), Vossen and Zhang (2015), and Kunnumkal and Talluri (2019) proposed tractable approximations to choice-based linear programs under both independent and discrete choice demand models, while Zhang et al. (2022) developed a product-based separable piecewise linear approximation that yields tighter relaxations. Despite these advances, existing approaches are not directly applicable to the huge-scale regimes we consider, those involving extremely large customer populations and product spaces, as they typically lead to formulations whose computational complexity grows rapidly with problem size. In contrast, our work focuses on the development of computationally scalable algorithms for large-scale assortment optimization under customer choice, with an emphasis on methods that scale linearly with the number of customers within the CBLP/SBLP framework.

Naturally, our approach belongs to the class of first-order methods for solving large-scale linear programs (LPs). To date, the most widely used LP solvers have been based on either the simplex method or the interior-point method (Mittelmann Accessed in Feb 2024). Both approaches rely heavily on solving linear systems through matrix factorization, which makes them unsuitable for extremely large-scale problems, as Hessian computation and factorization can become prohibitively expensive. Recent studies have demonstrated that first-order methods can generate highly accurate LP solutions in a relatively short time (Applegate et al. 2021). By employing first-order techniques, the computational bottlenecks inherent in simplex and interior-point methods can be overcome, as the primary operation reduces to gradient evaluation rather than Hessian computation. This shift enables the efficient generation of high-accuracy solutions even at massive problem scales. There is a recent trend of studying how to efficiently incorporate GPUs in first-order methods, with a special focus on LP and conic programming solvers (Lu and Yang 2025b, a, Lin et al. 2025). Our method differs from these general-purpose approaches in that it explicitly exploits the problem structure arising in huge-scale assortment optimization under customer choice, leading to substantially improved computational efficiency compared with generic methods.

Recent efforts have been made to establish the theoretical validity of first-order methods for solving general huge-scale LPs, including the works of Nesterov (2008), Nesterov (2012), and Lu and Yang (2021). Guo et al. (2025) proposed ML-based first-order methods for directly optimizing assortments under complex choice models, with a focus on scalability and benchmark performance. Our approach differs from these studies in that we aim to develop a computationally tractable first-order method tailored to LPs with a specific structure. Prior research has shown that for LPs possessing certain structural properties, specialized first-order algorithms can achieve faster convergence rates than general-purpose LP solvers, for example, nearly linear-time solvers for Packing LPs (Allen-Zhu and Orecchia 2019) and efficient solvers for Optimal Transport LPs (Mai et al. 2021, Liao et al. 2022). Nevertheless, our approach again departs from these directions, as it is straightforward to verify that neither the CBLP nor the SBLP falls into the category of Packing or Optimal Transport LPs.

3 Model Setup and Problem Formulation

We introduce a stochastic assortment optimization formulation under customer choice. Let denote the set for any positive integer . On the demand side, the positive integer denotes the number of customer types, assumed to be very large. For each customer type , where each type corresponds to an individual customer, we assume a homogeneous arrival rate . On the supply side, the positive integer denotes the number of product types, where . For each product type , the positive real number denotes the capacity, representing the maximum quantity available for purchase. The corresponding price is given by the positive real number .

The set of all potential assortments indicating a customer’s purchasing interest is denoted by . Each customer, given an assortment , will select product with probability . Let the consideration sets be distinct across customer types, i.e., customer of type may choose from a set . Since the analysis and algorithm remain unchanged, all sets are assumed equal, , for notational simplicity. For , . Then, upon each customer’s arrival, an assortment is made to the customer if a purchase is made for product , revenue is incurred and 1 unit of the inventory for product is consumed. The RM problem is then how to decide the offering of assortment to all customer arrivals to optimize the expected cumulative revenue.

Again, for notational simplicity, we adopt the multinomial logit model (MNL) to model the customer choice. Between each customer type and each product type , the real number denotes the preference weight. For each customer , the real number denotes the preference that the customer does not want to buy any product. Then, the MNL model specifies

The MNL model belongs to the basic attraction model (BAM) model (Luce 2012), but our algorithm design and analysis can easily extend to the case where the choice model is a GAM. In that case, besides the nominal attraction values , we use shadow attraction values to estimate the effect of items that are not in the assortment on customer choice. Namely, the choice probability of customer for product becomes

Since the equivalence between the CBLP and the SBLP holds not only for the MNL model but also for the broader GAM class (Gallego et al. 2015), the algorithmic design and theoretical guarantees presented in this work naturally extend to all choice models covered by GAM.

3.1 CBLP

The choice-based model refers to a decision-making model in which individuals make choices from a set of available alternatives, and it is well known that a deterministic LP formulation provides an upper bound for the RM objective (Talluri and Van Ryzin 2004). Our primary objective is to solve the following choice-based LP, defined as:

| (1) | |||||

| s.t. | (2) | ||||

| (3) | |||||

| (4) | |||||

Here, the function represents the total time that customer is offered the set and is the decision variable. The objective (1) maximizes the expected revenue by multiplying the product prices with the probabilities that customers desire to buy those products. Constraint (2) specifies that the total quantity of each product purchased by all customers should not exceed the capacity. Constraint (3) ensures that the number of customers purchasing products is equal to the arrival rate of each customer type. Constraint (4) ensures that customers may only purchase a positive number of products. This choice-based model has an exponential number of variables due to the size of .

3.2 SBLP

Gallego et al. (2015) developed a sales-based LP by applying the primal-dual theorem to the CBLP (and showed CBLP and SBLP are equivalent), defined as follows:

| (5) | |||||

| s.t. | (6) | ||||

| (7) | |||||

| (8) | |||||

| (9) | |||||

Here, the positive real variable denotes the quantity desired by customer for product . The positive real variable denotes the quantity that customer does not wish to purchase any product. The objective (5) maximizes the expected revenue by multiplying the product prices with the quantities that customers desire to purchase. Constraint (6) delineates the capacity, ensuring that the quantities of products that customers purchase do not exceed their respective capacities. Constraint (7) delineates the balance, ensuring that the number of customers of the same type, regardless of whether they purchase a product, equals the corresponding arrival rate. A demand is defined as the ratio of the quantity of products purchased and customer preferences (Gallego et al. 2015). Constraint (8) compares the demand for purchase and no-purchase behaviors. Constraint (9) ensures that customers only purchase a positive number of products. For further details on the derivation process of the sales-based LP, interested readers are referred to Gallego et al. (2015).

The SBLP is equivalent to the CBLP, but solving the CBLP is computationally challenging due to the exponential number of decision variables. Solving the SBLP is easier for this reason. Additionally, the formulation of the SBLP is similar to the Optimal Transport (OT) problem (Cuturi 2013, Peyré et al. 2019), but with an additional constraint (8). Therefore, solving the SBLP is technically more challenging than solving a general OT problem. Our goal is to tackle a huge-scale SBLP, where the parameter is much larger than .

4 Methodology Framework and Analysis

Our methodological framework adopts the BAM model to capture customer choice behavior in an assortment optimization setting, from which the CBLP is derived to compute the optimal product recommendation scheme, as illustrated in Figure 1.

To address the exponential growth of variables in the CBLP, an equivalent formulation, termed the SBLP, is identified, making large-scale optimization computationally tractable. In this section, we present our method for solving the SBLP, which can be viewed as a primal-dual first-order algorithm with sparse primal updates, referred to as SPFOM. The solution to the SBLP obtained by SPFOM can be equivalently transformed into the solution of the CBLP. The potential for parallel implementation within this framework is discussed. The complete structure of the SPFOM algorithm and its parallelized version are provided in Algorithms 2 and 3.

4.1 The Primal-Dual Approach

The constraint (6) is incorporated into the objective function (5) to obtain:

| (10) | |||||

| s.t. | (11) | ||||

| (12) | |||||

| (13) | |||||

| (14) | |||||

This formulation makes fast and sparse gradient updates on . Our primary focus is on fast updates for the inner optimization problem (recall that is assumed to be very large, so even scanning an -dimensional vector can be computationally costly), as the dual updates can be executed using a standard dual ascent approach. This assumption relies on the premise that is not excessively large. Namely, the inner problem for customer is:

| s.t. | ||||

A key observation regarding the structure of the inner optimization problem is, a greedy approach in is sufficient to solve the problem exactly when the value of is given.

Lemma 4.1

When is fixed, can be computed by a greedy algorithm (Algorithm 1) with computational time .

The proof of Lemma 4.1 is provided in Online Appendix 8.1. In practice, a mini-batch of customers can be sampled, and each customer ’s inner optimization can be efficiently solved via a golden-section search over the value of . This approach requires only time, where logarithmic factors are ignored and is the batch size. The Algorithm 1 solves the inner problem in this way.

After solving the inner problem, we perform the dual ascent update. For each , is updated as follows:

where is a constant step size. The complete SPFOM algorithm is summarized in Algorithm 2.

The computational cost of each iteration of SPFOM is by design. This efficient primal-dual first-order method with sparse primal updates ensures that our approach remains computationally feasible even for huge-scale instances.

4.2 Optimality Guarantees

Convergence guarantees are provided for a slightly modified variant of the algorithm, whose solution is shown to be arbitrarily close to that of the original formulation in theory. In particular, consider the case where a small regularization term, , is added to the minimax formulation. This is equivalent to solving the following penalized version of (5), where the constraint set for in the original minimax formula is denoted as .

| (15) |

Accordingly, the dual descent step in Algorithm 2 should be modified to

| (16) |

The following theorem, from Theorem 17.1 of Nocedal and Wright (2006), shows that as approaches zero, the solution of (15) recovers the true solution of the original linear programming problem.

Theorem 4.2 (Optimality Preservation)

Intuitively, this result shows that formulation (15) serves as an asymptotically exact approximation to the original LP. As the barrier parameter approaches zero, any accumulation point of the optimal solutions is an optimal solution of the original problem. This guarantees that the proposed algorithm asymptotically preserves optimality. The proofs of Theorem 4.2 is provided in Online Appendix 8.2.

We now establish a linear convergence rate of the solutions of SPFOM for the variant (15) of SBLP following the idea of Theorem 3.1 of Du and Hu (2019).

Theorem 4.3 (Linear Convergence)

Let be the sequence generated by Algorithm 2 with , where . Then, there exist constants and such that the iterates converge to the unique optimal solution at a linear rate:

The proof of Theorem 4.3 is provided in Online Appendix 8.4. The theoretical parameterization, particularly the design of the values for and , is intrinsically linked to the structural formulation of the SBLP. Specifically, represents the maximum weighted average revenue across all customers, serving as a global scale for expected returns within the system. By setting the step size , the algorithm employs an adaptive learning rate that accounts for this revenue scale. This configuration ensures that updates to the primal variables are appropriately tempered relative to the objective function’s sensitivity. Consequently, the scaling prevents numerical oscillations and satisfies the technical conditions required to achieve the linear convergence rate established in Theorem 4.3.

Remark 4.4

The proof of Theorem 4.3 shows that . This convergence result is different from those obtained for PDLP (Lu and Yang 2021) or cuPDLP (Lu et al. 2023). The linear convergence guarantees in PDLP and cuPDLP rely on the polyhedral sharpness of linear programs, which links distance to the solution set to global KKT residuals or duality gaps via Hoffman-type error bounds. In contrast, our SPFOM algorithm never forms such residuals: each update is computed from only randomly sampled customers out of a population of size , and therefore operates in a fundamentally different information regime.

4.3 Parallel Computing

The SPFOM (Algorithm 2) tackles a large-scale problem by sampling small-scale inner problems, solving them, and updating the solution iteratively until convergence is achieved. A crucial aspect of this method is the sampling process. To accelerate convergence for a huge-scale problem, one strategy is to simultaneously sample many small-scale inner problems and then solve and update them in parallel. The computational complexity of each iteration of the parallelized SPFOM is when considering workers.

Corollary 4.5

Consider Algorithm 3 with parallel workers. Under the assumptions of Theorem 2, the expected distance to the smoothed optimal solution satisfies

The proof of Corollary 4.5, which extends the analysis of Theorem 8.1, is provided in Online Appendix 8.5. The corollary shows that parallelization improves the contraction rate by effectively increasing the number of sampled customers per iteration from to . That is, while each worker processes a mini-batch of size , the aggregation across workers yields a linear speedup in the convergence rate. This acceleration is orthogonal to the per-iteration computational complexity reduction, which is discussed separately.

4.4 Mapping the SBLP Solution to the CBLP

A key challenge in applying the proposed framework is to map solutions from the SBLP back to interpretable decision strategies under the CBLP. To this end, a recovery procedure is developed to reconstruct a feasible CBLP solution from a given SBLP output, thereby enabling actionable recommendations to be derived from the computationally efficient surrogate formulation.

Lemma 4.6

For each customer , sort the products by the ratio for each in decreasing order. Define the sets and for each , where consists of the products ordered by the ration in decreasing order. Hence, define

The value of represents the probability that the set will be recommended.

Here, the value of corresponds to the value of in the CBLP. The proof of this result follows the construction approach developed in Topaloglu et al. (2012) and Gallego et al. (2015).

When the SBLP solution is mapped back to the CBLP via Proposition 4.6, the resulting assortment space is restricted to a subset of all possible product combinations. For example, consider a setting with three products , ordered according to the decreasing ratio as specified in Proposition 4.6. Under the CBLP formulation, the recommendation strategy may assign probabilities over the full power set of products, yielding combinations (including the empty set): , , , , , , , . In contrast, the SBLP solution restricts attention to only a prefix-closed subset of assortments based on the sorted order, namely: , , , . By limiting the feasible set to such structured combinations, the SBLP achieves a significant reduction in computational complexity, while still offering a close approximation to the CBLP’s revenue performance.

4.5 Numerical Study

Numerical experiments with SPFOM are conducted to perform a comparative analysis with PDLP, which is a state-of-the-art first-order method for solving huge-scale linear programs (Applegate et al. 2021, Lu et al. 2023). The computing environment for our experiments is as follows: CPU: AMD EPYC 7763 64-Core Processor, x86_64, 2.50 GHz (max), 1.50 GHz (base), 128 threads (64 cores per socket); RAM: 1.0 TiB total, 5.7 GiB used, 990 GiB free, 11 GiB buff/cache, 996 GiB available; Operating System: Ubuntu 20.04.3 LTS, Linux kernel 5.4.0-94-generic; Programming language: Julia 1.10.4.

Convergence, Optimality, and Computational Time of SPFOM.

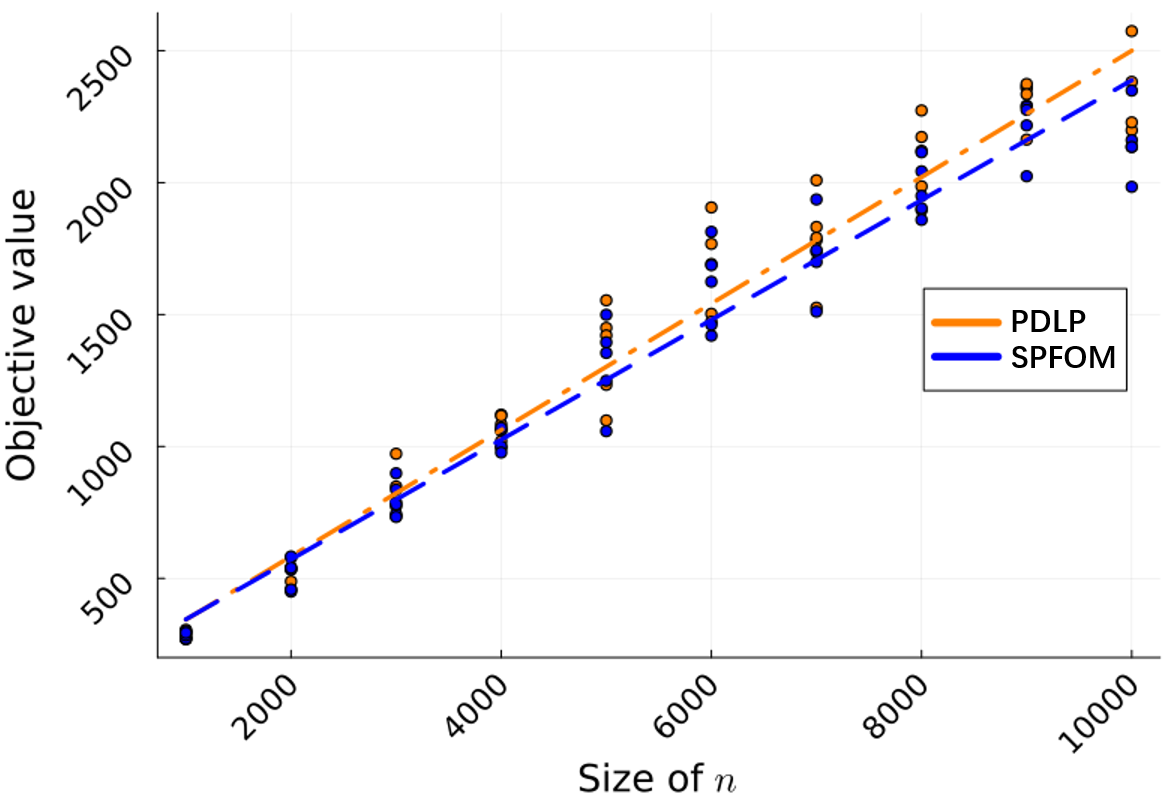

Parameters (capacity), (price), (preference) are generated from a continuous uniform distribution . The other computational variables are set to standard values: , and . Batch size is set to . The convergence criterion is established by using a stagnation-based stopping criterion. The iteration process stops when the objective function value remains unchanged for a specified number of consecutive iterations, as shown in Figure 3(b)(a). Based on empirical evidence, this number is set to . In practice, this number does not significantly affect the iterations, as we set a large value to ensure that the optimal or near-optimal solution is achieved. Objective function values of SPFOM and PDLP are compared in Figure 3(b)(b). As grows, representing an increasing size imbalance between the two sides of the market, the objective value of PDLP becomes noticeably larger than that of SPFOM, whose performance remains near optimal. Because SPFOM employs a primal-dual approach that embeds constraint (2) into the objective function (1) (as reformulated in (10)), its solutions may not fully satisfy constraint (2) in finite samples.

Computing speed of SPFOM compared to PDLP is shown in Figure 3. Figure 3(a) shows individual computing examples where for both methods. A polynomial regression highlights the increasing computing time as grows, with two key observations: (i) SPFOM computes significantly faster than PDLP, and (ii) SPFOM exhibits more stable computing times, whereas PDLP shows larger variation. The higher variance in PDLP’s runtime arises from its adaptive restart and scaling mechanisms, which cause the number of iterations and memory access patterns to fluctuate across instances (Applegate et al. 2021, Lu and Yang 2025b). Figure 3(b) illustrates the averaged logarithmic computing time for both algorithms across multiple runs. In Figure 3(c), SPFOM’s performance is examined in a large-scale market with and . In this case, SPFOM computes recommendations for product types to customers in around 5 hours on our CPU. The performance of PDLP is not included in Figure 3(c) since it crashes when exceeds due to out-of-memory issues. This happens because PDLP significantly increases storage demands during the model pre-solve step as problem size grows, causing its computation time to rise dramatically in our experiments.

| Computing time (s) | Logarithmic time () | Iteration times | |

| Single core | 1733.5 | 3.2 | 1014 |

| 2 cores | 1242.7 | 3.1 | 636 |

| 4 cores | 101.5 | 2.0 | 47 |

| 6 cores | 36.7 | 1.6 | 15 |

| 8 cores | 24.9 | 1.4 | 9 |

Speedup of Parallel Computing.

In large-scale optimization, increasing problem size leads to significantly higher computational costs. For example, as the problem grows, the column generation process becomes more complex and resource-intensive. The storage and computational power required by the algorithm rise non-linearly with the number of decision variables as it searches for the optimal point. Additionally, solvers perform a pre-solve step before finding the solution, but for large problems, this step alone can overwhelm the computer’s storage capacity.

The SPFOM algorithm does not pre-possess many decision variables at each iteration step. Instead, it computes and updates the solution for many small-scale problems, thereby avoiding the aforementioned computational limitations. As shown in Table 1, the computation time decreases significantly with more parallel workers. In steps 3-5 of the parallelized SPFOM algorithm 3, small-scale inner problems are computed in parallel. Multiple inner problems are sampled simultaneously, and then is updated using all the computed results. This effectively increases the iteration step size, reducing the number of steps needed for SPFOM to converge, thus speeding up the overall computation.

Compared to the non-parallelized SPFOM (Algorithm 2), the parallelized SPFOM (Algorithm 3) includes an additional data transfer step. Specifically, when inner problems are assigned to different workers, their parameters and results need to be transferred, a process referred to as fetch in Julia 1.10.4. This introduces two effects in our experiments. First, parallel SPFOM is more efficient than the non-parallel version when the batch size is large, as fetch time is relatively short compared to computation time in each iteration. Second, when the number of workers is large and iterations are few, the marginal speedup decreases because a larger proportion of time is spent on fetching.

5 Extensions

5.1 Extension 1: Multi-Period Setting

The proposed framework can be extended to a multi-period setting to better capture dynamic environments in which both demand and inventory evolve over time. This section illustrates how the SPFOM algorithm can be incorporated into a bid-price control policy for such dynamic settings, and evaluates its performance through numerical experiments.

5.1.1 Multi-Period LP Formulation

We present the multi-period CBLP formulation as follows. This formulation contains dynamic assortment decisions for multiple stages, indexed by , from to , where the customer choice distribution is i.i.d..

| (17) | |||||

| s.t. | (18) | ||||

| (19) | |||||

| (20) | |||||

The corresponding multi-period SBLP is given as follows.

| (21) | |||||

| s.t. | (22) | ||||

| (23) | |||||

| (24) | |||||

| (25) | |||||

Compared with the single-period formulation, the time index is introduced to capture temporal dynamics. The total inventory is given initially and gradually depletes across periods according to the realized recommendations and customer choices. Consequently, both the arrival intensities and preference weights evolve over time. The objective is to maximize the cumulative expected revenue from a sequence of product recommendations over the planning horizon.

5.1.2 Bid-Price Control

Bid price control is a widely used policy in multi-period RM problems for efficiently allocating limited resources across incoming customer requests (Talluri and Van Ryzin 1998). The core idea is to assign an implicit value, known as a bid price, to each unit of resource, and to accept a customer request only if the associated revenue exceeds the total value of the resources consumed. Formally, let denote the bid price of resource at period , which represents the opportunity cost of consuming one additional unit of resource . Under the bid price control rule, product is recommended to customer at time only if the marginal profit satisfies , where is the price of product . In our framework, corresponds to the dual variable obtained from the SPFOM formulation, which captures the shadow value of the remaining capacity. Intuitively, this rule ensures that resources are allocated only when the immediate gain exceeds the future value of capacity , thereby balancing short-term revenue and long-term availability.

Although the multi-period setting involves sequential decision-making over time, our formulation is fundamentally different from standard online algorithms. In online learning frameworks, the decision-maker observes feedback (e.g., realized demand) and adaptively updates decisions without knowledge of future arrivals, typically aiming to minimize regret relative to an offline benchmark. In contrast, our multi-period model assumes that the stochastic demand and preference distributions are known in advance, allowing the problem to be formulated as a deterministic, expectation-based linear program. Accordingly, our focus lies in developing an efficient primal-dual optimization algorithm for solving large-scale structured LPs, rather than in minimizing regret under partial information. Among possible control frameworks, bid-price control offers a tractable and interpretable approach that aligns naturally with LP-based formulations (Talluri and Van Ryzin 1998). Our work therefore enhances this classical framework by improving its computational scalability through the proposed SPFOM algorithm.

5.1.3 Global Market vs. Market Segmentation Decomposition

Under the bid-price control framework, two decision policies are compared: a global optimization (GO) policy based on SPFOM, and a segment-level policy derived from market segmentation decomposition (MSD).

GO Policy.

For each batch, products with zero inventory are first removed. If the number of available products does not exceed the recommendation limit, all remaining products are recommended; otherwise, the corresponding SBLP is solved using SPFOM to obtain global dual prices. A bid-price control rule is then applied, recommending products whose marginal revenue exceeds their bid prices. Customer purchases are simulated under the BAM framework, and inventory levels are updated accordingly.

MSD Policy.

The MSD policy processes each market segment independently within each batch. For each segment, if the number of available products is within the recommendation limit, all are recommended; otherwise, the segment-specific CBLP is solved to obtain local dual prices, which are used to guide bid-price control rule’s recommendations. Purchases are simulated separately for each segment, and the resulting outcomes are aggregated to update overall inventory and revenue.

When the overall inventory is sufficiently abundant, the GO policy identifies and recommends higher-revenue products while utilizing inventory more efficiently than the MSD policy.

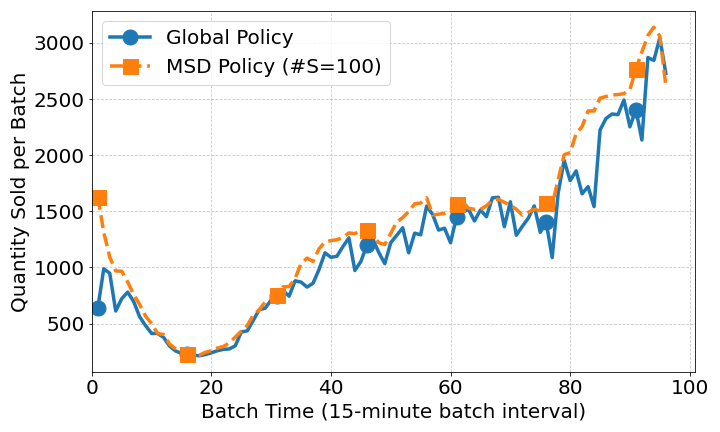

Figure 5(c) compares the GO and MSD policies across key performance metrics. As shown in Figure 5(c)(a), the GO policy consistently achieves higher cumulative revenue than the MSD policy under identical inventory and demand conditions. This difference reflects the distinct recommendation mechanisms of the two policies (Result 5.1.3): by leveraging global information through SPFOM-computed shadow prices, the GO policy constructs higher-value assortments. Figures 5(c)(b) and (c) further illustrate the temporal dynamics. In early batches, the GO policy achieves higher revenue per batch while selling fewer units, whereas the MSD policy sells more units but with lower per-batch revenue. As a result, the MSD policy rapidly depletes inventory and suffers a sharp revenue collapse after around batch 30, while the GO policy maintains a more gradual decline. These results highlight the advantage of the GO policy in sustaining profitability and managing inventory consumption over time, particularly under medium- to long-term operational horizons. From an economic perspective, this advantage stems from its ability to capture the long-term marginal value of inventory through global shadow prices and to use such signals to coordinate assortment decisions across products. A similar economic principle underlies recent work in multi-product inventory systems, where shadow values are used to guide allocation and upgrading decisions in a forward-looking manner (Tang et al. 2025). Recent studies have also shown that even under complex sequential choice and search dynamics, optimal or near-optimal assortment decisions can be guided by simple reduced-form signals, such as last-choice probabilities, which play a role analogous to shadow values in dynamic systems (Gao et al. 2023).

5.2 Extension 2: Network Revenue Management with Bundling

We extend our framework to Network Revenue Management (NRM) with bundling. In this setting, customers (indexed by ) choose from bundles (indexed by ) composed of base products (indexed by ). The resource constraint (6) is generalized as:

| (26) |

where represents the selection of bundle by customer . This formulation introduces a binary resource-request incidence matrix , where each element indicates whether bundle consumes base product , thereby capturing the joint consumption of resources.

Corollary 5.1

Corollary 2 directly extends the results of Theorem 8.1, the full details and proof of which are deferred to the Online Appendix. Intuitively, incorporating the resource-request matrix generalizes the structure of the standard constraint matrix while preserving its full row rank property. By characterizing the spectral properties of this augmented matrix, we adapt the conditions of Theorem 8.1 to verify the linear convergence of Algorithm 2 in the bundling context. These findings reaffirm the robustness and efficiency of the algorithm even under network-based resource-sharing constraints.

6 Computational Case Study for ZOZOTOWN

We evaluate the proposed method in a large-scale empirical setting using real-world data from ZOZOTOWN. In particular, we compare two approaches: global recommendation optimization and segmented recommendation optimization. Further details regarding the experimental setup and specific data preprocessing are provided in Online Appendix 9.

6.1 Empirical Context and Data Overview

Customers browsing a product on ZOZOTOWN are presented with a panel of recommended items. We define a customer’s action of clicking and subsequently adding a recommended item to the cart as a realized choice (treated as a “purchase” record for simplicity), a convention that is consistent with recent work incorporating click behavior into choice models to improve the prediction of customer decisions (Aouad et al. 2025). Only items with available inventory are displayed, ensuring that all observed choices are feasible. Our analysis uses large-scale proprietary transaction data from a single day in June 2024. The dataset contains the 1000 most popular SKUs and records realized choices made by unique customers. For our sequential optimization framework, the 24-hour period is discretized into 96 intervals of 15 minutes each, which defines our operational horizon. This temporal segmentation is purely methodological, does not reflect any inherent customer or product characteristics, and also supports standard anonymization of customer and product information.

6.2 Estimation of Preference Weights in the Choice Model

In this paper, we estimate customer–SKU preference weights using maximum likelihood estimation (MLE). We adopt the standard multinomial logit (MNL) specification for its tractability in large-scale settings (Berbeglia et al. 2022). To capture preference heterogeneity, we first partition users into behavioral segments using -means clustering on standardized customer features, where is determined through an iterative refinement process to ensure sufficient sample sizes for reliable estimation. We then estimate a separate MNL model for each segment (where ). The preference weight for customer belonging to segment is modeled as:

where and denote the intercept and marginal utility coefficients specific to segment . The feature vector consists of the product’s scaled price and one-hot encoded color attributes. Assuming i.i.d. Gumbel shocks, the MNL probabilities are computed using a sampled choice set that includes the observed chosen product and several randomly selected non-chosen alternatives. While more flexible structures (e.g., mixed logit) exist, they are computationally infeasible at our dataset’s scale. The segmented MNL model achieves a practical balance between behavioral interpretability, estimation stability, and computational tractability, providing consistent preference estimates for evaluating our global optimization framework, SPFOM.

6.3 Large-Scale Market Optimization via SPFOM

In this section, we compare the platform’s expected revenue and its inventory overload ratio under the two recommendation approaches over a fixed multi-period horizon. The results in Table 2 represent the average performance across 96 time periods (15-minute operational batches).

| Metric | MSD() | MSD() | MSD() | MSD() | GO |

| Total expected revenue | 7.6e7 | ||||

| Inventory overload ratio | 0.39% |

The table shows the superior performance of the centralized GO approach, which achieves the highest total expected revenue () while maintaining the lowest inventory overload ratio (). Conversely, the MSD performance degrades significantly as the number of segments () increases (revenue drops from at to at ). This outcome confirms that decentralization introduces inherent inefficiency under resource constraints. The GO strategy, with its unified global view, enforces the shared inventory constraint optimally, resulting in higher revenue and a reduced risk of stockouts. MSD, however, suffers from fragmented resource allocation and the accumulation of local estimation errors, causing a catastrophic loss in revenue potential and a severe violation of the global inventory constraint as market granularity increases.

6.4 Multi-Period Optimization via Bid-Price Control

This section compares the time-averaged results of the centralized GO strategy against the decentralized MSD strategy to determine their respective capacities for balancing immediate revenue against long-term inventory preservation.

As shown in Figure 6(d), the Global Policy (GO) significantly outperforms the MSD Policy in generating revenue and fulfilling demand. Specifically, Figure 6(d)(a) and (b) reveal substantially higher cumulative revenue and revenue per batch for GO. Figure 6(d)(d) shows that GO achieves a lower quantity sold per batch, leading to a slower depletion of inventory, as illustrated in Figure 6(d)(c). The GO policy outperforms MSD by internalizing global inventory scarcity through a unified shadow price, avoiding over-allocation to low-value transactions. In contrast, MSD’s decentralized structure assigns effectively zero scarcity cost, leading to systematic misallocation and stockouts. Two diagnostic metrics in Online Appendix 9.4, product sales diversity (entropy) and mean opportunity cost, further highlight these allocation differences through the distribution of chosen products.

7 Conclusions and Future Research

We propose SPFOM, a novel first-order algorithm designed to efficiently solve large-scale RM problems with combinatorial assortment constraints. The method achieves theoretical guarantees while exhibiting competitive empirical performance, scaling effectively to high-dimensional instances where conventional solvers fail to remain practical. In addition to its computational scalability, SPFOM facilitates fine-grained recommendation control through dual-based bid price policies. Globally coordinated decision-making enabled by SPFOM yields superior outcomes compared to decentralized, segment-based approaches, achieving higher revenue and more efficient inventory utilization. The proposed framework can also be naturally extended to NRM problems, where decisions are coupled through shared resource capacities. Future research directions include incorporating data-driven learning modules to jointly estimate customer preferences and optimize assortments in an adaptive fashion (Ferreira et al. 2018, Jia et al. 2021, Cheng et al. 2025). Extending the framework to online or dynamic settings would better capture the operational realities of real-time systems. Another promising avenue is the integration of inventory control policies into the decision-making process (Liang et al. 2021), thereby enhancing coordination between demand learning, assortment optimization, and stock management, particularly under supply constraints or uncertain replenishment dynamics.

References

- Nearly linear-time packing and covering lp solvers. Mathematical Programming 175 (1), pp. 307–353. Cited by: §2.

- Amazon selling stats. Note: https://sell.amazon.com/blog/amazon-statsAccessed: 2024-06-09 Cited by: §1.

- Market segmentation trees. Manufacturing & Service Operations Management 25 (2), pp. 648–667. Cited by: §1.

- The click-based mnl model: a framework for modeling click data in assortment optimization. Management Science 71 (8), pp. 6943–6960. Cited by: §6.1.

- Practical large-scale linear programming using primal-dual hybrid gradient. Advances in Neural Information Processing Systems 34, pp. 20243–20257. Cited by: §2, §4.5, §4.5.

- A comparative empirical study of discrete choice models in retail operations. Management Science 68 (6), pp. 4005–4023. Cited by: §6.2.

- Convex optimization: algorithms and complexity. Foundations and Trends® in Machine Learning 8 (3-4), pp. 231–357. Cited by: §8.3, §8.3, §8.3, §8.3, §8.3.

- From social to purchase: customer selection in social group buying. Production and Operations Management 34 (6), pp. 1512–1530. Cited by: §7.

- Sinkhorn distances: lightspeed computation of optimal transport. Advances in Neural Information Processing Systems 26. Cited by: §3.2.

- Linear convergence of the primal-dual gradient method for convex-concave saddle point problems without strong convexity. In The 22nd International Conference on Artificial Intelligence and Statistics, pp. 196–205. Cited by: §4.2, §8.3.

- Consumer choice models and estimation: a review and extension. Production and Operations Management 31 (2), pp. 847–867. Cited by: §2.

- Online network revenue management using thompson sampling. Operations research 66 (6), pp. 1586–1602. Cited by: §7.

- A general attraction model and sales-based linear program for network revenue management under customer choice. Operations Research 63 (1), pp. 212–232. Cited by: §1, §2, §3.2, §3.2, §3, §4.4.

- Assortment optimization under the sequential click-based choice model. Preprint, submitted August 3. Cited by: §5.1.3.

- Solving assortment optimization with first-order methods and neural networks: a computational framework and public benchmark. Available at SSRN 5671592. Cited by: §2.

- Assortment optimization: a systematic literature review. OR Spectrum 46 (4), pp. 1099–1161. Cited by: §2.

- Multi-armed bandit with sub-exponential rewards. Operations Research Letters 49 (5), pp. 728–733. Cited by: §7.

- Choice network revenue management based on new tractable approximations. Transportation Science 53 (6), pp. 1591–1608. Cited by: §2.

- Assortment and inventory planning under dynamic substitution with mnl model: an lp approach and an asymptotically optimal policy. Technical report Technical report, Tech. rep., University of Michigan, Ann Arbor, MI. Cited by: §7.

- Fast sinkhorn I: an O(N) algorithm for the wasserstein-1 metric. arXiv preprint arXiv:2202.10042. Cited by: §2.

- Pdcs: a primal-dual large-scale conic programming solver with gpu enhancements. arXiv preprint arXiv:2505.00311. Cited by: §2.

- On the choice-based linear programming model for network revenue management. Manufacturing & Service Operations Management 10 (2), pp. 288–310. Cited by: §2.

- CuPDLP-c: a strengthened implementation of cupdlp for linear programming by c language. arXiv preprint arXiv:2312.14832. Cited by: §4.5, Remark 4.4.

- Nearly optimal linear convergence of stochastic primal-dual methods for linear programming. arXiv preprint arXiv:2111.05530. Cited by: §2, Remark 4.4.

- A practical and optimal first-order method for large-scale convex quadratic programming: h. lu, j. yang. Mathematical Programming, pp. 1–38. Cited by: §2.

- CuPDLP. jl: a gpu implementation of restarted primal-dual hybrid gradient for linear programming in julia. Operations Research 73 (6), pp. 3440–3452. Cited by: §2, §4.5.

- Individual choice behavior: a theoretical analysis. Courier Corporation. Cited by: §3.

- A fast and accurate splitting method for optimal transport: analysis and implementation. arXiv preprint arXiv:2110.11738. Cited by: §2.

- External Links: Link Cited by: §2.

- Rounding of convex sets and efficient gradient methods for linear programming problems. Optimisation Methods and Software 23 (1), pp. 109–128. Cited by: §2.

- Efficiency of coordinate descent methods on huge-scale optimization problems. SIAM Journal on Optimization 22 (2), pp. 341–362. Cited by: §2.

- Numerical optimization. second edition, Springer. Cited by: §4.2, §8.2, §8.2, §8.2.

- Computational optimal transport: with applications to data science. Foundations and Trends® in Machine Learning 11 (5-6), pp. 355–607. Cited by: §3.2.

- Open bandit dataset and pipeline: towards realistic and reproducible off-policy evaluation. arXiv preprint arXiv:2008.07146. Cited by: §1.

- A review of choice-based revenue management: theory and methods. European Journal of Operational Research 271 (2), pp. 375–387. Cited by: §2.

- An analysis of bid-price controls for network revenue management. Management Science 44 (11-part-1), pp. 1577–1593. Cited by: §5.1.2, §5.1.2.

- Revenue management under a general discrete choice model of consumer behavior. Management Science 50 (1), pp. 15–33. Cited by: §3.1.

- Multiproduct inventory systems with upgrading: replenishment, allocation, and online learning. Manufacturing & Service Operations Management. Cited by: §5.1.3.

- On the approximate linear programming approach for network revenue management problems. INFORMS Journal on Computing 26 (1), pp. 121–134. Cited by: §2.

- Tractable open loop policies for joint overbooking and capacity control over a single flight leg with multiple fare classes. Transportation Science 46 (4), pp. 460–481. Cited by: §4.4.

- Reductions of approximate linear programs for network revenue management. Operations Research 63 (6), pp. 1352–1371. Cited by: §2.

- Product-based approximate linear programs for network revenue management. Operations Research 70 (5), pp. 2837–2850. Cited by: §2.

Online Appendices

8 Omitted Proofs

8.1 Proof of Lemma 4.1

Without loss of generality, we assume the indices s are ordered such that . Then, note the optimization problem for solving can be solved equivalently through a dynamic programming recursion, as follows: (let )

By an induction argument, we can show that is bounded above by . Then, we derive the greedy approach (try to set as large as possible) must be optimal due to the ordering of .

8.2 Proof of Theorem 4.2

We follow the notation used in this paper. To apply the quadratic penalty theory from Nocedal and Wright (2006), we first define a base feasible set incorporating constraints (7), (8), and (9):

Since and are fixed, finite, and positive parameters, is a closed and bounded set, hence it is compact. To address the resource inequality constraints (6), we introduce non-negative slack variables to reformulate them as equalities: . Following the construction in Theorem 17.1 of Nocedal and Wright (2006), the augmented objective function for our problem is defined as:

| (27) |

where is the quadratic regularization term. To eliminate , we find the value that minimizes this expression. Taking the partial derivative of (27) with respect to and setting it to zero:

Solving for the optimal dual variable, we get . Substituting this back into the objective function, we obtain the regularized objective (15). We note that as , the effective penalty coefficient tends to infinity, which is equivalent to the case in the original Theorem 17.1 of Nocedal and Wright (2006) where the penalty parameter goes to infinity. Since is compact, any sequence of solutions has at least one limit point. According to Theorem 17.1, every such limit point must satisfy the constraints and be an optimal solution to the original problem (6).

8.3 Preliminaries on Linear Convergence

We introduce some notations. By rewriting in matrix form, the problem (10)-(14) considered is equivalent to

where , , is the vector concatenating for times, , where each denotes the feasible set of the constraints eqs. (11) to (13) for , and is formed such that each row is split into blocks of entries, and the -th row is formed by repeating for times, where is the -th standard unit vector of .

Theorem 8.1

Consider Algorithm 2 for some . Let and respectively be the smallest and the largest singular values of . Assume that has full row rank, there is a constant such that for any for all . If and satisfy

then the expected distance from the iterates to converges at a linear rate. More specifically, let , there exists such that such that

Proof of Theorem 8.1. We first reformulate the problem via the conjugate function . The primal objective is -strongly convex and -smooth, implying that is -strongly convex and -smooth with respect to . We then identify a suitable step size for the block coordinate gradient descent update. Under this step size, we construct a ghost algorithm and, using existing results on randomized block coordinate descent, show that the primal error contracts linearly in expectation. Next, we analyze the dual update and derive a linear contraction bound for the dual residual by combining the primal contraction with the Lipschitz continuity of the dual gradient. Finally, the coupled primal–dual recursions yield the claimed linear convergence rate.

We define

then we can easily see that , and is -strongly convex and -smooth, while is -smooth in the sense of Bubeck and others (2015) as it is a linear function of . We see that the conjugate function

is therefore -strongly convex and -smooth with respect to , where and . With the definition of , we also see that the problem considered is equivalent to

| (28) |

Since the objective eq. 28 is strongly convex, we know that there is a unique optimal solution .

We can easily see that the diameter of is upper bounded by from the constraints. Therefore, it is clear that as long as and we take a step size

block coordinate gradient descent at the -th block of gives the exact solution of the subproblem with respect to . On the other hand, if , any and thus any step size is optimal because the objective value remains a constant. Therefore, from our assumption of the upper-boundedness of , our exact subproblem solution is equivalent to conducting the project gradient descent at the selected blocks with any step size .

Now we consider a ghost algorithm

| (29) |

where is a diagonal matrix designating the blocks selected by our algorithm at the -th iteration. It is clear that

| (30) |

Therefore, by using the proof of Theorem 3.12 in Bubeck and others (2015) and the non-expansiveness of convex projections, we can easily obtain

| (31) |

provided that .

On the other hand, we can easily see that , and therefore by defining , eq. 31 implies that

| (32) |

With routine calculations, similar to Proposition 3.3 of Du and Hu (2019), we also have that

| (33) |

Next, for the dual variables, we see that the update is over all coordinates without any stochastic elements. Therefore, it can be seen as conducting gradient descent for the following objective function

and it is clear that is -strongly convex and -smooth just like . Therefore, using eq. 33 and again from the proof of Theorem 3.12 in Bubeck and others (2015), for any , we can obtain after routine calculations that

| (34) |

where .

Summarizing section 8.3 and eq. 32, taking expectations over all iterations, and by defining and , we have the following recursion.

| (35) |

where . From our assumptions and by setting , we have that . Let us define , then clearly

Finally, we just need to bound . It is clear that and is upper bounded by the diameter of . We therefore obtain the claimed result.

8.4 Proof of Theorem 4.3

In Theorem 8.1, we show that, under the existence of a constant and several conditions, Algorithm 2 converges linearly in the general case. In Theorem 4.3, by exploiting the special structure of the SBLP under consideration, we further simplify the conditions required in Theorem 8.1 and provide an explicit choice of the parameter , ensuring linear convergence of the algorithm.

Lemma 8.2

The constraint matrix of the SBLP in standard form has full row rank.

Proof of Lemma 8.2. Consider the SBLP in its standard form. To convert the inequality resource constraints (10) into equalities, we introduce non-negative slack variables for each . The constraints can then be written as . Let the decision vector be defined as . The constraint matrix then takes the following partitioned structure:

where represents the coefficients of the original variables and is the identity matrix corresponding to the slack variables. Since contains a full identity matrix, its rows are linearly independent. Therefore, , which implies that the matrix has full row rank.

Lemma 8.3

The largest and smallest singular values of , denoted by and , can both be taken as 1.

Proof of Lemma 8.3. Following Lemma A.1, the constraint matrix is partitioned as . Consequently, the Gram matrix is given by: . Let denote an eigenvalue of . Since is positive semi-definite, for all . Thus, . This implies . Following the standard normalization in SBLP, we take . Under the normalized structure of the simplex constraints in SBLP, the row sums of are restricted such that the spectral radius of is bounded by . Therefore, , and .

We simplify the various conditions appearing in Theorem 8.1, where the requirements regarding the existence of constant are reduced to the most restrictive one . Hence we get

| (36) |

for any .

Lemma 8.4

for any .

Proof of Lemma 8.4. We analyze how the stationarity condition of KKT couples the primal variables with the dual variables . We define the Lagrangian by incorporating the equality constraint (11) and the similarity inequality constraint (12): . The stationarity condition requires the partial derivative with respect to each to be zero at optimality:

-

1.

For : .

-

2.

For the dummy variable : .

By combining them, we obtain: . Summing this over all resources for a fixed customer :

| (37) |

Hence, it holds

Let , bring it into (36). We obtain . Setting yields a feasible solution.

8.5 Proof of Corollary 4.5

The proof follows directly from Theorem 2. In Algorithm 3, workers independently process mini-batches of size in parallel and aggregate their updates within each iteration. As a result, each iteration effectively utilizes sampled customers, while preserving the same stochastic structure and independence assumptions as in Algorithm 2. Consequently, all arguments in the proof of Theorem 2 continue to hold with the batch size replaced by . In particular, the contraction factor in the expected distance to the smoothed optimum improves from to , yielding the stated result.

8.6 Proof of Corollary 5.1

The proof proceeds by verifying that the augmented matrix maintains full row rank, ensuring the dual problem is both strongly concave and smooth. Consequently, the linear convergence established in Theorem 8.1 applies, provided a valid constant exists, a condition equivalent to identifying a suitable . Unlike the simplified case where is an identity-based structure with unit singular values, the bundle-selling matrix exhibits , necessitating a re-evaluation of the convergence parameters. By simplifying the bounds from Theorem 8.1, we determine a value for to be .

We describe the augmented constraint matrix , which facilitates the transformation of the inequality constraints into a system of linear equations. This is achieved by introducing a vector of non-negative slack variables , where and account for the unused resource capacities and the satisfaction of the selection logic, respectively. The resulting block matrix is partitioned as follows:

To align with the augmented matrix , we define the complete decision vector as . Here, represents the selection probabilities for customer . The matrix is partitioned into three functional layers: (i) Resource Layer: Implements by repeating the incidence matrix across all customers. The identity block maps to slack variables , capturing residual product capacities. (ii) Demand Layer: Enforces demand conservation for each customer (). As these are equality constraints, no slack variables are required. (iii) Selection Logic Layer: Incorporates proportional constraints . The identity block corresponds to slack variables . This construction ensures that maintains full row rank. Following the proofs of Lemma 8.2 and Lemma 8.3, we can see that and .

By simplifying the conditions in Theorem 8.1 and isolating the most restrictive bound, we obtain:

Completing the algebraic simplification of this inequality concludes the proof.

9 Extended Analysis and Details of the Case Study with ZOZOTOWN Data

This section provides supplementary information and detailed methodological breakdowns for the empirical case study discussed in Section 6. The primary goal is to ensure the reproducibility and transparency of our findings. We first detail the complete data preprocessing pipeline and the feature engineering used for the MNL preference estimation (including customer clustering and product attribute definition). Following this, we provide an extended analysis and additional performance visualizations to further strengthen the conclusions drawn in the main paper regarding the comparison between the Global Optimization (GO) and Market Segment Decentralized (MSD) approaches.

9.1 Supplementary Empirical Context

Figure 6 illustrates the operational environment of the ZOZOTOWN recommendation interface from which our empirical data are constructed. When a customer visits the detail page of a particular SKU (highlighted in the blue dashed box), the platform simultaneously displays a set of recommended items directly beneath the focal product (red dashed box). These recommended items constitute the choice set from which the customer may potentially select an alternative item. Each recommended product card includes the item’s image, brand name, and the discounted price currently offered. The recommendation panel typically contains 8 items per page, and customers can scroll to view additional recommended products depending on the category.

On the right-hand side of the product page, ZOZOTOWN displays the available inventory information for each size variant of the focal product (green dashed box). The inventory status is categorized into three levels:

-

•

In stock (sufficient inventory; blue “Add to Cart” button),

-

•

Low stock (inventory almost depleted; displayed with a warning label), and

-

•

Out of stock (greyed-out button and labeled as sold out).

ZOZOTOWN displays only recommended products with strictly positive inventory, so both “in-stock” and “low-stock” SKUs remain visible to users while out-of-stock items are excluded. As a result, customers are always presented with a feasible choice set, and a click followed by an add-to-cart action is treated as the realized choice. For each browsing session, we record the focal product viewed, the set of recommended items displayed at that moment, and the user’s subsequent click and add-to-cart behavior. For every recommended SKU, we also capture its price and real-time inventory level at exposure. In addition, we extract product attributes, such as color, to construct feature vectors for estimating user preference patterns. These data allow us to observe realized choices from feasible assortments while incorporating the product characteristics required to model user–SKU preferences.

9.2 Supplementary Data Information

The empirical context described in Section 9.1 gives rise to a rich dataset capturing user interactions with product pages and recommendation panels on ZOZOTOWN. In our empirical analysis, we focus on a single day in June 2024 and track the behavior of a subset of active users on the platform. For each user, we observe the sequence of clicked products together with the corresponding SKU identifiers, product attributes such as color, and the displayed prices at the moment of interaction. For every SKU appearing in the dataset, we also collect its initial inventory level at the start of the day, abstracting away from any potential restocking during the observation period. Each interaction is time-stamped, enabling us to reconstruct the temporal order of browsing and choice activities. These components jointly form the dataset used for preference estimation and the subsequent case study analysis, as summarized in Table 3.

| #purchases | #customers | #SKUs | #colors | price range (mean) | stock range (mean) | time-spam | |

| Raw | - | - | - | ||||

| Processed | [100, ] (4505) | [1, ] (999) | 23:59:31 |

The initial dataset contained 5,342,966 raw purchase interactions, which was strategically refined to a processed dataset containing 1,372,671 records. This significant filtering process similarly reduced the customer pool from 64,700 to 38,746 active users. The reduction in record count and users is largely attributable to the strict temporal scope applied, confining the observation window to precisely 23:59:31. Despite the reduction, the final processed volume remains substantial, supporting a robust empirical analysis. Along the product dimension, strategic filtering was rigorously applied: the total number of unique SKUs was drastically reduced from 49,526 to 1,000, and the diversity of product colors saw a parallel refinement, dropping from 239 to 145. This focused approach ensures that the analysis and subsequent models concentrate exclusively on the most representative and frequently interacted products, thereby simplifying computational complexity while maintaining coverage of core consumer choice behavior. Furthermore, clear numerical boundaries were established for key variables: the price range was confined to , displaying an average price of 4,505. The price distribution visualization confirms this finding, showing the mean price to be 4,406 and the median price at 3,635, a pattern indicative of a strong positive skew where the majority of products are priced toward the lower end of the range. Concurrently, the initial inventory level (stock range) was set from , with a notably lower mean initial inventory of 999. The explicit lower bound of 1 confirms that all 1,000 products included in the analysis were verifiably available in stock at the moment of user interaction, a critical prerequisite for accurate demand modeling and inventory analysis.

9.3 Estimating Customer–SKU Preference Weights with an MNL–MLE Framework

The adopted framework employs a Segmented Multinomial Logit (MNL) model estimated via Maximum Likelihood Estimation (MLE) to capture unobserved consumer heterogeneity in product preferences. This approach addresses the limitation of a standard MNL model, which assumes homogeneous preferences across all users. The core logic follows a two-stage process: First, customers are clustered into homogeneous groups based on their historical behavior using K-Means; Second, a unique set of utility weights () is estimated for each segment using the MNL-MLE framework.

9.3.1 Stage One: Customer Segmentation via K-Means Clustering

The initial stage involves grouping the total customer base of 38,746 users into distinct preference segments.

Feature Engineering for Clustering. The customer feature matrix () is constructed from historical purchasing data to represent underlying preference traits:

-

•

Price Sensitivity Features: These include the mean purchase price and the standard deviation of purchase prices, which quantify a customer’s spending level and price consistency.

-

•

Color Preference Features: These are represented by the historical frequency of purchasing products of a specific color , indicating strong aesthetic biases.

All constructed features undergo Standardization to ensure that all dimensions contribute equally to the Euclidean distance calculation during clustering:

where and are the mean and standard deviation of the feature matrix .

Optimal Cluster Selection and Iterative Refinement. The initial number of clusters, , is determined using the Elbow Method, minimizing the Within-Cluster Sum of Squares (WCSS):

where is the -th cluster and is its centroid. Following initial clustering, an Enhanced Iterative Cluster Refinement process is applied to enforce a minimum sample size constraint required for the subsequent MLE estimation. A segment is deemed viable only if its total number of purchase records () exceeds a strict training threshold (MIN_RECORDS_CHECK):

where is the total number of parameters (product features plus the intercept term) to be estimated in the MNL model. This iterative process dynamically recalculates the centroids of viable clusters and reassigns all customers from undersized “small clusters” to the nearest viable cluster, ensuring a final set of segments ready for robust estimation.

As illustrated in Figure 7, the Within-Cluster Sum of Squares (WCSS) decreases sharply as increases from 2 up to approximately 102. The rate of reduction begins to slow significantly between and , marking the region of the “elbow”. Beyond , the curve flattens out, indicating that increasing the cluster count provides minimal additional explanatory power for the variance in customer features. Based on this analysis, and balancing the goal of capturing rich heterogeneity with the practical need for computational tractability, we selected as the optimal number of segments. This segmentation method allowed us to partition the customers into 160 distinct groups, each representing a homogeneous set of preference patterns.

9.3.2 Stage Two: Segmented MNL-MLE Estimation

For each of the segments, a separate MNL model is estimated.

The Multinomial Logit Model (MNL). The MNL model is rooted in the assumption that customer chooses the option that maximizes their utility . The utility function for product within segment is specified as a linear combination of its observable features :

where the product features include the standardized price and the color One-Hot Encoding (OHE). Assuming the error terms are IID Gumbel distributed, the probability that a customer in segment chooses option from the choice set is given by:

The choice set is constructed using a sampling method, consisting of the actual chosen product () and randomly sampled non-chosen products.

Maximum Likelihood Estimation (MLE) and Optimization. The segment-specific utility weights are determined by minimizing the Negative Log-Likelihood (NLL) function, which corresponds to maximizing the likelihood of observing the actual choices made by customers in that segment. The NLL function for segment is defined as:

Substituting the MNL probability formula yields the expression to be minimized:

The minimization is performed using the robust L-BFGS-B optimization algorithm, a quasi-Newton method suitable for high-dimensional parameter estimation.

Ensemble Averaging. To enhance the stability and robustness of the estimated parameters against the randomness introduced by the sampled choice sets, the entire estimation process is repeated times, each with a different random seed. The final estimated utility weight vector for each segment is computed as the average of the parameters obtained from all successful runs:

This averaging strategy mitigates variance and provides a more reliable estimation of consumers’ latent preferences.

9.4 Supplementary Results for the Comparison Between GO and MSD

| Metric | GO | MSD | Difference |

| Product Sales Diversity (Shannon Entropy) | GO MSD | ||

| Mean Opportunity Cost () | GO MSD |

The performance disparity between the Global Optimization (GO) and Market Segment Decentralized (MSD) policies is fundamentally rooted in their resource pricing mechanisms, as evidenced by two key metrics.

Analysis of Resource Scarcity Pricing and Allocation Efficiency. The Product Sales Diversity Index is quantified using Shannon Entropy (), a foundational concept in information theory that measures the degree of uncertainty or randomness within a probability distribution. In the context of this study, is applied to the distribution of successful transactions across all distinct product types to assess the uniformity of resource allocation. A higher value indicates that sales are broadly distributed across a greater variety of products (high diversity), while a lower value suggests that sales are highly concentrated on a few specific products (high centralization). The index is calculated using the formula: