Primal-dual splitting for structured composite monotone inclusions with or without cocoercivity

Abstract

In this paper, we propose a primal-dual splitting algorithm for a broad class of structured composite monotone inclusions that involve finitely many set-valued operators, compositions of set-valued operators with bounded linear operators, and single-valued operators possibly without cocoercivity. The proposed algorithm is not only a unification for several contemporary algorithms but also a blueprint to generate new algorithms with graph-based structures using a single transparent convergence analysis. Our approach reduces dimensionality compared with the standard product space technique, which typically reformulates the original problem as the sum of two maximally monotone operators in order to apply splitting methods. It accommodates different cocoercive or Lipschitz constants as well as different resolvent parameters, and yields a larger allowable stepsize range than recent methods. We demonstrate the practicality of the approach by a numerical experiment on cancer detection using the decentralized fused LASSO problem.

Keywords: Distributed optimization, composite monotone inclusions, splitting algorithms, primal-dual algorithms, fused LASSO problem.

Mathematics Subject Classification (MSC 2020): 47H05, 47H10, 65K10, 90C30.

1 Introduction

Many interesting problems such as composite optimization problems, structured saddle-point problems, and variational inequalities can be formulated as monotone inclusion problems [17, 28, 29]. Among the most widely used methods for solving such problems are splitting algorithms, in which computations are performed separately on each operator instead of their sums, see, e.g., [8, 21, 23, 25, 31, 35]. When an optimization problem involves compositions of set-valued operators with bounded linear operators, common mathematical tools such as resolvents can be computed for such compositions, however, it is generally very difficult, thus, not desirable. Instead, primal-dual splitting algorithms [3, 12, 15, 19, 36] are usually used to process the set-valued operators separately using backward steps via their resolvents, while the bounded linear operators are evaluated directly using forward steps on their own or on their adjoints. Considering the primal inclusion and the dual inclusion simultaneously provides us a better understanding of the problem.

Let and be real Hilbert spaces. We consider the primal inclusion

| (1) |

where, for each , is a maximally monotone operator, for each , is a maximally monotone operator and is a bounded linear operator with adjoint operator , and for each , is either a cocoercive operator, or a monotone and Lipschitz continuous operator. Problem (1) arises in a wide range of applications, including location problems [10], image reconstruction [15], and signal processing [17]. The associated dual inclusion in the sense of Attouch–Théra [6] is

| (2) |

When , , and , problem (1) reduces to finding a zero in the sum of finitely many maximally monotone operators that are potentially set-valued. The most well-known algorithm for the classical case is the Douglas–Rachford algorithm [21]. Recently, a splitting algorithm was proposed for by Ryu [31], while a different resolvent splitting for the general case was introduced by Malitsky and Tam [25]. The latter work was then extended into a framework [32] that covers these algorithms. In the setting when , , and , the problems involve not only maximally monotone operators but also single-valued operator which can be used directly by forward evaluations. When and , the forward-backward algorithm [23] is typically used when is cocoercive, while the forward-backward-forward algorithm [35] and the forward-reflected-backward algorithm [24] are commonly applied when is monotone and Lipschitz continuous. Moreover, the authors of [5] developed a distributed forward-backward algorithm for the case where , , and each is cocoercive, as well as a second algorithm for , , and each monotone and Lipschitz continuous. Recently, the forward-backward algorithms devised by graphs in [4] and a class of algorithms in [2] effectively characterized methods that use only individual resolvent evaluations and direct evaluations of cocoercive operators, while a general approach to distributed operator splitting [20] addresses the situations where the single-valued operators may not be cocoercive.

In the setting when , there are many primal-dual algorithms are proposed, but only for some special cases of problem (1). For example, in the case , , and , popular algorithms include the Chambolle–Pock algorithm [15] and an algorithm proposed by Briceño-Arias and Combettes [12]. When , , and , one can use primal-dual fixed-point algorithm based on the proximity operator (PDFP2O) or proximal alternating predictor-corrector (PAPC) [16, 22]. For the case where , , and , or when a Lipschitz and a cocoercive operator are treated simultaneously, we refer interested readers to [18, 19, 30, 36]. When , one can adapt some of the above algorithms and use product space reformulations, even though it may not utilize different structures of algorithm design. Recently, Aragón-Artacho et al. [3] studied the case with , , and in the reduced dimension . Then, to incorporate multiple bounded linear operators with , the proposed algorithm, however, still relies on a product space reformulation.

Most of the aforementioned algorithms reformulate the original problem as the sum of a maximally monotone operator and a skew-symmetric or cocoercive operator, then apply the forward-backward [19, 36] or forward-backward-forward approach [12, 18]. In this work, we introduce a primal-dual splitting algorithm for structured composite monotone inclusions that unifies many well-known algorithms in the literature through a single transparent convergence analysis. Our algorithm provides a different perspective using reduced dimension compared to dimension using product space reformulations which potentially contribute to the theory and applications of primal-dual algorithms. Furthermore, we directly handle the linear operators , rather than through a product space reformulation, which allows us to generate alternative designs with potentially significantly larger stepsizes compared to those in [3, Corollary 1]. Therefore, this approach facilitates distributed computation without central coordination which helps prevent bottlenecks that arise from centralized coordination in practice. In addition, different cocoercive or Lipschitz constants, as well as resolvent parameters are also allowed for distributed implementation without requiring the knowledge of a global cocoercive or Lipschitz constant.

In this work, our main contributions are as follows.

-

(i)

We develop a primal-dual algorithm for structured composite monotone inclusions involving finitely many set-valued operators, composition of set-valued operators with bounded linear operators, and single-valued operators that may not be cocoercive. Our algorithm does not rely on reformulating the original problem as the sum of a maximally monotone operator and a skew-symmetric or cocoercive operator using product space reformulations but rather directly exploit the problem structure to derive different algorithm designs, offer possibly larger stepsize ranges with explicit formulas. For our convergence analysis, we introduce the concept of quasicomonotonicity in Definition 2.1(ii) and its natural connection to quasiaveragedness [20, Definition 2.1].

-

(ii)

The proposed algorithm not only unifies several contemporary methods but also provides a general framework for constructing new graph-based algorithms within a single unified convergence analysis. Notably, our analysis enables the derivation of broader admissible stepsize ranges under weaker assumptions on the coefficient matrices compared with recent methods [2, 3, 20]. Moreover, the algorithm also allows different cocoercive or Lipschitz constants as well as different resolvent parameters suitable for distributed implementation, thereby improving upon certain existing methods. Finally, we explore various choices of the coefficient matrices of the algorithm and examine the effect of stepsizes on the algorithm’s performance in a numerical experiment on cancer detection using the decentralized fused LASSO problem.

The remainder of this paper is structured as follows. In Section 2, we introduce some notations and background materials on set-valued, single-valued operators, Kronecker product, and solution sets of the primal and dual problem. In Section 3, we present our primal-dual splitting algorithm in Algorithm 1 with main convergence results in Theorem 3.11. We discuss the relation to existing algorithms and new algorithms in Section 4. Section 5 provides a numerical experiment on the decentralized fused LASSO problem for cancer detection, examining the performance of the algorithm under different settings of the coefficient matrices and parameters.

2 Preliminaries

In this paper, the sets of nonnegative integers and real numbers are denoted by and , respectively. We assume that and are real Hilbert spaces equipped with their respective inner product and induced norm . Unless otherwise stated, we use the standard inner product in the product space , i.e., for and ,

With this inner product, we say that a linear operator is positive semidefinite, denoted by if, for all , . Strong and weak convergence of sequences are denoted by and , respectively.

For an operator on , we write when is set-valued, and when is single-valued. For such an operator , the domain, graph, fixed-point set, and zero set are defined by , , , and , respectively. The resolvent of is defined by , where denotes the identity operator. We say that is monotone if, for all ,

and maximally monotone if it is monotone and there exists no monotone operator whose graph properly contains .

An operator is -Lipschitz continuous for if, for all , and -cocoercive for if, for all , . By the Cauchy–Schwarz inequality, every -cocoercive operator is monotone and -Lipschitz continuous, which, in turn, means that it is also maximally monotone [8, Corollary 20.28].

For our convergence analysis, we will recall several related concepts.

Definition 2.1.

We say that

-

(i)

is -comonotone [9, Definition 2.4] with if, for all ,

-

(ii)

is -quasicomonotone (with respect to the set ) if, for all and ,

Unless stated otherwise, we will simply say is -quasicomonotone and drop the reference set .

-

(iii)

is conically -averaged [7, Definition 2.1] with if, for all ,

-

(iv)

is conically -quasiaveraged (with respect to the set ) [20, Definition 2.1] if, and for all and all ,

Unless stated otherwise, we will simply say is conically -quasiaveraged and drop the reference set .

Clearly, every conically -averaged operator is conically -quasiaveraged. It is known from [7, Proposition 3.3] that, for , is -comonotone if and only if is conically -averaged. Naturally, we will derive a similar connection between conical quasiaveragedness and quasicomonotonicity.

Proposition 2.2.

Let and . Then is -quasicomonotone if and only if is conically -quasiaveraged.

Take and take any . Then is conically -quasiaveraged

which means is -quasicomonotone. ∎

2.1 Kronecker product, the vector , and the diagonal set

For a matrix , we denote its range and kernel by and , respectively, its transpose by , and its pseudo-inverse by . For a positive diagonal matrix where , we denote its square root matrix by . Clearly, .

In an abuse of notation, we identify matrices with the Kronecker product . Therefore, for any , we have

Let be maximally monotone operators. Given , we define the operator by . It follows that is also a maximally monotone operator. As a consequence, its resolvent is given by . Note that we can write and as diagonal operators

Similarly, we define the diagonal operators

where the operators , , and are from the setup of problem (1).

We denote . When the context is clear, we will drop the subscript and simply write , for example, if , then . Using this notation, we can define the diagonal set

and thus its the orthogonal set is . Again, we will drop the subscript and denote when the dimension is clear. In particular, for , , , and .

2.2 Solution sets of the primal and dual problems

3 A primal-dual splitting algorithm

Throughout this section, for each , each , and each , and are maximally monotone operators, is a bounded linear operator with adjoint operator , and is a monotone and -Lipschitz continuous operator. Let , , and . Define an auxiliary operator by

| (5) |

Let and be positive diagonal matrices. Let , , , and . Given and , we define the operator as

where are defined via the solution operator with

We propose the following primal-dual algorithm.

Remark 3.1 (Conditions for explicitness).

Algorithm 1 can be written in the form

In general, the algorithm is implicit in the sense that the calculation of requires the value of itself. When the first rows of , , , and are zeros, is explicitly expressed as

| (14) |

but the remaining components may still be implicit. Although our convergence analysis of Algorithm 1 holds in this implicit setting, for practical implementation, we are interested in explicit versions, in which depends only on and, for each , the update of depends only on and components with that have already been computed. This property is guaranteed as soon as , , and are strictly lower triangular, equivalently, for all ,

| (15a) | ||||

| (15b) | ||||

| (15c) | ||||

| (15d) | ||||

Equations (15b) and (15c) mean that, for each , exactly one of the following happens:

-

•

;

-

•

;

-

•

.

These conditions, in fact, can be visualized nicely using a block structure in which the matrices , , and have complementary structure as in Figure 1(a). The possible nonzero parts of , , and are in blue, green, and red colors, respectively. Similarly, the conditions on and are illustrated in Figure 1(b).

It is worthwhile mentioning that condition (15) is weaker and easier to verify than the condition in [20, Remark 3.1(i)]. Moreover, based on Figure 1, the coefficient matrices can be easily customized to meet specific computational requirements. In practice, , , and are usually selected such that each column of and (when ), as well as each row of R, has exactly one nonzero entry equal . Similarly, and can be constructed analogously to, or even chosen equal to, and , respectively, as described in Section 4.

Now, we denote , set

and consider the following assumptions on the coefficient matrices.

Assumption 3.2 (Standing assumptions).

-

(i)

.

-

(ii)

.

-

(iii)

if , and if .

-

(iv)

if , and if .

Assumption 3.3 (Positive semidefiniteness).

There exists such that

3.1 Fixed-point encoding and preliminary results

Lemma 3.5 (Fixed points and Kuhn–Tucker points).

Suppose Assumption 3.2 holds. Then the following hold:

-

(i)

If and , then , , and .

-

(ii)

If , then there exists such that and .

Consequently, if and only if .

Since , it holds that

which leads to

Therefore, . This together with Remark 3.4(ii) and Assumption 3.2(i)(ii)(iv) implies that

Hence, as claimed.

(ii): Assume that . Then and . So, there exists such that

| (16) |

Define and . It follows that

| (17) |

Define , we have

| (18) |

Next, we will find such that

| (19) |

i.e., . Thus, to establish the existence of , it suffices to prove that

Indeed, we check that

due to by Assumption 3.2(ii), by Remark 3.4(ii), and (16). Therefore, we have proved the existence of satisfying (19).

The following lemma characterizes the cluster points of the sequence generated by Algorithm 1.

Lemma 3.6.

(i): Let be any vector such that . By Remark 3.4(i), , and so for some . As , since , one has

For all with , choosing , and all other entries equal to zeros, we derive

| (20) |

Next, since , using Assumption 3.2(iv) and (20), we have that, for all ,

which completes the proof of (i).

(ii): For each , and , we set

where is given by (5), which means

| (21) |

For each , set and . Then and , which are equivalent to

This can be written as

where

| (22) |

Letting be given by

we derive that

| (23) |

As are monotone and Lipschitz continuous, they are maximally monotone operators with full domain. By (21), are also maximally monotone operators. Using [8, Corollary 25.5(i), Example 20.35], is a maximally monotone operator as the sum of a maximally monotone operator and a skew symmetric linear operator.

Now, we show that the left-hand side of (23) converges strongly to . In view of (i), it suffices to show that as . We note that, for each ,

| (24) |

due to by (i) and is Lipschitz continuous by the Lipschitz continuity of . By the definitions of and , and Remark 3.4(i),

Noting from Assumption 3.2(iv) that , we have , which implies that

| (25) |

where we use (by Assumption 3.2(ii)) and (by (i)). Combining (24) and (3.1) with (22), we deduce that as .

Since is a weak cluster point of , there exists a subsequence, denoted by without relabeling, such that . It follows from (i) that and for some . We also have that

| and |

By combining with (3.1),

| (26) |

Since the graph of a maximally monotone operator is sequentially closed in the weak-strong topology [8, Proposition 20.38(ii)], passing to the limit in (23) and using (i) and (24), we obtain that

which together with (26) yields

| (27) |

Therefore,

| (28) | ||||

which implies that , and thus . As a result, .

Next, we have from (21) and Assumption 3.2(iii) that . By summing up the relations in (27), we derive

Since , it follows that . Finally, by (28), if the first rows of , , , and are all zeros, then . ∎

Next, we establish the convergence of Algorithm 1 in the presence of Fejér monotonicity.

Lemma 3.7.

Suppose Assumption 3.2 holds and the first rows of , , , and are entirely zeros. Let and be the sequences generated by Algorithm 1 and suppose that as . Then the following hold:

-

(i)

If is bounded, then so is .

-

(ii)

If is Fejér monotone with respect to , then as .

-

(iii)

As , if , then and with , , and .

(i): Since the first rows of , , , and are all zeros, we have from (14) that and . By the nonexpansiveness of ,

Since, for each , is bounded, so is , which together with Lemma 3.6(i) implies the boundedness of . The boundedness of then follows from the nonexpansiveness of along with the boundedness of , , and .

Now, let be an arbitrary weak cluster point of . By passing to another subsequences if necessary, there exist and such that is a weak cluster point of . According to Lemma 3.6(ii), . By [8, Theorem 5.5], converges weakly to .

(iii): Since converges weakly to , it is bounded, so is also bounded due to (i). Let be an arbitrary weak cluster point of . Then is a weak cluster point of . By Lemma 3.6(ii), , , , and . Thus, and do not depend on the choice of cluster points, and we must have . Together with the weak convergence of , we obtain that , which completes the proof. ∎

We observe that with :

| (29) |

where . Thus, the algorithm can be written as

Our aim is to prove that is conically quasiaveraged in the space with the (scaled) inner product

| (30) |

for and the corresponding induced -norm

In view of Proposition 2.2, we will show that is quasicomonotone. Thus, the next technical lemma is a key ingredient in our analysis.

Lemma 3.8 (A metric inequality for ).

Let , , , and . Then

Set , , , and . Then

| (31) |

By the definition of in (13), we have and , where

So, and . Set . Since is monotone,

Rearranging terms and using (31), we obtain

| (32) |

The first term on the right-hand side of (3.1) is rewritten as

| (33) |

where the last identity follows directly from the definition of and -norm. Next, set , . Then and , or equivalently, and . Since and is monotone,

Thus, the fourth term on the right-hand side of (3.1) can be estimated as

Adding the third terms on the right-hand sides of (3.1) and (33) to this inequality, and setting , , and , we obtain

3.2 Convergence with or without cocoercivity

Lemma 3.9 (Conical quasiaveragedness).

By Lemma 3.5(i), for some . It then follows from Remark 3.4(ii) that . Therefore,

| (35) |

using the monotonicity of .

Let , , and denote the -th rows of the matrices , , and , respectively. By the Cauchy–Schwarz inequality, the Lipschitz continuity of the , and the AM-GM inequality, we derive that

| (36) |

where the second last equality uses . Next, it follows from (3.2) and (36) that

Substituting this into the inequality in Lemma 3.8 and using the fact that , we obtain (34). Since , the quasicomonotonicity of follows from (34), and the conical quasiaveragedness of then follows from Proposition 2.2. ∎

Lemma 3.10 (Conical averagedness under cocoercivity).

Since , using the equality and the cocoercivity of the , we have the estimation

where and denote the -th rows of the matrices and , respectively. Noting that

we obtain

which implies (37) due to Lemma 3.8. Since , the comonotonicity of follows from (37). This together with [7, Proposition 3.3] implies the conical averagedness of . ∎

We now arrive at convergence properties of Algorithm 1.

Theorem 3.11 (Convergence properties).

Suppose and Assumptions 3.2 and 3.3 hold. Let and be the sequences generated by Algorithm 1 with in .

-

(i)

If , then, as ,

-

(a)

with .

-

(b)

, , and with , , and , provided that the first rows , , , and are entirely zeros.

-

(a)

-

(ii)

If are cocoercive, , and , then, as ,

-

(a)

and if , then .

-

(b)

.

-

(c)

with .

-

(d)

and with , , and , provided that the first rows of , , and are entirely zeros.

-

(a)

(i): By Lemma 3.9 and [20, Proposition 2.2], we obtain (i)(a) and the Fejér monotonicity of with respect to . Together with Lemma 3.7(ii)–(iii), this implies (i)(b).

(ii): First, (ii)(a) and (ii)(b) follow from Lemma 3.10 and [7, Proposition 2.9]. Next, since and for some (see Remark 3.4(iv)), we derive from Lemma 3.10 and Assumption 3.3 that, for all ,

Letting and recalling that and is bounded, we obtain (ii)(c). Finally, (ii)(d) follows from (ii)(b) and Lemma 3.7(iii). ∎

We consider a special case of problem (1) when , that is,

| (38) |

In this case, Algorithm 1 becomes

| (41) | ||||

| (48) |

The following result is a direct consequence of Theorem 3.11.

Corollary 3.12 (Convergence without single-valued operators).

Suppose , Assumption 3.2 holds, and for some . Let and be the sequences generated by Algorithm 1 with in satisfying . Then, as ,

-

(i)

. Moreover, if .

-

(ii)

.

-

(iii)

and with , , and , provided that the first rows and are entirely zeros.

Remark 3.13 (On the parameters , , and ).

Based on Assumption 3.3, we can derive the range for the parameters involved.

- (i)

-

(ii)

Assumption 3.3 holds if and only if

where denotes the infimum of the generalized Rayleigh quotient. We note that the resolvent parameter of is , rather than , and each is thus associated with the resolvent parameter . Similarly, the resolvent parameter of is , so each corresponds to the parameter .

- (iii)

4 Realizations of Algorithm 1

Example 4.1 (Algorithm for , , and ).

Consider a special case of problem (1) with , , and , namely,

To solve this problem, we apply Algorithm 1 with , , , and setting , . The coefficient matrices are then given by ,

Algorithm 1 now reduces to

| (50) | ||||

| (51) |

Using Moreau decomposition [8, Theorem 14.3(ii)], in (50) becomes

Set and . Then (50) becomes

Since and , the second equation in (51) becomes , or equivalently,

We obtain the algorithm

In turn, when , this algorithm simplifies to

| (52) |

which closely resembles, but is not exactly the same as, the Condat–Vũ algorithm [19, 36], where the dual update takes the form .

Example 4.2 (Algorithm for ).

We consider another special case of problem (1) when , that is,

With and , Algorithm 1 becomes

| (53) |

which not only recovers but also improves [20, Algorithm 1] significantly. When and each is cocoercive, (53) reduces to [2, Algorithm 1]. The scheme (53) further extends many existing algorithms including the frugal and decentralized splittings [32], the forward-backward algorithms devised by graphs [4], the forward-backward and forward-reflected-backward algorithms for ring networks [5], the forward-reflected-backward algorithm [24], the sequential and parallel forward-Douglas–Rachford algorithms [11], the generalized forward-backward algorithm [27]. Moreover, the scheme generates different product-space formulations of the Davis–Yin algorithm, including a reduced dimensional variant, and a generalization of Ryu splitting algorithm; see [20, Section 4].

In this case, Assumptions 3.3 reduces to

| (54) |

where is given by (49). The introduction of yields significantly weaker assumption than [20, Assumption 3.2(v)] and helps unifies the key inequalities and its variants in [20, Lemma 3.6 and Remark 3.7], thereby allowing a larger explicit stepsize range. To be more specific, one sufficient condition for (54) is

which includes the case when

When , the latter upper bound for becomes if (matching [20, Theorem 3.10]), and if , which improves on from [20, Theorem 3.9].

Another sufficient condition for (54) is , which reduces to [20, Equations (18) and (20)] if , and to [2, Assumption 4.7] if and .

When for some , as in Remark 3.13(iii), (54) yields an even larger upper bound for , namely

| (55) |

This situation commonly arises in graph-based splitting algorithms when the underlying graphs coincide. In that case, the condition is automatically satisfied; see Example 4.4.

Moreover, the explicitness condition in Remark 3.1 is simple, clear, and easy to customize. The method also accommodates different cocoercive or Lipschitz constants for the operator and the convergence analysis in Theorem 3.11 is unified for both cases with or without cocoercivity through the introduction of the notion of quasicomonotonicity.

In the sequel, we generate a class of algorithms with graph-based structures which easily satisfy Assumption 3.2. Moreover, we provide a simple choice for the coefficient matrices that achieves a large range for the stepsizes. Here, we briefly introduce the main idea of graph theory and refer readers to [20, Section 4] for more detail.

Let , where , , be a weighted undirected connected graph with , , and weight matrix . Let be a weighted connected subgraph of with , and weight matrix such that for all ,

i.e., the weight on each edge of is not greater than the weight on the corresponding edge of .

Let where if and if . Thus is a strictly lower triangular matrix. Let , where , is the degree matrix of . Let , where . It is clear that . Furthermore, let be an onto decomposition of the Laplacian matrix , i.e., . If is a tree, then can be chosen as the incidence matrix for some orientation of (see [4, Remark 2.17]). This graph-based selection of , , and satisfies Assumption 3.2(i)–(ii).

Example 4.3 (Algorithms based on ring and sequential graphs).

Let be a ring graph and be a sequential graph, both with unit weights. Since is a tree, we take as the incidence matrix. Then , ,

It can be seen that Assumption 3.2(iv) holds and . Taking , we have and . According to Remark 3.13(iii), once Assumption 3.2(iii) also holds, Assumption 3.3 becomes , which is satisfied as soon as

| (56) |

where is defined in (49).

Case 1: Each is -cocoercive. Then we set

which satisfy Assumption 3.2(iii). Algorithm 1 becomes

| (57) |

which reduces to [3, Algorithm 1] when (no single-valued operator and .

Letting , we obtain and . The condition (56) is equivalent to

In particular, when , the condition reduces to .

From now on, we work in the setting where each is -cocoercive, which allows us to take . In the absence of cocoercivity, one may instead choose any satisfying together with conditions (15b)–(15c) (if an explicit form is desired).

Example 4.4 (Algorithms based on complete, sequential, and star graphs).

We consider the particular instance of problem (1) when . Let with , , and for , meaning that and have the same graph structure but may differ in their edge weights. Then .

Case 1: and are complete graphs. In this case, we take as in [4, Proposition A.2], which is not the incidence matrix of but still satisfies . We now derive an algorithm based on the structure of complete graphs.

Complete graph algorithm:

Then Assumption 3.2(iii)–(iv) is satisfied. Taking , we have and . Moreover, , which yields . Assumption 3.3 is guaranteed when , which is equivalent to

| (60) |

Algorithm 1 reduces to

| (61) |

Case 2: is a tree. Then . Let be the incidence matrix of given by

Let and are defined based on the incidence matrix of ,

Using the coefficient matrices defined above, Assumption 3.2(iii)–(iv) is readily verified. Letting , we have that , , , and . In view of Remark 3.13(iii), Assumption 3.3 holds whenever

| (62) |

To illustrate, we give examples for algorithms based on the sequential and star graphs, both of which have tree structures.

Sequential graph algorithm:

Star graph algorithm:

Remark 4.5.

In the case where , i.e., no single-valued operator , the stepsize range allowed in Case 1 of Example 4.3 is , for . This range significantly improves upon that in [3, Corollary 1] which is only for , , and .

Moreover, we not only extend the result to the setting when but also design several algorithms with different graph structures including the complete graph (61), the sequential graph (63), and the star graph (64) algorithms. It follows from (60) and (62) that when (so that ), the stepsize range for the complete graph algorithm is

| (65) |

while for the sequential and star graph algorithms it is

| (66) |

As noted in Remark 3.13(ii), the resolvent parameters associated with and are and , respectively. It is clear that handling the linear operators directly, not rather than via the product space reformulation, can lead to alternative algorithmic designs with significantly larger stepsizes, as in (65) and (66).

Remark 4.6.

Although the new algorithms in Example 4.4 are derived for solving problem (1) when , they can be readily adapted to the case . Specifically, we apply the complete, sequential, and star graph algorithms to problem (1) with maximally monotone operators , compositions of with bounded linear operator , and cocoercive or monotone Lipschitz operators . Then by letting operator (or ), we obtain the corresponding algorithms. This is useful in some cases, as shown in the next section.

5 Numerical experiments

In this section, we present a numerical experiment on the decentralized fused LASSO (least absolute shrinkage and selection operator) problem to test different choices of the coefficient matrices, which correspond to different graph structures, in Algorithm 1. We also investigate the influence of stepsizes and the relaxation parameter on the performance of the algorithm.

Fused LASSO:

The famous LASSO problem is to find a sparse least squares solution of a linear system via -penalization. The fused LASSO [34] extends the classical LASSO in the sense that it encourages the sparsity of not only the solution but also the differences between adjacent components of the solution, i.e., the flatness of the solution. Specifically, given , the fused LASSO can be written as

| (67) |

where , and with , , and otherwise.

Decentralized fused LASSO:

Decentralized fused LASSO for cancer detection

We apply the decentralized fused LASSO to the problem of “hot-spot detection” which was studied in [33]. In particular, the goal is to detect the regions of gain or loss in comparative genomic hybridization (CGH) data. CGH is a technique used to measure the DNA copy numbers of selected genes across the genome. In cancer cells, mutations can lead to deletions or amplifications of genes, resulting in fewer or more DNA copies. CGH array experiments report the ratio of DNA copy numbers in tumor cells relative to those in reference cells. In CGH analysis, positive values indicate potential DNA copy number gains, while negative values suggest possible losses. Consequently, values close to zero correspond to normal genes, whereas profiles exhibiting multiple regions of gains and losses may indicate the presence of cancer. In contrast to the classical fused LASSO, the decentralized approach has an important advantage of preserving patient privacy, which is critical in healthcare data management.

The results of CGH experiments are often interpreted manually by biologists, which can be time-consuming and may lack accuracy. Therefore, the fused LASSO can be applied for automatic interpretation. In this experiment, we use the data from [33] to represent CGH measurements from 2 glioblastoma multiforme (GBM) tumors, which is a very aggressive and common type of primary brain cancer.

Parameter settings and results:

We consider problem (68) with and the data are partitioned into row blocks randomly. The dataset is given and the matrix is the identity matrix, following [33, Section 2]. Then is obtained by adding an independent and identically distributed Gaussian noise with variance to .

For the parameters, we set , , and , for . For each algorithm, we compute the corresponding upper bound and (or for the sequential and star graph algorithms) using (60) and (62). We then set and (or ), where . Finally, we select and set .

We measure the performance of the algorithms using the relative error

| (70) |

where the exact solution is computed by CLARABEL v0.11.1 solver, called via CVXPY v1.8.1. The settings for the solver, including absolute duality gap tolerance, relative duality gap tolerance, feasibility check tolerance are adjusted to to achieve higher precision. For simplicity, we examine the effect of varying parameters , and . The behaviors of the sequential and star graph algorithms are very similar, thus we only include the results for the sequential graph algorithm.

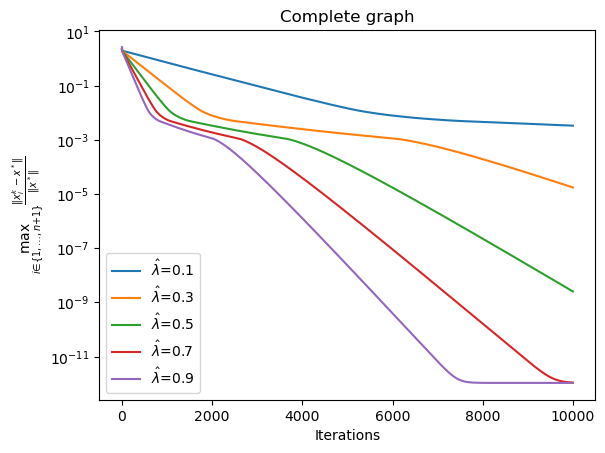

First, we examine the effect of on the performance by fixing , , , and varying . The results for the complete graph and the sequential graph algorithms are provided in Figure 2. They indicate that both algorithms perform better when is small. Repeating the experiment with varying , we observe the opposite behavior: the algorithms achieve the best performance when is large.

Next, we investigate how the algorithms behave as varies while , , and are fixed. Figure 3 presents the results for the complete graph and the sequential graph algorithms, showing that both algorithms converge faster when is large. In contrast, when varying within , we observe that the algorithms perform best for small values of . Similar behaviors with respect to and were also reported in [3, Section 5.2]. These behaviors may be explained by a trade-off between aggressiveness and stability: while larger values of lead to more aggressive updates, smaller values can produce more stable and better-conditioned iterations, resulting in faster practical convergence. As also noted in [24, Remark 2.8], the optimal convergence rate does not always occur for the largest possible stepsize.

Now, we compare the performance of three algorithms using , , and . In Figure 4(a), the data are represented by dots, while the solution obtained by the CVXPY solver and the complete graph algorithm are shown by red solid and green dashed lines, respectively. The result suggests that the complete graph solution successfully detects both regions of gains and losses and matches the solution given by the CVXPY solver mentioned above. The relative error shown in Figure 4(b) indicates that the complete graph converges faster in terms of iteration counts compared to the others. However, this comes at the cost of increased runtime. The sequential graph and star graph algorithms exhibit slightly different at the beginning but nearly identical after that.

We note that the performance of the algorithms can indeed vary depending on the coefficient matrices, as reflected in the numerical experiments. Choosing these matrices is, in general, a nontrivial task that has been studied independently [13, 14]. The primary aim of our numerical experiments is to demonstrate the generality and applicability of the proposed framework. We focus on clarity and accessibility, providing interpretations for specific scenarios rather than performing an exhaustive sensitivity analysis or drawing broad conclusions regarding performance.

Acknowledgements.

The research of MND, MKT and TDT was supported in part by Australian Research Council grant DP230101749.

References

- [1]

- [2] A. Åkerman, E. Chenchene, P. Giselsson, and E. Naldi, Splitting the forward-backward algorithm: a full characterization, arXiv:2504.10999.

- [3] F.J. Aragón-Artacho, R.I. Boţ, and D. Torregrosa-Belén, A primal-dual splitting algorithm for composite monotone inclusions with minimal lifting, Numer. Algorithms 93(1), 103–130 (2023).

- [4] F.J. Aragón-Artacho, R. Campoy, and C. López-Pastor, Forward-backward algorithms devised by graphs, SIAM J. Optim. 35(4), 2423–2451 (2025).

- [5] F.J. Aragón-Artacho, Y. Malitsky, M.K. Tam, and D. Torregrosa-Belén, Distributed forward-backward methods for ring networks, Comput. Optim. Appl. 86(3), 845–870 (2023).

- [6] H. Attouch and M. Théra, A general duality principle for the sum of two operators, J. Convex Anal. 3(1), 1–24 (1996).

- [7] S. Bartz, M.N. Dao, and H.M. Phan, Conical averagedness and convergence analysis of fixed point algorithms, J. Glob. Optim. 82(2), 351–373 (2022).

- [8] H.H. Bauschke and P.L. Combettes, Convex Analysis and Monotone Operator Theory in Hilbert Spaces, 2nd ed., Springer, Cham (2017).

- [9] H.H. Bauschke, W.M. Moursi, and X. Wang, Generalized monotone operators and their averaged resolvents, Math. Program. 189(1-2), 55–74 (2021).

- [10] R.I. Boţ and C. Hendrich, A Douglas–Rachford type primal-dual method for solving inclusions with mixtures of composite and parallel-sum type monotone operators, SIAM. J. Optim. 23(4), 2541–2565 (2013).

- [11] K. Bredies, E. Chenchene, D.A. Lorenz, and E. Naldi, Degenerate preconditioned proximal point algorithms, SIAM J. Optim. 32(3), 2376–2401 (2022).

- [12] L.M Briceño-Arias and P.L. Combettes, A monotone + skew splitting model for composite monotone inclusions in duality, SIAM J. Optim. 21(4), 1230–1250 (2011).

- [13] R.L. Bassett and P. Barkley, Optimal design of resolvent splitting algorithms, Math. Prog. Comp., (2026).

- [14] P. Barkley and R.L. Bassett, Coupled adaptable backward-forward-backward resolvent splitting algorithm (CABRA): A matrix-parametrized resolvent splitting method for the sum of maximal monotone and cocoercive operators composed with linear coupling operators, arXiv:2505.13927.

- [15] A. Chambolle and T. Pock, A first-order primal-dual algorithm for convex problems with applications to imaging, J. Math. Imaging Vis. 40(1), 120–145 (2011).

- [16] P. Chen, J. Huang, and X. Zhang, A primal–dual fixed point algorithm for convex separable minimization with applications to image restoration, Inverse Probl. 29(2), 25011 (2013).

- [17] P.L. Combettes and J.-C. Pesquet, Proximal splitting methods in signal processing, in: H.H. Bauschke, R.S. Burachik, P.L. Combettes, V. Elser, D.R. Luke, and H. Wolkowicz (Eds), Fixed-Point Algorithms for Inverse Problems in Science and Engineering, Springer, New York, (2011).

- [18] P.L. Combettes and J.-C. Pesquet, Primal–dual splitting algorithm for solving inclusions with mixtures of composite, Lipschitzian, and parallel-sum type monotone operators, Set Valued Var. Anal. 20(2), 307–330 (2012).

- [19] L. Condat, A primal–dual splitting method for convex optimization involving Lipschitzian, proximable and linear composite terms, J. Optim. Theory. Appl. 158(2), 460–479 (2013).

- [20] M.N. Dao, M.K. Tam, and T.D. Truong, A general approach to distributed operator splitting, J. Math. Anal. Appl. 562(2), 130692 (2026).

- [21] J. Douglas and H.H. Rachford, On the numerical solution of heat conduction problems in two and three space variables, Trans. Am. Math. Soc. 82(2), 421–439 (1956).

- [22] Y. Drori, S. Sabach, and M. Teboulle, A simple algorithm for a class of nonsmooth convex-concave saddle-point problems, Oper. Res. Lett. 43(2), 209–214 (2015).

- [23] P.L. Lions and B. Mercier, Splitting algorithms for the sum of two nonlinear operators, SIAM J. Nume. Anal. 16(6), 964–979 (1979).

- [24] Y. Malitsky and M.K. Tam, A forward-backward splitting method for monotone inclusions without cocoercivity, SIAM J. Optim. 30(2), 1451–1472 (2020).

- [25] Y. Malitsky and M.K. Tam, Resolvent splitting for sums of monotone operators with minimal lifting, Math. Program. 201, 231–262 (2023).

- [26] S. Noschese, L. Pasquini, and L. Reichel, Tridiagonal Toeplitz matrices: properties and novel applications, Numer. Linear Algebra Appl. 20, 302–326 (2013).

- [27] H. Raguet, J. Fadili, and G. Peyré, A generalized forward-backward splitting, SIAM J. Imaging Sci. 6(3), 1199–1226 (2013).

- [28] R.T. Rockafellar, Monotone operators associated with saddle-functions and minimax problems, in: F.E. Browder (Ed.) Nonlinear functional analysis, Proc. Symp. Pure Math. 18, 241–250 (1970).

- [29] R.T. Rockafellar and R. Wets, Variational Analysis, vol. 317. Springer, Berlin (1998).

- [30] F. Roldán, Forward-primal-dual-half-forward algorithm for splitting four operators, J. Optim. Theory. Appl. 204(1), 11 (2025).

- [31] E.K. Ryu, Uniqueness of DRS as the 2 operator resolvent-splitting and impossibility of 3 operator resolvent-splitting, Math. Program. 182(1-2), 233–273 (2020).

- [32] M.K. Tam, Frugal and decentralised resolvent splittings defined by nonexpansive operators, Optim Lett. 18(7), 1541–1559 (2023).

- [33] R. Tibshirani, P. Wang, Spatial smoothing and hot spot detection for CGH data using the fused lasso, Biostatistics 9(1), 18–29 (2008).

- [34] R. Tibshirani, M. Saunders, S. Rosset, J. Zhu, and K. Knight, Sparsity and smoothness via the fused lasso, J. R. Stat. Soc. Ser. B (Stat. Methodol.) 67(1), 91–108 (2005).

- [35] P. Tseng, A modified forward-backward splitting method for maximal monotone mappings, SIAM J. Control Optim. 38(2), 431–446 (2000).

- [36] B.C. Vũ, A splitting algorithm for dual monotone inclusions involving cocoercive operators, Adv. Comput. Math. 38(3), 667–681 (2013).