Bounds on inequality with incomplete data

Abstract

We develop a unified nonparametric framework for sharp partial identification and inference on inequality indices when the data contain coarsened observations of the variable of interest. We characterize the extremal allocations for all Schur-convex inequality measures, and show that sharp bounds are attained by distributions with finite support. This reduces the computational problem to finite-dimensional optimization, and for indices admitting linear-fractional representations after suitable ordering of the data (including the Gini coefficient and quantile ratios), we express the bound problems as linear or quadratic programs. We then establish inference for the upper and lower bounds using a directional delta method and bootstrap confidence intervals. In applications, we compute sharp Gini bounds from household wealth data with mixed point and interval observations and use historical U.S. grouped income tables to bound time series for the Gini and quantile ratios.

- Keywords:

-

Inequality indices, Incomplete data, Interval data, Partial identification, Linear-fractional program, Fractional program, Wealth inequality, ELSA data, Historic income inequality.

1 Introduction

It is often important to study inequality in settings where the variable of interest is only partially observed. These include studies when researchers draw upon historical data tables in previously published sources, use data from organizations which group individual records for privacy reasons, or draw upon statistical surveys which allow respondents to report interval responses. In such environments, an inequality index (such as the Gini coefficient, among others) will be set identified in general. While point identification could be obtained under strong assumptions - such as imposing a functional form for the distribution of the variable of interest, or assuming homogeneity within data groups - we instead focus on characterizing and estimating this identified set. Specifically, we develop a unified framework that (i) delivers sharp, nonparametric bounds for a broad class of inequality indices under several observational regimes; (ii) provides computationally tractable algorithms to obtain those bounds; and (iii) gives a general inference procedure for them. These allow us to gain more credible understanding of the level of inequality in these settings, without placing unrealistic assumptions on the data.

Viewed abstractly, we study a setting in which the inequality functional is set identified. Here is a latent scalar outcome with distribution , is an inequality functional, and the observed data reveal only a coarsened version of : for each unit, we observe an interval such that . In addition, we allow for auxiliary information about the distribution of , such as overall or subgroup means, which can be encoded as linear (in)equality restrictions on the feasible distributions. The identified set of interest is the set of values taken by , where ranges over all distributions of consistent with the observed interval information and any auxiliary linear restrictions. Our goal is to characterize and estimate the sharp lower and upper bounds on this set through optimization of . Our procedures are simple to implement with off-the-shelf solvers, scale well with sample size, and can easily incorporate additional linear information when available. The bounds are sharp in the sense that every value within the bound interval can be attained by some distribution consistent with the observed information and auxiliary restrictions.

Section 2 formalizes the setting we study and focuses on two observational regimes common in empirical work, defined by the nature of the available information. Scenario 1 covers the case where there are a collection of non-overlapping intervals within which each observation’s value is known to lie. These intervals may be predetermined (e.g. survey brackets) or constructed ex post, either exogenously or on the basis of percentile ranges of the responses. Scenario 2, by contrast, features individual-specific intervals that may overlap across individuals, as is common when sensitive variables are elicited through unfolding bracket designs. We allow intervals to degenerate to point observations in both scenarios; the framework therefore accommodates data sets that combine exact and interval observations111This occurs for example in our empirical application of Scenario 2, where many respondents report exact wealth values while others report intervals.. The key distinction is that Scenario 1 imposes a non-overlapping structure on the intervals, while Scenario 2 permits arbitrary overlap, leading to a different feasible set of latent distributions and, correspondingly, different sharp bounds for .

Our key insight is that many inequality indices, such as the Gini coefficient, the 90/50 quantile ratio, and others (possibly with mild modifications), can be expressed as linear-fractional functions of the sorted vector of the variable of interest. This representation is the key computational observation: it turns an infinite-dimensional optimization over feasible distributions into a finite-dimensional program with a globally optimal solution. Section 3 develops this idea in the context of Scenario 1 and shows that the problem of finding sharp bounds can be cast as a linear program in terms of the original variables (e.g., income or wealth), using well-known results in optimization theory developed by Charnes and Cooper (1962). Additional linear inequality or equality constraints can be incorporated naturally, so the framework is organized around empirically distinct observation schemes rather than around special cases of auxiliary information. We also illustrate that, in the special case with no additional constraints, the Gini coefficient (which we consider as the most prominent index in the family of linear-fractional indices after sorting) can be rewritten as a quadratic-to-linear objective in terms of the unknown mass shares assigned to the interval boundaries. In this form, the problem can be solved using results from the fractional programming literature, such as Dinkelbach (1967). We propose algorithms to implement this approach.

Section 3 also provides solution-form results for linear-fractional indices (after sorting) and for general Schur-convex inequality indices within Scenario 1. These results identify conditions under which the optimizers of the inequality indices of interest are supported on either a fixed number of points or on a number of points that increases sufficiently slowly with the sample size, which is later used in the asymptotic analysis. For linear-fractional indices, a broad range of additional linear constraints can be incorporated. For Schur-convex indices, the admissible auxiliary restrictions are more structured, but still include the main forms of auxiliary information emphasized in the paper.

Section 4 focuses on Scenario 2. We derive bounds on inequality indices in the presence of individual-specific interval data. We first characterize the forms of the optimizers for both linear-fractional and general Schur-convex measures, and then use these results to develop generic computational approaches for this scenario. These approaches rely on identifying mass shares allocated to a set of points known ex ante. The section also presents an alternative, direct method formulated in terms of the original observations for the Gini coefficient, and the same construction extends to other linear-fractional measures. We state the Scenario 2 results for the baseline case without additional distributional constraints because this is the empirically relevant case in our application; adding linear constraints amounts to augmenting the same finite-dimensional formulation. The informational environment of Scenario 2 is somewhat similar to that studied by Manski and Tamer (2002). However, their analysis focuses on partial identification of conditional mean functions in regression models, whereas our objective is to obtain sharp bounds for global distributional measures, which requires a different geometric, computational, and inferential treatment.

Section 5 develops statistical inference by viewing the bound endpoints as value functions of a constrained optimization problem over probability measures. Under the regularity conditions stated there, this value function map is directionally differentiable, which yields asymptotics for the estimated lower and upper bounds and bootstrap validity for inference. Although much of our computational discussion focuses on linear-fractional indices, the asymptotic argument also applies to several other inequality measures of interest, including the Theil, mean-log deviation, and Atkinson indices, when the conditions in Section 5 are satisfied. In our formulation, the feasible set is characterized through collections of piecewise-affine linear functionals of the latent distribution, possibly involving estimated nuisance objects such as cutoffs or point-data shares. This abstraction allows the grouped-data and interval-data environments studied in the paper, as well as closely related variants, to be analyzed under a common framework.

Section 6 presents a brief application for each scenario. Firstly, we illustrate the methodology by looking at wealth inequality using data from the English Longitudinal Study of Ageing (ELSA) which is characterised by having complex interval responses. This application naturally fits our Scenario 2. Our second application uses historical U.S. income distribution tables to construct time-series bounds for the Gini coefficient, selected quantile ratios, and the Hoover index under grouped information, with additionally available linear information taken into account where possible. Taken together, the results demonstrate the value of a flexible, transparent toolkit for studying inequality when incomes and wealth are only partially observed. As well as providing credible bounds for inequality in modern-day liquid savings wealth and the historical trends in US income inequality from the 1930s to the 1960s, these applications also demonstrate how the size of the resulting bounds depends on the quantity and complexity of the underlying interval data and the granularity of source material in the form of distributional information or additional data tables.

Related Literature. Within the inequality-measurement literature, related work studies partial identification of inequality or spread measures under coarse data. Stoye (2010) provides elegant characterizations of the identification regions for the expectation and several spread parameters, including the Gini coefficient, when the underlying distribution is observed only through interval-censored or otherwise coarsened data. Our setting differs in several important respects. First, we allow for overlapping interval information of the type considered in Scenario 2, which Stoye (2010) does not address. Second, we incorporate auxiliary linear restrictions arising from additional data sources. Third, Stoye (2010) focuses exclusively on characterizing identification regions and does not provide computational or inferential methods for the grouped-data environment he considers, which is most closely related to our Scenario 1A. By contrast, we develop tractable algorithms and establish inference for the bound endpoints via a directional delta method with bootstrap validity, making the bounds implementable in the settings we consider.

Other existing literature has studied selected special cases of Scenario 1, leading to valuable insights for bounding inequality measures. Many contributions, however, examine one particular configuration of auxiliary information at a time – e.g., known overall mean, known subgroup means, or knowledge of specific points on the Lorenz curve, and are typically not designed to extend beyond the specific case they treat. Much of this literature constructs bounds by interpolating the Lorenz curve from a small set of known points: Gastwirth (1972) uses subgroup means and produces non-sharp bounds, while Mehran (1975) uses known Lorenz curve points to attain sharp bounds. Murray (1978) takes a different route, giving a computational approach to finding Gini bounds under a known overall mean.

These papers illustrate the usefulness of bounding approaches in a variety of grouped-data environments, but each is tailored to a specific piece of auxiliary information. By contrast, our framework treats auxiliary information generically through linear (in)equality constraints and remains applicable when subgroup means or Lorenz-curve points are unavailable. Even within our Scenario 1, this substantially enlarges the set of feasible data environments.

To our knowledge, existing work does not provide sharp bounds and formal inference for settings such as Scenario 2, where individuals are observed through overlapping intervals. Most existing methods are developed for environments in which groups partition the support of income or wealth and are therefore mutually exclusive and ex-ante ordered. These approaches do not directly extend to the informational environments considered here. When intervals overlap across individuals, the feasible set of latent distributions has a different geometric structure, and techniques based on Lorenz-curve interpolation or group-level aggregation are no longer directly applicable. As a result, this setting raises distinct conceptual and computational challenges.

Our paper also contributes to the sparse literature on statistical inference for inequality bounds. McDonald and Ransom (1981) provides inference in the setting of Gastwirth (1972) using their closed-form Gini bounds, while Gastwirth, Nayak, and Krieger (1986) derives joint asymptotic distributions for Gini bounds and extends the analysis to other measures. Dedduwakumara and Prendergast (2019) proposes a parametric bootstrap when subgroup means are available. Our approach remains applicable in all these cases and beyond, without requiring closed-form bounds or restrictive informational assumptions.222A complementary literature imposes parametric structure on the income distribution; see Jorda, Sarabia, and Jäntti (2021) for a survey. Our approach is distribution-free and can be used as a sensitivity benchmark for parametric extrapolations.

Related methodological work includes Cowell (1991), who derives solution forms for strictly Schur-convex inequality measures when either the overall mean or the subgroup means are known in our Scenario 1. In contrast, we allow for general (not necessarily strictly) Schur-convex measures and characterize solution forms under a broader class of linear (in)equality restrictions in Scenario 1. We also obtain solution-form results for general Schur-convex measures in Scenario 2.

Finally, our setting naturally connects to ecological inference and data combination, where individual-level distributions are learned from coarse micro data combined with aggregate information from other sources (see Cross and Manski (2002)). We contribute by providing a unified value-function approach that yields sharp, finite-sample-implementable bounds for widely used inequality indices and by developing bootstrap-valid inference for the set-identified parameters. Recent econometric work on partial identification under combined data includes Pacini (2019), D’Haultfoeuille, Gaillac, and Maurel (2024). We differ from this work in both objective and method by focusing on inequality indices and exploiting structural properties (such as Schur-convexity or linear-fractional representations).

2 Data Scenarios and Inequality Indices

We study settings where a variable of interest , such as income, wealth, consumption or wages, is not observed exactly but only through interval restrictions. Formally, for each unit there is an unobserved realization , and we observe an interval known to contain it, i.e. , where are (possibly estimated) finite interval limits. The collection summarizes the observable information, while denotes the unobserved realization vector. We focus on two scenarios that cover many applications.

Definition 1 (Scenario 1).

There exists a finite collection of non-overlapping intervals , , with , such that for each unit there exists with . Thus the support of is coarsened through membership in one of finitely many common brackets. The boundaries may be deterministic (e.g. fixed survey categories) or stochastic (e.g. sample quantiles), with stochastic boundaries assumed to be estimable by an asymptotically linear estimator.333As the group boundaries are often finite-dimensional, this condition is usually quite weak. An example is when the group boundaries are given by quantiles of the empirical distribution. These estimate the population quantiles under standard conditions. Whether the group boundaries are deterministic or not makes no difference to computation of the bounds – only to statistical inference.

Without loss of generality, intervals are ordered such that for 444When boundaries coincide (e.g. one bracket is “” and the next is “”), we interpret the brackets as half-open so that membership is unambiguous. This convention is immaterial for our results.. In addition to interval information, we may have auxiliary data in the form of linear constraints, expressed as or , where and are potentially estimated from data.555Later, in our computational treatment of this scenario, we will express these constraints in this form for an ordered latent vector.

A rich set of auxiliary information can be incorporated either by refining the group structure or by adding linear constraints. For instance, if the sample median is known and lies in group , we can split into and and update the group counts accordingly. Thus, the knowledge of percentiles can be incorporated through the refinement of intervals rather than in the form of additional constraints to take into account in optimization.

The additional linear-restriction setup covers many cases of interest, including known subgroup means or income-share restrictions. For example, knowledge of the overall sample mean can be imposed through , while knowledge that the mean in group equals adds the restriction . Likewise, if a point on the Lorenz curve is known for some , where , then one can impose the linear restriction . While prior work typically treats such cases in isolation and rarely develops inference, our framework accommodates a broad class of auxiliary information that can be expressed through the linear equality/inequality restrictions studied in this paper. It also allows such information to be combined across multiple data sources within a unified computational and inferential framework.

A fixed number of non-overlapping groups featured in Scenario 1 is common in historical or privacy-binned data such as the historical income distribution tables reproduced in Figures A.1 and A.2 in the online supplement. We study both the simple case with no auxiliary information (1A), in which only are observed, and the richer case (1B), where interval indicators are supplemented with linear constraints. We allow for the possibility that , which leads to a setting with mixed point and interval data and non overlapping groups. In many applications, however, the data consist purely of intervals.

By contrast, Scenario 2 allows overlapping intervals, as in interval-response surveys that follow decision trees.

Definition 2 (Scenario 2).

Each unit has an individual-specific interval , . Intervals may overlap arbitrarily and need not admit a common ordering.

Intervals in this scenario are individual-specific and many of them will potentially be different. Like in Scenario 1, this allows for for some , ultimately leading to scenarios of mixed point and interval data. An example of this is explored in our application using data from English Longitudinal Study of Ageing (ELSA, see Section 6.1). Auxiliary linear information can be added here by the same logic as in the passage from Scenario 1A to Scenario 1B, but we keep Scenario 2 in its baseline form because this is the case commonly encountered in interval-response survey data.

In both scenarios we characterize the identified set via a finite-dimensional optimization problem, which yields both fast computation and a useful statistical theory.

A key ingredient is that many common inequality indices can be written, after sorting, as linear-fractional functions of the outcome vector:

where are known vectors and is understood to be sorted so that

| (2.1) |

To ensure these indices are well-defined, we assume throughout that denominators are strictly positive, i.e. for all feasible . Our two leading examples are the following:

Gini coefficient. Under (2.1), this takes the form of , where . This fits the above equation with and , where for any , denotes the -vector of ones.

Quantile ratio. The sample quantile ratio for quantile indices (e.g., ) fits our setup by taking and , where denotes the th canonical basis vector in .

Other linear-fractional statistics include weighted or generalized Gini indices, the top- income share, the Palma ratio, percentile ratios, and the Bonferroni index. While our main computational results apply to the linear-fractional family, our characterization of the identified set extends to any continuous and Schur-convex inequality function. Beyond the linear-fractional examples, this includes the Generalized Entropy family (including the Theil and mean-log-deviation indices), as well as the Atkinson, Eltető–Frigyes, Kolm, and Zenga indices, and the Herfindahl–Hirschman index when applied to income shares. In certain special cases, such as the Hoover index, we can still leverage linear programming ideas to obtain fast computation even though the index itself is not linear-fractional (discussed for Hoover in more detail before Proposition 2). We require some mild assumptions on the support of data in order to work with certain indices: for example, log-based indices such as the Theil index require all to be bounded away from , while quantile-based indices such as the 90-50 ratio require a separate regularity condition: a Lipschitz assumption on the relevant quantiles, together with a local density bound away from zero around those quantiles. All details are given in relevant sections and in the appendix.

3 Computation in Scenario 1

Because the feasible set is compact and connected, and is continuous, the image of the feasible set under is a compact connected subset of , hence a (possibly degenerate) closed interval. Therefore the identified set is fully characterized by its upper and lower bounds, obtained by minimizing and maximizing over the feasible set.

3.1 Charnes-Cooper transformation for optimizing linear-fractional inequality indices

To compute sharp nonparametric bounds for a linear-fractional , we solve

| (3.1) |

subject to (2.1),

| (3.2) |

and letting denote the number of observations in group :

| (3.3) |

Optimization of (3.1) subject to (2.1), (3.2) and (3.3) constitutes a linear-fractional problem, and it is well known how to convert it to a linear program by means of the Charnes and Cooper (1962) transformation. To illustrate how this can be accomplished, let us rewrite the constraints shaping the feasible set in the matrix form. The ordering (2.1) can be written as where is the matrix of first differences whose elements , , are 1, elements , , are -1, and all the other elements are 0. The constraints can be written as and , where

and is the identity matrix of size . Overall, if we denote

then the constraint set can be written as .

Charnes-Cooper transformation. Our linear-fractional problem can be solved as the following linear program: max_z,t r_1(n)^⊤ z subject to H_n z -b_n t ≤0, r_2(n)^⊤z=1, t > 0. This reformulation of the linear-fractional program is obtained by the well-known Charnes-Cooper transformation with , The optimal solution for yields the solution of the original problem as . This reformulation is attractive because it reduces the problem to linear programming, and also naturally allows one to incorporate a variety of additional information through the constraints . If is very large (say, in millions), one can utilize the population-size invariance property of an inequality metric to scale down the computational problem to a more feasible one, at the cost of a small approximation error.

3.2 Solution form for linear-fractional inequality indices

The form of the optimal solution depends on the additional linear constraints . Propositions 1 and 2 characterize the solution. Proposition 1 treats Scenario 1A, first for general linear-fractional measures and then for strictly Schur-convex ones.

Proposition 1 (Scenario 1A).

With only constraints (2.1) and (3.3), an optimal solution to (3.1) lies at the interval boundaries, i.e. , where is the group index of containing .

Additionally, if is strictly Schur-convex, then:

-

(a)

For the minimizer , there exists such that for in groups , and for in groups .

-

(b)

For the maximizer , there exists such that for (if ), if , and for (if ). Thus, at most one group may have some units assigned to and others assigned to .

The result of Proposition 1 allows reformulation of the optimization problem over a -dimensional parameter , where represents the proportion of units in group assigned to , with assigned to . The exact reformulation will depend on the vectors and in the linear-fractional definition. In the case of the Gini coefficient, we can reformulate the objective function as

| (3.4) |

where , , is a symmetric matrix of differences between interval boundaries, and is a vector of weighted boundaries:

This function needs to be optimized over .

An analogous form can be constructed for any linear-fractional for any linear-fractional index with the strict Schur-convex property; non-Schur indices (such as quantile ratios) are handled separately below. For the lower bound of the strict Schur-convex one, Proposition 1 implies that a minimizer takes the form , with a switch from 0 to 1 at some group . The sharp lower bound is computed by evaluating at vectors , , and selecting the minimum. For the upper bound, a maximizer takes the form with and potentially any in .777The atomic nature of the argmax and argmin may suggest that imposing smoothness on the c.d.f. of the latent variable could sharpen the bounds. However, smoothness alone is unlikely to help, since the step-function c.d.f.s corresponding to the argmax and argmin can be approximated arbitrarily closely by smooth c.d.f.s. Restrictions on the upper or lower bounds of the p.d.f. of , if it exists, could potentially tighten the bounds.

The observation that our sharp inequality bounds can be taken as dependent only on a finite-dimensional parameter 888This is when is fixed. Our statistical theory will allow to grow with sample size. will be a cornerstone of our statistical theory; analogous finite-dimensional reductions appear in the more general settings we consider.

We now outline a general approach to maximizing or minimizing the quadratic-to-linear objective in (3.4). While minimization is unnecessary in Scenario 1A by the results of Proposition 1, developing this framework prepares us for Scenario 2.

Consider the maximization of (3.4). Following Dinkelbach (1967), we introduce a family of subproblems indexed by :

where , and we let define the analogous problem. By Dinkelbach (1967), the function above is continuous, strictly decreasing on any interval where , and it is the supremum of affine functions of , hence convex. Under the sign conditions and (which hold here since ), there is a unique zero .

We solve for using bisection : at each step evaluate at the midpoint and update the bracket according to the sign; this is given in Algorithm 1, which iteratively locates the solution with arbitrary tolerance (e.g., ). This differs from the classical Dinkelbach (1967) procedure (and also procedures in subsequent literature), and achieves geometric convergence since , and is always contained within whichever of the intervals and are selected in the -th iteration of the algorithm. Note that the optimization in is over the full set , not the grid . This greatly speeds computation, at the cost of an asymptotically negligible approximation error as becomes dense (see Lemma 4). Optimizing over also allows one to work solely with sample shares in each interval, as the sample size is no longer needed to construct .

The lower bound can be computed by adapting Algorithm 1: replace with , keep the same sign update rule as in the maximization case (increase if and decrease if ), and use the stopping condition . This is redundant in Scenario 1A (Proposition 1) but may be needed more generally. Let us now discuss the computation of other linear-fractional inequality indices.

Quantile ratio. This inequality index is not strictly Schur-convex. In Scenario 1A, sharp bounds for the sample quantile ratio are immediate: the upper bound is and the lower bound is , where but for .999We interpret the upper bound as if . Hence, a maximizer (minimizer) can be taken at the interval boundaries. Since only and matter for the objective, the optimal solution is not unique.

Hoover index. While the Hoover index is not linear-fractional, we can leverage linear programming ideas to ensure fast computation. For each , consider a linear-fractional objective subject to (2.1), (3.3) (in Scenario 1B also subject to (3.2)) and additional constraints , for . For some such the additional constraints may result in an empty feasible set. But there will be for which it is non-empty. For all with non-empty feasible set optimize it using the methods outlined above. Among solutions for different , choose the one that gives the maximum value of the objective and the one that gives the minimum.

Proposition 2 characterizes the solution in Scenario 1B. With a fixed number of constraints, the optimal solution is supported on finitely many values (possibly sample-dependent) and the proposition bounds how the number of distinct values can grow as constraints are added. This result is important for our asymptotic theory.

Proposition 2 (Scenario 1B).

Let be a linear-fractional measure under (2.1). The additional constraints are given by , , for some and matrices and . Assume that the feasible set defined by these constraints together with (2.1) and (3.3) is non-empty. For each , let and denote the number of rows of and that involve variables from group . Suppose that , .

3.3 General results for Schur-convex indices

Although our computational emphasis is on indices that are linear-fractional after sorting, we also present solution-form results for a general Schur-convex inequality index . This identifies the structure of sharp optimizers beyond the linear-fractional class while keeping the computational development focused on the measures used in our applications.

Theorem 1.

Consider a Schur-convex inequality index . Suppose the components of the vector are ordered according to (2.1). Suppose the constraints are and described by and matrices and , respectively. Suppose all the constraints describe a non-empty feasible region.

Denote and let denote the submatrix of formed by the extraction of non-zero columns corresponding to elements of group and also rows of that contain elements of group (thus, its dimension is with and ). Suppose each has block-diagonal structure

where each row in each block matrix consists either only of 1 or only -1.

Then there is an optimizer of subject to (3.3), (2.1), , such that:

-

(a)

For any group , with no equality or inequality constraints on its elements the maximizer contains at most one element from group which is strictly in the interior of , and for the minimizer all the values within group are identical.

-

(b)

For any group , with some equality or inequality constraints on its elements, the minimizer does not contain more than different elements in group (assuming ), where is the number of blocks of consecutive elements in group for whom there are no constraints, and the maximizer does not contain more than different elements in group (assuming ).

First, note that Theorem 1 allows constraints on just some (not necessarily all) elements of group . Second, note that conditions on matrix allow for constraints on several subgroups within group . Suppose . Then we could have constraints (equality as well inequalities from above or/and below) e.g. on the sum of , on the median value in that group and on the sum . A special case of the condition given in Theorem 1 is when is invariant to a permutation of columns corresponding to elements within each group : that is, is invariant to permutation of columns . From the practical point of view, the condition on matrix in Theorem 1 is consistent with many empirically relevant settings, as most real-world constraints will treat some (or all) variables within a given interval group in a symmetric way. All the examples of constraints we consider (such as subgroup means, income ratios, points on the Lorenz curve, overall means) satisfy this condition. This same symmetry is what makes the later measure formulation natural: once the objective and constraints depend only on blockwise masses or moments, permutations within a group are irrelevant, so the explicit ordering constraints used in the computational derivations become bookkeeping devices rather than substantive restrictions.

An important conclusion from Theorem 1 is that asymptotically we can look at optimizers of as those composed from a finite number of values, both in a sample and asymptotically (as long as the structures of and remain stable as not to lead to the increase of with ).

4 Computation in Scenario 2

Scenario 2 allows mixed point observations and individual-specific intervals that may overlap. Unlike Scenario 1, the data generally cannot be summarized by counts in a fixed set of non-overlapping brackets and therefore cannot be fully ordered ex ante (only partially ordered). As a result, the linear-fractional structure of the inequality measures of interest cannot be exploited or transformed into linear programs, since these measures typically admit known linear-fractional representations only under a full ordering.

We start by splitting individuals into two subsets: those that have point data on and those with genuinely interval data. Define the Point Set as , and the Interval Set as . Let and . Thus records boundary values coming only from the genuinely interval observations in , while augments with the realized point observations from . Conceptually, point data are just degenerate intervals; we separate them only for computation, because their locations are already fixed whereas only observations in generate unknown allocations.

Unlike Section 3, we first present solution-form results, and only after that discuss computational aspects. In our solution structure results we first consider general Schur-convex inequality indices in Theorem 2, and then Schur-convex indices with a linear-fractional representation (with a fixed ordering of in the sample) in Theorem 3.

Theorem 2.

Consider data that comply with Scenario 2. Let be a Schur-convex function.

There is a maximizer (minimizer ) of subject to constraints of Scenario 2 that satisfies the following:

-

(a)

Vector contains at most one element corresponding to whose value does not belong to .

-

(b)

Set of values of all components in corresponding to observations in contains at most one value which is not in (but multiple elements may potentially take it).

The main insight of Theorem 2 is that at an extremum almost all interval observations can be placed at the interval boundary values in . This identifies the structure of sharp solutions in Scenario 2 beyond the linear-fractional class. Theorem 3 refines the result of Theorem 2 for linear-fractional indices and shows that at most one interior placement (for the max) and at most one interior value overall (for the min) - as described in Theorem 2 - have to be in .

Theorem 3.

Consider data on that comply with Scenario 2. Suppose that a Schur-convex takes a linear-fractional form upon a fixed ordering of elements in . Then

-

(a)

A maximizer of can be chosen such that its components lie in , with at most one component for some belonging to .

-

(b)

A minimizer of can be chosen such that its components lie in , with at most one value in the set belonging to .

Theorem 3 turns the structure of solutions into implementable programs as it allows us to look for a solution in the form of numbers allocated to each point when we consider linear-fractional inequality indices. Equivalently, point data are just degenerate intervals whose allocation is already known, so they enter as known masses at values in , whereas only observations in generate unknown allocations and, hence, the ones that need to be constrained.

First step: Ordering

Without loss of generality we can suppose that all unique elements of are arranged in the increasing order , and all unique elements in are ordered in an increasing way. Let index the position of in ordered .

Second step: Exhaustive inequality constraints

on and their various sums, where is the number of points from found at particular .

Take any consecutive block (; ), The lower bound counts intervals fully contained in the block:

The upper bound counts intervals that overlap the block (even partially):

The case yields the equality .

Constraints for non-consecutive unions are implied by those for consecutive unions (lower bounds additive; upper bounds subadditive with gap adjustments), adding no new information. Indeed, for , for the lower bound the constraint ∑_u ∈[b_d_1, b_d_1+1] ∪[b_d_2, b_d_2+1] N_u ≥∑_i ∈Q 1(I_i ⊆[b_d_1, b_d_1+1] ∪[b_d_2, b_d_2+1]) is the same as

with the latter implied by the existing lower bounds on consecutive unions. For the upper bound constraint for ,

Since the desired inequality from above would be implied by

or equivalently, , which is the upper bound inequality for a consecutive union and which is accounted for already.

Third step: Optimization

Since it is difficult to optimize subject to integer restrictions on all , it makes sense to rewrite the constraints obtained in the second step in terms of shares in the overall sample by dividing both the left-hand and the right-hand sides by . Then for any and any , letting implies that

| (4.1) |

We now focus on Gini in the class of linear-fractional inequality indices. Let . These are known shares as they measure the frequency of encountering a point from in the point sample . Some of them will naturally be zero as not all the points in are found in . Then the overall share of every point in the sample is the sum of a known and unknown , with the latter being subject to constraints in (4.1).

One could use various equivalent forms of Gini in terms of and . We write the elements of in increasing order as . For any , let and denote the (unknown) interval-share and (known) point-share at , respectively. Consider then the following form.

| (4.2) |

This is a quadratic-to-linear-fraction in that needs to be optimized in subject to (4.1). Its optimization is the quadratic-to-linear-fractional program. Let denote all that satisfy (4.1).

In practice the optimization of can follow Dinkelbach (1967) via the parametric quadratic programs f_2; max(λ)= max_^ϕ ∈S_^ϕ (12 ∑_i =1^ |U| ∑_j =1^ |U| (^ψ_u_i+^ϕ_u_i)(^ψ_u_j+^ϕ_u_j)|u_i-u_j|- λ∑_i=1^|U| (^ψ_u_i+^ϕ_u_i)u_i ) (and for the minimum). The unique root where 101010 is continuous, strictly decreasing and is convex in . gives the sharp upper bound; Algorithm 2 (analogous to Scenario 1, using bisection on with global optimization at each step) converges to . The lower bound is obtained analogously by finding the unique root where , with the same bisection sign rule as in the maximization case: increase when and decrease when .

Like in Scenario 1, in case of linear-fractional measures there may be a way to create computational procedures in terms of the original rather than using the process with unknown and known shares. Exact procedures may depend on the exact form of the share. If we take Gini index again as an example, then we can establish the result in Proposition 3 below that would lead to alternative computational procedures.

Proposition 3.

Consider data on that comply with Scenario 2. Let be the Gini index.

(a) Then there exists a minimizer of that satisfies the conditions of Theorem 3 (the components of lie in , with at most one value in the set belonging to ) and, in addition, the following property holds: there exists such that (i) for every with ; (ii) for every with ; (iii) for every with .

(b) Furthermore, there exists a maximizer of that satisfies the conditions of Theorem 3 and the stronger property that all components in the set belong to . In addition, there exists such that (i) for every with ; (ii) for every with ; (iii) for every with .

Proposition 3(a) establishes that the minimizer compresses unknown values for toward a common threshold , pushing bounded intervals to their nearer extreme and aligning overlapping ones at . The proposition implies an efficient minimization strategy based on a search over candidate thresholds in . For each candidate construct the assignment for , , according to the pattern in part (a) of the proposition. A single pass over candidates, computing the Gini index each time, is guaranteed by the proposition to return the global minimum and a corresponding minimizer .

Proposition 3(b) shows that a maximizer stretches the distribution by pushing uncertain values away from a common threshold . Unlike minimization, it does not uniquely prescribe the boundary assignment for the (typically small) subset . When is small, exhaustive enumeration of the possible boundary assignments for these intervals is feasible and exact. For larger , fast steepest-ascent greedy-flip heuristics (or beam search) often recover the global optimum in practice. Additional dominance rules can further prune the search: if satisfy and , then assigning the narrower interval to its upper bound precludes assigning the wider interval to its lower bound , and symmetrically for the dual case. Crucially, the proposition dramatically simplifies computation even within proportion-based optimization frameworks discussed earlier as all uncertain values lie on the finite boundary set , eliminating the need for continuous proportions over , which leads to a potentially large reduction in the number of unknowns.

5 Asymptotics of sharp bounds

This section establishes asymptotic theory and bootstrap validity for the vector of sharp bound estimators. Our key observation is that each endpoint can be written as the optimal value of a constrained optimization problem over probability measures. Letting the constraint right-hand sides be , the nuisance parameters indexing the constraint maps (such as group boundaries) be , and letting and denote the proportion and distribution of point observations, we collect these into a vector . We show below that the population bound endpoints can be written as for a function . Similarly, the estimators computed in Sections 3–4 can be written as , where approximates and .

After formalizing this representation, the argument proceeds in three steps. First, solution-form results imply that each estimator can be represented by measures supported on a small number of points. Second, this representation yields the expansion

Finally, we show that is Hadamard directionally differentiable and apply the directional delta method of Fang and Santos (2019) together with a functional CLT for . The presence of only directional differentiability in general means that inference relies on an -out-of- bootstrap, though the standard nonparametric bootstrap is also valid in special cases.

Throughout, we let circumflexes denote sample analogues and the subscript population counterparts. Let denote the support of , and let be the set of Borel probability measures on , equipped with the Wasserstein-1 () metric. For , let denote the Dirac measure at , and let denote the inequality index.

Writing the Problem Using Measures

Population problem: We first write the population bounds as an optimization problem over probability measures. Let denote the latent distribution of the variable of interest. When both grouped and point observations are present, write , where denotes the distribution of point data and their population share.121212In Scenario 1, degenerate brackets can be absorbed into , so that . As described in Sections 3–4, the data imply linear restrictions on . For example, the statement that of the data lie in a group is encoded as , while a mean restriction is encoded as . This covers the restrictions used in the paper, including group probabilities, subgroup means, and overall means.

Our estimands are the minimum and maximum of subject to these restrictions. Because the number of restrictions may increase with , we allow the population problem to contain countably many of them. Letting collect the equality and inequality restrictions, respectively, we suppose that for each , and are linear-functionals generated by the piecewise-affine integrands described below. This includes moment restrictions such as and indicator restrictions such as . We therefore define the feasible set as

where collects the right-hand sides of the equality and inequality restrictions. In Scenario 1A, only equality restrictions are imposed and these are encoded through . Scenario 1B adds further equality and/or inequality restrictions through or , while Scenario 2 uses inequality restrictions only. In the population, the only information available about is that and componentwise. As such, our information about is summarized by the requirement that .

This representation lets all sampling uncertainty enter through . Define . Let , and when convenient identify with its cumulative distribution function viewed as an element of . Write

equip with the product sup norm, and for write . When has finitely many components, we view it as an element of by padding with zeros. Then letting

we define our estimand by , where . Thus is the vector of lower and upper bounds on the inequality index implied by the population restrictions and the point-data component.

Sample problem: The same representation applies at the sample level. Conditional on the observed coarsening pattern, the sample problem gives sharp bounds for the inequality index of the realized sample, and under sampling it serves as a plug-in estimator of the population bounds. The original formulations in Sections 3–4 optimize over vectors , but because both and the restrictions depend on only through its empirical measure, the same problem can be written as optimization over empirical measures .131313In the measure formulation there is no need to impose an ordering on .

In addition, is unobserved. The data yield an estimator , where collects the estimated right-hand sides of the restrictions, collects any additional estimated nuisance quantities entering and (for example empirical cutoffs, quantiles, or smooth transforms thereof), and and are the empirical share and distribution of point data. The distinction between and is therefore only that enters on the right-hand side, whereas enters through the restriction maps. Let denote the feasible set in the -th sample problem, obtained by imposing all equality restrictions together with the inequality restrictions included at stage ; write for the choice used at sample size . For integers , let be the subset supported on at most points, and let further require each mass to be an integer multiple of . The exact indexing convention for the -th problem is given in the Appendix.

Lemma 1.

Fix any . If has at most distinct values and lies in , then . Conversely, any can be written as for some with at most distinct values.

As a result, the sample restrictions on are equivalent to . We therefore define

so that the computed estimator is , where denotes numerical optimization error and satisfies . Our theory studies the convergence of to as , allowing as additional inequality restrictions are included.

Regularity conditions

Each regularity condition below controls one part of the difference between and . For integers , let denote the vector of lower and upper endpoints obtained by replacing with . When we take . In the case , fix for some , and define on , since does not depend on , and let

Assumption 1 formalizes the idea that, for purposes of asymptotics, the optimization problem defining each bound can be effectively reduced to measures with a small number of support points.

Assumption 1.

There exists a sequence and a neighborhood of such that

Moreover, whenever , we also have .

Assumption 1 requires that restricting attention to measures supported on at most points changes the vector of endpoints by at most , uniformly over local perturbations of . In the settings considered here, this follows directly from the characterization results in earlier sections. Recalling that is the number of groups and is the number of constraints, one may take in Scenario 1A, for linear-fractional indices in Scenario 1B, and in Scenario 2; see Propositions 1, 2, and Theorems 2–3. Aside from numerical optimization error, the approximation error is then exactly zero. The substantive content of Assumption 1 is that is tied to the complexity of the restriction set rather than to the ambient dimension . This holds in all of the above settings, since is bounded by features of the restriction set.

Assumption 2 places restrictions on the constraints allowed in the problem. Write , where collects the cutoff values at which a restriction may change form and the remaining nuisance quantities. After relabeling coordinates if needed, each cutoff is either a fixed endpoint or a coordinate of . For each , let denote the relevant cutoffs, and write

Let and index the equality and inequality restrictions, let denote the integrand for restriction , and let collect those equality restrictions whose integrands are constant on each partition interval. This covers grouped-share and overlap restrictions, mean restrictions, and ratio or Lorenz restrictions; when groups are defined by quantiles of the latent distribution, the estimated quantiles enter through . In Scenario 2, .

Assumption 2.

There exist constants such that, for all sufficiently large , all in a neighborhood of , all , and all , the -th restriction has the form , where

The maps and are either constant or affine in , , and . In addition:

-

(i)

The number of equality restrictions remains finite as .

-

(ii)

Every restriction whose integrand is constant on each partition interval is the indicator of an interval of the form , , or , where and are partition boundaries.

-

(iii)

Whenever a partition boundary is an endpoint of a step-function equality restriction or a point at which some other restriction changes affine form, the cumulative indicator belongs to .

Assumption 2 says that, after partitioning at the relevant cutoffs, each restriction depends on within an interval only through the probability assigned to that interval and its first moment. This is the feature used in the proofs to replace within an interval by a discrete approximation while preserving the restrictions. We take to be the cutoffs themselves, so the local interval bounds used later are affine in . Part (iii) ensures that the probabilities of the subintervals determined by the relevant cutoffs can be recovered from cumulative-probability equalities, possibly after adding equalities implied by the original system; in Scenario 1 these are implied by grouped shares, while in Scenario 2 the condition is vacuous. As such, these constraints do not need to be separately added into the sample or population problem, beyond the constraints we already consider in each of our scenarios. The assumption therefore covers the grouped-share, overlap, mean, ratio, and Lorenz restrictions used in Sections 3–4.

Assumption 3 is a regularity condition on the objective . Part (i) is global. For part (ii), fix , one of the two endpoints, and an optimizer of the corresponding -point problem at . On a compact neighborhood of , write nearby feasible -point measures as , with the support points remaining in their current partition cells, and define .

Assumption 3.

There exists a neighborhood of and constants such that:

(i) For all and all , .

(ii) For all sufficiently large , on every such local parameterization, is in and Hadamard directionally differentiable in tangentially to , with

Moreover, for every compact there exist and a modulus as such that, for all , the corresponding first-order expansion holds with remainder bounded by , uniformly over all such local parameterizations and all directions .

Assumption 3(i) is a -Lipschitz condition for the objective. Part (ii) requires local smoothness of the finite-dimensional -point problems around each relevant optimizer, together with a first-order expansion in that is uniform on compact sets of directions. The Appendix verifies these conditions for the objective classes used in the paper: smooth functions of finitely many moments (including the mean log deviation, the Theil index, , the Atkinson class, the Kolm class, and linear moment functionals, with positivity restrictions where needed), quantile ratios such as the ratio under local regularity at the relevant quantiles, and the Gini and Hoover indices under local regularity of and a mean bounded away from zero.

Assumption 4 is our key condition on the sampling process. We require that satisfy a functional central limit theorem as an element of , and that the equality restrictions in have right-hand sides on the empirical grid . We impose the same conditions on the bootstrap analogue , computed from the -out-of- resample described below.

Assumption 4.

There exists a tight, mean-zero Gaussian element such that

conditionally in probability in for every sequence with either or . If , then almost surely. For every equality restriction whose integrand is constant on each partition interval, almost surely and conditionally almost surely.

A convenient sufficient condition is that the data are coarsened versions of underlying i.i.d. random variables . Let denote the distribution of . In Scenario 1, . In Scenario 2, , where indicates whether observation is a point or interval observation and are the lower and upper bounds on . Let be a class of measurable functions of , define and , and suppose and for a Hadamard differentiable map . If is -Donsker, then for a tight, mean-zero Gaussian ; whenever the relevant statistics can be recomputed from resampled sampling units, the same conditions yield the bootstrap limits for . If , fixing as above implies that the -coordinate has no first-order effect, so almost surely. This setup covers empirical shares, empirical moments, empirical distribution functions, ratios of empirical averages, and empirical quantiles under the usual local positive-density condition at the relevant quantiles.

In the designs studied here, these empirical-process conditions are routine. In Scenario 1, the relevant coordinates of are built from threshold indicators and bounded moment functions such as and . In Scenario 2, they are built from point-data terms such as and , and interval-data terms such as and . Indicator classes indexed by thresholds or rectangles, and bounded products of such indicators, are standard Donsker classes. The grid conditions are also natural: in Scenario 1, and are empirical group shares and hence exact multiples of and , while in Scenario 2, .

Assumption 5 controls the error from replacing the full inequality system by the -constraint problem. The equality restrictions are eventually fixed; what may grow with is the set of included inequalities. The assumption says that, uniformly over near , any measure feasible for the -problem violates the omitted inequalities by at most .

Assumption 5.

Fix any . There exists a deterministic sequence such that, for all sufficiently large ,

Assumption 5 says that omitted inequalities are relaxed by at most uniformly. Because the inequalities included in the -problem are imposed exactly, the display concerns only omitted inequalities. If the full inequality system is finite, then all inequalities are eventually included and from some onward; this already covers both applications in Section 6. More generally, the condition holds whenever the included inequalities uniformly approximate the omitted ones.

Under Assumption 1, each endpoint problem reduces to a finite-dimensional optimization problem over the masses and support points of a -point distribution, with possibly increasing with . We now impose a regularity condition that delivers a constraint qualification for these reduced -point problems; the formal version is given in Appendix E as Assumption 7.

Assumption 6.

For each and each endpoint problem (lower or upper): (i) there is a benchmark feasible measure that is uniformly slack for the full inequality system, and on each fixed support one can reweight the same support points so that every included inequality is slack by a uniform amount; (ii) after fixing the partition cell containing each support point, the equality restrictions can be reduced locally to a nonredundant, uniformly well-conditioned subset; and (iii) the gradients of the locally binding restrictions are linearly independent.

Assumption 6 has two roles. The first part of the assumption is a uniform Slater condition, which provides a uniformly feasible benchmark measure - both for the full inequality system and on a fixed support. We use this in the approximation arguments and to obtain a strict feasible direction for the local finite-dimensional problem. The rank part of Assumption 6 is used, after fixing each support point’s partition cell, to verify a standard constraint qualification (Robinson’s condition), to bound the associated Lagrange multipliers uniformly, and to make those multipliers unique. In Scenario 2 there are no non-step equality restrictions and no step-equality restrictions beyond the simplex constraint. In our applications grouped-share restrictions pin down block masses, mean and Lorenz-type restrictions are controlled by moving a small fixed number of interior atoms, and overlap restrictions enter only through the locally binding inequalities.

Main Results

Because the assumptions are local, take neighborhoods around small enough that Assumptions 1–6 hold simultaneously, with Assumption 5 applied on the corresponding -neighborhood. Let denote the tangent set associated with . Our main result is that is Hadamard directionally differentiable.

Proposition 4.

The map is Hadamard directionally differentiable at tangentially to , with Lipschitz continuous derivative . If, for each endpoint, the corresponding -point problem at has a unique optimizer measure for all sufficiently large , then is Hadamard differentiable at tangentially to .

Proposition 4 follows by proving that an envelope theorem applies to the finite-dimensional -point problem, together with approximation results that transfer differentiability to . Proposition 5 then shows that the errors arising from the finite-support reduction, the discretization of the masses, truncation of the constraint system, and numerical optimization are all in . Consequently,

so the directional delta method yields the following result.

Proposition 5.

in .

The limiting distribution is Gaussian when is linear, but need not be otherwise. In the latter case the standard nonparametric bootstrap may fail, so we use the -out-of- bootstrap of Shao (1994). Let be the analogue of recomputed on an -out-of- resample drawn with replacement from the original sampling units. Our theory requires only that and ; if is linear, the standard nonparametric bootstrap () is also valid.

On each bootstrap sample we solve the same optimization problem as in the original sample, writing . Since conditionally almost surely for every equality restriction whose integrand is constant on each partition interval, the bootstrap problem is well defined. As in the original sample, any numerical optimization error can be absorbed into an remainder and is suppressed in notation.

Proposition 6.

Let with , and let and be defined as above. Then conditionally in probability in . If, in addition, is linear, then the same conclusion holds for the Efron bootstrap (that is, with ).

Implementation is straightforward in Scenarios 1A and 2: one resamples the sampling units and recomputes . This works because our observed data in those scenarios can be viewed as empirical averages over the sampling units. In some Scenario 1B applications, however, the auxiliary aggregates cannot be reconstructed from a nonparametric resample without additional information such as microdata, replicate estimates, or a model for the covariance structure of the reported statistics. A practical alternative is to bootstrap the weaker problem that omits those auxiliary constraints and to report the sharper point estimate separately; this yields inference for an outer identified interval rather than for the sharper endpoints. As such, critical values computed from can then be used to construct asymptotically valid simultaneous inference for the lower and upper endpoints in each of these scenarios.

6 Example Applications

This section illustrates the framework with two applications, one for each observational scenario. The first uses the English Longitudinal Study of Ageing (ELSA), where many households report point values while others provide respondent-specific intervals generated by unfolding brackets (Scenario 2). The second uses published U.S. income distribution tables from the mid-twentieth century, which report frequencies in non-overlapping income brackets and, in some years, additional aggregates such as subgroup means or selected quantiles (Scenario 1). In both applications we report conventional point estimates based on common missing-data treatments alongside our sharp identified intervals. This comparison highlights when imputation yields deceptively precise conclusions and when auxiliary linear information materially tightens identification.

6.1 Household level wealth data

Household wealth surveys routinely face item nonresponse: respondents may be unwilling to report exact amounts or may not know them precisely. To reduce missingness while limiting respondent burden, many wealth surveys use unfolding brackets: if a respondent does not provide a point value, they are routed into a short sequence of Yes/No threshold questions (e.g. “Is it more or less than ?”) that places the value in an interval. The thresholds are typically randomized to mitigate anchoring and response-order effects. Juster and Smith (1997) and Juster, Smith, and Stafford (1999) discuss the design and performance of this approach, which is now used in a range of surveys including HRS, PSID, ELSA and the Survey of Health, Ageing and Retirement in Europe.

This design naturally produces both point-and-interval data with respondent-specific intervals (Scenario 2). We use the 2018/19 wave of ELSA (see Steptoe, Breeze, Banks, and Nazroo (2013)), focusing on households whose financial respondent is aged 50–74. This yields observations. We study two measures of liquid savings: (i) a narrow single-question measure with relatively straightforward interval data structure and (ii) a broader composite measure that aggregates three components and therefore exhibits more interval complexity. For each measure we compare sharp bounds to commonly used imputation-based point estimates.

The most straightforward, and narrowest definition of liquid precautionary savings is balances in savings and checking accounts at banks or building societies (a mutual financial institution in the UK that serves a similar role as community banks or credit unions in the US). ELSA financial respondents are asked to give the value of their household’s total current balances in bank and building society accounts in a single question response, returning a value of 0 if the household does not have such accounts. Of 4,422 observations in our sample, respondents were able and willing to give point values for this variable in 3,827 (86%) of the cases and sample statistics for this point value sample are given in panel A of Table 1. Of the remaining 595 observations with individual-specific intervals, 233 had some kind of bounded interval data generated from the unfolding bracket procedure, and a further 362 had interval data generated from the unfolding brackets that was unbounded at the top. For simplicity here we have taken twice the value of the top band as the upper interval limit for all unbounded cases. Specifically, for this variable in ELSA, the final bracket point ends at £150,000, so we have set the value for an open band to be £300,000.141414Alternative choices are straightforward to implement. Overall, the 595 observations generate only 11 distinct intervals.151515These unique intervals are , , , , , , , , , , .

Summary statistics computed for the subset of households with point data

| Mean | St. dev. | 1st decile | 1st quartile | Median | 3rd quartile | 9th decile | Min | Max |

| A. Narrow definition () | ||||||||

| 29,247 | 76,813 | 100 | 1000 | 7,000 | 26,000 | 70,000 | 0 | 1,300,000 |

| B. Broad definition () | ||||||||

| 43,201 | 95,775 | 150 | 1,731 | 11,500 | 45,000 | 110,000 | 0 | 1,450,000 |

| Note: Values in £; Sample size is 4,422. Remaining observations have some form of interval data. | ||||||||

In reality, other types of financial assets are functionally equivalent to balances in bank and building society accounts, in terms of offering similar liquidity, lack of risk and comparable interest rates. In the context of the UK savings landscape, so-called National Savings products and tax-advantaged Individual Savings Accounts (that are held in the form of cash as opposed to stocks and shares) fall into this category. Thus a more comprehensive measure of liquid savings should include any such balances held by households. In cases such as these researchers need to aggregate over multiple (in this case three) interview questions, each with differing patterns of missingness, in order to arrive at a total. Analogously to the narrow definition above, a respondent may still have a point value for this variable but this now happens if and only if all three components have point values. If at least one of the variables in the set has interval values for a respondent, then this broader definition of liquid savings will take an interval value with its lower value being the sum of the lower bracket points across the three variables and the same being true for the upper value. If a component variable is reported with a point value then it is treated as both the lower and the upper bracket in this calculation.

The consequence of this aggregation of variables, each with their own pattern of missingness, leads to more instances of interval data and, importantly, considerably more complexity in the nature of the intervals. Out of the 4,422 observations in our sample, 3,708 have point values for the broader measure of liquid savings and 714 individuals have interval data. Panel B of Table 1 gives summary statistics for the subset of individuals with point data. As for the observations with the interval data for this variable, there are 199 unique interval types; the five most frequent are (157 times), (109 times), (39 times), (34 times), (34 times).

In order to put the bounds we will compute in a relevant context we begin by computing values for the Gini coefficient in this household savings data using commonly-used approaches to deal with missing data. The most simplistic of these is simply to drop the cases where point data are missing and calculate the Gini on the basis solely of the continuous part of the sample. Researchers concerned with whether the data are missing at random, however, typically want to include information from the whole sample and therefore use a variety of imputation based methods.

The most basic imputation approaches just assign either the midpoint of the relevant band, or else the mean value computed from the continuous sample lying within the band, to all observations where the continuous data is missing. These have the advantage of using the non-missing data but are somewhat inappropriate for the study of inequality since they, by definition, reduce the variance in the overall sample. Hot-deck imputation approaches, where a random donor observation from the pool of continuous observations lying within the relevant band is assigned as the imputed value for each missing observation, do not suffer from this problem. For the purposes of this exercise, we consider a single hot-deck imputation measure and a multiple hot-deck imputation measure based on ten imputations that reduces the dependency on any single draw (see Rubin (1987) for an overview).

Gini coefficients under different methodologies

| A: Narrow definition | B: Broad definition | |||

| Method | Gini | se | Gini | se |

| A. Continuous Data only | 0.7617 | 0.007396 | 0.7388 | 0.006685 |

| B. Mean imputation | 0.7358 | 0.007866 | 0.7094 | 0.007066 |

| C. Midpoint imputation | 0.7339 | 0.005792 | 0.7016 | 0.005653 |

| D. Single hot-deck | 0.7567 | 0.006718 | 0.7288 | 0.006050 |

| E. Multiple hot-deck | 0.7568 | 0.006717 | 0.7288 | 0.006050 |

| Note: Rows D and E present the mean value from 1000 repetitions. | ||||

| Bootstrap standard errors are from 1000 bootstrap draws. | ||||

The results from these exercises for both the narrow and broad definitions of liquid savings are presented Table 2. The level of inequality is high compared to that typically seen in income distributions but this is entirely to be expected, and particularly so for households at the older end of the cycle where differences in income and expenditure will have accumulated up over time. Looking across the various measures, mean and midpoint imputation methods yield a lower measure of inequality as expected, while the inequality in the continuous (non-missing) sample is higher than that measured by the hot-deck imputation methods that take into account the unfolding bracket information for the missing cases. The Gini coefficients (and their s.e.) for the broader savings definition presented in Panel B of the table are lower than for the narrow single-variable case, which is consistent with some substitutability between the three different types of assets in the class.

For each of the hot-deck imputation methods we ran the procedure 1000 times, reporting the mean values and bootstrap confidence intervals for the Gini coefficient in the table. For every hot-deck run of 1000 repetitions the distribution is more compressed in the multiple imputation case, as expected. However, the aggregated values across 1000 repetitions have similar bootstrap standard errors.

The sharp bounds on the Gini interval computed using our methodology for Scenario 2 are given in Table 3.161616As expected, the sharp upper bound on the Gini is sensitive to our treatment of the unbounded top interval. When we set the upper interval limit for entries with the open right bracket to 1,500,000 (instead of 300,000), the sharp upper bound on the Gini for the narrow definition of liquid savings changes to 0.8829. The bounds are considerably wider than either the confidence intervals on Gini coefficients calculated on the imputed data or on the range of values for the Gini covered by the 1000 draws of the hot-deck imputation samples. The bootstrap standard error for the length of the sharp Gini interval in the narrow case is 0.0039 and the confidence interval for that length constructed on the basis of the bootstrap 2.5th and 97.5th percentiles is . The bootstrap distributions of lower and upper sharp bounds for the narrow savings definition, as well as the sharp Gini interval length, are given in Figure 1.

| A: Narrow Definition | B: Broad Definition | |||

| Lower Bound | Upper Bound | Lower Bound | Upper Bound | |

| Gini | 0.7144 | 0.7918 | 0.6857 | 0.7666 |

| s.e. | 0.0077 | 0.0050 | 0.0070 | 0.0054 |

| Confidence interval: | ||||

| Confidence interval: Bootstrap | ||||

| Note: Bootstrap confidence interval constructed from 2.5th and 97.5th percentiles. | ||||

Note that while the imputation based methods in Table 2 indicate a lower Gini and smaller standard error in the broad savings case than for narrow savings measure, comparing Panel A and Panel B of Table 3 shows that the width of the bounds on the Gini for the broad definition are actually wider, reflecting the increasing missingness and more complex interval nature of the broader data — the width of the bounds is 0.0895 in comparison to 0.0774 in the narrow case.

From the computational perspective we maximize the Gini index represented as in (4.2) subject to the exhaustive list of inequality constraints in (4.1) and one equality constraint capturing the total number of interval records. In the broad savings definition case (in contrast, in the narrow definition ), so our optimization is over 961 variables and, since (in the narrow definition ), we have 57,368 inequality constraints, in contrast to 88 constraints in the previous narrow definition case.

This shows how in our generic computational approach of Section 4 the problem naturally gets more complicated as we incorporate more variables with potentially missing data. This happens through both an increase in constraints (driven by the number of unique intervals for individuals in set for aggregated variable) and an increase in the number of unknowns (driven by ) even though for the latter one could incorporate our results of Theorem 3 to reduce that dimensionality. In practice, a measure of total net financial wealth might bring together ten to fifteen subcomponents, so the missing-data structure can become quite intricate. Even so, our algorithm works in exactly the same way. This mainly means it raises computation time but does not alter the core logic of the procedure.

6.2 Income inequality in the U.S. from historical data

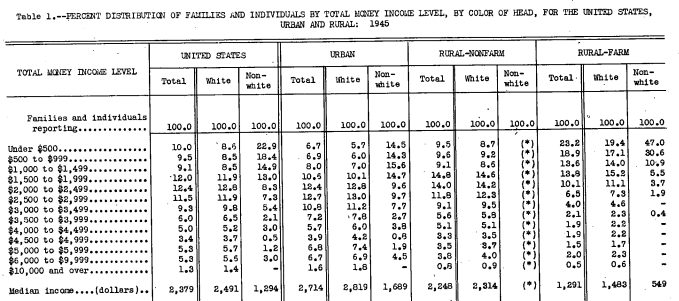

In our second example we consider a different type of interval data corresponding to the more straightforward scenarios 1A and 1B in our previous theoretical analysis. This is the scenario where data are given in non-overlapping intervals, as is often the case when information on how a distribution breaks down into summary intervals is presented in distributional tables typically presenting the number of observations falling into different ranges, perhaps with additional subgroup means or medians. For our empirical example we consider the case of historical data on US income inequality in the early to mid twentieth century and use data from the distributional tables covering various years from 1929–1971 that were produced by government agencies prior to their public release of microdata for analysis by researchers.

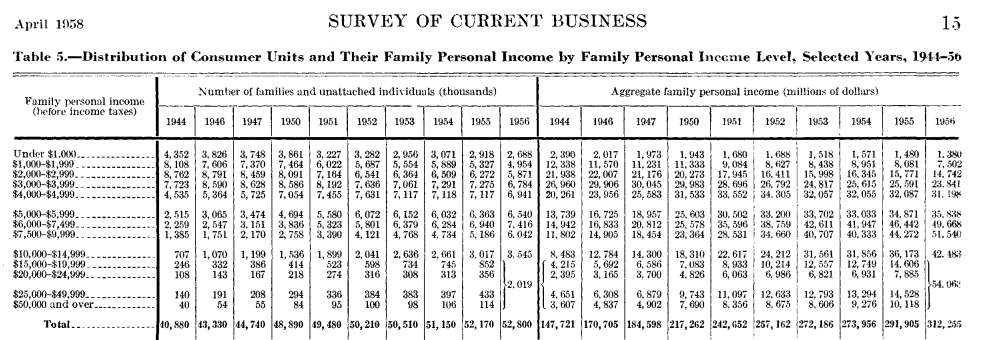

Early descriptions of the income distribution in America were developed by Selma Goldsmith from the US Department of Commerce Office of Business Economics, who produced various summary distributional tables for select years between 1929 and 1950 (see Goldsmith, Jaszi, Kaitz, and Liebenberg (1954) and Goldsmith (1958)). Subsequently, the Office of Business Economics (OBE) produced distributional tables as part of their regular outputs in many years from 1958 onwards (Office of Business Economics, U.S. Department of Commerce (1958)). Inequality statistics were not produced, and in addition the distributional tables were in different formats for different years. The 1929 income distribution was presented in 8 income categories, with additional aggregate income ratios presented for the bottom 40%, 40-60%, 60-80%, 80-95% and top 5%. Data covering select years 1935 to 1950 (in Goldsmith (1958)) used the same 8 income categories but instead presented subgroup mean incomes for the bottom 40%, 40-60%, 60-80%, 80-95% and top 5% groups. In contrast to this, data from the OBE (Office of Business Economics, U.S. Department of Commerce (1958)) presented the distribution in 13 categories along with subgroup means until 1954, then with the addition of the median, 20th, 40th, 60th, 80th and 95th quantiles for the years 1955–1962, before switching to 25 categories along with subgroup means within each category from 1964 onwards.

These data provided a wealth of information for scholars of historical inequality in the US (see, for example, Budd (1970) or Lindert (2000)) but did not provide statistics, such as the Gini, which could be combined with calculations from modern microdata to produce long run series. While some individual studies have used assumptions on the underlying distribution to allow an estimate of the Gini from subsets of the available distributional statistics, our method allows for the computation of sharp bounds on Gini coefficients or quantile ratios for the US income distribution incorporating all the information from the published statistics, regardless of the fact that the nature of the information available changes over time.

Sharp Gini bounds computed from these historical US Income data are given in Figure 2. The figure presents our calculations for two time-series of upper and lower bounds, depending on whether the source data come from Goldsmith (1958) covering years from 1929 to 1950 or the various OBE sources covering for the period from 1944 onwards. In addition, and as a comparison, we present the point estimates for the Gini over this time period that have been estimated by Lindert (2000).