Decomposition-Based Modular Conformal Prediction for Two-Stage Modeling

Abstract

Conformal prediction offers finite-sample coverage guarantees under minimal assumptions. However, existing methods treat the entire modeling process as a black box, overlooking opportunities to exploit and understand modular structure. We introduce a conformal prediction framework for two-stage sequential models, where an upstream predictor generates intermediate representations for a downstream model. By decomposing the overall prediction residual into stage-specific components, our method enables practitioners to attribute uncertainty to specific pipeline stages. We develop a risk-controlled parameter selection procedure using family-wise error rate (FWER) control to calibrate stage-wise scaling parameters, and introduce an adaptive extension for non-stationary settings. Experiments on synthetic distribution shifts, as well as real-world supply chain and stock market data, demonstrate that our approach improves coverage under structural, stage-wise shifts compared to standard conformal methods, while identifying stage-wise error contribution. This framework offers diagnostic advantages and robust coverage that standard conformal methods lack.

1 Introduction

Modern machine learning systems increasingly rely on modular pipelines, where upstream predictors generate intermediate representations for downstream models. Such pipelines appear across diverse applications: macroeconomic forecasting, where supply chain indicators inform market predictions, and medical diagnosis, where imaging features guide treatment decisions (Crane and Crotty, 1967; Soybilgen and Yazgan, 2021). In these settings, uncertainty quantification is essential and should reflect how error propagates across stages. Conformal prediction (Vovk et al., 2005) provides principled prediction intervals with finite-sample coverage guarantees under exchangeability. However, existing conformal prediction methods treat these multi-stage systems as monolithic black boxes, overlooking their modular structure and missing opportunities for targeted error attribution, i.e., identification of the major source of error. While conformal prediction has seen substantial recent development in adaptive and reweighting methods, existing methods generally treat models as single-stage or black boxes rather than taking a modular and sequential perspective (see Section 2 for a detailed review).

This perspective is especially pertinent under distribution shift, which often affects stages asymmetrically—e.g., upstream sensors may drift while downstream mappings remain stable. Standard conformal methods cannot disentangle such effects, which may force practitioners to retrain the entire pipeline when targeted interventions would suffice. To address this gap, we propose a stage-wise decomposition that isolates these effects, embedding stage-wise uncertainty into conformal prediction, yielding robust intervals under distribution shift that characterize the error produced at each stage.

By decomposing residuals into stage-wise components, our method constructs prediction intervals through a linear combination of stage-specific quantiles, weighted by scaling parameters selected via family-wise error rate (FWER) control over a calibration set. This yields valid intervals without requiring internal model access—only structural knowledge of the pipeline. Our approach offers two key advantages over existing conformal methods: (i) it provides diagnostic transparency, identifying which stages contribute most to uncertainty, and (ii) it improves coverage under structural distribution shifts affecting stage-wise components where standard approaches degrade.

For intuition, we briefly introduce the two-stage setting with triplets and latent structure , , where denote additive noise, and the model learns estimators , . For example, in automobile supply chains, could denote semiconductor prices, with estimating new vehicle demand (), and predicting used vehicle prices (). Our method decomposes the residual into upstream () error component and downstream () residual , capturing the uncertainty of each stage.

We also extend our decomposition framework to adaptive settings for which we update scaling parameters based on component-wise empirical coverage, improving responsiveness to (i) upstream, (ii) downstream, and (iii) end-to-end distribution shifts. We illustrate our method on synthetic shifts and real-world supply chain and financial data, demonstrating the ability to explicitly adapt to stage-wise shifts, and showing improved robustness over adaptive conformal baselines (Gibbs and Candès, 2021, 2024; Angelopoulos et al., 2023, 2024b). For simplicity, we focus on two-stage models, but our methodology can be extended to multi-stage models (Appendix C).

Contributions:

-

•

We propose a residual decomposition framework for sequential multi-stage models that partitions prediction error into distinct upstream and downstream components, enabling stage-wise uncertainty attribution (Section 4).

-

•

We develop a risk-controlled parameter selection procedure using FWER-based hypothesis testing to construct valid prediction intervals from decomposed residuals with coverage guarantees (Section 6).

-

•

We introduce an adaptive extension that dynamically adjusts scaling parameters based on component-wise coverage feedback, preserving long-run coverage guarantees while providing stage-sensitive diagnostics for distribution shifts (Section 7).

-

•

We demonstrate the framework’s effectiveness on synthetic shifts and real-world economic forecasting, showing improved coverage over cutting-edge conformal methods that degrade under structural shifts, with diagnostic capabilities that enable targeted model interventions (Section 8).

Paper Outline. In Sections 3 and 4, we formalize the two-stage prediction setting and introduce our residual decomposition. Section 5 describes our method for constructing stage-aware prediction intervals, followed by the FWER calibration procedure in Section 6. We extend our method to an adaptive version in Section 7, and evaluate empirical performance under distribution shifts in Section 8.

2 Related Work

Conformal Prediction.

Conformal prediction (Vovk et al., 2005) constructs prediction sets with finite-sample marginal coverage under exchangeability, with popular split/inductive variants (Papadopoulos et al., 2002) that calibrate on a held-out set; see Angelopoulos and Bates (2023) for a survey. A complementary line of work generalizes conformal prediction beyond coverage: risk-control (Bates et al., 2021) and learn-then-test (Angelopoulos et al., 2025) produce sets which certify user-chosen losses with high probability, with the latter doing so via multiple hypothesis testing over a parameter family. We build on this framework in Section 6.

Extensions of Conformal Prediction.

Recent work expands the flexibility of conformal prediction through reweighting and adaptive calibration (Barber et al., 2023; Angelopoulos et al., 2023; Oliveira et al., 2024; Farinhas et al., 2024; Angelopoulos et al., 2024b; Gibbs and Candès, 2021, 2024), model-aware adaptations (Zargarbashi et al., 2023; Zhang et al., 2025; Wu et al., 2025). These methods consider single-stage/black-box models, rather than considering how uncertainty propagates between stages.

Stage-wise Uncertainty Propagation in Pipelines.

Stage-wise uncertainty propagation has been studied in medical imaging pipelines (Mehta et al., 2021; Feiner et al., 2023; Ozdemir et al., 2017) via Monte Carlo sampling over internal model components, whereas our approach is black-box and targets valid prediction intervals. Most closely related, Gong et al. (2023) apply a stage-wise decomposition to model error, but use a conservative upper-bound that provides neither stage-wise attribution nor an adaptive extension. Our framework uses FWER-controlled selection over scaling parameters and an adaptive update rule responsive to stage-specific shifts; we make a comparison to this method in Appendix D.3.2.

3 Problem Setting

We consider a sequential two-stage prediction problem: each data point is characterized by a triplet where is the input to the first-stage model (upstream features), is an intermediate representation, and is the final prediction target. We learn predictors and which are composed to form end-to-end predictor , where .

To fit these models and perform conformal prediction, we assume access to three disjoint subsets: (i) a training set used to fit both stages of the model via and pairs for each stage respectively; (ii) a conformal set for computing nonconformity scores; and (iii) a calibration set for parameter selection. At prediction time, only the upstream input is observed, while the intermediate value and target are unobserved and must be predicted.

We list some assumptions that we consider at different points throughout the paper. (i) Exchangeability. Unless stated otherwise, for theoretical guarantees, we assume the data in to be exchangeable, as well as the test point . However, we make an extension to -mixing (Appendix C.2) and experimentally validate performance on non-exchangeable data. (ii) Learning algorithms. We assume that the algorithms that learn are deterministic, i.e., given the same training data, they produce identical predictors; and we also assume they are symmetric, i.e., invariant to permutations of the data. We also assume that the intermediate variable is observable for the given datasets. We clarify that is observable at the pipeline-level, not an internal component: it is the upstream output read by the downstream model, naturally recorded at the stage interface.

Objective.

Given test upstream input , the goal is to construct prediction interval such that , where is the target miscoverage level. Under exchangeability, this is the standard conformal prediction objective. However, under distribution shifts, we seek to maintain robust coverage near the nominal level, while identifying the impact of specific pipeline stages on prediction uncertainty.

The key goals in this setting are: (i) Attribution: Understanding which stage contributes more to prediction uncertainty; (ii) Adaptivity: Improving coverage under shifts affecting different stages; (iii) Transparency: Providing actionable insights for model improvement or retraining decisions. Our approach addresses these challenges by decomposing the end-to-end prediction error into stage-specific components for targeted uncertainty quantification and robust interval construction. While we define these concepts for two-stage models, we discuss extensions to auxiliary inputs, multiple upstream models, and deeper sequential pipelines in Appendix C. We also provide a notation table in Appendix B.2.

4 Two-stage Residual Decomposition for Conformal Prediction

To address the aforementioned challenge of attribution, we partition the total prediction residual into upstream and downstream components. This decomposition enables stage-wise attribution of error, in contrast to standard black-box conformal methods. We provide a visualization in Figure 1.

Definition 4.1 (Second-stage residual).

Given a point and downstream predictor , the second-stage residual is

This captures downstream prediction error given the true intermediate input .

Definition 4.2 (First-stage delta).

Let be the output of the first-stage predictor. The first-stage delta is defined as

This quantifies the change in downstream prediction error induced by replacing the true intermediate with its prediction .

For notational purposes, we drop the dependence on , and refer to these terms as , and . Intuitively, reflects the error of the upstream predictor, while isolates downstream error without upstream influence. This decomposition satisfies a fundamental upper-bound property.

Proposition 4.3.

For any point , the total residual satisfies:

By definition, . Let and . By the triangle inequality, . This upper bound property ensures that the sum of components provides a conservative estimate of the total error, which is crucial for the coverage guarantees developed subsequently.

This decomposition provides a clean interpretation: measures the inherent uncertainty of the downstream model, while measures how upstream prediction errors affect the final prediction error magnitude. When is small relative to , the upstream predictor performs well and downstream uncertainty dominates. Conversely, when is large relative to , upstream errors drive prediction uncertainty. Furthermore, these components exhibit intuitive relationships with the full residual: when is small, closely approximates , while when the upstream model is accurate and is smooth, closely approximates (see Appendix A.2). Importantly, at least one component must represent a majority of the error, ensuring meaningful stage-wise attribution.

This attribution enables practitioners to identify which stage requires improvement and guide retraining decisions. Furthermore, these components provide insights for handling distribution shifts: under upstream shifts, typically increases as the first-stage predictor encounters out-of-distribution inputs, while under downstream shifts, increases. These changes can be experimentally visualized in Appendix Figure 17(b). Thus, the varied responses enable targeted adaptive strategies for different distribution shifts. Next, we describe two complementary approaches to combining these residual components into prediction intervals.

5 Constructing Prediction Intervals

We describe two approaches that incorporate , utilizing the conformal set , to compute component-wise quantiles, with data-driven parameter selection using addressed in Section 6. Note that there exists a rich space of heuristics for combining these residual components beyond those listed below—see Appendix C.1. For proofs of the following results, see Appendix A.1.

5.1 Separate Component Quantiles

For the first approach, we compute sets of residual components on : and , which we abbreviate as and . Prediction intervals are constructed by summing quantiles computed separately from each set, with the quantile levels controlled by and for the respective stages.

Definition 5.1 (Separate component quantiles).

Let be quantile levels. For test input , the prediction interval is constructed by summing separate quantiles of each component at levels:

This construction inherits coverage guarantees from standard conformal prediction:

Theorem 5.2 (Coverage of separate component quantiles).

Under the assumption of exchangeability, for , the prediction interval satisfies

5.2 Scaled Component Quantiles

Our second approach fixes a quantile level for both components and selects scaling parameters to weight their respective contributions. This provides an intuitive explanation of stage-wise attribution of uncertainty.

Definition 5.3 (Scaled component quantiles).

For a fixed quantile and scaling coefficients , the prediction interval is

where the quantiles are computed over .

The choice of scaling parameters and provides clear control: setting ignores upstream uncertainty while setting ignores downstream uncertainty, focusing only on upstream effects. However, coverage guarantees for arbitrary choices of require careful analysis. For fixed weights, we have the following:

Corollary 5.4 (Coverage with ).

Under exchangeability, for and , the interval satisfies

Proof.

This follows directly from Theorem 5.2 with . ∎

For appropriately chosen quantiles and scaling weights, we observe that both methods can yield similar intervals. To provide maximum flexibility for both theoretical analysis and implementation, we can combine both approaches into a general framework:

This unified form allows independent control of both quantile levels and scaling parameters, enabling fine-tuned balance between coverage guarantees and stage-wise attribution of error. We provide guidance on default parameter choices in Appendix D.2 and discuss the selection process of in the following sections.

5.3 Coverage for Scaled Parameters

While coverage for intervals of the form (Definition 5.1) follows from standard conformal analysis, establishing similar guarantees for intervals with scaled residuals (Definition 5.3) with arbitrary weights presents significant challenges. The scaling parameters have no direct mapping to quantile levels, making it difficult to derive explicit guarantees. Despite this, we can establish that valid scaling parameters exist: Under mild regularity conditions, there always exist optimal scaling parameters that yield exact marginal coverage.

Proposition 5.5 (Existence of ideal scaling parameters).

For desired coverage level , such that the interval with those scaling parameters satisfies the marginal coverage guarantee

provided the distribution of the residual has no point masses.

Thus for some desired coverage level , for residual component pieces taken at quantile level , there exist (possibly many) scaling weights that provide exact coverage. However, finding optimal scaling parameters requires knowledge of the residual distribution, which is unavailable in practice. This creates a fundamental trade-off: scaled intervals offer direct control of stage-wise error contribution but lack accessible guarantees, while separate quantile intervals provide coverage under minimal assumptions but offer less direct explanation of stage-wise error.

To resolve this trade-off, we adopt a conservative risk-controlled approach (Bates et al., 2021; Angelopoulos et al., 2024a, 2025) that selects parameters with demonstrable coverage over recent points, using , providing both theoretical guarantees as well as empirical robustness to the distribution shifts that motivate our framework. Section 6 formalizes this through a risk-controlled calibration procedure, and Section 7 extends it to adaptive parameter updates that respond to component-wise coverage feedback.

6 Risk-Controlling Approach with Residual Components

Since finding an exact is impossible in practice, we reframe the problem as filtering for coefficient pairs that satisfy the nominal coverage level . We select scaling parameters through multiple hypothesis testing with FWER control. For each , we test whether the miscoverage rate exceeds ; FWER ensures we rarely accept poor parameters. This conservative approach provides three benefits: (i) robustness buffer under moderate shift, (ii) diagnostic abstention to signal when retraining is needed, and (iii) flexible search over stage-wise attribution of error.

6.1 Testing Miscoverage via Empirical Risk

We aim to identify scaling parameters for which the resulting prediction interval achieves coverage at least . Since theoretical guarantees for arbitrary are unavailable, we perform a hypothesis test for whether its miscoverage rate exceeds . We fix a finite candidate set of scaling pairs and define the corresponding prediction interval for each :

which we denote as , using the general framework introduced earlier that combines Definition 5.3 and Definition 5.1. Here, the quantile parameters and are fixed in advance with quantiles taken over , while the miscoverage testing is performed using to identify suitable .

6.2 Computing -values from Calibration Data

Let denote the size of the calibration set. For each choice of scaling parameters , we define the empirical miscoverage rate . Under the stronger assumption that the calibration points are IID, and that the true miscoverage rate for a given is constant, the number of missed points follows a Binomial distribution with parameters and the underlying miscoverage probability. For each , define the null hypothesis

Thus, for each we define a -value . The -values are super-uniform under (Appendix A.5); that is, for any , we have , which is crucial for FWER-controlling guarantees (Bates et al., 2021). Thus, we apply FWER-controlling multiple testing algorithms (Appendix B.4) to the collection of to obtain the set of valid scaling parameters . This ensures that, with probability at least for some , no with a miscoverage rate exceeding is accepted. Note that the are more conservative as they require evidence of coverage of at least . In contrast, other prediction interval methods yield coverage that is merely close to . This conservatism may result in unnecessarily wide intervals, particularly when coverage is less critical than efficiency, such as in IID settings. To remedy this, we can include tolerance parameter and calculate with , trading some guarantees for practical performance. As demonstrated in our experiments (Figure 2), even small values of significantly improve efficiency while improving empirical coverage under non-IID settings.

6.3 Coverage Guarantees via Risk-Controlled Scaling

Thus, given the -values and a FWER-controlling multiple testing algorithm (Appendix B.4), we identify the set of validated scaling parameters . The following result states any intervals associated with achieve coverage with high probability:

Theorem 6.1 (Risk control via FWER calibration).

Let be the set selected by a FWER-controlling algorithm at level , based on -values computed over the IID calibration set with tolerance . Then, for any , we have

where the outer probability is over the randomness of , and the inner probability is over the test point .

This guarantee follows from the FWER-controlling property: by reducing the probability of false positives, i.e., selecting scaling parameters with poor coverage, we ensure that all selected parameters satisfy the coverage requirement with high probability. Thus, with probability at least over , any selected interval has coverage rate at least . Note that while does not explicitly appear in the guarantee, larger calibration sets lead to more precise -value estimates, typically resulting in a larger and less conservative interval selection. In practice, any pair can be used to construct prediction intervals. Although the quantile levels from Definition 5.1 could also be tuned jointly with , we fix for simplicity, which is typically sufficient in our experiments.

We note that can be empty, producing no interval. This is intentional, as it can indicate that the shift is too large and retraining is needed, rather than producing an unreliable interval. In this setting, fixed offer a clear interpretation as stage-wise sensitivity to shifts. While the coverage guarantees assume IID , the selective FWER process creates a robustness buffer, which we extend to targeted adaptation of the selected weights when distribution shifts affect pipeline stages asymmetrically, which we define in Section 7 and demonstrate experimentally in Section 8. Lastly, Appendix C.2 shows how the IID assumption on can be relaxed to allow stationary -mixing sequences as an initial extension of the theoretical coverage guarantees to the non-exchangeable/non-IID settings considered in Section 8.

7 Adaptive Risk Control with Residual Decomposition

We consider an adaptive variant of our method for nonstationary data by updating the prediction intervals over time. The sets and are defined using a sliding window over the most recent observations, with a user-specified window-length . We construct intervals combining Definition 5.3 and Definition 5.1:

parameterized by scaling coefficients , quantile levels , and target coverage level , where quantiles are taken over , and is recalculated at each time step. With each new point, we dynamically update the using adaptive rules based on recent performance: when coverage drops below target, we decrease and vice versa using stepsize ; when specific components show persistent errors, we adjust their corresponding scaling parameters; and when is too restrictive, we adjust the quantile levels with stepsize to expand future options. The algorithmic details are provided in Appendix B.5.

Crucially, the selection algorithm (SelectLambda) implements the adaptive adjustments to : it first identifies which residual component constitutes more of the error by comparing recent averages and over the sliding window. If coverage fails and upstream errors dominate (), it seeks to increase within the validated set . Conversely, when downstream errors dominate (), it prioritizes . If the desired scaling adjustment is unavailable in , the algorithm returns signals to adjust , effectively “adjusting” the constraints to allow more suitable scaling options.

Even with additional parameters, this approach preserves the long-run coverage guarantee from prior work: , where denotes coverage at time . This is because the core update rule remains identical to the adaptive conformal method of Gibbs and Candès (2021), resulting in the convergence guarantee formally stated in Appendix A.1.1.

8 Experiments

We evaluate our method on synthetic and real-world forecasting tasks to assess its ability to (i) preserve coverage, (ii) attribute predictive error to specific model stages, and (iii) adapt to distribution shifts in modular pipelines. We validate the shift robustness mechanisms outlined previously: conservative calibration via FWER provides a safety margin, while stage-wise parameters adapt to distribution shifts that affect upstream and downstream components differently. Our experiments are designed to isolate upstream, downstream, and full-pipeline shifts, highlighting how stage-aware intervals improve transparency and robustness over existing conformal baselines. Additional experiments and details are in Appendix D where we provide hyperparameter ablation studies, practical guidelines for hyperparameter selection, experiments on covariate shift, a real-world stocks dataset, single-stage baseline comparisons, and visualizations of how the chosen weights adapt to distribution shifts.

Code for reproducing our experiments is available at: https://github.com/william-zhang64/Split-Residual-Conformal-Prediction.

8.1 Non-Adaptive Method Experiments

We evaluate our non-adaptive method (Section 5), using the FWER-based procedure for our unified interval which we denote as to generate a validated set of , using fixed quantile levels . We then select the pair from this set that yields coverage closest to the nominal level on . We compare against two main non-adaptive methods: standard split conformal prediction (SC, Vovk et al. (2005)) which has been recently noted to maintain coverage under certain non-exchangeable settings (Oliveira et al. (2024)) and weighted split conformal prediction (WSC, Barber et al. (2023)), which explicitly accounts for non-exchangeability via weighting. Lastly, the cascaded confidence method (CC, Gong et al. (2023)) consistently over-covers across our settings; we report the comparison in Appendix D.3.2.

We begin with a synthetic dataset generated by the structural equations , , where . After an initial stationary period, the data undergoes rapid or gradual distribution shifts in either the upstream or downstream via increasing variance in the corresponding noise terms.

We visualize mean width and coverage across for each method, including our method with and without tolerance . We show results under IID settings, gradual downstream shift, and rapid downstream shift in Figure 2. Point opacity encodes , color denotes the method, and error bars indicate standard deviations in coverage and width.

In the IID setting, setting (blue) increases efficiency greatly over (orange), is comparable to WSC and SC and outperforms WSC at low . Under gradual and rapid distribution shifts, displays strong relative improvements in coverage to WSC and SC, particularly at higher , while remaining less conservative than . Notably, our method with is well calibrated under rapid shifts, but produces overly wide intervals under other settings, making a balanced middle ground. This illustrates how the parameter allows for fine-grained interpolation between efficiency and conservativeness. Thus, our framework gives practitioners explicit knobs to navigate the tradeoff between robustness, interval width via , and also abstention sensitivity via and , and we provide a parameter flowchart in Appendix D.2.

Corresponding figures for upstream distribution shift are in Appendix D.3.3, where similar conclusions hold, but with greater drops in coverage for all methods. A table of additional results for upstream, downstream, gradual, and rapid shifts are reported in Appendix D.3.1, particularly with varying parameters. An important intuition is that parameters act as stage-wise abstention sensitivity, with higher (resp. ) causing the model to abstain more under upstream (resp. downstream) shifts, allowing the method to detect rapid shifts and abstain rather than provide a faulty interval.

8.2 Adaptive Methods Experiments

We evaluate our adaptive method (Section 7) in settings with drastic distribution shifts, comparing against recent adaptive baselines: adaptive conformal inference (ACI, Gibbs and Candès (2021)), conformal PID control (PID, Angelopoulos et al. (2023)), online conformal with decaying step sizes (OCID, Angelopoulos et al. (2024b)). We also consider error quantified conformal inference (ECI, Wu et al. (2025)), and dynamically tuned adaptive conformal inference (DtACI, Gibbs and Candès (2024)), an extension of ACI, and report their results in Appendix D.4.2 due to weaker performance. We also consider covariate shifts, hyperparameter ablation, and a real-world stock price dataset, with full experimental details in Appendix D.

Controlled two-stage regression with structured shifts.

We simulate a two-stage regression pipeline, with controlled stochastic relationships between upstream input , intermediate representation , and downstream output . The initial data follows an i.i.d. structure with where . Both stages are modeled using ordinary least squares. At test time, we simulate a temporal sequence of three phases: (i) Upstream distribution shift: becomes ; (ii) Reversion: The upstream returns to ; (iii) Downstream distribution shift: becomes . We report coverage and widths in Figure 3, capturing the robustness of our methods to stage-specific distribution shifts without overcompensating on width, particularly for upstream shifts.

Automobile indicators dataset.

We evaluate our method on a real-world dataset consisting of monthly economic indicators for the U.S. automobile supply chain and used vehicle valuations. Upstream features are sourced from FRED (2025), including metrics such as price indices, inventory levels, and manufacturing prices, which are then forecasted at a 6-month horizon. Downstream outputs , aggregated used car prices, are obtained from Manheim (2025). This setting fits the two-stage modeling framework: upstream economic conditions influence downstream pricing, and training a separate upstream predictor leverages more widely available historical supply chain data.

A notable feature of this dataset is the sharp distribution shift in 2020 due to the COVID-19 pandemic, which disrupted global supply chains, leading to production halts, resulting in a steep and persistent rise in used vehicle prices (Mullin, 2022). The nature of the distribution shift may also affect the model asymmetrically, leading to exacerbated upstream inaccuracy, which we observe via the scaling parameter changes in Appendix D.4.5. For the upstream forecasting task, we use an ensemble of VAR and ARIMA models to predict supply-chain indicators. The model is trained on a rolling-window basis, with residual scores computed at each time step. A 40-month sliding window forms the held-out set from which we derive and .

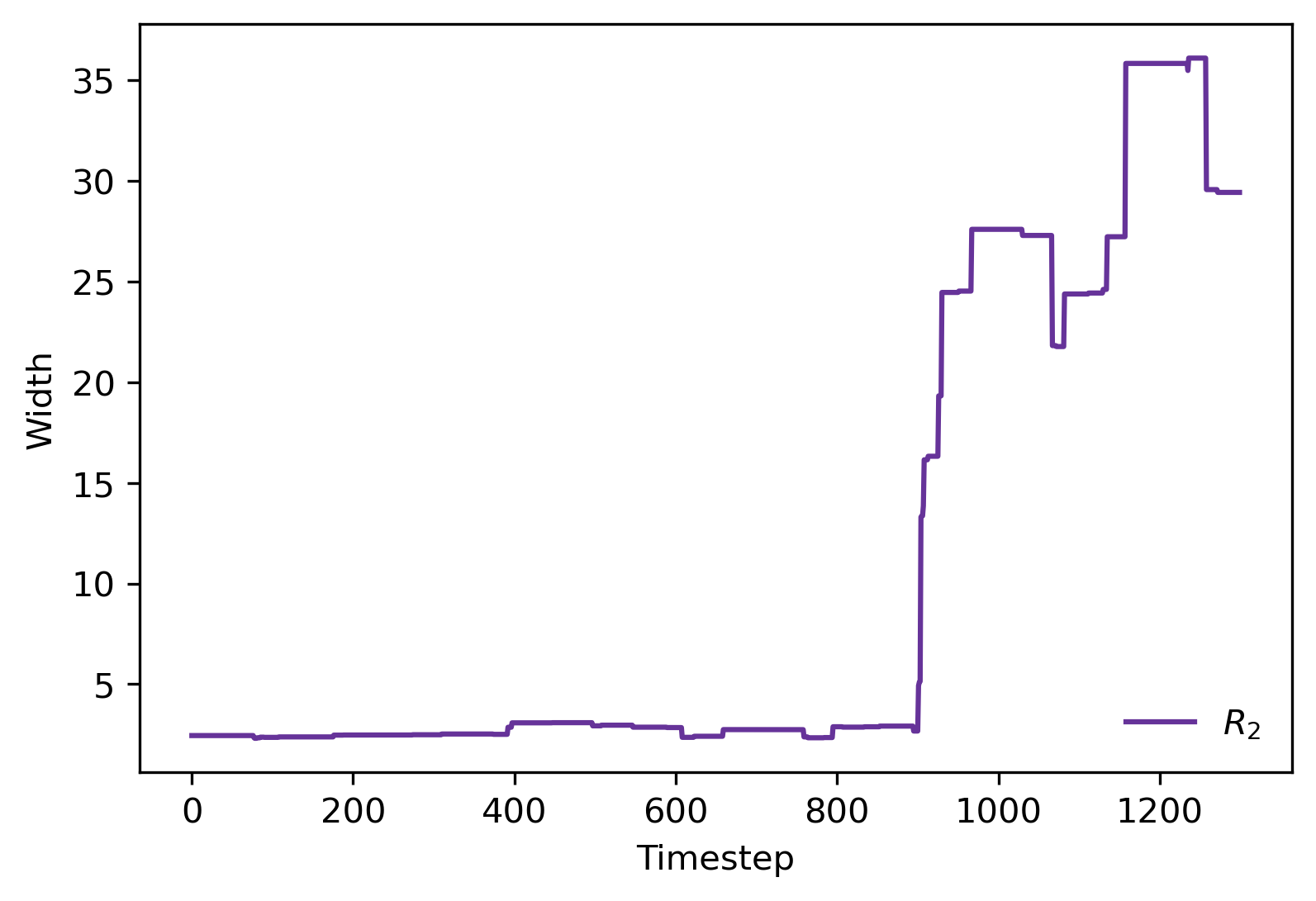

We present the resulting prediction intervals for our method, ACI, PID, and OCID in Figure 4. Our method effectively responds to the distribution shift in 2020, maintaining coverage relative to other methods. Notably, our approach maintains a comparable mean width (18.957 vs 15.696 (ACI), 18.469 (PID), 15.667 (OCID)). This demonstrates our method can quickly adjust to distribution shifts by considering more conservative values of in , while remaining efficient during the stationary period (2014-2020). This suggests that our method is well-suited for real-world forecasting and shines under asymmetric (stage-wise), structural distribution shifts. Contrast with OCID, which only partially covers the shift in 2020 due to the high variance fluctuations in width, even during the stationary period. For covariate shifts (Appendix D.4.7) that affect the entire pipeline, the benefits of our method are less significant and all methods perform similarly in width and coverage.

9 Conclusion

We proposed a conformal prediction framework for sequential models that decomposes prediction residuals into distinct stage-specific components. Our method combines this decomposition with risk-controlled parameter selection to construct prediction intervals that provide coverage guarantees and uncertainty attribution. The approach allows practitioners to identify which pipeline stage contributes to prediction uncertainty and provides diagnostic tools for targeted model improvement. Empirical evaluation on synthetic distribution shifts and real-world economic forecasting shows that our method’s coverage degrades less severely under shifts compared to standard conformal approaches. While this robustness comes at the cost of wider intervals and occasional abstention when shifts are severe, these trade-offs reflect the method’s conservative design that prioritizes reliable coverage and attribution of error over optimistic predictions. The stage-wise decomposition proves particularly valuable for asymmetric shifts affecting different pipeline components, enabling targeted adaptive responses that standard methods cannot provide. Lastly, we note that the concept of stage-wise residual decomposition and reweighting can be extended to incorporate other conformal methods for potential further improvements.

Impact Statement

This paper presents work whose goal is to advance the field of Machine Learning. There are many potential societal consequences of our work, none of which we feel must be specifically highlighted here.

References

- Conformal risk control. In International conference on learning representations, Vol. 2024, pp. 55198–55218. Cited by: §5.3.

- Conformal pid control for time series prediction. Advances in neural information processing systems 36, pp. 23047–23074. Cited by: 6th item, §1, §2, §8.2.

- Learn then test: calibrating predictive algorithms to achieve risk control. The Annals of Applied Statistics 19 (2), pp. 1641–1662. Cited by: §A.1, Theorem A.6, §C.2, §2, §5.3.

- Conformal prediction: a gentle introduction. Foundations and Trends in Machine Learning 16 (4), pp. 494–591. Cited by: §2.

- Online conformal prediction with decaying step sizes. In International Conference on Machine Learning, pp. 1616–1630. Cited by: 7th item, §1, §2, §8.2.

- A note on strong mixing of arma processes. Statistics & probability letters 4 (4), pp. 187–190. Cited by: §D.3.4.

- Conformal prediction beyond exchangeability. The Annals of Statistics 51 (2), pp. 816–845. Cited by: §A.3, §A.3, §A.3, §A.3, §2, §8.1.

- Hoeffding and bernstein inequalities for weighted sums of exchangeable random variables. Electronic Communications in Probability 29, pp. 1–13. Cited by: §C.2.

- Distribution-free, risk-controlling prediction sets. Journal of the ACM (JACM) 68 (6), pp. 1–34. Cited by: §2, §5.3, §6.2.

- Multiple testing in clinical trials. Statistics in medicine 10 (6), pp. 871–890. Cited by: §B.4.

- A two-stage forecasting model: exponential smoothing and multiple regression. Management Science 13 (8), pp. B–501. Cited by: §1.

- Non-exchangeable conformal risk control. In International Conference on Learning Representations, Vol. 2024, pp. 50952–50966. Cited by: §2.

- Propagation and attribution of uncertainty in medical imaging pipelines. In International workshop on uncertainty for safe utilization of machine learning in medical imaging, pp. 1–11. Cited by: §2.

- Automobile indicators. Note: data retrieved from FRED, https://fred.stlouisfed.org/series/CUSR0000SETA02 Cited by: §8.2.

- Conformal inference for online prediction with arbitrary distribution shifts. Journal of Machine Learning Research 25 (162), pp. 1–36. Cited by: §1, §2, §8.2.

- Adaptive conformal inference under distribution shift. Advances in Neural Information Processing Systems 34, pp. 1660–1672. Cited by: §A.1.1, §A.1.1, §A.1.1, §1, §2, §7, §8.2.

- Confidence calibration for systems with cascaded predictive modules. arXiv preprint arXiv:2309.12510. Cited by: §D.3.2, §2, §8.1.

- Concentration inequalities for dependent random variables via the martingale method. Annals of Probability. Cited by: §C.2.

- Used vehicle value index. Note: data retrieved from Cox Automative, https://site.manheim.com/en/services/consulting/used-vehicle-value-index.html Cited by: §8.2.

- Propagating uncertainty across cascaded medical imaging tasks for improved deep learning inference. IEEE Transactions on Medical Imaging 41 (2), pp. 360–373. Cited by: §2.

- Stability bounds for stationary -mixing and -mixing processes.. Journal of Machine Learning Research 11 (2). Cited by: §C.2.

- Supply chain disruptions, inflation, and the fed. Econ Focus (3Q). Cited by: §8.2.

- Split conformal prediction and non-exchangeable data. Journal of Machine Learning Research 25 (225), pp. 1–38. Cited by: §2, §8.1.

- Propagating uncertainty in multi-stage bayesian convolutional neural networks with application to pulmonary nodule detection. arXiv preprint arXiv:1712.00497. Cited by: §2.

- Inductive confidence machines for regression. In European conference on machine learning, pp. 345–356. Cited by: §2.

- Conformal language modeling. In International Conference on Learning Representations, Vol. 2024, pp. 11654–11681. Cited by: Lemma A.5.

- Probability inequalities for the sum in sampling without replacement. The Annals of Statistics, pp. 39–48. Cited by: §C.2.

- Nowcasting us gdp using tree-based ensemble models and dynamic factors. Computational Economics 57 (1), pp. 387–417. Cited by: §1.

- Algorithmic learning in a random world. Vol. 29, Springer. Cited by: §1, §2, §8.1.

- Error-quantified conformal inference for time series. In International Conference on Learning Representations, Vol. 2025, pp. 81566–81593. Cited by: §2, §8.2.

- Conformal prediction sets for graph neural networks. In International Conference on Machine Learning, pp. 12292–12318. Cited by: §2.

- Conformal structured prediction. In ICLR 2025 Workshop on Building Trust in Language Models and Applications, External Links: Link Cited by: §2.

Appendix A Appendix

A.1 Main Results/Proofs

Proof of Theorem 5.2

Proof.

We consider the event

where is the prediction interval defined by with the quantiles being taken over the residual components calculated on held-out conformal set . This event is when the coverage of the interval fails. See that

But then by definition

Thus, the split residual on the point also falls outside the region. However, this implies that at least one of the following events occur:

or

Then each of these pieces holds due to exchangeable properties as the probability of the new residual piece being higher in rank than the quantile (resp. ) is (resp. ). For , the exchangeability is clear as it is directly the prediction interval for on data . For the latter, it is still clearly exchangeable as well: the functions are symmetric and deterministic and are pretrained, thus being fixed on the held-out set. Thus can be interpreted as the result of some deterministic function on each point , which implies that

where denotes the first residual component of the -th point of . Then we have exchangeability of , thus the probability of each of the noncontainment events for each residual component are bounded by and respectively.

Therefore

In fact, as can be seen in the above equation, the stated result is looser than necessary. ∎

Proof of Proposition 5.5

Proof.

Since the traditional residual is assumed to be continuous, the function that maps the scaling parameters to the marginal coverage probability of the interval is itself continuous. When , the interval degenerates to a single point and thus has zero coverage (assuming the problem is nontrivial). When , the interval is wide enough to ensure coverage of at least by Corollary 5.4. By the intermediate value theorem, there must exist a pair such that the interval achieves exactly coverage. ∎

As an aside, one can further view the problem as an optimization problem

which by KKT conditions implies that any must satisfy

which provides that at any optimal solution there must be the same balance between the magnitude of components and the impact (derivative) of the scaling parameter on true coverage probability for each parameter. Thus large magnitude implies large impact, confirming intuitive understanding.

Proof of Theorem 6.1

Proof.

By Lemma A.5, the -values are super-uniform under the null hypothesis. Then we may apply Theorem 1 of Angelopoulos et al. (2025) (Theorem A.6), given a FWER algorithm with parameter to obtain the result. We note that the size of does not explicitly appear in the bound, however, it directly affects the -values which can be seen via Hoeffding’s inequality:

where is the empirical error rate on ∎

A.1.1 Long-Run Coverage

Proposition A.1 (Long-Run Coverage of Adaptive Method).

Let be the step size, the nominal coverage level, and let denote the coverage indicator at time . Then the adaptive algorithm satisfies:

This result ensures that in the long run, the algorithm achieves the desired coverage level , without requiring distributional assumptions on the data.

The additional parameters are updated as deterministic functions of the algorithm’s history, ensuring they do not interfere with the update steps that underlie the coverage guarantee.

Proof of Proposition A.1

Please refer to Algorithm 1 for notation. We first show a preliminary lemma.

Lemma A.2 (Boundedness of and ).

Let be a constant. Then, for all , the sequences and are bounded within the interval . That is,

Proof.

To establish the lower bound for , observe that the argument for follows similarly, and the upper-bound can be treated identically.

Suppose that for some time step . In this case, by the definition of the residual component , we have:

where denotes the coverage of the model at time . Additionally, since by the construction of the residual, this implies that in the output of the algorithm SelectLambda, the update step , meaning that:

Thus, if were negative at some time step, the next value is non-decreasing. Consequently, the sequence cannot decrease below . Therefore, the minimum value attainable by is .

A similar argument holds for the upper-bound.

Hence, we conclude that:

This holds similarly for . ∎

Next, we show the long-run coverage result, Section A.1.1 via the same arguments as Proposition 4.1 of Gibbs and Candès (2021).

Proof.

Although our algorithm includes additional parameters , the update rule for remains unchanged from Gibbs and Candès (2021):

where is the coverage indicator at time and is the target coverage level.

As in Gibbs and Candès (2021), we show that with probability 1. For the lower bound (the upper-bound follows symmetrically), suppose at some time . Then the candidate set , so , and the update becomes:

Hence, is pushed upward, preventing it from decreasing without bound. Therefore, for all .

Next, unfolding the recursion gives:

Rearranging terms and using the bound, we obtain:

Equivalently:

which converges to zero as , yielding the desired result. ∎

A.2 Auxiliary Results

Proposition A.3.

For a given point , if for some small i.e., is close to the true value , then

Proof.

This follows immediately by definition of .

∎

Next, we show the equivalent for under additional assumptions

Proposition A.4.

For a given point , for small under certain assumptions, such as if is a Lipschitz continuous function for some parameter , and the first stage has small prediction error, . Then

Proof.

∎

The main takeaway of these two results is that they confirm the intuition for when and are roughly similar to , particularly when one model is accurate (and in the case of when the learned function is smooth). This also implies that both being small is impossible, thus one must represent a majority of the error. Note that and can also serve as rough lower bounds on , though each can individually exceed under adversarial noise or model miscalibration.

Theorem A.6 (Theorem 1 of Angelopoulos et al. (2025)).

Suppose has a distribution stochastically dominating the uniform distribution. Let be a FWER controlling algorithm at level . Let be the expected risk for the choice of and be the maximal error rate. Then satisfies the following

A.3 Extensions of Theorem 1

We can also state Theorem 5.2 for the setting with auxiliary data (Section C.3).

Corollary A.7.

For and new point , and interval defined as in Section C.3 to include auxiliary data, we have

which follows by the same proof as above; auxiliary data does not change the proof (assuming that with auxiliary features, the data is still exchangeable). Lastly, we note that the prior results can easily be adapted to nonexchangable data settings using weighted quantiles and a weighting scheme as mentioned in Barber et al. (2023). Thus we have

Corollary A.8.

Let and be weights for each point. For and new point , and interval defined as in Definition 5.1, we have

where and are coverage penalties from nonexchangability.

Proof.

The result follows analogously to the proof of Section A.1, with modifications to account for the use of weighted quantiles and associated penalty terms. Specifically, we let and denote penalties applied to the empirical weighted quantiles, as introduced in Theorem 2 of Barber et al. (2023). These penalties are of the form where , represents the vector of full residuals and is the same vector with the -th point swapped with .

When applying weighted conformal prediction, the standard quantile threshold used in the unweighted case is replaced with a weighted quantile. By Theorem 2 of Barber et al. (2023), these penalties ensure that the resulting prediction set retains valid marginal coverage.

Therefore, by adapting the same steps as in Section A.1—but replacing the empirical quantiles with weighted quantiles and applying Theorem 2 of Barber et al. (2023), we obtain the stated result. ∎

We also introduce a result for coverage for fixed scaling values of under some assumptions.

Corollary A.9.

Assume that the CDF of the residual for an out-of-sample point is Lipschitz continuous with constant . Furthermore, if the maximal value of (resp. ) is bounded by , then if we set (resp. ) with , we have coverage with

Proof.

Consider , which has coverage guarantee

By assumption, , and thus instead using results in a change of at most , which by Lipschitz continuity of the CDF produces a resultant change of in the probability guarantee. ∎

The existence of the Lipschitz condition is quite reasonable, for example, we consider to be a linear function and the noise term is normally distributed, the residuals themselves are half-normally distributed and thus satisfy the above requirement. We pay a small theoretical guarantee when shrinking the interval, under the assumption is small, which is not necessarily true (and is generally unknown). However, this result gives the intuition that if one of the residual pieces contributes little to the overall error, we can remove it for little coverage cost and serves as part of the motivation for the adaptive algorithm. We find that for certain settings with unbalanced residual components, even simple heuristics such as where achieves similar coverage to the full residuals.

Appendix B Conceptual information

B.1 Discussion on Quantiles of Residual Components.

We observe that when quantiles of the residual components are taken then summed, they do not necessarily serve as upper-bounds on the corresponding quantiles of the full residuals, which we use in our implementation. Specifically, the inequality

may not hold. This observation is significant because while the triangle inequality holds for each individual point, i.e., , such a relationship does not extend to the quantiles. This discrepancy is intentional, as it allows for a tighter combination of residuals compared to the traditional residual. Moreover, in practice, this situation occurs rarely.

B.2 Notation Table

We provide a table of notation in Table 1.

| Symbol | Meaning |

|---|---|

| First stage hypothesis | |

| Second stage hypothesis | |

| Residual for two-stage model | |

| First stage residual component | |

| Second stage residual component | |

| Desired Miscoverage Rate | |

| Scaled weight for | |

| Scaled weight for | |

| Quantile level to take of | |

| Quantile level to take of | |

| Rejection stringency to control FWER | |

| Step-size for updating with empirically performing well | |

| Step-size for updating with performing well | |

| Tolerance for calculating -values for hypothesis testing | |

| Window length for adaptive method, with stabilized performance above 100 points |

B.3 Choice of Components

Certainly, one could instead take quantiles or rescalings of the total sum instead of separating it into components. However, we choose to separate it for multiple reasons. First, we note that by splitting the quantiles/weights, it becomes clear in the decomposition which stage contributes more to the error. Second, under co-monotonicity of , the quantiles of match and thus both approaches result in the same interval which satisfies coverage guarantees as it is an upper-bound on the black-box width. Furthermore, for smaller miscoverage levels then is an upper-bound on , so our use of can be an upper-bound. Lastly, we also desire the ability to be tighter than at times, unlike , to be able to quickly adapt to easy settings.

B.4 FWER-controlling Algorithms for Scaling Selection

To construct the set of valid scaling parameter pairs , we apply multiple hypothesis testing procedures that control the family-wise error rate (FWER). This ensures that, with high probability, none of the accepted scaling pairs exhibit a true miscoverage rate above the nominal level .

Definition B.1 (FWER-Controlling Algorithm).

Let be a candidate set of scaling pairs, and let denote the associated -values testing the null hypothesis that the miscoverage of each exceeds . A selection procedure is said to control the family-wise error rate (FWER) at level if:

where is the set of true null hypotheses.

Bonferroni Correction.

A classical method for controlling FWER is the Bonferroni correction. It accepts any for which , where . By the union bound, this ensures that the probability of falsely including any with miscoverage above is at most . However, Bonferroni can be overly conservative when the number of tests is large.

Fixed Sequence Testing.

To improve power in large-scale settings, we adopt fixed sequence testing (Bauer, 1991). This procedure assumes a pre-specified ordering of hypotheses , based on prior knowledge or heuristics (e.g., larger values of are expected to have lower risk). Hypotheses are tested sequentially: each is compared to , and the first failure (i.e., ) terminates the process. All previous hypotheses are accepted, and the rest are rejected. This method is more powerful than Bonferroni in the presence of a meaningful ordering.

Practical Note.

In our algorithm, we use fixed sequence testing to select valid scaling parameters. If no candidate passes the test, i.e., , we abstain from prediction. This outcome indicates a lack of statistical evidence and may signal that additional calibration data or model refinement is necessary.

B.5 Adaptive Method Pseudocode

We define the coverage indicator at time as To capture deviations in the score components, we define to be 0 if the true value lies within the estimated quantile interval for , and equal to the excess otherwise. This can be succinctly written as and similarly for .

Appendix C Extensions

C.1 Additional Heuristic

One could alternatively define the residual components and combination as signed residual components to obtain tighter, asymmetric intervals, at the cost of coverage. We define new residual components

such that the sum of the components is exactly the full error rather than an absolute value upper-bound. Because the components are now signed, one should construct intervals differently, which also results in asymmetric intervals. Similarly to before, we can scale each component to produce intervals of the form

Experimentally in IID settings, it produces slightly tighter intervals without additional tolerance, however this heuristic is more prone to producing empty sets. For example, we report the performance of the method under IID settings with varying levels of nominal error rate in Table 2 exemplifying this behaviour.

| Metric | ||||

|---|---|---|---|---|

| Coverage | 0.90130.02 | 0.91960.01 | NA | NA |

| Width | 2.02650.13 | 2.15230.12 | NA | NA |

Thus we have chosen to use the heuristic given in the main body of the text, but we provide this as an option for many possible ways of constructing intervals using the residual decomposition we introduce. Furthermore, because the decomposition itself is flexible, one could incorporate any recent conformal prediction advancements into the ways quantiles are taken, such as weighted data, or in the adaptive case how the stepsize and etc. change.

C.2 Stationary -mixing

We describe how the FWER control method outlined in Section 6 can be extended beyond the IID setting to accommodate stationary -mixing processes. Note that for dependent data, the concentration properties of empirical quantities degrade, resulting in looser tail bounds. This, in turn, inflates the values of the empirical error estimates , thereby requiring larger thresholds to ensure that the selected set remains nonempty.

Our goal is to identify values of for which the expected coverage error is below a target level . For each , we consider the null hypothesis

and compute an empirical estimate of the coverage error using a held-out calibration dataset. To test this hypothesis, we apply a concentration inequality that bounds the deviation of the empirical error from its expectation under dependence. Specifically, we employ a result for bounded functions of -mixing sequences from Kontorovich and Ramanan (2008), with refinements from Mohri and Rostamizadeh (2010), which provides suitable control over the error rates in the non-IID case.

Theorem C.1 (Mixing Concentration Inequality).

Let be random variables distributed according to a -mixing distribution. Let be a measurable function that is -Lipschitz with respect to the Hamming metric for some . Then, for any , the following inequality holds:

where

We apply this theorem with . Clearly this is -Lipschitz with respect to Hamming metric. Furthermore,

due to stationarity and the null hypothesis. Then

where we substitute our realized for and plug it into the RHS to obtain a -value for .

Then we have the following:

Corollary C.2.

Let be the set selected by a FWER-controlling algorithm at level , based on -values computed over using the above method, which is assumed to be stationary -mixing. Then, for any , we have

where the outer probability is over the randomness of , and the inner probability is over the test point which is assumed to be drawn from the same stationary distribution.

While the statement of the result is similar to before, note that is a conservative upper-bound on the true -value, thus the threshold to accept a is more stringent. We show that the are still super-uniform. Let be the random variable representing empirical risk when the error rate is and be the empirical risk when the error rate is . Under the null hypothesis, , which implies that stochastically dominates (). Let and and represent CDFs of and respectively. Then

Furthermore, letting , by the stochastic dominance assumption,

Then we apply a FWER-controlling algorithm such as one from Section B.4 to set the acceptance threshold to reject the null hypothesis such that the total type-1 error rate is less than , then use Theorem 1 of Angelopoulos et al. (2025) (Theorem A.6).

C.3 Decomposition for Auxiliary Data

We can also define and when considering auxiliary data.

Definition C.3.

If we have sample where data is of the form where represents auxiliary data for the second stage such that we have learned upstream and downstream models , . Then we can decompose the residual into components as the following for some new point

We can use these residual components to create prediction intervals analogously to the original setting without auxiliary data.

C.4 Decomposition for multi-stage model

Now we consider extending the definition of to more than two stages. We provide a straightforward extension, but a cleverer one may exist.

Definition C.4.

Suppose we have sample where data is of the form with stages and corresponding learned hypotheses . Then for a point , define

Observe that the sum of these terms is still an upper-bound on the “full” residual by the triangle inequality and thus we have a residual decomposition.

An issue with this definition is that if we try a hypothesis testing method and FWER algorithm to weight each of these components, the set becomes prohibitively large as it grows exponentially with each stage. A FWER algorithm that is able to intelligently search the possibilities will become necessary, whereas for two-stages, it was feasible to search across the entire grid. One way to mitigate this is to restrict the proposed set at each step by focusing only on the most important residual components, fixing the weight of the remaining ones to remain; i.e., select the top residual components with the highest average width in the window of recent observations and define only for those components, freezing the other component weights. In fact, one can sort the residual components by magnitude then sequentially search through , freezing the others outside of the top , resulting in only tests, if is the number of sub-divisions for each component.

C.5 Decomposition for Multiple Upstream Models

We consider an augmented two-stage model, with multiple upstream models each producing a component of , the intermediate value, which is now vector valued. Suppose there are upstream models, that each map upstream features to their corresponding intermediate feature in . Denote the output of the -th upstream model to be . Then we can define components for each downstream feature and take a weighted sum. Thus, for the -th downstream feature, we have

Then see that a convex combination forms an upper-bound on . This approach has a similar issue as the multi-stage model, as the search-space scales with the number of upstream models.

Appendix D Additional Experiments

We provide additional experiments on the non-adaptive methods and adaptive methods, providing further insight into the parameters of the split residual method and the resulting coverage improvements. We include hyperparameter ablation studies as well as an additional real-world dataset. We include experiments on covariate shift to demonstrate that the split residual method is robust to multiple types of shift and is not limited to stage-wise shift, which was extensively explored in the main text. All experiments were conducted on a laptop with an Intel i7 processor and 8GB of RAM. No specialized hardware (e.g., GPUs or TPUs) was used for training or evaluation.

D.1 Experimental Hyperparameter Details

We describe the default hyperparameters we use for the other methods in our experiments: SC, WSC, ACI, DtACI, PID, OCID, ECI.

-

•

SC: There is no other parameter used for split conformal prediction intervals other than the nominal desired miscoverage level (default = 0.1) which we keep the same across all methods

-

•

WSC includes a weighting parameter 0.99 which exponentially weights points as they go further back in time, resulting in recent points having more weight.

-

•

ACI updates using the same default step size as well as the same default window size as our method.

-

•

DtACI uses default multiple candidate values for step-size as well as a window size which we default to .

-

•

ECI uses the same default step size .

-

•

PID uses the same default step size , and window size . Two additional parameters KI and are estimated with appropriate hypothesized bound depending on the data, using the default heuristic given in Appendix B of Angelopoulos et al. (2023).

-

•

OCID uses decay parameter with the decay weight function given by Angelopoulos et al. (2024b)

Furthermore, note that for our method is a subset of the held-out data which the other methods have full access to, so we do not use additional data relative to the other methods but simply partition it into smaller sets, which has little effect.

D.2 Hyperparameter Guidelines

We provide some simple guidelines for parameter settings for both the non-adaptive and adaptive case.

-

•

A default grid: , which can be improved in granularity based on the size of calibration set . A suggested granularity could be number of grid points. Experimentally, we used a default .

-

•

Initial values of (or fixed values for the non-adaptive case) we recommend balanced . If one wishes to be more upstream-sensitive, and if one wishes to be downstream-sensitive, .

-

•

For , a default choice of is for moderate conservativeness, but is a more conservative choice that induces more abstention.

-

•

For to be more conservative, we default to , but improves efficiency Table 5, so in “easier” regimes such as IID one should choose such values.

-

•

For window-size for the adaptive method, we recommend , however, the more held-out data the more efficient values the method can consider.

-

•

For step-size we recommend a default of 0.01 which has sufficed under a variety of scenarios, however a grid of should cover all possible values.

-

•

For step-size we recommend a default of 0.01 for stable performance; higher values encourage more extreme behavior (more efficient widths, but higher abstention rate)

We also provide a quick flow-chart for deciding parameter values

-

1.

Is data stationary (IID)?

-

•

YES: Use non-adaptive method (Section 5)

-

–

Set

-

–

-

•

NO: Use adaptive method (Section 6)

-

–

Set

-

–

-

•

-

2.

Are both stages equally reliable?

-

•

YES: Keep

-

•

NO: Increase quantile level for less reliable stage

-

–

Upstream unreliable:

-

–

Downstream unreliable:

-

–

-

•

-

3.

What is the cost of coverage violations?

-

•

HIGH: (accept more abstentions)

-

•

MED: (default)

-

•

LOW: (prioritize efficiency)

-

•

-

4.

How much data is available?

-

•

: Use fine grid for (0.1 increments)

-

•

: Use coarse grid for (0.2 increments)

-

•

D.3 Non-Adaptive Experiments

We discuss results for the non-adaptive intervals using our residual decomposition as well as hyperparameter ablation studies.

D.3.1 Coverage under shifts

We first report the results under gradual upstream and downstream shifts, and then rapid upstream and downstream shifts.

| Shift | Metric | SRa,b (c=d=0.01) | SRa,b (c=0.05,d=0.01) | SC | WSC | CC |

|---|---|---|---|---|---|---|

| Gradual | Coverage | 0.8233 | 0.7280 | 0.7488 | 0.9230 0.01 | |

| Width | 2.9884 | 2.4272 | 2.3726 | 2.4849 | 3.91210.20 | |

| Rapid | Coverage | 0.8041 | NA | 0.6910 | 0.7218 | 0.91870.02 |

| Width | 3.9703 | NA | 2.9544 | 3.1969 | 5.9236 0.39 |

| Shift | Metric | SRa,b (c=d=0.01) | SRa,b (c=0.01,d=0.05) | SC | WSC | CC |

|---|---|---|---|---|---|---|

| Gradual | Coverage | 0.9309 | 0.9133 | 0.8695 | 0.8748 | 0.9776 0.01 |

| Width | 2.4274 | 2.3738 | 2.0143 | 2.0472 | 3.1639 0.14 | |

| Rapid | Coverage | 0.8981 | NA | 0.8419 | 0.8506 | 0.9760 0.01 |

| Width | 2.4878 | NA | 2.1035 | 2.1498 | 4.37120.43 |

Our method achieves higher coverage than the other methods (besides CC), which suffer degradation under distributional shifts, particularly under upstream. For example, our method drops from 0.84 to 0.80 coverage vs. SC dropping from 0.73 to 0.69 for gradual vs. rapid upstream shifts. These coverage improvements are at the cost of wider intervals and occasional abstention; this trade-off is worthwhile when attribution and robustness are prioritized. We note that selecting larger (resp. ) increases the sensitivity of the method to upstream (resp. downstream shift), resulting in abstention under rapid shifts. This is intentional, with abstention signaling that retraining may be necessary for the given stage; black-box methods lack this ability, as they cannot isolate which part of the model fails, resulting in unnecessary retraining.

Thus, and control sensitivity: by selecting larger or smaller and , practitioners can balance robustness and abstention at each stage, offering flexibility beyond traditional conformal approaches. We note that while CC meets the coverage level here, it severely over-covers in all cases, particularly under downstream shifts and simpler settings (Section D.3.4). Below we provide a few more comparisons with CC.

D.3.2 Comparison with Cascaded Confidence

We compare against the non-adaptive method of Gong et al. (2023), which we denote CC. CC uses a similar error decomposition but applies a direct upper-bound, with an optional K-means clustering step to select the interval width; we compare against this K-means variant. CC has two notable drawbacks: (i) the K-means clustering step forfeits coverage guarantees, and (ii) it tends to over-cover with wider intervals. We include CC throughout the tables and figures in the Appendix, but we provide equivalent figures for Figure 2 with CC here (Figure 5). CC severely over-covers across settings. Under rapid shifts it attains higher coverage than the other methods (especially upstream; see the following section), but this reflects uniformly wide intervals rather than calibration, as its widths remain large even in easy regimes, with no tolerance parameter allowing for tightening, unlike our method.

D.3.3 Upstream Shift Figures

We provide upstream gradual and rapid shift figures analogous to Figure 2. We see similar behavior for which our methods with and perform better in coverage relative to SC and WSC and similarly to CC at larger , but with a larger drop in coverage compared to the downstream shifts. This is quite intuitive as an upstream shift compounds through two models and has a larger impact on performance. Importantly, for gradual shifts it appears is sufficient for moderate coverage performance, while being quite efficient, if being slightly below nominal is acceptable. We note that under rapid shifts for lower , we see WSC does begin to outperform , but not . On the other hand is able to maintain coverage at larger values of even under severe shifts at the cost of additional width. This demonstrates the ability of to customize the approach’s conservativeness. CC performs well under upstream shift but, as elsewhere, greatly over-covers at lower , which is a consistent over-coverage pattern rather than genuine calibration.

D.3.4 Coverage under easy settings

We implement both Definition 5.3 and Definition 5.1 separately and test them on simple IID data with linear relationships between . We also include results for IID synthetic data featuring a nonlinear relationship in which the upstream task is a binary classification task of diagnosing a patient for a disease given their health (using logistic regression), and the downstream model predicts the cost of treatment given the upstream probabilistic prediction (using XGBoost). Additionally, we implement these prediction interval methods in a -mixing setting which we provide guarantees for in Section C.2 where the data is generated by a stationary AR(1) process with bounded uniform noise (known to be a -mixing process (Athreya and Pantula, 1986)) and linear relationships between . We report the width and coverage of the methods in Table 4.

| Shift | Metric | SC | WSC | CC | ||

|---|---|---|---|---|---|---|

| Linear | Coverage | 0.9439 | 0.9492 | 0.8971 | 0.9062 | 0.9889 0.01 |

| Width | 2.3555 | 2.3930 | 1.9924 | 2.0584 | 3.16350.25 | |

| Non-linear | Coverage | 0.9416 | 0.9794 | 0.8969 | 0.9300 | 0.99980.01 |

| Width | 4.6343 | 5.2007 | 4.2179 | 4.5089 | 7.1755 0.42 | |

| Non-IID (linear) | Coverage | 0.9561 | 0.9886 | 0.8997 | 0.9067 | 0.9335 0.01 |

| Width | 3.1299 | 3.6106 | 2.6749 | 2.7304 | 2.9042 0.09 |

We observe that both are conservative for these settings, producing wider intervals but attaining the desired coverage guarantee, while CC greatly over-covers in all cases by a significant margin. Thus, our methods tend to over-cover in easier settings such as IID data and stationary -mixing conditions because FWER hypothesis testing requires an error rate below whereas for other methods simply being close is sufficient. Note that is without tolerance. Thus, as we see in the ablation studies below, over-coverage can be easily remedied if desired by including a tolerance for the hypothesis test itself, which CC is unable to do.

D.3.5 Hyperparameter Study

We vary the tolerance parameter which alters the hypothesis test, obtaining to demonstrate that when comparing our method with some tolerance, the width and coverage even under the IID settings are comparable and do not over-cover.

| Method | Metric | |||

|---|---|---|---|---|

| Coverage | 0.92400.01 | 0.91500.02 | 0.90190.02 | |

| Width | 2.17500.09 | 2.09220.08 | 2.01920.11 | |

| Coverage | 0.95160.01 | – | – | |

| Width | 2.40320.05 | – | – | |

| SC | Coverage | 0.89810.01 | – | – |

| Width | 2.00510.04 | – | – | |

| WSC | Coverage | 0.90150.02 | – | – |

| Width | 2.03200.13 | – | – | |

| CC | Coverage | 0.9889 0.01 | – | – |

| Width | 3.16350.25 | – | – |

We observe that even low values of the tolerance parameter, such as , are sufficient to make similar to the black-box methods in the IID setting. This suggests that is not simply over-covering, but rather enforcing stricter criteria for valid prediction intervals than the black-box approaches. These stricter requirements likely contribute to its improved performance under distributional shifts. Therefore, if one seeks tighter but potentially less robust intervals, adjusting the tolerance parameter provides a principled way to trade-off between coverage robustness and interval sharpness, however experimentally, unless stated otherwise, we use .

We also vary the parameter, which controls the FWER rejection threshold, which for smaller values encourages more sensitivity of the method overall to abstain from producing an interval; in a sense it has a similar effect to parameters but collectively for both stages at once rather than a stage-wise sensitivity.

| Method | Metric | |||||

|---|---|---|---|---|---|---|

| Coverage | NA | NA | 0.89690.08 | 0.92940.02 | 0.92680.02 | |

| Width | NA | NA | 2.22310.09 | 2.21950.10 | 2.18670.11 | |

| Coverage | 0.95040.01 | – | – | – | – | |

| Width | 2.39190.05 | – | – | – | – | |

| SC | Coverage | 0.89920.01 | – | – | – | – |

| Width | 1.99870.04 | – | – | – | – | |

| WSC | Coverage | 0.90820.02 | – | – | – | – |

| Width | 2.06030.14 | – | – | – | – | |

| CC | Coverage | 0.9889 0.01 | – | – | – | – |

| Width | 3.16350.25 | – | – | – | – |

D.4 Adaptive Experiments

We include additional experiments using additional synthetic experiments with covariate shift and real-world stock data to demonstrate the flexibility of our method. Furthermore, we provide visualizations of the scaling parameters to demonstrate the identification of the decomposition. In addition, we perform hyperparameter sweeps over the synthetic dataset described in Section 8. We also include comparisons to additional cutting-edge baselines DtACI and ECI, although both methods perform poorly where the former tends to be inefficient and the latter tends to undercover.

D.4.1 Stocks Dataset

We consider a dataset consisting of daily closing values of three SP 500 stocks, AAPL, AMZN, MSFT with the goal of forecasting the AAPL closing value. We do so via a two-stage approach in which the first-stage is an N-BEATS forecasting model that forecasts the three stocks at a 6-day horizon, then the second-stage is ridge regression that predicts AAPL given the forecasted values to correct for error from the first stage. We rescale the data and compare against ACI, Conformal PID, and OCID methods to showcase the robustness of our method. The coverage of these methods is presented in Figure 7.

We observe that our adaptive method provides better coverage than the other baseline methods, particularly when the forecasts perform worse in July and October, seeing a much less dramatic drop in performance while not being overly tight. Our method uses almost the same average width (0.1347) as ACI (0.1344), while the other methods have tighter intervals but significantly worse coverage. We list the results in the table below Table 7, and visualizations in Appendix Figure 8. We see that there are two main sudden distribution shifts, and that in comparison to ACI, our method is able to capture the second distribution shift, while OCID is also able to but has volatile intervals during the stable period prior to the distribution shifts.

| Method | Avg. Width | Std. Width | Min Coverage |

|---|---|---|---|

| SR(adaptive) | 0.1347 | 0.0216 | 0.89 |

| ACI | 0.1344 | 0.0193 | 0.86 |

| PID | 0.1183 | 0.0226 | 0.85 |

| OCID | 0.1240 | 0.0348 | 0.83 |

| ECI | 0.0645 | 0.0166 | 0.52 |

D.4.2 DtACI and ECI

We also include results on additional baselines, ECI and DtACI. While DtACI is designed for online adaptation, it may be less effective in fixed-horizon forecasting tasks where the lag between prediction and feedback complicates adaptation. Further, ECI focuses on efficiency but with severe shifts may be too optimistic.

First, we discuss results for DtACI, using the method in comparison to the others for the same synthetic dataset with two drastic distribution shifts used in Section 8.2, with the plots shown in Figure 9(a).

We observe that DtACI outputs values of which we clip to 1, resulting in very conservative intervals and is extremely unstable. This is most likely due to the fact that it is not designed for forecasting with a horizon and suffers in performance because of that. We see similar behavior for the automobile indicators dataset (Figure 10), in which DtACI achieves good coverage but is wider (compared to our method) because it often outputs . Interestingly, this does not hold for the stocks dataset, where DtACI produces the tightest intervals but has the worst coverage.

We obtain similar conclusions for ECI, however this method is designed for better efficiency and tends to produce tighter intervals, resulting in consistently being too optimistic and producing much tighter intervals than the other methods at a significant cost to coverage (Figure 11).

D.4.3 Automobile Visualizations

We also include additional visualizations of width and coverage for the automobile dataset in Figure 12. We note that our average width over the entire range is strong in efficiency (18.957), only behind PID (18.469), ACI (15.696), OCID (15.667), and ECI (7.734) which have poor coverage, whereas DtACI is significantly wider (31.356). We note that OCID’s efficiency here also does not appear to be due to good calibration but due to high variance in interval width.

We also include comparisons of empirical coverage and width of our method compared against ACI, PID, and OCID across various values of in Figure 13. These values are averaged over the last four years of the automobile indicator data to specifically capture the COVID-19 spike. We see that our coverage is strong across multiple values of while remaining relatively well calibrated, particularly around and being tighter than OCID at low (0.1) and high (0.9) nominal coverage levels. Note that coverage dips at due to abstention which we do not count. Furthermore, while OCID is well-calibrated visually, it very quickly alternates between large and small widths even under no shifts (2014-2019), resulting in non-informative interval widths that are not truly calibrated for the shifts.

D.4.4 Hyperparameter Study

First, we visualize the effect of various values, which affects the rate at which changes. We find that our method excels at lower values of and performance decays at higher values such as , particularly because this causes to drop to extremely low values, making the algorithm abstain from producing intervals under large shifts. We display the coverage effects for synthetic data in Figure 14 and for Manheim data in Figure 15, where we see a similar decay as increases.