How much should we care about what others know?

Jump signals in optimal investment under relative performance concerns

Abstract.

We present a multi-agent and mean-field formulation of a game between investors who receive private signals informing their investment decisions and who interact through relative performance concerns. A key tool in our model is a Poisson random measure which drives jumps in both market prices and signal processes and thus captures common and idiosyncratic noise. Upon receiving a jump signal, an investor evaluates not only the signal’s implications for stock price movements but also its implications for the signals received by her peers and for their subsequent investment decisions. A crucial aspect of this assessment is the distribution of investor types in the economy. These types determine their risk aversion, performance concerns, and the quality and quantity of their signals. We demonstrate how these factors are reflected in the corresponding HJB equations, characterizing an agent’s optimal response to her peers’ signal-based strategies. The existence of equilibria in both the multi-agent and mean-field game is established using Schauder’s Fixed Point Theorem under suitable conditions on investor characteristics, particularly their signal processes. Finally, we present numerical case studies that illustrate these equilibria from a financial-economic perspective. This allows us to address questions such as how much investors should care about the information known by their peers.

- Mathematical Subject Classification (2020):

-

91G10, 91A06, 91A16, 91B06

- Keywords:

-

Optimal investment, jump signals, relative performance concern, idiosyncratic information

1. Introduction

Information is a key driver of investment decisions, especially when shaped by idiosyncratic signals about impending stock price shocks. When combined with relative performance concerns—the competitive drive to measure one’s wealth against the average—this creates a compelling dynamic: investors must not only interpret their own signals but also account for their peers’ information flows and resulting actions, leading to questions such as: How much should we care about what others know?

In this paper, we propose a simple and tractable framework that allows us to address such questions. We combine the works of [BK22] and [LZ19] to obtain a financial market model featuring a heterogeneous population of agents who make strategic decisions based on dynamically generated idiosyncratic signals on imminent price shocks. Their goal is to maximize their own expected utility from a ratio between their terminal wealth and a measure of their peers’ average wealth.

We start with a finite number of investors who trade between their individual risk-free bank accounts that pay a constant interest rate and individual risky assets modeled by exponential Lévy processes. These processes are driven by an idiosyncratic Brownian motion, a common Brownian motion and a Poisson random measure generating both common and idiosyncratic jump noise. Such an asset specialization reflects real-world observations: investors often concentrate on stocks they are familiar with (cf. [MER87]), are geographically bound to (cf. [CM99]), or specialize in certain industries (cf. [KSZ05]). That said, the possibility of one common stock market for all investors is a special case of this setting.

The key modelling feature is the presence of short-lived idiosyncratic jump signals: at (random) times the market is subject to a price shock and, at the same instant, some or all investors may receive idiosyncratic signals that carry imperfect information about that imminent price jump. Investors who receive a signal can react instantly by adjusting their fraction of wealth invested in the stock right before the price shock materializes. So, intuitively, the timeline of events as follwos: first the investor receives a signal about a price jump, allowing her to adjust her position right before the actual price jump is realized. In other words, the investor reacts to a signal on an impending price shock before the latter materializes. In [BK22], the authors develop a rigorous theory for these kinds of jump signals and signal-driven strategies in the context of a single investor’s optimal investment problem. Formally, strategies should be measurable with respect to a so-called Meyer--field that enriches the predictable field by the signal; we refer the reader to [LEN80, BB19] and [BK22] for the precise definitions and constructions.

Importantly, in the present paper the information provided by signals may differ between investors: for example, some investors may receive more frequent but less reliable signals than others, or different investors may observe different signal-to-noise ratios. To capture investor heterogeneity, we therefore allow differences both in the information structure (signal arrival intensity and signal quality) and in economic parameters such as risk aversion and performance-concern coefficients. Empirical evidence from [KOI14] supports the presence of heterogeneity in risk aversion among fund managers and motivates consideration of agents who differ in their attitudes toward absolute and relative wealth. Each investor’s characteristics are collected in her type vector, whose distribution is assumed to be common knowledge; this assumption is partially justified by the public observability of past returns and other performance indicators (cf. [KOI14]), which allow market participants to infer, at least approximately, peers’ types.

Strategic interactions among investors arise from various motivations. For individual investors, these interactions may stem from aspirations to accumulate more wealth than their peers (cf. [ABE90, DKK08]). For fund managers, interactions may reflect career concerns or efforts to attract inflows (cf. [BM13]). We model these interactions through relative performance concerns: investors adopt power utility where a concern parameter mediates the trade-off between absolute terminal wealth and a measure of peers’ geometric mean terminal wealth. Optimal investment under such relative performance criteria has been studied in [Fd11, ET15, BM13, BLd17, LZ19], among others.

The relative performance criteria lead to an interdependence of the investors’ target functionals and thus introduce a stochastic game of optimal investment which calls for the search for Nash equilibria. To address this, we focus on a class of signal-driven strategies, where investment decisions depend only on the signal (if any) received at each time. This choice is motivated by the work of [LZ19], where the authors construct the unqiue equilibrium where investors hold time-independent constant positions. In our setting, this corresponds to what we call signal-driven strategies where agents employ time-independent policies reacting to the jump signals received, i.e., they continuously hold a baseline position in the stock, and react with instantaneous adjustments to jump signals. The existence of a Nash equilibrium with such signal-driven stategies is established in two steps. First, we solve a single investor’s best response problem when her peers follow fixed signal-driven strategies. Using the approach in [BK22] we formulate an Hamilton-Jacobi-Bellman (HJB) equation and prove the corresponding verification result which characterizes best response strategies as solutions to one-dimensional concave optimization problems and identifies them to also be signal-driven. This allows us to introduce, in a second step, a fixed-point mapping that encodes the so-called consistency condition: each strategy must coincide with its best response given the peers’ strategies. Under suitable assumptions on the investors’ types, we use Schauder’s fixed point theorem to establish the existence of an equilibrium.

The focus on signal-driven strategies is even more natural in a mean field setting where a single agent’s action does not impact the overall average considered by her peers. We thus provide a formulation for the corresponding mean field game via randomization over the investors’ type vectors. The random type then represents the representative investor for which we can again solve the best response problem having fixed the competitive environment. An important intermediate step is the derivation of the geometric mean wealth in the mean field setting by conditioning on the common noise. For this, we carefully disentangle which part of the randomness is common to all investors and which part is idiosyncratic (and thus averaged out in the mean field limit).

Finally, we prove existence of a mean field equilibrium in two scenarios. First, we analyze the case of finitely many investor types under suitable assumptions, employing arguments analogous to those used in the multi-agent game. Secondly, when the mean field allows for infinitely many different types, we devise an alternative fixed-point map which permits us to prove existence of an equilibrium under the assumption of finitely many distinct common shock marks.

In numerical experiments we investigate how idiosyncratic investment signals affect investors with relative performance concerns. For concreteness we fully specify a mean field game with two types of investors and introduce a suitable certainty-equivalent measure for one of these types. By varying parameters across types we explore questions such as how much an investor should care about what is known by her peers. Our findings reveal a dual effect: investors who value relative wealth prefer their peers to have strong (and even superior) signal quality because better-informed peers help mitigate relative wealth fluctuations; they also support increased competitiveness among peers because this aligns incentives to stabilize fluctuations in relative wealth. At the same time investors favor a relatively uniform signal quality across the population: when peers’ signals are equally reliable to one’s own, their impact is limited, whereas differences in signal reliability amplify the role of others’ information.

Related literature. Multi-agent and mean field games provide a powerful framework for the study of strategic interactions among a large number of agents, such as investors in financial markets. While multi-agent games capture the finite-population dynamics where individual decisions may affect others, mean field games approximate these interactions in large populations by considering the aggregate behavior, which simplifies analysis and computation. Mean field games, introduced independently by [HMC06] and [LL07], have become influential in financial mathematics over the last two decades; for general treatments see [BFY13, CDL+19, CD18]. For works closest to our setting, see [ET15, BLd17, LZ19]. The former two consider optimal investment for exponential utility with relative performance concerns in Black–Scholes markets; [ET15] establishes existence and uniqueness of Nash equilibria, and [BLd17] studies -agent and mean field formulations via coupled quadratic BSDEs. The latter, [LZ19], treats CARA and CRRA preferences in a Black–Scholes market with common-noise Brownian motion and obtains unique time-independent constant equilibria; it has inspired a number of subsequent works including [BG23, BWY24a, BWY24b, LS19, dP22, FZ23, SZ24].

None of these works, however, considers in detail the interplay between asymmetric, short-lived information about market jumps and relative utility maximization. There is relatively little literature treating jumps as both part of common and idiosyncratic noise. In this direction, [BH24] considers a mean-field portfolio game with idiosyncratic and common jump components modeled via integer-valued random measures; they characterize equilibria for exponential (CARA) utility via McKean–Vlasov FBSDEs with jumps and show existence and uniqueness.

We take a different path and use a Poisson random measure to place, at common jump times, both idiosyncratic and common jump marks. These jump marks account both for jumps in stock prices and for idiosyncratic signals which may carry imperfect information about the price jumps. In particular, our investors can be viewed as ‘small insiders’ who do not affect prices and for whom any information advantage on imminent price shocks is short-lived. It is precisely this short-lived, instantaneous nature of the information advantage that makes the model tractable: because signals are revealed and acted on at the same moment as the price jump, strategic complications such as information leakage (what do my trades reveal about my private signal?) or bluffing (strategically misleading other players) are irrelevant as they would not give our investors an edge.

Finally, the heterogeneity in signals allows us in our numerical illustration to consider agents with different signal frequencies and signal qualities. So, when receiving signals, the agents will muse not only about what the signal means for the ultra-short-term price development, but also about how many of their peers have also received signals and what these entail for their investment choices. Under relative performance concerns, these considerations are reflected in their decision policies and allows us to answer the question How much should we care abouth what others know?

The remainder of this paper is organized as follows. Section 2 introduces the multi-agent game, analyzes the single-agent best-response problem and proves existence of Nash equilibria. Section 3 develops the mean field formulation and proves existence of mean field equilibria. Section 4 presents numerical experiments and discusses economic implications.

2. The Multi-Agent Game

This section introduces a multi-agent framework where investors navigate interactive utility maximization in the presence of jump signals. Subsection 2.1 presents the market model, the investors’ signal processes and their sets of admissible strategies. Subsection 2.2 specifies the individual utility functions, accounting for relative performance concerns and heterogeneity in risk aversion and concern parameters, which shape the investors’ best response problems. Subsection 2.3 provides a best response map for a single investor interacting with investors who employ fixed signal-driven strategies. Subsection 2.4 provides a proof of existence of a Nash equilibrium. Finally, Subsection 2.5 establishes a convergence result for aggregate wealth as the number of investors goes to , paving the way for the mean field game.

2.1. The Financial Market Model with Jump Signals

In the following, we introduce the market model and specify the investors’ admissible strategies.

Let be a finite time horizon and . In our model, randomness is introduced via a probability space which supports independent standard Brownian motions and an independent Poisson random measure . The Poisson measure is compensated by the intensity measure for a positive finite measure on some Polish mark space equipped with the corresponding Borel--field . We denote by the right-continuous filtration induced by the completions of

and by the predictable -field generated by all left-continuous -adapted processes on .

Market Model. We consider a finite number of investors111The choice of (rather than just ) investors underscores that we are considering at least two invesors and allows us later to consider a geometric average over the performance of the other investors when specifying the preference structure of a given investor. who trade between their individual risk-free bank accounts with interest rate and an individual risky stocks . The asset price dynamics are given by

| (1) |

for constants and such that for and for measurable functions for . We will assume

| (2) |

to guarantee that each remains nonnegative at all times. So, while the Brownian motions are idiosyncratic noise for respective investor , the Brownian motion accounts for common noise. The Poisson random measure introduces jumps by placing marks at common times for all investors. These marks translate into jump sizes which may differ between the investors .

The Poisson random measure produces common jump times with possibly stock-specific price shocks, so this parsimoniously models events that occur simultaneously across the market (e.g. macro announcements, sector shocks or common liquidity events) while allowing heterogeneous impacts on different assets or portfolios. In other words, the jump times represent common events and the marks capture how those events translate into each investor’s risky asset price.

The simplest setting, on which we will focus on in our numerical experiments, is the single common stock case where all investors trade between the same common bond and the same common stock. This corresponds to the parameter choice where, for all , , , , and for some , , and some measurable function .

The possibility for idiosyncratic stocks does, however, not add any mathematical difficulties and is thus included here for sake of consistency with the literature; see, e.g., [LZ19].

It is merely for notational simplicity that we refrain from specifying a multivariate model with several stocks.

Wealth Dynamics. Let be the th investor’s initial wealth. The th investor’s investment strategies are described by a stochastic process specifying the fraction of wealth invested in the risky asset at times . So, the investor’s wealth process will evolve accordingly as

| (3) |

This will be well-defined for any real-valued predictable satisfying

In fact, since we assumed the intensity measure to be finite, there will be only finitely many jumps in asset prices in each scenario so that wealth dynamics will even be defined for optional with the above square-integrability. We refer to [BK22] for the additional integrability required in the case where allows infinitely many jumps and refrain from considering this possibility here for ease of exposition.

Jump Signals via Meyer--Fields. As already mentioned, when deciding over the proportions invested in the risky asset, investors may, at times, have the possibility to recourse to some signal that gives them extra information on impending jumps in the stock price.

The signal process of the th investor is defined as

| (4) |

for a measurable function . Observing a value allows the investor to infer (typically imperfect) information about the mark that has been set by the Poisson random measure. As a consequence, she will revise the probability of the corresponding asset prices jumps and even start musing who among her fellow investors will also have received a signal, what this signal may have been and what reaction it will trigger. Obviously, we have to allow our investor to account for the received signal in her investment choice and so we let her choose a stategy which can be written as

| (5) |

for some -measurable field . Thus, investor has to decide in a predictable manner about all the respective positions , , she will take if in the next moment she was to receive a specific signal . Mathematically, by [BK22, Corollary 2.2], such strategies are in fact measurable with respect to the Meyer--field generated by the signal process. We refer to [LEN80], [KAR81] and [BB19] for the detailed theory of Meyer--fields.

Admissible strategies. It will be crucial to understand what information each investor can derive from her signals. For instance, the kind of signals received (or not) at any one time will affect the investors’ positions that keep their respective wealth nonnegative almost surely.

We follow the disintegration argument in [BK22, pp.1306-1307]. That is, we write

Note that this disintegration is indeed possible since is finite and positive, cf. [JS03, II. 1.2, p. 65]. The finite measure describes the frequency with which the th investor receives a non-zero signal , while describes the a posteriori distribution of the marks given a signal . Note that .

In moments when investor receives a signal , she can adopt any position that guarantees nonnegative wealth after any imminent price jump that may come from any mark that is compatible with the observed signal in the sense that . To formalize this, we recall (2) and introduce tight jump bounds

which allow us to describe the positions ensuring nonnegative wealth by the interval

Note that these intervals are compact under our henceforth standing no arbitrage condition

| (6) |

which rules out that investors learn for sure the direction of the next price jump given a signal .

In case of no signal, i.e. when , the investor learns that (if any) a mark can only be set in . Thus, if there are no unsignaled shocks, i.e. if , she can choose any position in . If, by contrast, there may be unsignaled shocks, i.e. if , we ensure nonnegative wealth by restricting to positions in

where the jump bounds in this case are

Notice that the condition ensures no arbitrage also when unsignaled shocks can only go in one direction since it ensures that at least one of the Brownian motions or keeps stock prices fluctuating suitably.

This allows us to fix the set of admissible strategies which keep our investors’ wealth levels even strictly above zero as follows:

Proposition 2.1 (cf. [BK22], Corollary 2.5).

Note that an investor only holding bonds will never end up with zero wealth and, so, can always be chosen to include the possibility of a zero investment in stock. In general, our choice of admissible positions shields the investor from ruin and in fact ensures that she has strictly postive wealth throughout. This insistence on strictly positive wealth will become important later when investors are invited to interact with one another, because the individual optimization problems only remain meaningful if none of the other investors’ wealth drops to zero; see the next Section 2.2. It should also be noted that compactness and convexity of is essential for applying Schauder’s fixed point theorem later.

With the financial market model, the signal and wealth processes of investors subject to admissible strategies at hand, we can move on to their individual optimal investment problems.

2.2. Risk Preferences, Relative Performance Concerns and Investor Types

We assume that each investor has an individual constant relative risk aversion . She assesses her wealth not only by itself but also in view of her peers’ average wealth . Her specific concern for the others’ performance is measured by a parameter which enters her utility function via

| (7) |

We furthermore let and, for , we fix

| (8) |

For investor , her peers’ geometric average wealth at any time is of course

| (9) |

and so, comparing the terminal average with her own terminal wealth , she will assess this investment outcome by its utility

| (10) |

Given this utility structure, a concern parameter close to corresponds to low (or even no) relative performance concerns while close to corresponds to high relative performance concerns of the th investor. In other words, the higher the value of , the more the investor’s concern shifts from her net worth to its size compared to the average wealth . Clearly, the geometric mean is chosen for tractability, as it allows us to exploit the homogeneity of the utility function. Economically, this specification captures a simple “keeping up with the Joneses” motive (cf. [GAL94]): investors care not only about how much wealth they accumulate in absolute terms, but also about how well they perform in comparison to others. Note that degeneracies will occur when one of the investors has as this entails , a singularity we will be able to avoid due to our notion of admissible strategies, see Proposition 2.1.

Remark 2.2.

We model the interaction and relative performance concerns as in [LZ19, Section 3]. The authors in [LZ19] investigate both constant absolute risk aversion (CARA) and constant relative risk aversion (CRRA) utility separately. Since [BK22] considers CRRA utility only, we focus here excusively on such utility functions as well, making this paper correspond to the special case where . Note also that we omit the case corresponding to log-utility, because investors with log-utility are always indifferent to their peers, regardless of .

The characteristics of each investor are now fully described and can be summarized by her corresponding type (vector)

from the type space

where denotes the set of measurable functions mapping to .

Noting that a collection of type vectors captures all relevant information about the investors involved, we henceforth assume types to be common knowledge, that is all investors know their own type and the other investors’ types.

It will be convenient for our analysis to make the following standing assumption:

Assumption 2.3.

Our investors’ types are such that

-

the stock price remains nonnegative, i.e. ,

-

the no-arbitrage condition holds, i.e. ,

-

the signal map takes only finitely many values, and

-

jump sizes are sufficiently integrable, in the sense that

Here, means that, while there may be an infinite range of possible marks placed by the Poisson random measure, each signal function , classifies this information into a range of only finitely many discrete categories. This is not unreasonable in a real-world context, as this classification helps reduce the complexity of decision making by providing a manageable amount of information that is still sufficiently useful. Mathematically, will be crucial to get the necessary continuity and compactness we need for our proof of existence of a Nash equilibrium. Condition is a non-degeneracy assumption which ensures that expected utility functions remain finite.

Moreover, this assumption allows to show a very convenient property:

Lemma 2.4.

Following an admissible strategy , each investor is uniformly shielded from ruin in the sense that her investment returns satisfy

Proof.

Now, given the other investors’ strategies and their corresponding average wealth of (9), the th investor’s best response problem is to find a strategy which

| (11) |

subject to her wealth dynamics

| (12) |

Here, whenever there is no signal, the wealth process evolves depending on the agent’s zero signal position , while at times of a jump signal , the wealth process changes with respect to the signal-dependent position taken just for this moment. Recognizing the interdependence of the investors’ optimization problems through the geometric mean, we find that we are dealing with an -dimensional stochastic differential game which is best understood in terms of its Nash equilibria:

Definition 2.5.

A vector of admissible strategies is called a Nash equilibrium, if for each we have

| (13) |

So, as usual, a collection of strategies is called a Nash equilibrium if it is its own best response in the sense that each , solves (11) for . While finding such best responses for arbitrary peers’ strategies is a daunting task in general, it will turn out to be entirely feasible if they come from the following restricted class:

Definition 2.6.

Strategies are called (purely) signal-driven if each , , can be written in the form

| (14) |

for some -measurable time-independent and deterministic function . We denote by

the set of admissible signal-driven strategies for the th investor.

Definition 2.7.

A Nash equilibrium is called a signal-driven Nash equilibrium if it is signal-driven in the sense of Definition 2.6, i.e. if .

Note that either notion of Nash equilibrium presented here is of open-loop type, that is, the equilibrium strategies are best responses within a class of strategies written in terms of the system’s driving noise.

2.3. HJB equation and Best Response Map for The Multi-Agent Game

The main result of this section is a verification theorem for best response controls for an investor who interacts with investors employing signal-driven strategies. As we will see, the best response in the set of all admissible strategies is itself signal-driven, i.e., it comes from the smaller set .

This result will be obtained by dynamic programming techniques similar to the case with one investor solved in [BK22]. As in [LZ19], the key difference here is of course that each investor has to take into account her peers’ average mean wealth (9). When they pursue admissible, signal driven strategies , , we can use Itô’sformula to compute the dynamics of this average, which, conveniently, turns out to be an exponential Lévy process:

| (15) |

with dynamics given by

| (16) |

where

Bringing together the perspectives from [LZ19] and [BK22, pp.1312-1314], we can now derive the HJB equation for the best response problem (11). The corresponding value function is

Assuming to be smooth, we expect by Itô’s formula that, for any admissible strategy , the value process , , to have the dynamics:

where the superscript denotes the continuous part of a process. Inserting the respective dynamics (12) and (16), we get

where, is the compensated Poisson random measure .

Following the martingale optimality principle, we look for conditions such that the value process is a supermartingale for any admissible and a martingale for some (then) optimal . This leads us to the following HJB equation:

| (17) |

with boundary condition

To prepare the verification theorem for the HJB equation, we include the following auxiliary lemma.

Lemma 2.8.

For all , there exist -integrable functions and such that for all we have:

For all , for all

and, for all admissible signal-driven strategies ,

Proof.

With this result in place, we present the verification theorem for the best response problem and its proof:

Theorem 2.9.

Assume that our type assumption 2.3 holds and suppose investor ’s peers use admissible signal-driven strategies .

Then the value function of the th investor’s best response problem (11) is given by

| (18) |

where

| (19) |

is a finite constant. The function is indeed a smooth solution of the HJB equation (17) and the th investor’s best response control is unique and it is again an admissible signal-driven strategy : when receiving no signal, investor ’s best response to is holding in stock a fraction of total wealth

| (20) |

and, at moments when receiving a signal , changes this to a fraction of size

| (21) |

Proof.

(cf. [BK22, proof of Theorem 3.1]) Let us first argue that . For this, as by is a finite measure, we only need to show finiteness of the suprema in (19), for which we take a closer look at its integrands. Observe that for all , for all we have

| (22) |

Thus, both for and , the right-hand side exhibits a denominator which is uniformly bounded away from zero by Lemma 2.4, and a numerator which is bounded from above by a -integrable function, which does not depend on , by Lemma 2.8. Hence, both suprema in (19) are taken for continuous functions over compacts and thus are attained and finite.

Now, a simple calculation shows that as defined in (18) is a -solution of (17) and meets the initial condition for all . Note that satisfies for all , , by our convention (8).

Let us argue that, for fixed, , , is a supermartingale where solves the wealth dynamics (12) for some . For this, we show that is bounded from below, i.e. for some integrable . Indeed, for , the utility is bounded from below by zero. For , however, we ensure a uniform bound by showing that

| (23) |

for all . In fact, the mean wealth process is the product of independent stochastic exponentials and strictly positive and can be written in closed form as

| (24) |

for . Let and let us argue for one component after another: First, note that

does not involve any randomness and is trivially finite. Secondly, as the maximum Brownian motion has finite exponential moments, it is easy to see that

Hence, we are left to observe that

but, since the integral against the Poisson random measure admits almost surely finitely many jumps on any finite time interval, we only need to check whether the jumps have finite expectation with respect to and this immediately follows from Lemma 2.8.

Thus, (23) holds and together with having nonnegative drift, which follows from our arguments leading to the HJB equation, this implies that is a supermartingale. In particular, this allows us to observe

By sending , we even have

So the function on the right-hand side of (18) yields an upper bound for the value of investor ’s best response problem (11).

It remains to show that is a martingale for the wealth process given the strategy . Then, this strategy is optimal since we can conclude

We note that is signal-driven (and admissible) in the sense of Definition 2.6 and that the use of instead of is justified since the in both (20) and (21) are singletons. This follows immediately from the fact that the target functions are strictly concave in .

Further, our arguments leading to the HJB equation (17), show that has zero drift:

In particular, is the product of independent exponentials. The stochastic exponentials with respect to the Brownian motions are martingales, since , , and are constants, and the exponential with respect to the compensated compound Poisson process is a martingale, because (cf. [SAT99, Theorem 33.2])

is ensured to be finite by being finite. Thus, is a martingale and the proof is complete. ∎

2.4. Existence of a Nash Equilibrium

Having found the best response for a single investor interacting with peers employing signal-driven strategies, we are now in a position to demonstrate the existence of an equilibrium.

Theorem 2.10.

Under Assumption 2.3, there exists a signal-driven Nash equilibrium .

The proof is based on Schauder’s Fixed Point Theorem which requires a continuous self-mapping of a compact and convex domain. For our best response map above (20) and (21), these requirements are difficult to meet in general, but our Assumption makes this tractable: There are only finitely many distinct signals to account for and so the space of admissible signal-driven strategies can be identified with a vector

The set is compact and convex by construction and thus serves as the domain and image set of the desired fixed point mapping.

Proof.

A sufficient condition for a candidate to be a signal-driven Nash equilibrium is to satisfy , where is described in Theorem 2.9. Thus, the equilibrium is characterized by a fixed point of

Let us argue for continuity of . By Lemma 2.8, we can use dominated convergence to find that the target functions in both (20) and (21) are continuous in . Thus, by Berge’s Maximum Theorem (cf. [AB06, Theorem 17.31]), is upper-hemicontinuous in . In fact, since by strict concavity of our utility functions the operators in (20) and (21) always yield singletons, the maximizers are actually continuous functions. As a consequence, is indeed continuous in .

Finally, since is non-empty, compact and convex and is continuous, we can use Schauder’s Fixed Point Theorem, cf. [SCH30], to conclude that there exists with . ∎

In summary, we have demonstrated the existence of a signal-driven Nash equilibrium, which also qualifies as a Nash equilibrium within the broader class of admissible (not necessarily signal-driven) strategies. Let us emphasize that we neither claim uniqueness of such equilibria nor can we rule out existence of Nash equilibria involving strategies which are not signal-driven.

2.5. Common vs. Idiosyncratic Noise in Aggregate Wealth

An important question arises: how can this framework transition to a corresponding mean field game? This transition is particularly motivated by the fact that, in such a mean field setting a single individual’s actions do not impact the environment of others and, so, the signal-driven strategies that we are focussing on are an even more natural concept as the average wealth at the core of the interactions between agents cannot be influenced anymore by every single investor. One way to interpret the mean field setting is to consider it as the limit of the multi-agent game for the number of agents .

Before moving on to a rigorous formulation of the mean field game in Section 3 below, we provide an appetizer discussion and deliver a result on the limit of the average wealth for future reference.

Let us assume that the types of our investors are obtained from a corresponding sequence , ,… in generated by independently and identically distributed samples from a probability which describes the distribution of types among the population of investors. We denote a generic sample from by

and with some abuse of notation consider

Each investor is equipped with her own independent idiosyncratic Brownian motion ; the Brownian motion specifies common Brownian noise shared by all agents.

The specification of common and idiosyncratic jump noise is less obvious. A particular challenge in this context is the specification of a framework which allows for idiosyncratic signals on (partially) common price shocks, a key feature of our model, which, to the best of our knowledge, has not been addressed in the literature so far. Indeed, while jump times of the Poisson random measure should be common to all investors, it is important to address the question how the marks set by represent common and idiosyncratic noise. For instance, we want to allow for the possibility that each of our investors receives a signal on common impending price shocks which is affected by idiosyncratic noise. So, an investor may have a type that affords her warnings about impending price shocks with some probability . While the price shock may be common to all investors and the warning probability will be shared by her fellow investors of type , the actual heads-or-tails outcome of her idiosyncratic coin flip experiment for the shock warning may be independent from that of everyone else. The distinction between common and idiosyncratic noise becomes particularly crucial in the mean field framework. Here, idiosyncratic noise can be averaged out by a law of large numbers to yield a deterministic quantity while common noise persists as a random quantity affecting everyone.

To allow for a rigorous formalization of such settings with idosyncratic and common jump noise, let us consider the mark space as an infinite product space

for Polish spaces and identical with generic elements

The independent Poisson random measure with jump rate has intensity measure

where is a probability measure on and

generates independently for each investor identically distributed idiosyncratic noise marks, each with law on . In particular, this leads to jumps and signals with both common and idiosyncratic components for each investor via and where and are the jump and signal maps on for an investor of type .

Of course, the actual signals that each individual investor may, at the various mark times , receive are exposed to both the respective common mark and the investor specific mark . As a result, even investors of the same type may make differing investment decisions and figuring out the limiting geometric average wealth when their number goes to infinity has to account for this:

Lemma 2.11.

Suppose each investor follows a signal-driven strategy determined solely by her respective type , determined as i.i.d. sample from the type distribution . Moreover, suppose the following integrability assumptions hold:

and for

Then, as the number of investors converges to , the average wealth of each investor’s peers converges for all almost surely to

for

| (25) |

and

| (26) |

Proof.

For , , and consider from (15) for the specified noise structure:

By the law of large numbers, we immediately find

Similarly, we find convergence of

For the term aggregating the independent idiosyncratic Brownian motions , we find

For the term involving the common noise Brownian motion , we get the average

Lastly, for the jump term, we note that all investors have in common the mark times and the noise marks , while the are i.i.d. for with distribution . The law of large numbers thus yields the almost sure convergence

Putting everything together, we find the desired result. ∎

It is an intriguing question whether, when adding more and more investors in an i.i.d. fashion, the corresponding Nash equilbria also converge to a mean field equilibrium, whose definition we provide and existence we establish in the following Section 3. Moreover, one could ask whether the average wealth of investors employing equilibrium strategies in a multi-agent game converges to the average wealth in the mean field game under its equilibrium strategy. We have to leave these questions for future research. The main reason is that we cannot even prove uniqueness of equilibria; see Remark 3.14 where we discuss the pertaining difficulties.

3. The Mean Field Game

In this section we give a mean field formulation for interactive utility maximization with jump signals. Section 3.1 provides a model for the representative investor which leads to a canonical notion of mean field equilibrium in signal-driven strategies. Section 3.2 provides the best response function which maps a proposed signal-driven stragey used in the mean field environment to the representative investor’s best response. Section 3.3 then proves existence of a mean field equilibrium, preparing the ground for the numerical case studies carried out in the next Section 4.

3.1. The Representative Investor

Guided by the considerations of the average wealth in Section 2.5, let us assume that our representative investor’s type is determined by a probability on the type space

with its Borel -field . As this type choice should be independent from the other sources of randomness in our system, we pass from our original probability space supporting independent Brownian motions , along with an independent marked Poisson point process to

The processes , , are lifted to via the canonical projection .

Similarly, we consider the projection defined for a generic . The components of this projection implicitly define the population’s charateristics

as measurable mappings on . To emphasize their dependence on the type, we sometimes will denote , i.e. , where the latter is the initial wealth compoment stored in the type vector ; we proceed similarly for , , etc.

Idiosyncratic and common jump noise can be introduced in analogy to our setting in Section 2.5 except that we only need idiosyncratic and common noise for one representative investor. We thus consider a mark space in product form

with two Polish spaces , , equipped with their respective Borel--fields and . We write

as the product of two probability measures and scaled with the jump rate . Elements of will be generically denoted by and noise such as price shocks that commonly affect all investors will only depend on via its component; idiosyncratic noise resulting from a mark such as shock warnings will also depend on , a source of randomness that we will use to allow for individual noise in signals that should be thought of as independent between agents.

Let us also lift the information flows generated by the drivers. That is, denoting by the set of -negligible events, we have

Supplemented by the information generated by the type this gives us the full information filtration

Also, denote by the common noise filtration

An immediate, albeit fundamental consequence is that any -measurable random variable is actually -measurable and independent of , and under . Additionally,

are jointly measurable in their arguments.

As in the multi-agent game, investors will obtain information from their signal process. In the present mean field setting, we define the representative investor’s signal process as

Observe that this signal process is type-dependent as

In the following, we rely on the type-dependent disintegration of the jump intensity measure: For all , we have

| (27) |

where and are -measurable. This allows us to introduce

for all and .

By the same reasoning as in the multi-agent game, we obtain both the no-arbitrage condition

| (28) |

and the admissible positions ensuring non-negative wealth: In case when unsignaled jumps are possible, the default positions without signal can be chosen from

if , then all jumps are signaled and so . For a non-zero signal we have

We make the following standing assumption on the distribution of investor types.

Assumption 3.1.

The type distribution is such that

-

the stock prices are nonnegative, i.e. for -almost every ,

-

the no-arbitrage condition, i.e. , holds for -almost every ,

-

each investor type can receive only finitely many different signals, i.e. for -almost every , and

-

the market parameters and the risk aversion are bounded, i.e.

and the initial wealth allows for a finite geometric average

-

()

jump bounds are uniformly bounded away from zero: There exists such that for -almost every

-

if only finitely many distinct types can occur (i.e. if ), jump sizes have finite moments in the sense that

otherwise, we need uniform boundedness in the sense that

Let us review these assumptions. First of all, - are consistent with our assumptions in the multi-agent game, see Assumption 2.3. Further, will give us bounds on the geometric mean field wealth by ensuring that market parameters do not differ too much between different types of investors. It will hold immediately if distinguishes only finitely many types. Similarly, () will ensure ‘nice’ properties of the mean field jumps, as it yields uniform bounds for admissible positions of all investor types, see (i) in Lemma 3.8 below. This will be particularly important in the construction of a suitable fixed point mapping in our proof for existence of mean field equilibria, see Lemma 3.12. Lastly, ensures sufficient integrability of stock price jumps, a condition also needed in the multi-agent game.

Let us next define the set of admissible strategies for the representative investor. For this, we will again consider compact intervals included in for all , . However, to ensure measurability and uniformly nonnegative wealth, we specify the intervals to be of the following form: If is finitely supported, we let

for -measurable , . In case of infinitely many possible types, we consider

| (29) |

for all and for type-independent .

To prepare the application of the Measurable Maximum Theorem (cf. [AB06, Theorem 18.19]) let us record the following lemma:

Lemma 3.2.

The map is weakly -measurable in the sense of [AB06, Def. 18.1], that is, for all open subsets of , we have

Proof.

It suffices to show that for all we have

for . Thus, we get the desired measurability for both maps as soon as we have shown measurability of the interval bounds, that is, we need to show that each of the maps

is -measurable.

The argument for the other maps being similar, let us show that is -measurable. Noting that by Fubini-Tonelli

is -measurable since the integrand is jointly -measurable and positive, we can write as the pointwise limit of -measurable functions:

Thus, is -measurable. ∎

As before, admissible strategies are signal-dependent investment choices of the form

| (30) |

for some -measurable field . In the light of Meyer--fields, we consider strategies measurable with respect to The set of admissible strategies is

Although is very similar to the definition in the multi-agent game, here we insist on being a set of positions for the representative investor, not for an investor of a specific type.

Proposition 3.3.

Given an admissible strategy , the representative investor’s wealth process has dynamics

| (31) |

for and it remains uniformly bounded away from zero on -almost surely.

The proof of this uniform boundedness is an immediate consequence of the following result:

Lemma 3.4.

Independently from the strategy applied, the returns from jumps are uniformly bounded from below: There exists a constant such that for all :

Proof.

As in the multi-agent game, we will prove existence of equilibria for the special class of signal-driven strategies:

Definition 3.5.

An admissible strategy is called (purely) signal-driven if in (30) does not depend on and , that is, if it can be written in the form

| (32) |

for a -measurable time-independent function . We denote by

the set of admissible signal-driven strategies.

We will limit our search for (yet to be defined) mean field equilibria to signal-driven ones, following the same reasoning as in the multi-agent case. Also, we will, in preparation for our proof of existence of an equilibrium, solve a best response problem for the representative investor given a fixed environment. This environment is again described through the geometric mean wealth as induced by a signal-driven strategy which specifies each type’s signal-driven strategy . Indeed, denoting by the expected value over the product space with respect to , we define the average wealth in the mean field setting as

In light of our considerations for the limiting average wealth with infinitely many agents in Section 2.5, our next result shows that this is consistent with our initial derivation of average wealth in Lemma 2.11:

Lemma 3.6.

Proof.

Let . We note that

where the second equality holds because is independent of and . By Itô’s formula, we easily find that

where, since is signal-driven, the strategies do not depend on and but on the signal. In particular, is -measurable for . This is important, as in the following, we take conditional expectation with respect to the common noise and then apply the exponential:

First, for the initial value, we find that

because , being -measurable, is independent from the common noise. Similarly, for the drift term, we exploit that the lifted common noise drivers and actually only depend on , while the market parameters and only depend on the type , thus, the -integrand averages to

Further, since , and are independent from the common noise drivers, we find that when taking conditional expectation with respect to the -term vanishes as a martingale with zero expectation. However, for the -term, randomness remains in the types of the integrand, that is

for

Finally, for the Poisson integral, we have to average over the types and the idiosyncratic jump marks, that is

for the mark times and common and idiosyncratic jump marks , , set by the Poisson random measure . Together with (26) and taking the exponential, we find (33) which coincides with the limit from Lemma 2.11. ∎

As we will see soon, the above geometric mean field wealth works as a sufficient statistic of the control’s environment enabling us to bypass the so-called master equation when considering best responses.

Let us fix some . The geometric mean wealth is defined as . Then, the representative investor’s best response problem is to

subject to her wealth process from (31). Here, is the utility function dependent on the type , which almost surely behaves as the utility defined in (7), i.e.

Ultimately, an equilibrium strategy aligns an agent’s best response with the environment generated by that same strategy. The consistency condition that characterizes a mean-field equilibrium requires that the best response

to the geometric mean wealth induced by satisfies

This consistency requirement is central to our definition of a mean-field equilibrium.

Definition 3.7.

Let be an admissible strategy and consider , where is the wealth process corresponding to . We say that is a mean field equilibrium if

| (34) |

A mean field equilibrium is called signal-driven if is signal-driven in the sense of Definition 3.5.

As mentioned, we first solve the best response problem of the representative investor.

3.2. HJB equation and Best Response Map for The Mean Field Game

Let describe the investment decisions made in the mean field and consider the resulting geometric mean wealth from (33).

The following lemma collects some technical results ensuring, in particular, that the mean wealth behaves ‘nicely’.

Lemma 3.8.

We find that

-

(i)

signal-driven investment positions are uniformly bounded: There exists a constant such that for all and for -almost every

-

(ii)

there exists a constant such that for all ,

-

(iii)

for all there exists a -integrable function such that for all , we have

Further, from (ii) and (iii) it follows that for -almost every , for all and any there exists a -integrable function such that for all we have

| (iv) |

Note that, by (ii), the mean wealth dynamics in (33) remain strictly positive. Also, (i) together with , ensures that is finite and is uniformly bounded with respect to independent from the choice of . Further, (iii) and (iv) ensure finiteness of the suprema of the HJB equation below, see (38), as well as sufficient continuity of the target funtions of the best response maps, see (41) and (42), and, later, also continuity of the fixed point maps in the proof of existence of mean field equilibria.

Proof.

Let . For (i), it is straightforward that () bounds signal-driven investment positions uniformly in types and signals independently from as

For (ii), it suffices to show that there exists independent from such that for all , we have that

because then the exponential is uniformly bounded away from zero on ; and indeed, this follows immediately from Lemma 3.4.

Returning to our initial goal, for given , we search the best response determined by the problem to

| (35) |

To make this problem amenable to dynamic programming we write

and introduce the value function for the representative investor’s problem when she is of type :

| (36) |

Here we use the type-dependent set of admissible strategies

where the filtration on is induced by the completions of

and for the resulting wealth dynamics:

| (37) |

We will later also consider the type-dependent set of signal-driven admissible strategies which we define to be

| for some |

Using the wealth dynamics (33) and (37), we can follow the same heuristics as in the multi-agent game to derive the corresponding HJB equation:

| (38) |

together with the boundary condition

and where, for simplicity of notation, we write for , cf. (26). Moreover, we provide the following verification result:

Lemma 3.9.

Fix . Then, for -almost every , the value function of (36) is given by

| (39) |

for the finite constant

| (40) |

Moreover, the value function is indeed a smooth solution of the HJB equation (38) and the best response control is again a signal-driven strategy : at times without a signal, i.e., when , it is given by the default investment

| (41) |

and, at moments when receiving a signal , it is best to invest the fraction

| (42) |

This lemma closely resembles the corresponding result, Theorem 2.9, in the multi-agent game. Consequently, the proof requires only minor adaptations to account for the different mean wealth. For sake of brevity, we omit it here and confine ourselves to pointing the reader to our standing Assumption 3.1 and Lemma 3.8 which give us all the tools to argue exactly as in the proof of Theorem 2.9.

Having thus found the best responses of each type of agent, we can now piece these together to find the best response control of our representative agent and thus solve her best response problem (35):

Theorem 3.10.

Proof.

For given , we need to show that the strategy given by (41) and (42) maximizes

over all on . By Lemma 3.9, for any , it holds that

| (43) |

Defining for with given by (41) and (42), we find that indeed attains the upper bound in (43) as soon as we have shown that is a -measurable field. Since, by , there are only finitely many signals for each type, it sufficies to ensure measurable dependence of (41) and (42) on . For this, note that the target functions in (41) and (42) are Carathéodory functions: they are continuous in by dominated convergence using Lemma 3.8 (iv), and as functions of they are -measurable. Together with Lemma 3.2 this allows us to apply [AB06, Theorem 18.19] to show that the unique maximizers are indeed -measurable. In conclusion, is an admissible signal-driven strategy and the best response control to in the sense of (35). ∎

3.3. Existence of a Mean Field Equilibrium

Similarly to the multi-agent game, the main task now is to define appropriate domain and image sets which ensure that Schauder’s Fixed Point Theorem can be applied to a suitable fixed point mapping. However, here, instead of finitely many investors, we will rely on a restriction to finitely many types of investors, or on a restriction to finitely many different common noise marks, i.e. . Consequently, we will provide two existence results, the first of which treats the setting of finitely many types:

Theorem 3.11.

Under Assumption 3.1, there exists a signal-driven mean field equilibrium if .

Proof.

We need to find which coincides with its best response, i.e. which satisfies , where is the optimal best control from Theorem 3.10 corresponding to . In fact, we, then, have that the consistency condition for the mean field equilibrium

holds.

This fixed point problem can be reformulated as follows. Let us recall that is finite by assumption and that each type can receive only finitely many distinct signals due to assumption . Therefore, the set of admissible signal-driven strategies can be identified with the compact, convex and non-empty set

This is the domain and image set of the fixed-point mapping

Let us show continuity of . For this, first, we observe that, by Lemma 3.8(i) together with and Lemma 3.8(iii), both and are continuous on , for each . Secondly, Lemma 3.8 (iv) allows us by dominated convergence to deduce that the target functions of the best response control in (41) and (42) are continuous in . Thus, by Berge’s Maximum Theorem (cf. [AB06, Theorem 17.31]) the maximizers (41) and (42) are upper-hemicontinuous in . Since these -sets are actually singletons, the maximizers are continuously depending on . As a consequence, is indeed continuous on .

Finally, since is non-empty, compact and convex and is a continuous function, there exists such that by Schauder’s Fixed Point Theorem, cf. [SCH30]. ∎

Note that the previous proof uses the assumption in an essential way to conclude continuity of the fixed-point mapping on a compact set. Indeed, when , defining an appropriate domain and image set for such a fixed-point mapping becomes a more delicate task as we can no longer rely on a finite-dimensional representation of the representative investor’s strategy. In the following we propose a way to circumvent this technical issue by assuming that there are only finitely many common noise marks. Indeed, under this assumption, the next lemma provides existence of a suitable fixed point mapping.

Lemma 3.12.

Suppose and . Then, there exists a constant such that for all , -almost every and -almost every , we have

| (44) |

Moreover, there exist a non-empty convex and compact with the following properties:

-

(i)

For all , we have

-

(ii)

Every , yields an admissible signal-driven strategy where -a.e. type will invest a fraction

(45) of wealth in the stock when observing a signal .

In particular,

| (46) |

yields a mapping .

Proof.

First, we show (44). For this, let , and . We find that, on , the -term is negative but uniformly bounded from below by Lemma 3.4. For the complementary case, i.e., on , the -term is positive and we find

where both factors on the right-hand side are uniformly bounded by Lemma 3.8 (i) and (read for the present case ).

For the the existence of , we have that is bounded on independently from the choice of by Lemma 3.8 (i) together with . Also, for the mean jumps, Lemma 3.8(ii) provides the lower and (44) the upper bound, that is, we immediately, find that for all for all . Putting everything together, this ensures existence of .

Now, we are ready to prove the existence of a mean field equilibrium when there are not necessarily finitely many types.

Theorem 3.13.

Under Assumption 3.1, there exists a signal-driven mean field equilibrium if and .

Proof.

Let us show that the self-map from (46) is continuous on . First, we show continuity of

for all , for -almost every . By Lemma 3.8 (iv) and dominated convergence, the target functions of the argmax-operators of from (45) are continuous in . Then, by Berge’s Maximum Theorem (cf. [AB06, Theorem 17.31]) the -operators are upper-hemicontinuous in . As these -sets are actually singletons, the maximizers in (45) are given by functions which are continuous in , for all and for -almost every .

Secondly, recalling that

| (47) |

for all , we find that the continuous dependence on carries over because both integrands are uniformly bounded by Lemma 3.8(i), and (44), allowing us to apply dominated convergence. Thus, is continuous on .

As a consequence, is a continuous self-map on . Since is a non-empty compact and convex set, Schauder’s Fixed Point Theorem [SCH30] gives existence of a fixed point for . ∎

Remark 3.14 (Uniqueness of Equilibria).

The uniqueness of the found signal-driven equilibria in the above multi-agent and mean-field games remains an open question. In [LZ19], the authors prove the uniqueness within the class of constant equilibria for which they can rely on explicit best response controls in this very small class. We, however, consider merely signal-wise constant equilibrium strategies, for which the best response controls are given by one-dimensional concave optimization problems. Here, even in case of submodular utility, i.e. with , uniqueness of the found equilibria seems far from straightforward to prove, at least to us.

This lack of uniqueness in equilibrium strategies prevents us from making any convergence statements based on these strategies and their aggregate wealth. Nevertheless, we note that our numerical experiments suggest uniqueness of the identified equilibrium. Indeed, in all our simulations, the fixed-point iteration always converged to the same equilibrium, irrespective of the randomly chosen strategies by which we started the iteration. This observation provides numerical evidence for uniqueness inside the restricted signal-driven class. It does not reveal anything about the existence or non-existence of equilibria involving non-signal driven strategies.

4. Case Studies and Financial-Economic Discussion

Equilibrium strategies are not available in explicit form, making equilibrium behavior difficult to characterize. Therefore, we turn to case studies and numerical methods to analyze how strategic interactions shape investor welfare and risk perception and to address questions like how much we should care about what others know.

In the following case studies, we will examine scenarios where investors differ in signal quantity, signal quality, and competitiveness. By systematically varying these parameters, we will identify how they impact the certainty equivalent assessing the investors’ happiness and perceived risk. Our findings reveal when and why investors prefer certain competitive dynamics, whether they benefit from informational advantages or even favor better informed peers.

Our discussion focuses exclusively on mean field games for three reasons. First, we prefer scenarios where the influence of an individual on relative wealth is negligible and interactions are between the different types of players within the population. Secondly, and consequently, when individual decisions do not affect others, mean field games yield a more compelling framework than multi-agent games for our focus on (comparably simple) time-independent, signal-driven strategies. Finally, mean field games significantly reduce dimensionalty, simplifying the analysis and interpretation of investor behavior in large populations.

4.1. A Single Stock Model with Two Investor Types Receiving Different Signals

For simplicity, we consider mean field games with two different types of investors trading in a single common stock subject to log-normal price shocks, that is, the parameters and do not vary with the type but are fixed. The proportions of types are given by , with . We put and , and denote by a generic element in which accounts for the independent idiosyncratic noise. Then, we specify the jump intensity measures

where denotes the standard normal distribution and the uniform distribution on . We define the common log-normal jumps as

for additional common market parameters , . Note that .

The idiosyncratic noise enters through the individual signals our agents receive. Each type of investor receives, in case of an imminent jump in the stock price, a non-zero signal with an individual probability denoted by . Such a non-zero signal will be a categorical indication about the sign and the size of a idiosyncratically noisy version of the impending common price shock .

Specifically, we consider a perturbed version of this price shock

where determines the signal quality for an investor of type . Since, our existence theorems only work with finitely many distinct signals, we cannot use this to define Type ’s signal map . Instead, we ensure for by categorizing the perturbed jump mark as “small”, “medium”, or “large” in absolute size and give an indication of the direction. Specifically, we put:

Thus, for both types the signal range is . Still, signals may differ both in their frequency as parametrized by the probability of signal reception and in their quality as determined by the perturbation parameter . Figure 1 and Figure 2 ilustrate this choice of jump signals.

Specifying the following intervals of integration given a signal

we find the disintegration of for type to result in the signal frequency

and, for a signal , we find the a posteriori distribution for the jump marks to be

We impose that the probability of receiving a signal in case of a jump satisfies and, hence, find that for all .

In the remaining part of this paragraph, we explain how to efficiently compute the optimal investment positions for an investor of type . Readers may skip this section at first reading, and instead proceed directly to the numerical results and their discussion in Subsection 4.2.

For a signal-based strategy , we recall that the representative investor’s best reponse will be to invest a fraction

when not receiving a signal. We can explicitly compute

and

| (48) |

Note that, given , a non-zero signal allows one to deduce that the mark part has to be in the interval

Hence, the integrals in (48) simplify:

which is easily computed using the cummulative distribution function of the standard normal distribution.

Similarly, we can compute the components of the best response to when receiving a non-zero signal :

4.2. Numerical experiments

For all our experiments, we will consider the two types of investors to be of the same size in our population, i.e., , and to have the same risk aversion . Further, we choose the market parameters to be

and the time horizon for investments is .

We investigate how the presence of investment signals impacts investors with relative performance concerns. For this, we consider investors of type as a reference point and investigate how they assess their prospects when investors of type are receiving more/less accurate or more/less frequent signals. To compare the outcomes of the different equilibria, let us introduce a suitable kind of certainty equivalent. The reference point for this certainty equivalent is in each case an equilibrium for the fully homogeneous reference type environment

We, then, let the characteristics of the investors of type deviate from those in the reference scenario, that is, we consider an alternative type environment

for various choices of , and .

For both enviroments we compute the equilibrium strategies by numerical fixed point iterations. That is, we iteratively evaluate the best response controls from Section 4.1 using numerical integration and optimization methods until the iterations only yield negligible changes. The expected utilities for Type investors will typically differ between these equilibria. We then determine the certainty equivalent as the initial capital that an investor of type would need in the reference setting to achieve the same expected utility there as in the alternative setting :

for and as in (40) for corresponding type spaces and and equilibrium strategies and , respectively.

Below, we present our results. For ease of presentation, we will sometimes refer to investors of type as Type and to investors of type as Type . Also, whenever it is clear, we will drop the superscripts ‘ref’ and ‘alt’. Lastly, let us note that the lack of smoothness in some plots, notably in Figure 4, results from numerical approximation errors. The issue in these approximations arises from the computation of the integrals in the target functions of the best response strategies, which involve numerically delicate “spiky” integrands.

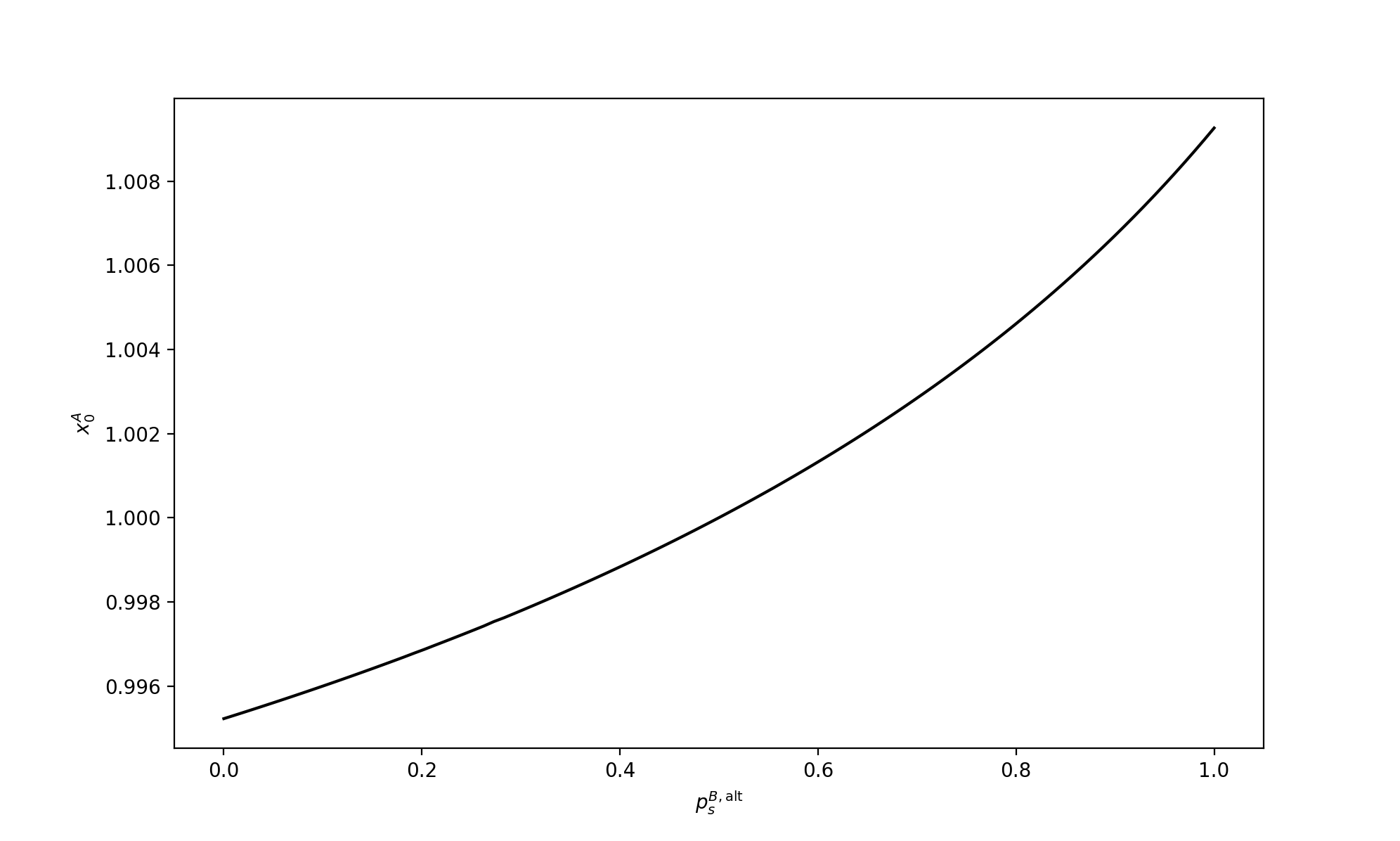

Better-Warned Peer Lowers Risk Exposures. Figure 3 describes how the certainty equivalent changes as the probability for Type to receive a signal increases, the other parameters being kept fixed at their values in the reference setting. We find that the certainty equivalent increases with , indicating that investors of type become happier when Type is warned about price shocks more often.

More precisely, Type investors find themselves confronted with competitive peers of Type who, when warned less frequently, will have to take more risk in order to still catch up with the advantaged Type investors. As a consequence, the average wealth fluctuates more. These stronger fluctuations carry over to the relative performance of Type investors whose risk aversion, then, makes them attribute a lower certainty equivalent value to such environments. Conversely, when Type is receiving more fequent signals, the added security that this affords also to Type translates into higher certainty equivalents for the latter, even if it is harder for them to catch up with their peers under these circumstances.

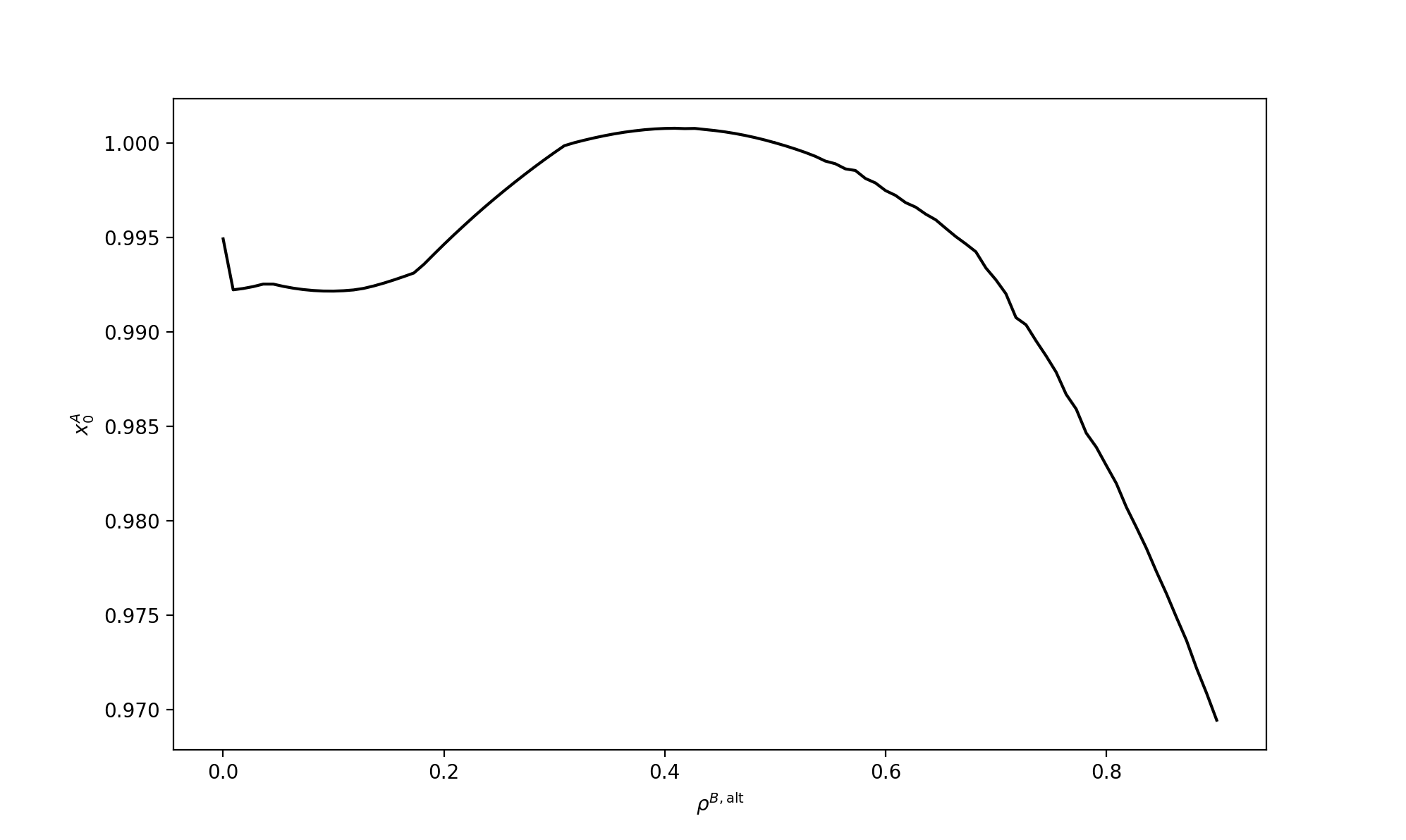

How much should we care about what others know? Figure 4 describes how Type investors feel about their peers receiving more or less reliable signals when their signal frequency and concern for others is kept at the level in the reference equilibirium.

It reveals that they like a largely homogeneous signal quality, with the peak at revealing a slight preference for being blessed with a signal that is just a bit more reliable than that of the competition. When Type peers receive more reliable signals, Type finds it much harder to compete in wealth generation leading to a drop in the certainty equivalent for . The drop when falls below is explained by Type ’s risk aversion: here, Type investors know that they have some catching up to do and thus take more risky positions, making also the relative performance of Type investors more risky. When, however, their signal becomes too unreliable () the risk aversion of type investors makes them refrain from such aggressive positions in the stock market. This makes Type ’s relative performance less volatile again, leading to the certainty equivalent’s increase close to . In short: we should care a lot about the others’ knowledge if that knowledge is not as reliable as our own—and it does not matter whether our peers’ knowledge is significantly more or less reliable!

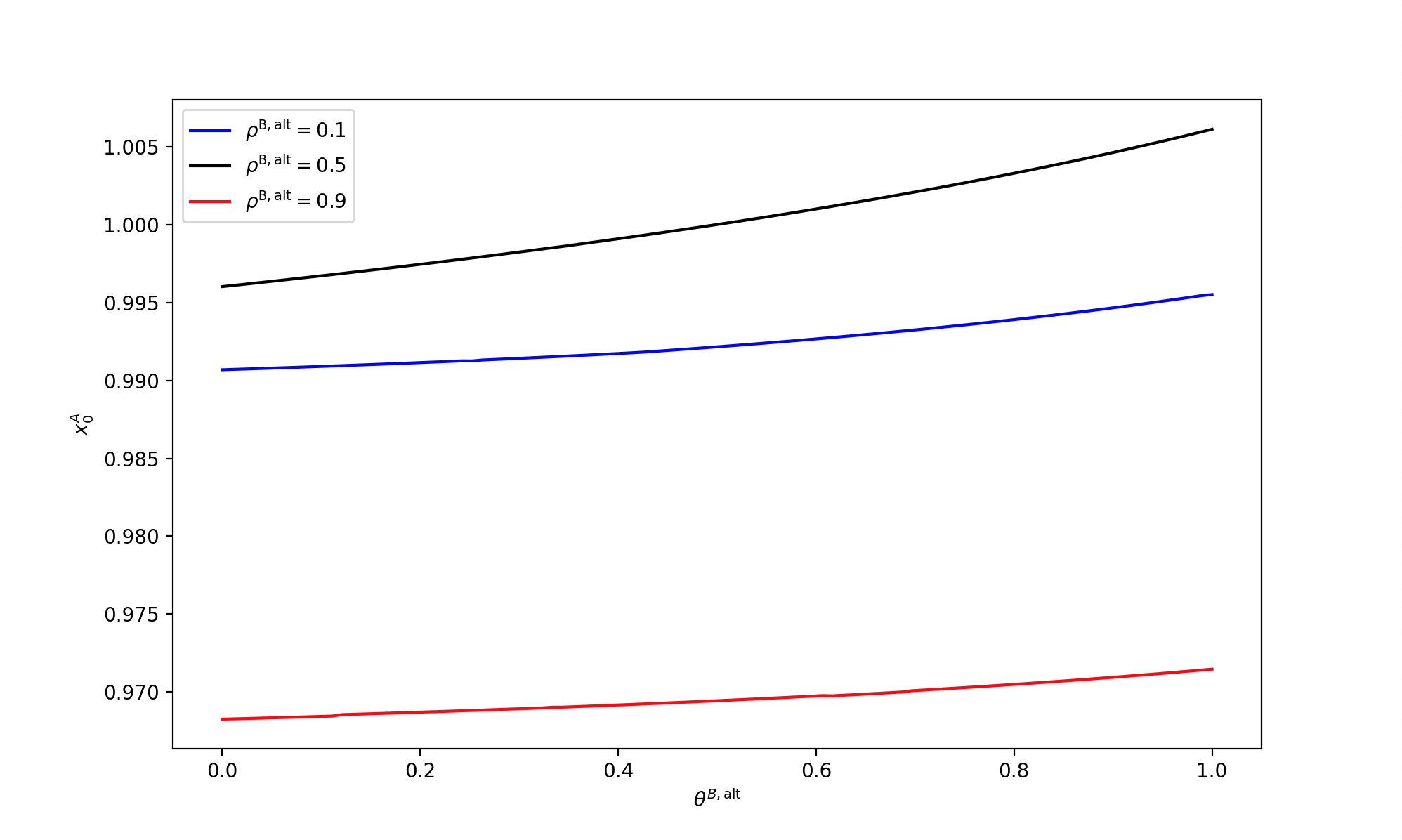

Furthermore, it is not just what others know that matters, but also how fiercely they act on that knowledge. The level of competitiveness among peers affects risk exposure and, consequently, the certainty equivalent. This dynamic is explored in the next two plots.

Increased Competitiveness Aligns Investor Objectives. Figure 5 shows that investors of type always prefer an increase in the competitiveness of investors of type . This preference persists regardless of whether Type ’s signal frequency is lower (), higher (), or at the same level (). This preference arises because the more competitive investors of type are the more they strive to reduce fluctuations in relative mean wealth, which aligns with the objective of (also) risk-averse investors of Type .

Moreover, as in Figure 3, Type investors prefer an environment where Type is warned more frequently than they are, even if this means that they are operating at a disadvanage.

Additionally, the effect of increasing competitivness on investors’ happiness is more pronounced when Type is stronger in signal quantity. Since Figure 3 already shows that investors of Type prefer better-warned peers, the combination of increased signal quantity and competitiveness further reinforces this preference. A better-informed and more competitive Type takes proactive investment positions that reduce the fluctuations in relative wealth, very much to the pleasure of risk-averse Type investors.

Preferences for Homogeneous over Heterogeneous Information. Figure 6 considers the same situation as Figure 5 but focusses on advantages and disadvantages in signal quality. Again, Type prefers an increase in the competitiveness of Type . However, in contrast to Figure 5, Type favors having an advantage in signal quality over being disadvantaged and, perhaps unexpectedly, prefers equal signal quality over holding an advantage. Knowing about their disadvantage, highly competitive Type investors have strong incentives to compensate for their inferior signals by adopting more aggressive investment positions, increasing their wealth fluctuations and thus also the relative performance of their peers. In contrast, when signal quality is homogeneous, both investors react similarly to new information, fostering a more stable environment. As a result, Type prefers equal signal quality over an advantage, not because an informational edge is inherently undesirable, but because the volatility created by a disadvantaged but aggressive competitor outweighs the benefits of superior information.

Still, we note that the curves in Figure 6 are less steep compared to Figure 5, suggesting that the impact of increasing competitiveness is weaker when differences in signal quality, rather than quantity, drive the competition. This aligns with the earlier findings: disparities in signal quantity affect more directly how often investors adjust their positions, leading to larger shifts in market dynamics. While differences in signal quality introduce instability, they do so less forcefully, making competitiveness a less dominant factor in shaping investor preferences.

References

- [ABE90] (1990) Asset Prices under Habit Formation and Catching up with the Joneses. The American Economic Review 80 (2), pp. 38–42. Cited by: §1.

- [AB06] (2006) Infinite Dimensional Analysis: a Hitchhiker’s Guide. Springer, Berlin; London. Cited by: §2.4, §3.1, §3.2, §3.3, §3.3, Lemma 3.2.

- [BB19] (2019) On Lenglart’s Theory of Meyer--fields and El Karoui’s Theory of Optimal Stopping. arXiv e-prints. Cited by: §1, §2.1.

- [BK22] (2022) Merton’s Optimal Investment Problem with Jump Signals. SIAM Journal on Financial Mathematics 13 (4), pp. 1302–1325. Cited by: §1, §1, §1, §2.1, §2.1, §2.1, §2.3, §2.3, §2.3, Proposition 2.1, Remark 2.2.

- [BM13] (2013-04) Competition among Portfolio Managers and Asset Specialization. Working Papers Technical Report w0194, New Economic School (NES). External Links: Link, Document Cited by: §1.

- [BG23] (2023) Nash equilibria for relative investors via no-arbitrage arguments. Mathematical Methods of Operations Research 97 (1), pp. 1–23. Cited by: §1.

- [BH24] (2024) Common noise by random measures: mean-field equilibria for competitive investment and hedging. External Links: 2408.01175 Cited by: §1.

- [BFY13] (2013) Mean field games and mean field type control theory. SpringerBriefs in Mathematics, Springer New York. Cited by: §1.

- [BLd17] (2017) Equilibrium pricing under relative performance concerns. SIAM Journal on Financial Mathematics 8 (1), pp. 435–482. Cited by: §1, §1.

- [BWY24a] (2024) A mean field game approach to equilibrium consumption under external habit formation. Stochastic Processes and their Applications 178, pp. 104461. Cited by: §1.

- [BWY24b] (2024) Mean field game of optimal relative investment with jump risk. Science China Mathematics 67 (5), pp. 1159–1188. Cited by: §1.

- [CDL+19] (2019) The master equation and the convergence problem in mean field games: (ams-201). Vol. 2, Princeton University Press. Cited by: §1.

- [CD18] (2018) Probabilistic Theory of Mean Field Games with Applications I-II. Springer. Cited by: §1.

- [CM99] (1999) Home Bias at Home: Local Equity Preference in Domestic Portfolios. The Journal of Finance 54 (6), pp. 2045–2073. Cited by: §1.

- [DKK08] (2008) Relative Wealth Concerns and Financial Bubbles. The Review of Financial Studies 21 (1), pp. 19–50. Cited by: §1.

- [dP22] (2022) Forward utility and market adjustments in relative investment-consumption games of many players. SIAM Journal on Financial Mathematics 13 (3), pp. 844–876. Cited by: §1.

- [ET15] (2015) Optimal Investment under Relative Performance Concerns. Mathematical Finance 25 (2), pp. 221–257. Cited by: §1, §1.

- [Fd11] (2011-04) A Financial Market with Interacting Investors: Does an Equilibrium Exist?. Mathematics and Financial Economics, pp. 161–182. Cited by: §1.

- [FZ23] (2023) Mean field portfolio games. Finance and Stochastics 27, pp. 189–231. Cited by: §1.

- [GAL94] (1994) Keeping up with the joneses: consumption externalities, portfolio choice, and asset prices. Journal of Money, Credit and Banking 26 (1), pp. 1–8. Cited by: §2.2.