Newton Methods in Generalized Nash Equilibrium Problems with Applications to Game-Theoretic Model Predictive Control

Abstract

We prove input-to-state stability (ISS) of perturbed Newton-type methods for generalized equations arising from Nash equilibrium (NE) and generalized NE (GNE) problems. This ISS property allows the use of inexact computations in equilibrium-seeking to enable fast solution tracking in dynamic systems such as in model predictive control (MPC). For NE problems, we address the local convergence of perturbed Josephy-Newton methods from the variational inequality (VI) stability analysis, and establish the ISS result under less restrictive regularity conditions compared to the existing results established for nonlinear optimization. Agent-distributed algorithms are also developed. For GNE problems, since they cannot be reduced to VI problems in general, we use semismooth Newton methods to solve the semismooth equations arising from the Karush-Kuhn-Tucker (KKT) systems of the GNE problem and establish the ISS result under a quasi-regularity condition. To illustrate the use of the ISS in dynamic systems, applications to constrained game-theoretic MPC (CG-MPC) are studied with time-distributed solution-tracking for real-time implementation. Boundness of tracking errors is proven. Numerical examples are reported.

I Introduction

A Nash equilibrium (NE) problem [15] concerns solving interdependent optimization problems subject to independent agents’ constraints:

| (1a) | ||||

| (1b) | ||||

where represents the agent, is the feasible set of agent , and is the cost function of agent . When agents have coupled constraints, a generalized NE (GNE) problem [9] is composed as:

| (2a) | ||||

| (2b) | ||||

where depends on , leading to coupled (rather than independent) agents’ constraints.

Similar to nonlinear optimization problems, the stationary conditions for the NE and GNE problems can be expressed as a generalized equation using normal cone mapping [6]:

| (3) |

where is a function, is a set-valued mapping acting between Banach spaces, and could be either the decision variable or the primal-dual variable from the Karush-Kuhn-Tucker (KKT) conditions [6] depending on the setting of the problem. One way of solving the generalized equation (3) is to use Newton-type methods [10], e.g., Josephy-Newton method [13] if is continuously Fréchet differentiable [10]. The Josephy-Newton method extends the classical Newton’s method for solving equations to more general variational problems (3) with the iterations of the form:

| (4) |

where is the number of iterations with being a given starting point, and is the gradient of . Local convergence of this Josephy-Newton method for nonlinear optimization problems has been established in the literature [4], and most of them are based on metric regularity conditions requiring that is strongly regular or strongly subregular [4, 2, 3, 5]. We show in this paper that similar properties can be established for generalized equations arising from NE problems (1) and that the local convergence can be achieved under relaxed regularity conditions (specifically, regularity but not strong regularity) via variational inequality (VI) stability analysis. Agent-distributed Josephy-Newton methods where each agent performs local computations for its own decision variable updates are also developed.

Perturbed Newton-type methods [2], where the perturbations may come from an inexact evaluation of the gradient or a nonzero reminder in solving (4), play a critical role when analyzing the interconnection between the optimizer and a dynamic system the controller of which requires solving consecutive optimization problems such as in model predictive control (MPC) [14]. For these systems, the input-to-state stability (ISS) of the perturbed Newton method is the key property to ensure trackable optimizer performance and closed-loop system properties such as stability, robustness, and constraint satisfaction. In a recent study [2], the ISS of perturbed Newton methods for nonlinear optimization was established under the strong regularity assumption. In this paper, we extend such results to the NE and GNE problems and show that the ISS holds under relaxed regularity conditions.

Note that for a GNE problem, its first-order necessary conditions do not reduce to a VI problem due to the coupled agents’ constraints; instead, they lead to a quasi-VI (QVI) problem [9], the solution to which is not well understood yet. By using complementarity functions, the stationary conditions from coupled KKT systems can be reformulated as a system of nonsmooth equations, which could be solved by semismooth Newton methods [8]. However, because the conventional VI stability analysis is not applicable (unless a variational-GNE (v-GNE) problem), it has been an open question whether the ISS holds for the perturbed semismooth Newton methods arising from the GNE problems. We answer this question by proving the ISS under suitable nonsingularity conditions with proven -quadratic local convergence.

To illustrate the role of the ISS in closed-loop dynamic systems, we study constrained game-theoretic MPC (CG-MPC) problems [20]. The CG-MPC concerns solving consecutive NE or GNE problems along the state trajectory, which is computationally demanding in general. One way to reduce the computational load is to employ the time-distributed optimization (TDO) strategy by distributing the optimizer iterations over time to track approximate solutions of the optimal control problem at each time instant [14]. With such an implementation strategy, the solver itself becomes a dynamic system evolving in parallel with the plant, resulting in an interconnected plant-optimizer feedback system. We show in this paper that the appealing properties of the TDO-based MPC, including the closed-loop stability and robustness [14], also hold in the CG-MPC problem with the Newton-type methods developed in this paper.

Notation. We use , , and to denote the set of real, non-negative real, and positive real numbers respectively, and to denote the set of non-negative and positive integers respectively, to denote the Euclidean norm, and to denote the infinity norm.

II Newton Methods for NE Problems

Consider the NE problem (1). We use to represent the game, where and . Let represent the set of all players’ decision variables with being the set of all other agents except for agent . Note that although (1) involves constrained optimization, it is a NE (rather than a GNE) problem because does not depend on . If solves (1) for all , i.e.,

| (5) |

holds for all , then is a NE.

We make the following assumptions throughout this section.

A1. (Smoothness): For every , the cost function is twice continuously differentiable in its arguments, and its second-order derivatives are Lipschitz continuous;

A2. (Player-wise convexity): For every and every , the cost function is convex, and the set is compact and convex.

Under A1 and A2, the problem (1) is guranteed to be solvable [18], i.e., a NE always exists. The following theorem shows that under A1 and A2, the NE problem (1) is equivalent to a VI problem.

Theorem 1 (Corollary 3.4 in [9]).

By Theorem 1, is a NE if and only if it solves the following generalized equation:

| (7) |

where is the normal cone to at .

Denote the game Hessian for (1) as

| (8) |

Remark 1.

Denote the critical cone of agent ’s optimization problem when (i.e., problem (5)) as

| (9) |

where denotes the tangent cone of the set at a point , and denotes the orthogonal complement of the gradient . Denote as the critical cone of the game.

The game Hessian is strictly semicopositive on the cone if for every nonzero vector ,

| (10) |

where . This strictly semicopositive property is important in the NE local uniqueness and stability analysis as discussed in the next subsection.

II-A Stability of NE

In terms of the stability of an NE of the game , we are interested in (i) when is an isolated (i.e., locally unique) NE, and (ii) whether the “nearby games” of always have a NE that is “close” to .

To start with, let us first define the isolatedness of a NE . This property is desirable for showing that this is indeed an “attractor” of all NEs of “nearby games”, and it is central to the local convergence analysis of Newton-type methods.

Definition 1.

A NE of the game is said to be locally unique, or isolated, if there exists a neighborhood of such that

| (11) |

where is the set of NEs of the game .

The next theorem establishes the conditions under which is an isolated NE of the game .

Theorem 2 (Proposition 12.14 in [11]).

Let A1 and A2 hold. Let be a NE of the game (1). If is strictly semicopositive on the critical cone , then is an isolated NE.

Next, to be able to define NE stability, we first formally define “nearby games” of a given game restricted to a subset of , by introducing a game neighborhood concept.

Definition 2.

Given a game satisfying A1 and A2, a game is said to be in the -neighborhood of restricted to , denoted by , if satisfies A1 and A2 and their pseudogradients satisfy

| (12) |

where is the pseudogradient of the game .

Definition 3.

A NE of the game is said to be stable if for every open neighborhood of satisfying (11) and for every , where is the closure of ,

| (13) |

and, in addition, there exists two positive scalars and such that, for every and every ,

| (14) |

where is the difference function of the pseudogradients of the two games.

Definition 3 states that a NE of a game is stable if (i) its nearby games are locally solvable (i.e., (13)), and (ii) the distance between the NE of the given game and that of a nearby game yields an upper bound in terms of the maximum deviation of the pseudogradients of the two games (i.e., (14)). This stability concept corresponds to the regularity condition in VI problems [10, Definition 5.3.2]. The following theorem establishes the stability result. The proofs of these and other results are in the Appendix.

Theorem 3.

Let be a NE of the game . If A1 and A2 hold and if is strictly semicopositive on the critical cone , then is a stable NE.

II-B Josephy-Newton method

We consider the Josephy-Newton method to solve the generalized equation (7). Specifically, given , one solves the following semi-linearized generalized equation to find :

| (15) |

where is the game Hessian (8) evaluated at , and is the linearization of the pseudogradient at .

The next theorem shows that the sequence , generated by (15), converges -quadratically to .

Theorem 4.

Let be a stable NE of the game and be its pseudogradient. There exists a such that for every , where is the open ball with center at and radius , the Josephy-Newton update (15) generates a well-defined sequence in , and every such sequence converges -quadratically to .

Remark 2.

Compared to the Josephy-Newton method for nonlinear optimization [2], here we do not require to be strongly regular at . Instead, we only require to be stable (but not strongly stable). Note that since may not be strongly stable, the sequence satisfying (15) may not be unique, but every such sequence converges to -quadratically. In addition, we do not require any constraint qualification conditions here. In fact, the feasible set may not necessarily be representable by a finite number of equality and inequality constraints. If is indeed a finitely representable set, then the strict semicopositive condition in Theorems 2-3 may be replaced by a weaker condition while ensuring the stability of [10, Section 5.3.1].

II-C Perturbed Josephy-Newton method

Now we consider a perturbed version of the Josephy-Newton method:

| (16) |

where , , and is a disturbance sequence that could model the inexact evaluation of the pseudogradient or a nonzero reminder in solving (7). Assume that , and and are both uniformly Lipschitz continuous in its arguments at .

Eq. (16) can be treated as a perturbed dynamic system:

| (17) |

Theorem 5 shows that this dynamic system is locally ISS.

Theorem 5.

Corollary 1.

Remark 3.

The strictly semicopositivity condition used to establish the stability of the NE (and thus Theorems 4 and 5 and Corollary 1) is weaker than the strictly monotone game condition widely used in the literature [17, 1], which requires to be strictly monotone on . Note that is strictly monotone if and only if the game Hessian is positive definite on , leading to the satisfaction of the strict semicopositivity condition. However, a strictly semicopositive does not ensure a monotone . For example, consider a two-player game on with costs and . The pseudogradient is not monotone on ; while the game Hessian is strictly semicopositive on . In other words, every strictly monotone game satisfies the strictly semicopositive condition, but the reverse is not true.

II-D Distributed Josephy-Newton method

Next we consider distributed algorithms where each agent performs a local computation to update its own decision variable using its local information, i.e., , , and ; but not or its gradient or Hessian. Other agents’ decision variables from previous rounds of iterations are available. Such distributed NE seeking is often designed based on better- or best- response dynamics [17, 19]. We here show that the Josephy-Newton method can be used to solve the best response or proximal response problem, which, with appropriate monotonicity assumptions, leads to the NE [19].

Given the current decision variables , agent seeks its proximal response to , denoted by , as its next decision, i.e.,

| (20) |

where is a parameter of selection. Denote .

The optimization (20) can be solved by the Newton update:

| (21) |

Theorem 6 shows that from (21) converges to ; and that the proximal response converges to a NE under a monotonicity assumption on .

Theorem 6.

Let A1 and A2 hold. If is strictly copositive on the critical cone and is sufficiently close to , then generated by (21) converges to -quadratically. In addition, if is monotone on and is large enough, then the proximal response by iterating converges to a NE of the game .

III Newton Methods for GNE Problems

This section considers the GNE problem (2). In this section, we assume that can be represented by a finite number of inequality constraints, i.e., , where . The game (2) can then be equivalently written as

| (22a) | ||||

| (22b) | ||||

If solves (22) for all , then is a GNE [9]. The Lagrangian associated with (22) is

| (23) |

where are dual variables. Denote .

If is an optimal solution to (22) given , and if a suitable constraint qualification holds, there exists such that satisfy the following KKT conditions [6]:

| (24) |

Concatenating these KKT systems gives

| (25) |

where

We make the following assumption throughout this section.

A3. (Smoothness): For every , the functions and in (22) are twice continuously differentiable in their arguments, and their second-order derivatives are Lipschitz continuous.

III-A A special class of GNEs: Variational-GNE

Due to the complexity of the GNE problems, most existing studies focus on a special class of GNEs: v-GNE [1, 16], which often requires the following assumptions.

A4. (Player-wise convexity): For every and , is convex, and is compact and convex;

A5. (Common constraints): Agents share common constraints: .

Under Assumption A5, we have and that (25) becomes

| (26) |

If solves (27), then , where for all , must solve (26). Further, by noting that (27) is the KKT condition of VI with defined by (6) and , we can say that if solves VI and if A3-A5 hold, then must be a GNE of (22). Due to this equivalence, one may employ the Newton-type methods in Section II directly for the v-GNE seeking.

III-B Semismooth Newton methods

In this subsection we consider solving (25) without A4 and A5. Note that (25) is not equivalent to a KKT system of any VIs. Instead, it corresponds to a quasi-VI problem, QVI, in which the feasible set is not fixed but depends on the point being evaluated. We start with the coupled KKT systems (25), use complementarity functions to transform them to nonsmooth equations, and employ semismooth Newton methods to solve these nonsmooth equations.

A complementarity function is a function such that If is a complementarity function, then by denoting

| (28) |

the KKT system (25) can be reformulated as

| (29) |

where .

One widely-used complementarity function is the function:

| (30) |

Because this function is a strongly semismooth function and because the composition of strongly semismooth functions is strongly semismooth [10, Proposition 7.4.4], the function in (29) is strongly semismooth everywhere.

We now consider the semismooth Netwon method to solve the system of equations (29). At the iteration , one solves the following linear equation to find :

| (31) |

where , with being the limiting Jacobian of at .

To ensure that the sequence generated by (31) is well-defined, the following quasi-regularity condition is needed.

Definition 4.

[8, Definition 3] A point is quasi-regular if all matrices in are nonsignular.

Remark 4.

According to [7], this quasi-regular condition is weaker than the strongly regular condition in nonlinear optimization problems.

III-C Perturbed semismooth Newton methods

III-D Distributed semismooth Newton methods

Similar to the NE problem, the distributed GNE seeking algorithm can also be designed based on proximal response dynamics. That is, given the current decision variables , agent solves the following constrained optimization problem to find its next decision:

| (34a) | ||||

| (34b) | ||||

The KKT conditions of (34) can be solved by the semismooth Newton update with guaranteed convergence and ISS following a similar analysis as in Sections III-B and III-C. However, we comment that the convergence of the proximal response in a GNE problem requires more restrictive conditions on the game structure. One sufficient condition, for example, is that the game is a generalized potential game [12].

IV Application to CG-MPC

We apply the ISS results to CG-MPC problems to enable time-distributed solution seeking and real-time computation.

IV-A CG-MPC problem

Consider a multi-agent system with dynamics

| (35) |

where , , and .

Each agent is controlled using MPC to optimize its self-interest subject to coupled constraints. Mathematically, a CG-MPC problem at each is formulated as:

| (36a) | ||||

| (36b) | ||||

| (36c) | ||||

| (36d) | ||||

where , , , , , and . For simplicity, all functions in (36) are assumed to be twice continuously differentiable in their arguments, and their second order derivatives are Lipschitz continuous.

The CG-MPC problem (36) can be written compactly as the following GNE problem parameterized by :

| (37a) | ||||

| (37b) | ||||

IV-B Time-distributed CG-MPC solver

Instead of solving (37) completely at each sampling instant, we consider approximately tracking the solution trajectory of (37) as evolves. To this end, we distribute the iterations of the CG-MPC solver over time and warmstart the approximate solution at using the result at . Specifically, the approximate solution at is generated by

| (38) |

where is an estimate of or (decision variable or primal-dual variable, depending on the algorithm design), and represents a fixed number (i.e., ) of solver iterations parametrized by . The iteration (38) is itself a dynamic system evolving in parallel to the controlled plant. The iteration algorithm should be designed such that when , , where denotes the exact solution of the CG-MPC problem at . The Newton-type methods developed in Sections II and III can serve as such algorithms. That is, means times of consecutive updates (15) in NE problems with , , and being parameterized by ; or times of consecutive updates (31) in GNE problems with and being parameterized by . Such iterations may also be performed in an agent-distributed manner:

| (39) |

with and , where can be designed based on the proximal response dynamics.

Next we show that the approximate solution from (38) tracks the optimal solution with bounded tracking error:

| (40) |

Theorem 9.

Remark 5.

Theorem 9 states that the tracking error of the CG-MPC solver remains bounded for all and could be made arbitrarily small by increasing . Other closed-loop properties, such as the ISS of the interconnected plant-solver system against external disturbances to the plant, and the constraint satisfaction, can be established analogously to [14], thanks to the -quadratic convergence and the ISS property of the developed Newton-type methods.

IV-C Numerical studies

Consider a dynamic system of agents:

| (41) |

where and . At each , the following GNE problem needs to be solved with , , and :

| (42) |

Study 1: We first solve the GNE problem (42) at one specific (e.g., ). Because of the coupled constraints, we use the semismooth Newton method developed in Section III-B. The convergence of to with the update rule (31) and the disturbed update (32) are shown in Fig. 1 and Fig. 1 respectively. For the disturbed update, a random disturbance is added to each element of , . As shown in Fig. 1, the semismooth Newton method solves the KKT system of (42) with fast convergence (Fig. 1), and is robust to external disturbances (Fig. 1).

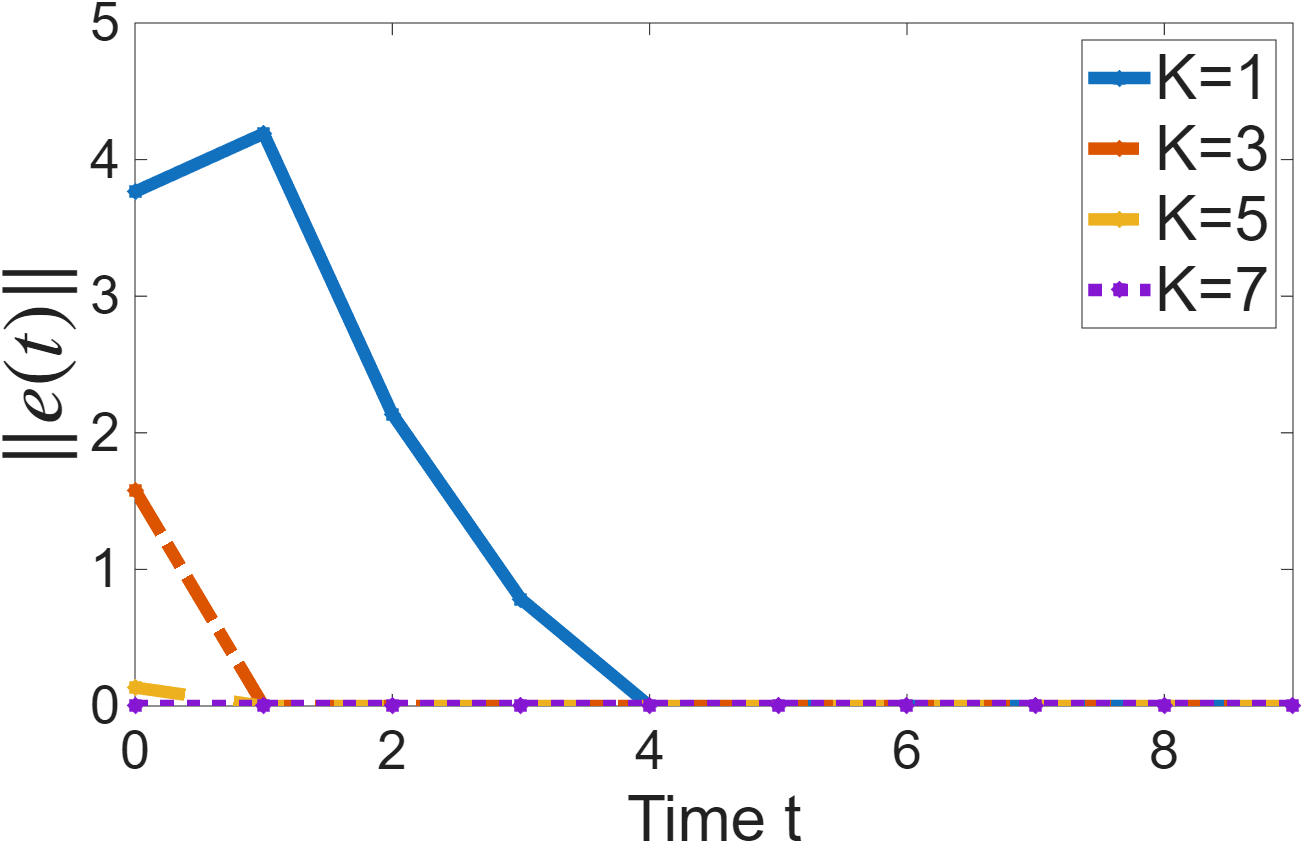

Study 2: We then consider the CG-MPC problem (42) for consecutive and with time-distributed iterations. Specifically, given , the CG-MPC solver generates a sequence according to (31), where each element represents a time sequence of the primal-dual variables with and being the maximum iterations at each . The primal part of is then applied to the plant (41), which leads to ; the solver then seeks following the same procedure. Note that a sufficiently large means that the KKT system of (42) is solved completely at each , while a small means possibly non-zero error . Figures 2 and 2 show and for different , respectively. It is observed that when , remains for all , suggesting that iterations of Newton updates are sufficient to solve the KKT system of (42) at each . As decreases, the errors at the first few time instants increase, indicating incomplete optimization. As increases, the state converges to constants, and the error goes to regardless of , as suggested by Theorem 9.

Study 3: Next we consider the agent-distributed implementation. Specifically, at each , agent solves its proximal response according to (34) until convergence, and the KKT condition of (34) is solved by the semismooth Newton method. Other procedures are the same as in Study 2. Figs. 3 and 3 show when and , respectively. It is observed that for both values of and for all , goes to as increases, indicating the convergence of the proximal response algorithm; and that leads to a much faster convergence of compared to , consistent with the observations in Study 2.

V Conclusion

Newton-type methods have been widely used in nonlinear optimization, and this paper shows that their effectiveness is retained in NE and GNE problems. In NE problems, the convergence of Josephy-Newton method and the ISS of the perturbed iterations were proven under the NE stability condition, weaker than the strong regularity condition typically used in nonlinear optimization, and weaker than the strictly monotone game condition typically used in the NE-seeking literature. For GNE problems, semismooth Newton methods were developed to solve the KKT systems. The ISS was proven under a quasi-regularity condition, also weaker than the strong regularity condition. A CG-MPC solver with time-distributed iterations was developed for real-time implementation. Boundness of tracking error was proven and was verified by numerical analysis.

Appendix

V-A Proof of Theorem 3

V-B Proof of Theorem 4

Define the error function as the residual of the first-order Taylor expansion of at relative to :

| (43) |

If is Lipschitz continuous in a neighborhood of , then according to [10, Proposition 7.2.9],

| (44) |

Denote and . By the continuous differentiability of near , the affine function is a strong first-order approximation (FOA) of at [10, Section 5.2.2]. Because is a stable NE of the game , it is a stable solution to VI. Because is a strong FOA of at , is also a stable solution to VI [10, Proposition 5.2.15]. The remaining proof is then analogous to [10, Theorem 7.3.5] by noting that (15) is equivalent to solving VI, and that (44) results in , leading to -quadratic convergence.

V-C Proof of Theorem 5

According to (16), is a solution to VI, where

| (45) |

Denote

| (46) | |||

| (47) |

Due to the stability of , we have

| (48) |

V-D Proof of Corollary 1

V-E Proof of Theorem 6

Eq. (21) is equivalent to solving VI, where . Denote .

V-F Proof of Theorem 8

Denote and , generated from (32) satisfies

| (52) |

V-G Proof of Theorem 9

The proof is analogous to the proof of Lemma 1 in [14] by noting that from the developed Newton methods is at least -quadratically convergent and is locally ISS to disturbances.

References

- [1] (2024) Online feedback equilibrium seeking. IEEE Transactions on Automatic Control. Cited by: §III-A, Remark 3.

- [2] (2024) Input-to-state stability of Newton methods for generalized equations in nonlinear optimization. Proceedings of IEEE Conference on Decision and Control. Cited by: §I, §I, Remark 2.

- [3] (2009) Implicit functions and solution mappings. Vol. 543, Springer. Cited by: §I.

- [4] (2013) Convergence of inexact Newton methods for generalized equations. Mathematical Programming 139 (1), pp. 115–137. Cited by: §I.

- [5] (2021) Lectures on variational analysis. Vol. 205, Springer. Cited by: §I.

- [6] (2011) On the solution of the KKT conditions of generalized Nash equilibrium problems. SIAM Journal on Optimization 21 (3), pp. 1082–1108. Cited by: §I, §I, §III.

- [7] (1998) On the accurate identification of active constraints. SIAM Journal on Optimization 9 (1), pp. 14–32. Cited by: Remark 4.

- [8] (2009) Generalized Nash equilibrium problems and Newton methods. Mathematical Programming 117 (1), pp. 163–194. Cited by: §I, Definition 4, Theorem 7.

- [9] (2010) Generalized Nash equilibrium problems. Annals of Operations Research 175 (1), pp. 177–211. Cited by: §I, §I, §III-A, §III, Theorem 1.

- [10] (2003) Finite-dimensional variational inequalities and complementarity problems. Springer. Cited by: §I, §II-A, §III-B, §V-A, §V-B, §V-B, §V-E, §V-F, Remark 1, Remark 2.

- [11] (2010) Nash equilibria: the variational approach. Convex optimization in signal processing and communications, pp. 443. Cited by: §V-A, Theorem 2.

- [12] (2011) Decomposition algorithms for generalized potential games. Computational Optimization and Applications 50, pp. 237–262. Cited by: §III-D.

- [13] (1979) Quasi-Newton methods for generalized equations. Ph.D. Thesis, University of Wisconsin. Cited by: §I.

- [14] (2020) Time-distributed optimization for real-time model predictive control: stability, robustness, and constraint satisfaction. Automatica 117, pp. 108973. Cited by: §I, §I, §V-G, Remark 5.

- [15] (1950) Equilibrium points in n-person games. Proceedings of the National Academy of Sciences 36 (1), pp. 48–49. Cited by: §I.

- [16] (2019) Distributed GNE seeking under partial-decision information over networks via a doubly-augmented operator splitting approach. IEEE Transactions on Automatic Control 65 (4), pp. 1584–1597. Cited by: §III-A.

- [17] (2022) Dissipativity theory in game theory: on the role of dissipativity and passivity in Nash equilibrium seeking. IEEE Control Systems Magazine 42 (3), pp. 150–164. Cited by: §II-D, Remark 3.

- [18] (1999) On the existence of pure and mixed strategy Nash equilibria in discontinuous games. Econometrica 67 (5), pp. 1029–1056. Cited by: §II.

- [19] (2014) Real and complex monotone communication games. IEEE Transactions on Information Theory 60 (7), pp. 4197–4231. Cited by: §II-D, §V-E.

- [20] (2014) Game theoretic model predictive control for distributed energy demand-side management. IEEE Transactions on Smart Grid 6 (3), pp. 1394–1402. Cited by: §I.