Pricing and Hedging of Cross-Currency

Equity Protection Swaps

Abstract.

We study arbitrage-free pricing and static hedging strategies for an innovative insurance product called the equity protection swap (EPS). Notably, we focus on the application of EPSs involving cross-currency reference portfolios, reflecting the realities of investor asset diversification across different economies. The research examines key considerations regarding exchange rate fluctuations, pricing and hedging frameworks, in order to satisfy dynamic requirements from EPS buyers. We differentiate between two hedging paradigms: one where domestic and foreign equities are treated separately using two EPS products and another that integrates total returns across currencies. Through detailed analysis, we propose various hedging strategies with consideration of different types of returns — nominal, effective, and quanto - for EPS products in both separate and aggregated contexts. The aggregated hedging portfolios contain basket options with cross-currency underlying asset, which only exists in the OTC market, thus we further consider a superhedging strategy. A numerical study assesses hedging costs and performance metrics associated with these hedging strategies, illuminating practical implications for EPS providers and investors engaged in international markets. We further employ the Monte Carlo method for the basket option pricing, together with two other approximation methods - geometric averaging and moment matching. This work contributes to enhancing fair pricing mechanisms and risk management strategies in the evolving landscape of cross-currency financial derivatives.

Keywords: Equity protection swap; Cross-currency portfolio; Effective return; Static hedging; Basket option.

a School of Mathematics and Statistics, University of Sydney,

Sydney, NSW 2006, Australia

b Faculty of Mathematics and Information Science, Warsaw University of Technology,

00-661 Warszawa, Poland

c National University of Singapore, Department of Mathematics,

21 Lower Kent Ridge Road, 119077.

1. Introduction

Xu et al. [35] have introduced a new type of insurance for superannuation - equity protection swap (EPS). It is a financial derivative, which is reminiscent of a total return swap but has also some features of the annuity insurance product RILA. Additionally, the structure of an EPS makes it a reliable safeguard when the value of a reference portfolio drops, and it can also be tailored to accommodate the specific requirements of super fund members. Compared with variable annuity riders, an EPS is less complex and is not necessarily associated with a variable annuity. Apart from that, there is a main difference between RILA and EPS products that EPS is an insurance product that can be added to the variable annuity rather than the annuity itself in order to manage the risks.

An important direction in the study of EPSs is the case of a cross-currency reference portfolio, which will be discussed in this paper. In reality, it is fairly common for investors to hold assets across different economies in order to do risk diversification. Then the underlying reference portfolio for an EPS will contain assets from several economies. Therefore, to generalise the application scope of the concept of an EPS, the pricing and hedging strategies should take into account the exchange rate fluctuations, as well as the correlation between prices of domestic and foreign assets. Various existing approaches to the arbitrage-free pricing and hedging of cross-currency reference portfolios include either considering two independent local returns on domestic and foreign assets or focusing on the total return on the portfolio’s value expressed in the domestic currency. This area of research is essential for providers and investors operating in international markets and it provides a valuable insight into fair pricing and hedging strategies for an EPS in a global context.

To mitigate the foreign exchange risk, a variant of the Black-Scholes model was first proposed for pricing and hedging of European currency options by Garman and Kohlhagen [14]. It should be acknowledged that since the Garman-Kohlhagen model is based on the geometric Brownian motion, it is unable to correctly specify the dynamics of the exchange rate.

In order to hedge the risk of investments in domestic and foreign reference portfolios, we need to consider the preferences of EPS buyers and examine their respective strategies. If the purchaser regards the underlying portfolio as two separate independent portfolios, they will focus on the actual returns of domestic and foreign equities independently. In this case, we can model two hedging portfolios to hedge domestic and foreign equity risks separately. We need to mention that the hedging portfolio for domestic equity has been discussed before, thus we only need to consider foreign equity risks in this strategy. In another situation, EPS buyers only focus on the total return on the whole reference portfolio rather than separate returns of domestic and foreign equities. The insurance company should hedge total return risks together with currency risks and build only one hedging portfolio, it is more difficult to structure than in the first case.

We aim to analyse the pricing and hedging of an EPS with a cross-currency reference portfolio. For conciseness of notation, we assume that the reference portfolio contains only two economies - a domestic and a foreign one. By convention, the domestic currency is chosen to be the Australian dollar (AUD) and the foreign one is the U.S. dollar (USD) but, obviously, all definitions and results from this paper can be applied to any two (or more than two) currencies.

We start this paper by defining a setup for the domestic and foreign markets in Section 2. We discuss not only the nominal return but also the effective return of the foreign equity, then provide the cross-currency and quanto (i.e., for a guaranteed exchange rate) rate of return for the cross-currency portfolio. The cross-currency reference portfolio of EPS is defined and we discuss the hedging strategies for such EPS products. Unlike for a standard EPS with a single currency reference portfolio studied by Xu et al. [35], here we have several different hedging strategies since we consider alternative conventions regarding realised returns and hence various structures of the protection and fee legs.

In Section 3 , we study separate hedging strategies, which correspond to the EPS convention where the realised returns of domestic and foreign equities are mitigated independently and, as a consequence, two sets of hedging portfolios with various kinds of domestic and foreign options are used. In fact, in that case we can adapt the static hedging strategies for a standard EPS with a single currency reference portfolio to fully hedge the domestic equity, by adding appropriate weights to the notional principal. However, for the foreign equity, we need to consider not only its realised return but also the returns on the exchange rate. Firstly, the EPS provider can hedge only the nominal return of the foreign equity and exchange this foreign nominal return to domestic return by multiplying the exchange rate at maturity. In this case, European options written on foreign equities can be used directly to build the hedging portfolio and the volatility of the exchange rate will not be considered.

Secondly, one can also hedge the foreign equity’s effective return, which is the return on the foreign equity struck in domestic currency. The EPS provider needs to track the value of foreign equity expressed in the domestic currency in the holding period of the EPS product and, in this case, he needs to use European options with foreign equity struck in the domestic currency as the underlying asset. We also consider in Section 3.6 the issue of hedging the foreign equity’s quanto rate, which predetermines a fixed exchange rate corresponding to the EPS holder’s requirements.

In Section 4, we consider the hedging strategy for an EPS referencing the total return that combines the returns of both domestic and foreign equities. We discuss two different hedging strategies here, the first one is a static hedging strategy that uses European cross-currency basket options with the whole portfolio struck in domestic currency as the underlying asset; here we can extend the algorithm of the hedging strategy for standard EPS products with single currency reference portfolio to do the hedging. However, we need to mention that this fully hedging strategy may be unattainable in that European cross-currency basket options on bespoke portfolios are unlikely to be offered in practice, though they can be negotiated on the OTC market. In order to build a more practical hedging portfolio, we further introduce a joint superhedging strategy. By using the subadditive property, we build a joint superhedging strategy by using European options with single currency underlying assets. However, some parts of this joint superhedging strategy still need to be structured in the OTC market.

In Section 5, we present a numerical study for EPS products with the cross-currency reference portfolio. We select parameters for domestic and foreign markets and examine trends of stock prices and exchange rates with correlated volatility. Our numerical study illustrated the hedging costs for separate hedging strategies: domestic return, effective foreign return, and quanto foreign return, as well as for aggregated hedging strategies: cross-currency strategies, quanto hedging strategies, and superhedging strategies. For the aggregated hedging strategies, we need to use basket options to build the hedging portfolio. However, we cannot find an explicit formula for the basket option and we will use some approximations instead. We will consider the premium obtained using the Monte Carlo method as an exact cost, the closed-form solutions for basket options with geometric averaging approximation and under three-moment matching approximation method are also included as a comparison.

Each hedging strategy satisfies different requirements from EPS buyers, which influence the structure and clauses of the EPS product at the beginning, thus all of them are important and cannot be substituted. We note that the aggregated superhedging strategy requires higher hedging costs compared with other aggregated hedging strategies, which is consistent with the definition of superhedging. We conclude this work by summarising our findings and emphasising the practical importance of this study.

2. Generic Equity Protection Swaps

We first define a generic equity protection swap (EPS), which is a financial contract with a single terminal payoff at maturity determined by the notional principal and performance of an underlying reference portfolio over the lifetime of an EPS. Let us denote by the simple rate of return on the strictly positive wealth process of a reference portfolio so that satisfies . In the cross-currency framework the portfolio’s wealth process , which is given in the domestic currency, can be formally specified in several alternative ways, depending on the financial interpretation of a reference portfolio and investor’s preferences and thus also the random variable can be specified in various ways (see Section 3.1).

Before we state the definition of a generic EPS, we need to introduce some notation. We consider sequences and of real numbers representing a predetermined set of thresholds for losses and gains, respectively. For each , the protection rate over the loss interval is denoted as whereas the fee rate over the gain interval is denoted by . It is natural to assume that protection rates belong to the interval , but it suffices to assume that the fee rates are arbitrary nonnegative constants.

According to the definition of a generic EPS introduced in Xu et al. [35], the cash flow at time from the investor to the provider of an EPS is given by where the function is used to encode the structure of an EPS and is the notional principal of an EPS. We postulate that the payoff profile is a piecewise linear, non-decreasing, continuous function such that . The following definition was introduced in Xu et al. [35].

Definition 2.1.

A generic EPS is a financial contract with the payoff at maturity date to its provider given by the adjusted return where the non-positive protection leg represents the provider’s loss and equals, per one unit of the notional principal ,

and the non-negative fee leg represents the provider’s gain and satisfies

Equivalently, the EPS provider’s payoff is specified by the adjusted return where the derivative of the adjusted return function exists almost everywhere and is given by the equality

Throughout this work, our main goal is to study arbitrage-free market-based pricing of various classes of cross-currency EPSs and analyze static hedging strategies based on European options. In particular, we adopt the following natural definition of fairness of a generic EPS, which explains why the term ‘swap’ is suitable for a generic EPS with fair initial value. Recall that the term swap is commonly used in reference to a financial contract that is worthless at its inception.

Definition 2.2.

We say that an EPS initiated at time 0 with the payoff structure is fair if the terminal payoff with the settlement date has null arbitrage-free price at time 0 or, equivalently, if it can be replicated by a static portfolio of European options such that the portfolio’s initial cost is null.

2.1. Buffer and Floor EPS

Two EPS products introduced by Xu et al. [35] will be used throughout as examples of a generic EPS. Needless to say, much more complex products can be offered to cater for individual risk preferences of investors and all of them can be dealt with using general pricing and hedging results from this work. For simplicity, we only deal here with EPS products of European style with a payoff at maturity date , although one may allow for cancellation of an EPS by its holder at its current market price provided that the underlying European options are liquidly traded.

We first set and define the buffer EPS where the concept of a buffer applies to both the protection and fee leg. Let and denote the payoffs of a European call and put options written on the process , with the strike and maturity date .

Definition 2.3.

The buffer EPS is obtained by taking (hence for all where and ) and some values for and . Hence the cash flow at maturity of a buffer EPS to its provider equals

where and .

In the floor EPS we set , which means that the provider covers the holder’s losses above the level but the holder’s losses below are not covered at all. Notice that, by convention, the buffer is applied to the fee leg and thus it is exactly the same as in a buffer EPS.

Definition 2.4.

The floor EPS is specified by and thus the cash flow at maturity to its provider equals

2.2. Static Hedging of a Generic EPS

After representing the payoff of a generic EPS, one can observe that its payoff can be written in terms of a combination of European calls and puts on rate of return maturing at . Hence our next goal is to examine a hedging portfolio for a generic EPS in terms of options written on the underlying portfolio .

Definition 2.5.

A static portfolio of European put and call options is represented by a vector and its value process is given by, for every ,

where for we have that where the strike equals and where .

According to our convention, the provider receives from the buyer the initial premium at time 0 and the cash flow at time . Assume that the provider establishes at time 0 a portfolio of plain-vanilla call and put options written on . Then we have the following definition for the provider’s hedged cash flow and fair price where is the price of the domestic zero-coupon bond with unit notional principal.

Definition 2.6.

For a generic EPS introduced in Definition 2.1, the provider’s hedged cash flow at time per one unit of the notional principal , denoted by , equals

We say that an EPS can be statically hedged by the provider if there exists a static portfolio established at time 0 and an initial premium such the equality holds almost surely. Then the number is called the fair premium for an EPS per one unit of the notional principal.

Notice that it suffices to find such that the where is the notional principal of an EPS and set . The static hedge and fair price for a generic EPS with arbitrary payoff structure can be identified from the following proposition, which is due to Xu et al. [35] (see Proposition 3.1 therein). Recall that and, for convenience, we also adopt the convention that . We stress that the static hedge from Proposition 2.1 is model-free and can be easily implemented if the relevant European options are traded.

Proposition 2.1.

The static hedge composed of call and put options for a generic EPS with the notional principal satisfies the following equation

| (1) |

where and for every and . The fair premium for an EPS is equal to per one unit of the notional principal where, in the domestic currency,

| (2) |

The proof of Proposition 2.1 hinges on the following elementary equalities, for every ,

and, for every ,

Remark 2.1.

Let us define so that and the rates of return on processes and manifestly coincide. Then we obtain an equivalent representation for equality (1)

| (3) |

which shows that, formally, it suffices to examine options written on the normalized process . Since in Section 3, the process is assumed to represent a market quantity (e.g., the price of a given equity or a specific domestic or foreign market index) we will use there representation (1), which is based on traded options written on . In contrast, in Section 4 we prefer to employ equality (3) since, firstly, options on a bespoke cross-currency portfolio are unlikely to be traded and, secondly, equation (3) yields simpler pricing and hedging formulae within the cross-currency market model of Section 3.2. To sum up, equality (1) is used when the emphasis is put on the possibility of static hedging of an EPS with traded options on market indices, whereas representation (3) is convenient when performing computations within a stochastic market model, especially when dealing with a basket option on a bespoke portfolio composed of domestic and foreign assets.

Remark 2.2.

Recall from Definition 2.2 that an EPS is said to be fair if its initial premium vanishes, that is, in Definition 2.6. In the case of a buffer or floor EPS, assuming that all parameters except for the fee rate are fixed, one can find a unique level of for which the fair premium for an EPS is null by solving for the linear equation (2) (or, equivalently, (3)) with initial hedging cost set to 0. For instance, the fair fee rate for the buffer EPS equals

and for the floor EPS we have

3. Protection Against Separate Domestic and Foreign Losses

For simplicity of notation, we will focus here on the case of two financial markets, the domestic market in Australia and the foreign market in the U.S., with AUD and USD being the respective currencies, although an extension to several economies does not present any difficulties. Then it suffices to examine two separate hedging portfolios, the first one for the domestic component of holder’s portfolio with the notional principal given in AUD and the second one for the foreign component with the notional principal given in USD (or, equivalently, with the domestic value in AUD). The exchange rate process represents the direct quote, which means that gives the price at time of one unit of the foreign currency (by our convention, USD) in terms of variable number of units of the domestic currency (AUD).

Generally speaking, investors are faced with the choice: either to obtain a protection against losses from their domestic and foreign investments using separate EPSs, one EPS for each component of their portfolio, or to enter into a single EPS furnishing an effective protection against total losses from their combined portfolio of domestic and foreign assets. In the latter case, the portfolio’s value process is expressed in the domestic currency using a particular accounting method.

Assume first that the investor decides to purchase two independent products yielding protection against negative returns on either or , respectively, where and represent the current values at time of domestic and foreign reference portfolios (e.g., particular market indices) with the respective values expressed in the domestic and foreign currency. To be more specific, we first assume that the payoff from domestic EPS with the profile (resp. the foreign EPS with the profile ) is referencing the domestic return (resp. the nominal foreign return ) with the corresponding domestic and foreign EPSs examined in Sections 3.3 and 3.4, respectively. Next, we introduce and study the domestic pricing of foreign EPSs based on the effective and quanto foreign returns in Sections 3.5 and 3.6, respectively. Subsequently, in Section 4, we study cross-currency EPSs that yield protection against combined effective losses of a cross-currency portfolio.

3.1. Cross-Currency Portfolios

We introduce the following notation for the domestic rate of return and the (nominal) foreign rate of return, as well as the return on the foreign currency, for every ,

Another important concept is the effective foreign rate of return, that is, the rate of return on the foreign portfolio when its value at any date is expressed in the domestic currency using the current value of the exchange rate. The effective foreign return satisfies, for every ,

where the quantity represents the current domestic value of .

We also need the notation for the notional principal of the holder’s cross-currency portfolio and for its decomposition into the domestic and foreign holdings. We consider an agent who invests at time 0 in a portfolio of domestic and foreign risky assets with a total wealth equal to (in AUD). Then the notional principal can be decomposed into domestic and foreign holdings as follows where (in AUD) is the notional principal of domestic assets in holder’s portfolio and (also given in AUD) is the notional principal of foreign assets expressed in the domestic currency. Recall that we denote by the notional principal of foreign assets in holder’s portfolio expressed in the foreign currency, which means that (in USD). This leads to an equivalent representation .

It is convenient to introduce the weight (resp. ), which gives the proportion of the total wealth invested at initial date in domestic assets (resp. foreign assets). Then the number of units of the domestic and foreign reference portfolios and held in a cross-currency portfolio satisfy

where and represent holdings in and , respectively, and satisfy

Then the cross-currency portfolio in domestic assets represented by and foreign assets given by with the notional principal and the weight can be identified with the pair .

3.2. Cross-Currency Market Model

Although our main focus is on a model-free static hedging of an EPS, we will also use a particular stochastic model to give an alternative pricing method, which will be used in assessment of the forward performance of various classes of cross-currency EPSs. Therefore, we briefly summarize in this section the classical cross-currency model as presented, for instance, in Chapter 13 of Musiela and Rutkowski [27]. The domestic and foreign bank accounts are given by and for some constant short-term interest rates and . For a fixed horizon date , the dynamics of domestic and foreign equities, and , and the exchange rate, , under the physical probability measure are specified by the SDEs

| (4) | |||

with strictly positive initial conditions and where the column vector where ∗ denotes the transpose is a standard Brownian motion on and the volatilities are given by row vectors: and . Then the dynamics of the domestic and foreign equity and the exchange rate under an equivalent probability measure , which is the domestic martingale measure, are given as

| (5) | ||||

where is a standard Brownian motion on . Finally, the process is a standard Brownian motion on where is the foreign martingale measure and thus the processes and are governed under by the following SDEs

| (6) | ||||

It is well known that if the volatility matrix is non-singular, then the cross-currency market model given by (3.2) is arbitrage-free and complete.

It is worth noting that initial prices of the foreign and domestic equity is immaterial when pricing equity protection swaps within the setup of a cross-currency market model. This is easy to understand since the payoffs of equity protection swaps only depend on realized returns on the reference domestic and foreign portfolios, and respective notional principals so they are independent of the initial prices of equities. However, when presenting implementations of static hedging for various classes of EPSs, we assume that the trading strategies are based on actively traded options and thus the initial market prices of equities and actual strikes for traded options will be used. To sum up, one should note the crucial distinction between the real-world pricing results based on market quotes for traded options, which give market prices of EPSs, and theoretical computations yielding the model prices of options obtained within a cross-currency market model. The former approach relies on the existence of a liquid market for relevant European options, whereas the latter hinges on an implicit assumption that European options can be dynamically hedged using underlying domestic and foreign assets.

3.3. Protection Against Domestic Losses

To protect the domestic component of his portfolio with the initial wealth and weight , the holder may use the domestic EPS with the notional principal and the payoff at time given in the domestic currency

We write to denote the strike price denominated in the domestic currency (resp., the foreign currency). It is assumed that call and put options with payoffs and for all strikes are traded, which is a natural assumption given that the portfolio typically represents a market index. The case of the domestic EPS does not demand a detailed study since it was already examined in Xu et al. [35]. We stress that all results on static hedging are model-free and thus they do not rely on the cross-currency market model introduced in Section 3.2. The following result is an easy consequence of Proposition 2.1.

Corollary 3.1.

The static hedging in terms of domestic equity options for the domestic EPS is given by Proposition 2.1 with and , that is, where for every ,

where and for every and .

Typically, the domestic and foreign portfolios of investors can be associated with existing market indices, such as the S&P 500 Index in the U.S. or the S&P/ASX 200 Index in Australia, which encompass a large majority of listed equities in respective economy. Furthermore, many financial institutions maintain and offer shares in exchange traded funds (ETFs) containing multiple stocks which are designed to meet a predetermined goal, most frequently, to approximate the performance of a certain market index. Hence ETFs can be considered as actively traded proxies for market indices and thus the assumption that market indices can be seen as traded assets has some merit.

Furthermore, it is clear from Corollary 3.1 that liquidly traded options on market indices, which are available on stock exchanges worldwide, can be used by providers of domestic and foreign EPSs for implementation of static hedging and hence also pricing of various EPS products they offer, not only when they are issued but also for marking-to-market if, for instance, the cancellation of an EPS by its holder is allowed. In this context, it is worth mentioning the CBOE S&P 500 Index options (SPX), Nanos S&P 500 Index options (NANOS), and SPDR S&P 500 ETF options (SPY) offered in the U.S., as well as ASX S&P/ASX 200 Index options (XJO) actively traded in Australia. The above mentioned index and ETF options are of European style, except for SPY options, which are of American style.

Plain-vanilla options on most typical domestic and foreign portfolios, and , are likely to be actively traded on options exchanges and thus Corollary 3.1, which is a model-free result, is sufficient for real-life market pricing and static hedging of a domestic EPS. In contrast, Corollary 3.2 is useful when studying model pricing of domestic EPSs and using their model prices in the context of more complex cross-currency EPSs, which are studied in the foregoing sections. If we assume that the dynamics of the domestic portfolio are given by (3.2), then we may use the classical Black-Scholes options pricing formula to obtain the following pricing result for the domestic EPS where we write to denote the cumulative density function of the standard normal distribution.

Corollary 3.2.

The model price at time 0 of the domestic EPS with the payoff at time equals, in the domestic currency,

where

3.4. Protection Against Nominal Foreign Losses

Analogous pricing results can be formulated for the foreign EPS with the payoff denominated in the foreign currency and given by where the payoff function is given by parameters and . Then the model-free pricing formula for the foreign EPS with the payoff at maturity and the foreign notional principal reads, in the foreign currency,

where and for every and . Using dynamics (3.2) under the foreign martingale measure , we obtain the foreign market counterpart of Proposition 3.2.

Corollary 3.3.

The model price at time 0 of the foreign EPS with the foreign notional principal equals, in the foreign currency,

where

3.5. Protection Against Effective Foreign Losses

A more practical protection against losses from the foreign part of a cross-currency portfolio with the notional principal and the weight for foreign assets can be obtained by entering into the effective foreign EPS with the notional principal and with the payoff at time to the provider given by

Consider a foreign equity call option struck in the domestic currency where the holder has the right to buy at time one unit of by paying units of domestic currency, which yields the payoff equal to in the domestic currency. We set and and we denote by and the price processes of call and put options written on the synthetic risky asset representing the domestic value of a reference portfolio of foreign assets.

Corollary 3.4.

The static hedging in terms of foreign equity call and put options struck in the domestic currency for an effective foreign EPS is given by Proposition 2.1 with and , that is, where, for every ,

where and for every and .

For the purpose of static hedging of an effective foreign EPS, we assume that the provider can trade in foreign equity options with the foreign equity struck in domestic currency as the underlying asset and strike price given in the domestic currency. Several ETFs available in Australia allow to track the performance of the S&P 500 AUD Index, which is the index designed to measure the AUD performance of large capitalisation U.S. equities. Investing in such ETFs can be seen as a proxy for the theoretical concept of the value process representing the domestic value of a foreign portfolio, e.g., a particular market index in the foreign economy. Corollary 3.4 shows that related options of European style could be used to hedge and price effective foreign EPSs and thus, in principle, their current market values would be given in terms of market quotes for options on such ETFs provided that they are publicly available.

It is a realistic assumption that the above mentioned options are available on the OTC market, in which case the provider of an effective foreign EPS can establish the static hedging strategy. However, for the purpose of obtaining a better insight into properties of arbitrage-free prices of effective foreign EPSs of various classes and with differing parameters, we will also use the following classical result, which is known to be valid within the setup of Section 3.1. In fact, it is an easy consequence of the dynamics of under

Proposition 3.1.

The model price at time of a foreign call option struck in the domestic currency with the terminal payoff at maturity given by is equal to, for every ,

where and

The price of a put option with the payoff equals

Notice that Proposition 3.1 allows for a dynamic hedging of an effective foreign EPS using the underlying portfolio , which is formally represented by the process , and the domestic money market account . Furthermore, by combining Corollary 3.4 with Proposition 3.1, we obtain the pricing formula for an effective foreign EPS, which holds within the setup of Section 3.2.

Corollary 3.5.

The model price at time 0 of the effective foreign EPS with the payoff at time equals, in the domestic currency,

where

3.6. Protection Against Quanto Foreign Losses

A quantity-adjusting derivative (or, simply, a quanto derivatinve) is a cross-currency derivative in which the underlying asset is denominated in one currency but settlement is made in another currency at a predetermined exchange rate, hereafter denoted as . Another name for such a financial product is a guaranteed exchange rate derivative since they enable investors to fix at the contract’s inception the exchange rate between two currencies. By construction, quanto derivatives help to safeguard the investors against unfavourable fluctuations in the exchange rate but, of course, at the cost of no benefiting from a favourable move of the exchange rate.

We henceforth assume that the exchange rate has been fixed at time 0 and at any date the domestic value of foreign holdings is calculated using the exchange rate , which in fact is an investment opportunity offered to investors by some financial companies. In principle, the exchange rate in a quanto contract is completely arbitrary but we sometimes set to simplify the presentation.

We first consider a quanto EPS with a reference portfolio composed of foreign assets only and with the foreign notional principal . In the quanto foreign EPS with the predetermined exchange rate , the provider’s cash flow at time equals, in the domestic currency,

Similarly, the terminal payoffs of the quanto call and put option written on are defined by and where and are given in the foreign currency and the option’s payoff is expressed in the domestic currency. Similarly, let and stand for the domestic price processes of quanto call and put options written on the foreign asset . We first state a model-free result on static hedging of a quanto foreign EPS and hence also the price in terms of quanto options.

Corollary 3.6.

The static hedging in terms of quanto options for the quanto foreign EPS is given by Proposition 2.1 with and , that is, where, for every ,

where and for every and .

As a proxy for the concept of the quanto foreign return, we could mention returns on exchange traded funds aiming to provide investors with the performance of the S&P 500 AUD Hedged Index, which uses a currency hedged strategy to reduce the risk of currency fluctuations while accepting underlying market risk of major U.S. equities. As usual, we refer to AUD as the domestic currency but analogous indices are also offered for other major currencies. Then, as shown in Corollary 3.6, the market value of the quanto foreign EPS would be given in terms of market prices of options on such ETFs, of course, provided that they are traded on the OTC market.

If the provider of the quanto foreign EPS cannot directly trade in quanto options, then a plausible alternative is to use a stochastic model to compute their prices and obtain a synthetic versions of quanto options by dynamic trading. To this end, one may use the following result, which holds in the model of Section 3.1. Let us denote . Then we have the following result.

Proposition 3.2.

The model price of a quanto call option with the payoff is given by, in the domestic currency,

where and

The price of a quanto put option with the payoff equals

From Corollary 3.6 and Proposition 3.2, we obtain the pricing formula for the quanto foreign EPS in the model of Section 3.2. Notice that in Corollary 3.7 we set and thus the equality holds.

Corollary 3.7.

The model price at time 0 of the quanto foreign EPS with the payoff at time with equals, in the domestic currency,

where

4. Pricing and Hedging of Cross-Currency Basket EPSs

It is natural to expect that holders of superannuation accounts will focus on the value of their foreign holdings expressed in the domestic currency and pooled with their domestic holdings. Therefore, after discussing separate EPSs protecting against either domestic or foreign losses, we move on to examination of the case of a cross-currency basket EPS, which refers to aggregated returns of a basket of equity indices. As usual, is the nominal value in the domestic currency of the holder’s portfolio of domestic and foreign assets and also the domestic notional principal of a cross-currency basket EPS.

4.1. Cross-Currency Basket EPS

By the effective wealth of a cross-currency portfolio we mean its total value expressed in the domestic currency. Specifically, for any notional principal and weight , the effective wealth of a cross-currency portfolio satisfies and, for every ,

where we denote

so that, in particular, . We now consider the basket process as a reference portfolio for an EPS and thus also as the underlying process for related cross-currency call and put options. For any notional principal and weight , the effective rate of return on a cross-currency portfolio equals, and ,

Definition 4.1.

In a generic cross-currency basket EPS, the provider’s cash flow at time is given in the domestic currency and equals

for some adjusted return function with parameters and .

To derive the static hedging strategy for a generic cross-currency basket EPS, we consider cross-currency basket call and put options written on with the payoffs and where the payoffs are given in the domestic currency.

Corollary 4.1.

The static hedging in terms of options written on for a generic cross-currency basket EPS is given by Proposition 2.1 with and , that is, where, for every ,

where and for every and .

Using this static hedging strategy, the provider can perfectly hedge the effective return on the whole reference portfolio, which includes both domestic equities and foreign equities struck in the domestic currency. Although the provider’s hedging strategy is fairly simple, it hinges on a strong postulate that the relevant call and put options on the value process are actively traded, which is a rather unrealistic postulate, in particular, due to the fact that depends on the choice of the weight . Therefore, we will also examine the theoretical pricing and hedging for a generic cross-currency EPS within the framework of the market model introduced in Section 3.2, as well as its superhedging.

To this end, we start by noticing that

where, for computational convenience, we introduce normalized processes and so that . Of course, that normalization does not affect the dynamics of price processes and , which were specified in Section 3.2, but only their initial values and thus we have that

The cross-currency basket call option written on has the terminal payoff at maturity given by in the domestic currency. Since is a sum of lognormally distributed random variables it does not follow a lognormal distribution and thus the Black-Scholes-like pricing formula for a basket option is not available. Therefore, we analyze other ways of computing, at least approximately, the initial prices of cross-currency basket options within the model from Section 3.2:

(i) numerical pricing using the Monte Carlo method,

(i) approximate analytical pricing using the geometric averaging method,

(ii) approximate analytical pricing using the moment matching technique.

4.2. Approximate Pricing Through Geometric Averaging Method

For the analytical approximation of the price of the cross-currency basket call option, it is convenient to rewrite the pricing equality as follows

where we introduce the discounted values and and so that

with . To get an approximation for the price of a classical basket option on equities, Gentle [15] proposed to replace the weighted arithmetic mean by a similarly weighted geometric mean, which is henceforth denoted as and, in the present setup, is given by

where

Notice that is a Gaussian random variable under with null expected value and the variance where

Consequently, the random variable has the lognormal distribution under with the expected value

Then the proposed approximation for the initial price of the cross-currency basket call option is given by the expected value

where equals

with

which is a consequence of the dynamics of and under . Elementary computations now lead to the following result, which can be seen as a variant of a more general pricing formula for an option written on a basket on domestic equities in the multi-dimensional Black-Scholes model (see Proposition 6.9.1 in Musiela and Rutkowski [27]).

Proposition 4.1.

The model price of the cross-currency basket call option can be approximated by

where

The model price of the cross-currency basket put option with the payoff can be approximated by

Remark 4.1.

The put-call parity for cross-currency basket options has the form (recall that is a martingale under and ) whereas for the approximated values it is given by . Hence it suffices to focus on the pricing formula for a cross-currency basket call option.

4.3. Approximate Pricing Through Moment Matching Method

Borovkova et al. [8] considered the problem of pricing basket options in a futures market and proposed a numerical approach based on matching three moments to approximate the distribution of baskets with possibly negative weights, which in turn yields a fairly accurate approximation for the price of a basket option. To be more specific, their method uses the first three moments to match the real-valued parameters of the approximating shifted lognormal distribution of the form

where is a standard normal random variable under a probability measure . The quantity can be interpreted as a scale parameter, the parameter represents a shape parameter, and is a location parameter. The parameter is included to adjust the overall sign of the basket price when weights are not all of the same sign and it is chosen to coincide with the sign of the skewness of the basket. For the pricing algorithm proposed in [8], a real-valued closed-form solution for the set of nonlinear equations was recently developed by Hu et al. [19] who obtained the closed-form approximation for the price of a basket option in terms of the mean, variance, and skewness of the basket’s distribution at maturity . We are going to adapt their results to the present context.

Recall from Section 4.1 that our goal is to compute

where and for every . We have

with and thus, in particular,

The first step hinges on computation of the first three moments of the random variable . The proof of Lemma 4.1 is elementary and thus it is omitted.

Lemma 4.1.

Let and . Then the first three moments of the random variable under the martingale measure are

Let us denote the mean of by , the standard deviation by , and the skewness by

It can be checked that first three moments of the random variable are

Then the parameters can be obtained by solving the moment matching conditions for . The following result was proven in Hu et al. [19].

Lemma 4.2.

A particular set of real-valued solution that satisfy the moment matching conditions for is given by the following functions of

where sgn is the sign function and

In view of Lemma 4.2, it is clear that the parameters are given by explicitly known functions of moments and hence also by functions of market parameters and portfolio’s weights . Furthermore, using the values of parameters from Lemma 4.2, the initial price of the basket call option can be approximated by

or, more explicitly, if

and, if

where is a standard normal random variable under the probability measure . Then the approximation for the price of the cross-currency basket call option is given by the following result, which is an immediate consequence of Theorem 2.3 in Hu et al. [19].

Lemma 4.3.

To approximate the price of the cross-currency basket put option, one can employ the classical put-call parity and hence obtain also an approximation for the price of a cross-currency EPS.

4.4. Superhedging Cost of the Buffer Cross-Currency Basket EPS

It should be acknowledged there are still some weaknesses in the concept of the static hedging strategy for a cross-currency EPS since it may be not easily available in practice. Market makers are more likely to use either a particular equity or a market index as an underlying asset for liquidly traded options, whereas bespoke options with the holder’s portfolio as the underlying asset can only be offered on OTC market. Although Corollary 4.1 shows that, in theory, a perfect static hedging of a generic EPS on a cross-currency reference portfolio is feasible, it may be difficult to implement the static hedging even for most basic cross-currency EPSs. For that reason, we will also study some superhedging strategies for cross-currency EPSs. Obviously, another viable option for the provider is to choose a stochastic model for the cross-currency market and use it to implement a dynamic hedging strategy based on actively traded assets and futures contracts on currencies.

Lemma 4.4.

The following inequalities hold, for every ,

where the first inequality is strict on the set and the second one is strict on the set

Our goal is to construct a particular superhedging strategy for the cross-currency buffer EPS by using options with the underlying assets and introduced in Sections 3.3 and 3.4. Recall that the aggregate effective return satisfies . Hence Lemma 4.4 leads to the following result.

Lemma 4.5.

The following inequalities hold, for every ,

Proof. For the first two inequalities, we observe that

and we apply Lemma 4.4. For the last two, we use the equality

and, once again, we make use of Lemma 4.4.

It is worth noting that the first inequality in Lemma 4.5 is strict on the event

and the second one is strict on

The third one is strict on the event

and the last one is strict on

Lemma 4.5 can be used to construct a particular superhedging strategy for the buffer cross-currency basket EPS. From Corollary 4.1, we obtain

where and . Hence it suffices to set and consider the contingent claim

where and are strictly positive numbers. Our goal is to find a contingent claim such that and static hedging of is feasible with relatively simple options. By combining the first inequality with the last in Lemma 4.5, we obtain

Since dominates it is clear that a replicating strategy for is also a superhedging strategy for and, in fact, it is a strict superhedging of on the event . Let us denote such a strategy by so that . Since our goal is to obtain a static trading strategy, we introduce two instances of cross-currency European call options with the payoff in the domestic currency given by

and

The following corollary to Lemma 4.5 gives a superhedging cost for the buffer cross-currency basket EPS

Corollary 4.2.

Let be a static superhedging hedging strategy for the buffer cross-currency basket EPS such that . Then the initial cost of equals

To find the closed-form expression for the superhedging cost within the cross-currency market model introduced in Section 3.2, it suffices to compute the initial model prices and of cross-currency call options. Let denote the c.d.f. of the two-dimensional standard Gaussian distribution with the correlation coefficient . We set

Proposition 4.2.

The following equality holds, for every ,

where and

Proof. Recall that and satisfy under the domestic martingale measure

with initial conditions . We observe that

where so that and . Let us introduce the probability measure equivalent to on by the Radon-Nikodym density

Then the process is a standard Brownian motion under and the dynamics of and under are

It is now easy to check that

with the parameters and are given in the statement of the lemma.

The result for is analogous Proposition 4.2, although it requires minor adjustments to the notation.

Proposition 4.3.

Proof. We have

We introduce an equivalent probability measure on by the Radon-Nikodym density

Then the process is a standard Brownian motion under and the dynamics of and under are

and thus the stated expressions are valid.

4.5. Superhedging Cost of the Floor Cross-Currency Basket EPS

Our next goal is to study a static superhedging strategy for the floor cross-currency basket EPS. Setting , we now have that

and we denote

and

The following corollary to Lemma 4.5 gives the initial cost of a static superhedging strategy for the cross-currency floor EPS.

Corollary 4.3.

The initial cost of a static superhedging strategy for the floor cross-currency basket EPS with satisfies

In view of Corollary 4.3, in order to find an explicit representation for the superhedging cost , it suffices to combine Propositions 4.2 and 4.3 with the following result.

Proposition 4.4.

The following equalities are valid, for every ,

4.6. Approximate Hedging of the Buffer Cross-Currency Basket EPS

The superhedging strategy combined with the premium ensures that the provider will never lose money and thus it can be seen as a good choice for the provider. However, the value is not necessarily competitive and may be too high for the buyer of the EPS since it does not represent an arbitrage-free price. It thus make sense to search for a less expensive hedging strategy even if it may generate a loss in some scenarios. For lack of a better term, we will refer to that situation as an approximate hedging. Of course, we would like to find an approximate hedging with some desirable properties, such as closeness to superhedging and convenience of implementation in practice.

If the indicator functions in definition of are omitted, then we obtain the claim

which coincides with on the complement of the event . On the one hand, it should be acknowledged that the claim does not dominate , in general. On the other hand, to replicate it suffices to use European options with the underlying assets and to build the hedging portfolios from Propositions 3.1 and 3.4. Then an approximate replication is obtained by combining the domestic and effective foreign static hedging strategies with weights and , respectively. Formally, the wealth of the approximate hedging strategy for the cross-currency buffer EPS satisfies

where and are given by Corollaries 3.1 and 3.4, respectively. The strategy does not satisfy the superhedging condition and thus it may result in provider’s losses in some adverse market scenarios. However, it only requires to use on simple options on reference portfolios and .

Corollary 4.4.

The initial cost of the approximate hedging strategy for the buffer cross-currency basket EPS with equals

Notice that the static hedging strategy from Corollary 4.2 has a similar structure to two separate hedging strategies from Propositions 3.1 and 3.4. The main differences between the strategy from Corollary 4.2 and separate strategies are the underlying assets and the strikes of European options used in hedging portfolios. In separate hedging strategies, the provider considers domestic equity and foreign equity independently and thus the strikes of options are only related to each economy and, as a consequence, this also applies to the combined superhedging strategy. In contrast, a static hedging strategy given by hinges on the cross-currency reference portfolio as an underlying asset and thus strikes are based on the whole portfolio.

5. Numerical Studies and Backtesting

In numerical studies based on the cross-currency market model given by (3.2), we use the model parameters from Xu et al. [35]. In particular, the volatility of the domestic portfolio is set to be , which is consistent with the level of implied volatility represented by the ASX 200 VIX index in 2024, and for the foreign portfolio the volatility is chosen to be , which is the medium value of the implied volatility of the U.S. equity options market during the same period, as measured by S&P 500 VIX index. The dividend yields are taken to be and and thus they are in accord with the dividend yields for stock indices ASX 200 and S&P 500, respectively. The exchange rate USD/AUD is set to be 1.58 (i.e., USD 1.00 costs AUD 1.58), which represent the approximate mean value of the exchange rate in April 2025, and the volatility of the exchange rate is assumed to be , which is based on the recent data for USD/AUD currency options.

Regarding the choice of correlations, it’s important to note that the relationship between the Australian and U.S. equity markets is highly sensitive to the time period and the return interval chosen. As reported in [23], from 2000 to 2018, the correlation between the daily returns on ASX 200 and S&P 500 was just 0.14. However, our numerical study analyzing historical data from 2014 to 2024 found that the correlation between the one-year trailing returns on ASX 200 and S&P 500 was 0.77. Therefore, we consider several values for the correlation between domestic and foreign equities: -0.4 (negative correlation), 0.1 (low correlation), and 0.7 (high correlation), as these provide a useful range for analysis. The correlation between the exchange rate and equity market is also a notable phenomenon, although that relationship can be complex and thus its analysis requires a strong expertise in FX market. For concreteness, we set the correlation between the domestic equity (resp., the foreign equity ) and the exchange rate to be (resp., ). This means, for example, that a falling AUD (i.e., an increasing exchange rate ) is likely to be linked with in a rising ASX 200 quote (resp., a falling S&P 500 quote), and vice versa.

To obtain the vectors of volatilities in dynamics (3.2) we introduce the correlated Brownian motions and by

| (7) |

where is a standard Brownian motion under and where we denote

| (8) |

Then the parameters used in what follows are summarised in Table 1 and they are consistent with the set of volatilities and correlations chosen above.

5.1. Model Pricing of Domestic and Foreign EPSs

| Parameter | Value |

| Domestic short-term interest rate | 4.1% |

| Foreign short-term interest rate | 4.5% |

| Dividend yields of the domestic asset | |

| Dividend yields of the foreign asset | |

| Initial exchange rate | 1.58 |

| Volatility of the domestic asset | |

| Volatility of the foreign asset | |

| Volatility of the exchange rate | |

| Correlation between two assets | |

| Correlation between the domestic asset and exchange rate | |

| Correlation between the foreign asset and exchange rate |

After defining the parameters of domestic and foreign markets, we first examine the pricing of some standard EPSs on separate domestic and foreign portfolios. We focus here on two particular instances of a standard EPS, the buffer EPS and the floor EPS, and we analyze the weighted cost for a portfolio of EPSs associated with separate hedging strategies, which were discussed in Section 3. We only consider here the case of one year maturity since the influence of maturity is likely to be similar as in the case of EPSs with a single currency, which was extensively studied by Xu et al. [35].

Table 2 presents the hedging cost and key parameters for several variants of domestic and foreign EPSs.

For brevity, we use the shorthand notation for various portfolios of domestic and foreign EPSs with all prices

expressed in the domestic currency for the notional principal equal to AUD 100:

(i) Domestic – the price of the domestic EPS (Corollary 3.2);

(ii) Nominal – the weighted cost where is the price of the foreign EPS

(Corollary 3.3);

(iii) Effective – the weighted cost where is the price of the effective foreign EPS

(Corollary 3.5);

(iv) Quanto foreign – the weighted cost where is the price of the quanto EPS (Corollary 3.6).

| Buffer | Domestic | Nominal | Effective | Quanto | |||||

|---|---|---|---|---|---|---|---|---|---|

| [1] | 50% | -5% | 5% | 0.5 | 0.5 | -0.114 | -0.874 | -0.503 | -0.995 |

| [2] | 50% | -5% | 5% | 0.8 | 0.5 | 0.421 | 0.048 | 0.197 | -0.097 |

| [3] | 20% | -5% | 10% | 0.5 | 0.5 | 0.426 | -0.167 | 0.023 | -0.327 |

| [4] | 50% | -5% | 10% | 0.5 | 0.5 | 0.426 | 0.055 | 0.174 | -0.044 |

| [5] | 80% | -5% | 10% | 0.5 | 0.5 | 0.426 | 0.277 | 0.325 | 0.238 |

| [6] | 20% | -5% | 10% | 0.8 | 0.5 | 0.961 | 0.986 | 0.822 | 0.789 |

| [7] | 50% | -5% | 10% | 0.8 | 0.5 | 0.961 | 0.976 | 0.874 | 0.853 |

| [8] | 80% | -5% | 10% | 0.8 | 0.5 | 0.961 | 0.967 | 0.926 | 0.918 |

| [9] | 50% | -5% | 10% | 0.8 | 0.8 | 0.681 | 0.088 | 0.279 | -0.071 |

| [10] | 20% | -10% | 10% | 0.8 | 0.5 | 0.070 | -0.504 | -0.217 | -0.663 |

| [11] | 50% | -10% | 10% | 0.8 | 0.5 | 0.070 | -0.289 | -0.109 | -0.388 |

| [12] | 80% | -10% | 10% | 0.8 | 0.5 | 0.070 | -0.073 | -0.002 | -0.113 |

| Floor | Domestic | Nominal | Effective | Quanto | |||||

| [1] | 50% | -5% | 5% | 0.8 | 0.5 | 0.591 | -0.410 | -0.088 | -0.518 |

| [2] | 50% | -5% | 10% | 0.5 | 0.5 | 0.532 | -0.231 | -0.004 | -0.308 |

| [3] | 20% | -5% | 10% | 0.8 | 0.5 | 1.131 | 0.152 | 0.264 | 0.013 |

| [4] | 50% | -5% | 10% | 0.8 | 0.5 | 1.131 | 0.519 | 0.589 | 0.432 |

| [5] | 80% | -5% | 10% | 0.8 | 0.5 | 1.131 | 0.886 | 0.914 | 0.851 |

| [6] | 50% | -5% | 10% | 0.8 | 0.8 | 0.851 | -0.369 | -0.006 | -0.493 |

| [7] | 50% | -10% | 10% | 0.8 | 0.5 | 2.022 | 1.784 | 1.573 | 1.674 |

| [8] | 20% | -15% | 10% | 0.5 | 0.5 | 1.330 | 0.787 | 0.700 | 0.622 |

| [9] | 50% | -15% | 10% | 0.5 | 0.5 | 1.330 | 0.991 | 0.936 | 0.888 |

| [10] | 80% | -15% | 10% | 0.5 | 0.5 | 1.330 | 1.194 | 1.172 | 1.153 |

| [11] | 20% | -15% | 10% | 0.8 | 0.5 | 2.407 | 2.513 | 1.905 | 2.307 |

| [12] | 50% | -15% | 10% | 0.8 | 0.5 | 2.407 | 2.473 | 2.093 | 2.345 |

| [13] | 80% | -15% | 10% | 0.8 | 0.5 | 2.407 | 2.434 | 2.282 | 2.382 |

| [14] | 50% | -15% | 10% | 0.8 | 0.8 | 2.127 | 1.585 | 1.498 | 1.420 |

From Table 2, the influence of protection and fee thresholds, as well as the associated participation rates, are the same for separate hedging strategies as for single currency underlying asset, which has been discussed by Xu et al. [35]. With the setting of the predetermined exchange rate equal to the initial exchange rate, we can see that the price of the quanto EPS is usually close to the price of the corresponding foreign EPS with the same parameters, for both buffer and floor EPSs. We observe that the level of the volatility for the domestic and foreign assets has a profound effect on the price of the quanto EPS.

Moreover, the prices of effective EPS has the highest values among the three weighted hedging strategies. This was expected since only the effective EPS involves the stochastic exchange rate and thus covers also the currency risk. If the weight for the domestic asset increases, then the influence of hedging costs for foreign equities decreases and thus the difference between costs of three variants of EPSs become smaller.

Example 5.1.

As an illustration of static hedging, we consider the buffer EPS No. 3 from Table 2 with the notional principal equal to one million AUD (i.e., AUD 1M) with 20% invested in domestic assets and 80% held in foreign assets. We assume that the domestic EPS and the effective foreign EPS mature in one year, have the buffer threshold with the protection rate and the fee threshold with the fee rate . It is clear that the initial prices of domestic and foreign assets are irrelevant in all pricing results (see Corollaries 3.2, 3.3, 3.5 and 3.6) but they are important when constructing the static hedging with European options. Here we assume that and correspond to market quotes of ASX 200 and S&P 500, AUD and USD, and the exchange rate .

For the domestic EPS, we find from Corollary 3.2 that the fair premium equals , which is used to establish a static hedging strategy for the domestic component of the EPS using domestic call and put options written on , as explained in Corollary 3.1. For the foreign component, we use Corollary 3.3 to find that the provider can obtain AUD 216 by building the hedging portfolio using European options written on the process with the initial value AUD. Specifically, the static hedge is composed of:

-

•

long put options with strike AUD,

-

•

short call options with strike AUD.

Hence to statically hedge the foreign component the provider needs to long units of put options with strike AUD 105.07 and short units of call options with strike AUD 121.66. The fair premium for the combined position in two EPSs equals AUD per one million of the notional principal.

5.2. Model Pricing of Basket Options

Before applying the pricing formula of cross-currency EPSs, we analyzed the two approximation methods of basket options - geometric averaging (reported as GM) and moment matching (reported as MM). Table 3 reports basket option prices for different strikes , obtained using Monte Carlo simulation as the benchmark alongside the two approximation methods. The results show that both geometric averaging and moment matching methods deliver prices very close to the simulation values, with deviations typically below across all parameter settings. This indicates that both methods are accurate and reliable for basket option valuation.

| Options | Parameters | Call() | Put() | ||||||

|---|---|---|---|---|---|---|---|---|---|

| No. | T | Simulation | GM | MM | Simulation | GM | MM | ||

| [1] | 20% | -0.4 | 1 | 0.01745 | 0.01661 | 0.01742 | 0.09695 | 0.09611 | 0.09691 |

| [2] | 20% | 0.1 | 1 | 0.02041 | 0.01993 | 0.02040 | 0.09995 | 0.09943 | 0.09990 |

| [3] | 20% | 0.7 | 1 | 0.02390 | 0.02373 | 0.02393 | 0.10350 | 0.10323 | 0.10343 |

| [4] | 50% | -0.4 | 1 | 0.00468 | 0.00418 | 0.00468 | 0.09003 | 0.0895 | 0.0900 |

| [5] | 50% | 0.1 | 1 | 0.00991 | 0.00958 | 0.00993 | 0.09529 | 0.09490 | 0.09525 |

| [6] | 50% | 0.7 | 1 | 0.01603 | 0.01587 | 0.01609 | 0.10145 | 0.10118 | 0.10140 |

| [7] | 80% | -0.4 | 1 | 0.00402 | 0.00385 | 0.00403 | 0.09523 | 0.09499 | 0.09517 |

| [8] | 80% | 0.1 | 1 | 0.00707 | 0.00704 | 0.00709 | 0.09829 | 0.09818 | 0.09824 |

| [9] | 80% | 0.7 | 1 | 0.01096 | 0.01093 | 0.01099 | 0.10219 | 0.10207 | 0.10214 |

| [10] | 20% | -0.4 | 2 | 0.03855 | 0.03692 | 0.03852 | 0.09870 | 0.09706 | 0.09867 |

| [11] | 20% | 0.1 | 2 | 0.04327 | 0.04226 | 0.04326 | 0.10347 | 0.10240 | 0.10341 |

| [12] | 20% | 0.7 | 2 | 0.04865 | 0.04824 | 0.04871 | 0.10895 | 0.10839 | 0.10885 |

| [13] | 80% | -0.4 | 2 | 0.01179 | 0.01146 | 0.01186 | 0.09463 | 0.09420 | 0.09461 |

| [14] | 80% | 0.1 | 2 | 0.01774 | 0.01762 | 0.01780 | 0.10059 | 0.10037 | 0.10055 |

| [15] | 80% | 0.7 | 2 | 0.02458 | 0.02445 | 0.02465 | 0.10745 | 0.10719 | 0.10740 |

| Options | Parameters | Call() | Put() | ||||||

| No. | T | Simulation | GM | MM | Simulation | GM | MM | ||

| [1] | 20% | -0.4 | 1 | 0.05265 | 0.05239 | 0.05262 | 0.03616 | 0.03590 | 0.03613 |

| [2] | 20% | 0.1 | 1 | 0.05650 | 0.05629 | 0.05649 | 0.04006 | 0.03980 | 0.04000 |

| [3] | 20% | 0.7 | 1 | 0.06069 | 0.06061 | 0.06073 | 0.04431 | 0.04413 | 0.04424 |

| [4] | 50% | -0.4 | 1 | 0.03344 | 0.03307 | 0.03347 | 0.02281 | 0.02240 | 0.02281 |

| [5] | 50% | 0.1 | 1 | 0.04197 | 0.04171 | 0.04199 | 0.03137 | 0.03104 | 0.03133 |

| [6] | 50% | 0.7 | 1 | 0.05008 | 0.04997 | 0.05013 | 0.03951 | 0.03931 | 0.03947 |

| [7] | 80% | -0.4 | 1 | 0.03051 | 0.03054 | 0.03056 | 0.02573 | 0.02570 | 0.02572 |

| [8] | 80% | 0.1 | 1 | 0.03627 | 0.03624 | 0.03631 | 0.03150 | 0.03140 | 0.03147 |

| [9] | 80% | 0.7 | 1 | 0.04206 | 0.04205 | 0.04212 | 0.03731 | 0.03721 | 0.03728 |

| [10] | 20% | -0.4 | 2 | 0.07752 | 0.07686 | 0.07749 | 0.04554 | 0.04487 | 0.04551 |

| [11] | 20% | 0.1 | 2 | 0.08275 | 0.08220 | 0.08274 | 0.05082 | 0.05021 | 0.05076 |

| [12] | 20% | 0.7 | 2 | 0.08838 | 0.08814 | 0.08845 | 0.05655 | 0.05615 | 0.05647 |

| [13] | 80% | -0.4 | 2 | 0.04288 | 0.04290 | 0.04297 | 0.03359 | 0.03352 | 0.03359 |

| [14] | 80% | 0.1 | 2 | 0.0508 | 0.05067 | 0.05086 | 0.04152 | 0.04129 | 0.04148 |

| [15] | 80% | 0.7 | 2 | 0.05871 | 0.05860 | 0.05881 | 0.04946 | 0.04922 | 0.04943 |

When comparing the two approaches, the moment matching method consistently produces prices that are slightly closer to the Monte Carlo benchmark than geometric averaging method, for both call and put options across all strikes. In contrast, geometric averaging method tends to slightly underestimate call prices and, in some cases, overestimate puts relative to the benchmark. Although the deviations are small, the systematic pattern indicates that MM more accurately captures the distributional characteristics of the basket and better reflects the hedging costs of these options.

The superior performance of moment matching method can be attributed to its use of higher-order moments to approximate the distribution of the basket, which allows it to more precisely replicate both the variance and skewness of the underlying assets. geometric averaging method, while computationally simpler, relies on a geometric mean approximation that may slightly distort the distribution, particularly when asset correlations and weights create asymmetry in the basket payoff. Despite this, both methods remain efficient and produce results very close to the benchmark simulation, making them suitable for practical applications.

Overall, although both geometric averaging and moment matching methods are accurate and computationally efficient, the moment matching method demonstrates a clear advantage in replicating Monte Carlo prices. This systematic edge makes moment matching method the preferred choice for basket option approximation in subsequent cross-currency EPS pricing, ensuring greater precision in both valuation and hedging analysis.

5.3. Model Pricing of Cross-Currency EPSs

Using once again the data reported in Table 1 we now analyze model prices of cross-currency and quanto EPSs, as given by Corollary 4.1. Recall that in both cases we deal with European basket options on domestic returns combined with either effective or quanto foreign returns. Since closed-form solutions for basket options with arithmetic averaging are not available in a lognormal model, we use instead four numerical approaches, which were studied in Section 4:

(i) Simulation – the Monte Carlo method applied to payoffs of various kinds of EPSs;

(ii) Geometric – the closed-form solutions for basket options with geometric averaging, which were obtained in Propositions 4.1 for effective;

(iii) Moments – the approximate prices obtained by the moment matching method for the cross-currency EPS from Lemma 4.3;

(iv) Super – the superhedging costs and from Corollaries 4.2 and 4.3.

| Buffer | Simulation | Geometric | Moments | Super | ||||

|---|---|---|---|---|---|---|---|---|

| [1] | 50% | -0.4 | -5% | 5% | -0.045 | -0.091 | -0.112 | 1.474 |

| [2] | 80% | -0.4 | -5% | 5% | 0.111 | 0.096 | 0.081 | 1.228 |

| [3] | 50% | 0.7 | -5% | 5% | 0.249 | 0.163 | 0.159 | 0.439 |

| [4] | 80% | 0.7 | -5% | 5% | 0.341 | 0.304 | 0.304 | 0.361 |

| [5] | 50% | -0.4 | -5% | 10% | 0.416 | 0.385 | 0.369 | 1.767 |

| [6] | 80% | -0.4 | -5% | 10% | 0.533 | 0.526 | 0.511 | 1.508 |

| [7] | 50% | 0.1 | -5% | 10% | 0.674 | 0.617 | 0.610 | 1.496 |

| [8] | 80% | 0.1 | -5% | 10% | 0.738 | 0.710 | 0.712 | 1.263 |

| [9] | 50% | 0.7 | -5% | 10% | 0.910 | 0.840 | 0.836 | 0.973 |

| [10] | 80% | 0.7 | -5% | 10% | 0.923 | 0.893 | 0.893 | 0.927 |

| [11] | 50% | 0.1 | -10% | 10% | -0.098 | -0.124 | -0.140 | 0.513 |

| [12] | 80% | 0.1 | -10% | 10% | -0.013 | -0.028 | -0.029 | 0.335 |

| [13] | 50% | 0.7 | -10% | 10% | -0.051 | -0.096 | -0.105 | 0.210 |

| [14] | 80% | 0.7 | -10% | 10% | 0.023 | 0.005 | 0.003 | 0.101 |

| Floor | Simulation | Geometric | Moments | Super | ||||

| [1] | 50% | -0.4 | -5% | 5% | 0.608 | 0.543 | 0.538 | 2.893 |

| [2] | 50% | 0.7 | -5% | 5% | 0.107 | 0.040 | 0.036 | 0.679 |

| [3] | 50% | -0.4 | -5% | 10% | 1.068 | 1.019 | 1.019 | 3.187 |

| [4] | 80% | -0.4 | -5% | 10% | 1.190 | 1.167 | 1.169 | 3.001 |

| [5] | 50% | 0.7 | -5% | 10% | 0.769 | 0.717 | 0.713 | 1.513 |

| [6] | 80% | 0.7 | -5% | 10% | 1.016 | 0.995 | 0.993 | 1.668 |

| [7] | 50% | -0.4 | -10% | 10% | 1.589 | 1.509 | 1.519 | 3.328 |

| [8] | 50% | 0.7 | -10% | 10% | 1.730 | 1.653 | 1.654 | 2.156 |

| [9] | 20% | -0.4 | -15% | 10% | 1.997 | 1.857 | 1.859 | 3.596 |

| [10] | 50% | -0.4 | -15% | 10% | 1.715 | 1.628 | 1.637 | 3.348 |

| [11] | 80% | -0.4 | -15% | 10% | 1.914 | 1.880 | 1.878 | 3.099 |

| [12] | 20% | 0.1 | -15% | 10% | 2.05 | 1.908 | 1.912 | 3.265 |

| [13] | 50% | 0.1 | -15% | 10% | 2.042 | 1.948 | 1.954 | 3.917 |

| [14] | 80% | 0.1 | -15% | 10% | 2.155 | 2.115 | 2.117 | 3.198 |

| [15] | 50% | 0.7 | -15% | 10% | 2.216 | 2.124 | 2.127 | 2.437 |

| [16] | 80% | 0.7 | -15% | 10% | 2.323 | 2.282 | 2.284 | 2.359 |

| Buffer | Simulation | Geometric | Moments | Super | ||||

|---|---|---|---|---|---|---|---|---|

| [1] | 50% | -0.4 | -5% | 5% | -0.182 | -0.221 | -0.247 | 1.974 |

| [2] | 80% | -0.4 | -5% | 5% | 0.045 | 0.035 | 0.016 | 1.442 |

| [3] | 50% | 0.7 | -5% | 5% | 0.068 | -0.016 | -0.020 | 0.307 |

| [4] | 80% | 0.7 | -5% | 5% | 0.267 | 0.230 | 0.231 | 0.149 |

| [5] | 50% | -0.4 | -5% | 10% | 0.295 | 0.272 | 0.251 | 2.299 |

| [6] | 80% | -0.4 | -5% | 10% | 0.465 | 0.466 | 0.445 | 1.727 |

| [7] | 50% | 0.1 | -5% | 10% | 0.531 | 0.478 | 0.470 | 1.979 |

| [8] | 80% | 0.1 | -5% | 10% | 0.672 | 0.646 | 0.646 | 1.466 |

| [9] | 50% | 0.7 | -5% | 10% | 0.752 | 0.683 | 0.679 | 1.333 |

| [10] | 80% | 0.7 | -5% | 10% | 0.856 | 0.825 | 0.826 | 0.986 |

| [11] | 50% | 0.1 | -10% | 10% | -0.174 | -0.195 | -0.213 | 0.737 |

| [12] | 80% | 0.1 | -10% | 10% | -0.042 | -0.055 | -0.057 | 0.435 |

| [13] | 50% | 0.7 | -10% | 10% | -0.153 | -0.195 | -0.205 | 0.092 |

| [14] | 80% | 0.7 | -10% | 10% | -0.014 | -0.032 | -0.033 | 0.045 |

| Floor | Simulation | Geometric | Moments | Super | ||||

| [1] | 50% | -0.4 | -5% | 5% | 0.492 | 0.427 | 0.421 | 3.716 |

| [2] | 50% | 0.7 | -5% | 5% | 0.002 | -0.064 | -0.069 | 0.743 |

| [3] | 50% | -0.4 | -5% | 10% | 0.969 | 0.919 | 0.919 | 4.041 |

| [4] | 80% | -0.4 | -5% | 10% | 1.152 | 1.129 | 1.132 | 3.363 |

| [5] | 50% | 0.7 | -5% | 10% | 0.686 | 0.636 | 0.630 | 1.769 |

| [6] | 80% | 0.7 | -5% | 10% | 0.988 | 0.967 | 0.965 | 1.805 |

| [7] | 50% | -0.4 | -10% | 10% | 1.409 | 1.329 | 1.340 | 4.242 |

| [8] | 50% | 0.7 | -10% | 10% | 1.592 | 1.515 | 1.515 | 2.707 |

| [9] | 20% | -0.4 | -15% | 10% | 1.715 | 1.580 | 1.579 | 5.065 |

| [10] | 50% | -0.4 | -15% | 10% | 1.502 | 1.416 | 1.425 | 4.270 |

| [11] | 80% | -0.4 | -15% | 10% | 1.807 | 1.778 | 1.771 | 3.475 |

| [12] | 20% | 0.1 | -15% | 10% | 1.775 | 1.634 | 1.636 | 4.636 |

| [13] | 50% | 0.1 | -15% | 10% | 1.848 | 1.754 | 1.761 | 3.917 |

| [14] | 80% | 0.1 | -15% | 10% | 2.065 | 2.024 | 2.026 | 3.198 |

| [15] | 50% | 0.7 | -15% | 10% | 2.037 | 1.943 | 1.946 | 3.127 |

| [16] | 80% | 0.7 | -15% | 10% | 2.242 | 2.201 | 2.203 | 2.650 |

In Table 4 (resp., Table 5) we report prices of cross-currency EPSs (resp., quanto EPSs) for AUD 100 notional principal computed using four alternative numerical approaches. The Monte Carlo estimates are based on one million simulations and thus the prices of cross-currency basket options, and hence also the prices of cross-currency EPSs, obtained through simulation are considered to be exact values. It is clear that the three numerical approaches for the hedging costs - simulation, geometric averaging, and three moment matching - provide very close results, with no more than 0.01% difference in most cases. We also note that, when compared with the three moment matching method, the geometric average approximation provides prices closer to the exact prices obtained by the Monte Carlo method in most cases. Moreover, the hedging costs under three moment matching method are usually lower than the exact costs, for both the buffer and floor EPS. As was expected, the superhedging prices are always higher than the exact prices since the terminal value of a superhedging strategy dominates the payoff of an EPS and the market model is arbitrage-free.

It should be noted that the prices of cross-currency and quanto EPSs with identical protection and fee parameters are very close. This is due to the fact that we use a quanto exchange rate and the volatility of the exchange rate is relatively small (as compared to the volatilities of equities), so that the influence of the exchange rate is also relatively small. Of course, if a holder chooses a predetermined exchange rate markedly different from its current value then the prices of cross-currency and quanto EPSs would be markedly different. It is worth noting that in Tables 4 and 5 the prices of cross-currency EPSs are higher than that of quanto EPSs when dealing with both buffer EPSs and floor EPSs, because the protection of a cross-currency EPS is more comprehensive than that of a quanto EPS with identical parameters.

Comparing hedging and superhedging strategies, it is clear that a superhedging cost, which is reported as Super in Tables 4 and 5, dominates the cost of a respective hedging and quanto hedging strategy in all cases. This result is consistent with the property that the superhedging strategy covers more than the overall provider’s gains or losses and thus it should cost more than the respective hedging strategy.

Moreover, the structure of EPS products influences the difference between hedging and superhedging costs. We can see that the difference between hedging and superhedging costs for the floor EPS is higher than for the buffer EPS for both cross-currency and quanto EPS. Since the floor EPS has a more complex structure than the buffer EPS it needs more long and short positions in European options to hedge the respective final payoff and this increases the costs rapidly when applying superhedging strategies.

Example 5.2.

As an example of a cross-currency EPS, we consider the floor EPS No. 6 from Table 4 with the notional principal one million AUD (i.e., AUD 1M), in which 80% invested in domestic assets and 20% held in foreign assets. The buffer threshold equals with participation rate and the fee threshold equals with participation rate . As usual, the maturity date is taken to be . As shown in Section 5, assume the correlation between two assets is , the arbitrage-free premium for the EPS equals AUD 10160.

We first note that AUD. Hence a static hedging portfolio with European options written on involves:

-

•

short put options with strike ,

-

•

long put options with strike ,

-

•

short call options with strike .

The provider needs to short units of put options with strike 97.014, long units of put options with strike 102.12, and short units of call options with strike 112.332.

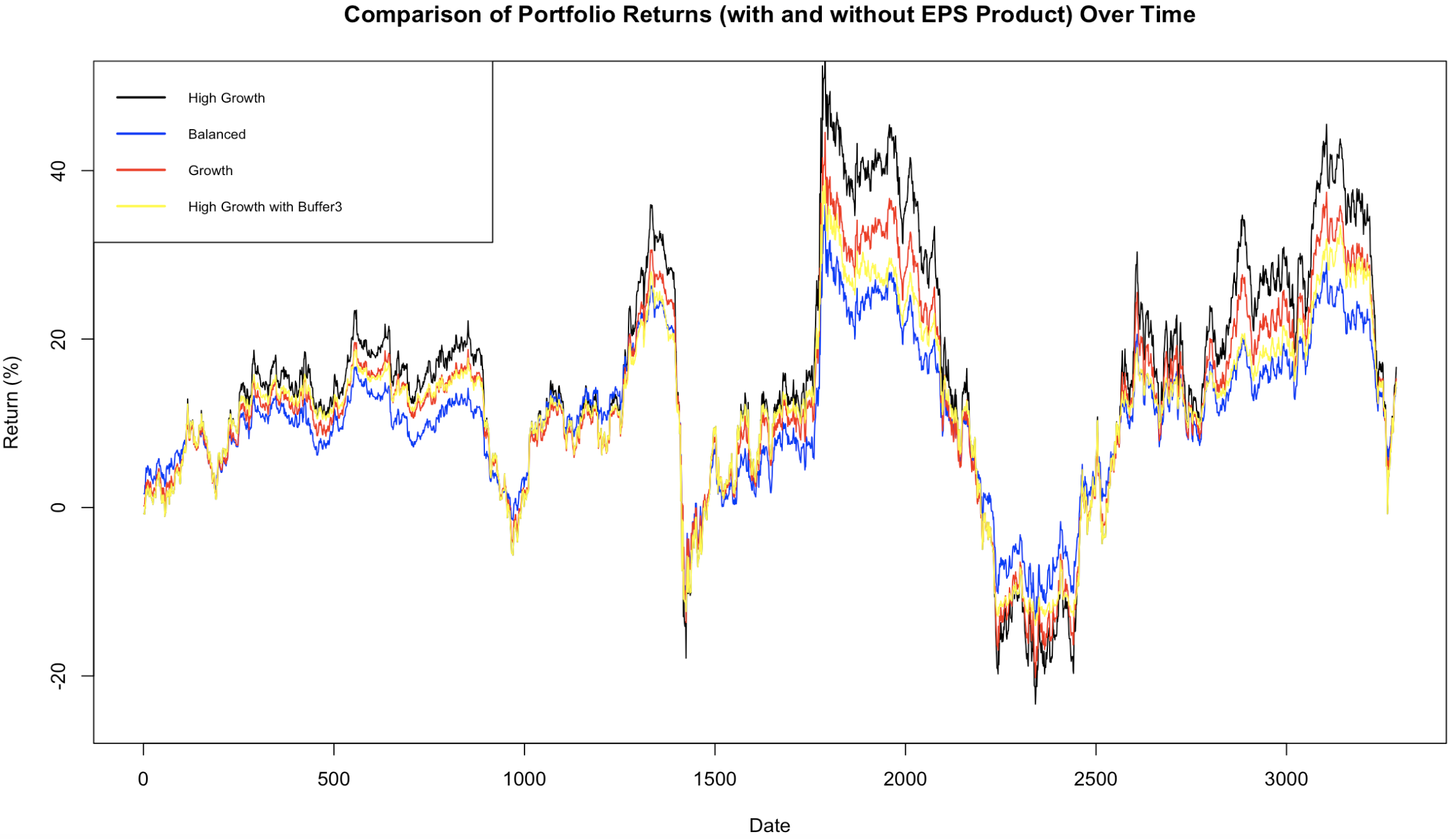

5.4. Backtesting of Aggregated Cross-Currency EPS

We now present a backtesting framework for the cross-currency EPS product. From UniSuper, we obtain daily cumulative historical returns for the Balanced, Growth, and High Growth portfolios from May 1, 2015, to April 30, 2025, along with daily returns for Australian shares, international shares, and cash. Additionally, we utilize daily closing prices of the S&P 500 and ASX 200 indices to align with the daily returns of international and Australian shares, respectively. We compute the correlations between the weekly returns of Australian shares and the ASX 200 index, and between international shares and the S&P 500 index. Both correlations exceed 0.9, suggesting that these indices are appropriate proxies for simulating the historical returns of Australian and international shares in the UniSuper portfolios.

Our analysis assumes that a cohort of investors enters into one-year EPS contracts of a specific type on each trading day, with all contracts initiated on the same day having the same notional principal. Considering one-year EPS contracts initiated from May 1, 2015, to April 30, 2024, we generate 3288 one-year trailing returns for the Balanced, Growth, and High Growth portfolios. We apply the cross-currency basket EPS contracts to the High Growth portfolio to assess the effect of loss protection. The EPS-adjusted one-year trailing returns are then compared to the original realized returns of the Balanced, Growth, and High Growth portfolios.

According to UniSuper [33], the High Growth portfolio consists of Australian shares, international shares, infrastructure and private equity, and property. For simplicity, we assume that of the portfolio is allocated to cash, with the remaining allocation invested in Australian and international shares.