On the optimal objective value of random linear programs

Abstract

We consider the problem of maximizing subject to the constraints , where , is an matrix with mutually independent centered subgaussian entries of unit variance, and is a cost vector of unit Euclidean length. In the asymptotic regime , , and under some mild assumptions on , we prove that the optimal objective value of the linear program satisfies

In the context of high-dimensional convex geometry, our findings imply sharp asymptotic bounds on the spherical mean width of the random convex polyhedron . We provide numerical experiments as supporting data for the theoretical predictions. Further, we carry out numerical studies of the limiting distribution and the standard deviation of .

1 Introduction

1.1 Problem setup and motivation

Consider the linear program (LP)

| (1) |

where the entries of the coefficient matrix are mutually independent random variables, and denotes the vector of all ones. Note that is a vector of free variables. In this note we deal with two settings: either is a non-random unit vector or is random uniformly distributed on the unit Euclidean sphere. For any realization of the above LP is feasible since the zero vector satisfies all the constraints. We denote the value of the objective function of (1) by , the optimal objective value by , and any optimal solution by .

The main problem we would like to address here is the following: Under the assumption that the number of constraints is significantly larger than the number of variables, what is the magnitude of the optimal objective value?

We provide theoretical guarantees on the optimal objective value in the asymptotic regime , , and carry out empirical studies which confirm that medium size random LPs (with the number of constraints in the order of a few thousands) closely follow theoretical predictions. The numerical experiments further allow us to formulate conjectures related to the distribution of the optimal objective value, which we hope to address in future works.

Our interest in LP (1) is twofold.

-

(i)

The LP (1) with i.i.d random coefficients can be viewed as the simplest model of an “average-case” linear program. LP of this form has been considered in the mathematical literature in the context of estimating the average-case complexity of the simplex method [7, 9, 8] (see Subsection 1.4 below for a more comprehensive literature review). Despite significant progress in that direction, fundamental questions regarding properties of random LPs remain open [44, Section 6]. The results obtained in this note contribute to better understanding of the geometry of random feasible regions defined as intersections of independent random half-spaces. We view our work as a step towards investigating random LPs allowing for sparse, inhomogeneous and correlated constraints, which would serve as more realistic models of linear programs occurring in practice.

-

(ii)

Assuming that the cost vector is uniformly distributed on the unit sphere and is independent from , the quantity

(where is the expectation taken with respect to the randomness of ) is the spherical mean width of the random polyhedron . The mean width is a classical parameter associated with a convex set; in particular, , where is the polar body for defined as the convex hull of the rows of , and is the average value of the Minkowski functional for on the unit Euclidean sphere,

The mean width plays a key role in the study of projections of convex bodies and volume estimates (see, in particular, [50, Chapters 9–11] and [40]). The existing body of work (which we revise in Subsection 1.4) has focused on the problem of estimating the mean width up to a constant multiple. In this paper, we provide sharp asymptotics of in the regime of parameters mentioned above.

1.2 Notation

In the course of the note we use the letter (with subscripts) for constant numbers and , , , for standard asymptotic notations. Specifically, for positive functions and defined on positive real numbers, if there exists and a real number such that for all , and if . Further,

Definition 1.1.

A random variable is –subgaussian if

The smallest satisfying the above inequality is the subgaussian moment of (see, for example, [50, Chapter 2]). We will further call a random vector with mutually independent components –subgaussian if every component is –subgaussian. Examples of subgaussian variables include Rademacher (i.e symmetric ) random variables, and, more generally, any bounded random variables. The Rademacher distribution is of interest to us since a matrix with i.i.d entries produces a simplest model of a normalized system of constraints with discrete bounded coefficients.

1.3 Theoretical guarantees

In this paper, we study asymptotics of the optimal objective value of (1) in the regime when the number of free variables tends to infinity. We will further assume that the number of constraints is infinitely large compared to , i.e (while the setting is of significant interest, it is not covered by our argument).

The main result of this note is

Theorem 1.2 (Main result: asymptotics of in subgaussian setting).

Let . Assume that , and that for each , the entries of the coefficient matrix are mutually independent centered –subgaussian variables of unit variances. Assume further that the non-random unit cost vectors satisfy . Then for any constant , we have

and, in particular, almost surely.

Remark.

Distributional invariance under rotations makes analysis of Gaussian random polytopes considerably simpler. In the next theorem, we avoid any structural assumptions on the cost vectors, and thereby remove any implicit upper bounds on :

Theorem 1.3 (Asymptotics of in Gaussian setting).

Assume that and that for each , the entries of the coefficient matrix are mutually independent standard Gaussian variables. For each , let be a non-random unit cost vector. Then for any constant we have

In particular, almost surely.

As we mentioned before, the setting when the cost vector is uniform on the Euclidean sphere is of special interest in the field of convex geometry since the quantity (where denotes the expectation taken with respect to ) is the spherical mean width of the random polyhedron . As corollaries of Theorems 1.2 and 1.3, we obtain

Corollary 1.4 (The mean width in subgaussian setting).

Let , let matrices be as in Theorem 1.2, and assume additionally that . Then the spherical mean width of the polyhedron satisfies

Corollary 1.5 (The mean width in Gaussian setting).

Let and be as in Theorem 1.3. Then the spherical mean width of the polyhedron satisfies

1.4 Review of related literature

1.4.1 Convex feasibility problems

In the setting of Theorem 1.2, existence of a feasible vector with is equivalent to the statement that the intersection of random convex sets

is non-empty. The sets can be naturally viewed as independent random affine subspaces of the hyperplane and, with that interpretation, the above question is a relative of the spherical perceptron problem, in which the object of interest is the intersection of random affine halfspaces of the form , for independent random vectors and a constant parameter (see [46, 47] for a comprehensive discussion). Our proof of the lower bound on (equivalently, showing that ) is based on an iterative process which falls under the umbrella of the block-iterative projection methods.

The problem of constructing or approximating a vector in the non-empty intersection of a given collection of convex sets has been actively studied in optimization literature. The special setting where the convex sets are affine hyperplanes or halfspaces, corresponding to solving systems of linear equations and inequalities, was first addressed by Kaczmarz [28], Agmon [1], Motzkin and Schoenberg [37]. We refer, among others, to papers [48, 2, 45, 17, 38, 11, 34, 25, 31, 27, 14, 5, 35, 39, 24, 33, 51, 36, 52, 53] for more recent developments and further references. In particular, the work [2] introduced the block-iterative projection methods for solving the feasibility problems, when each update is computed as a function of projections onto a subset of constraints.

In view of the numerous earlier results cited above, we would like to epmhasize that the goal of our construction is verifying that the intersection is non-empty with high probability rather than approximating a solution to a problem which is known to be feasible in advance. Since we aim to get asymptotically sharp bounds on , we have to rely on high-precision analysis of constraint’s violations, not allowing for any significant losses in our estimates. To our best knowledge, no existing results on the block-iterative projection methods addresses the problem considered here.

1.4.2 Random linear programs

Linear programs with either the coefficient matrix or the right hand side generated randomly, have been actively studied in various contexts:

-

•

Average-case analysis. As we mentioned above, the setting of random LPs with the Gaussian coefficient matrix (or, more generally, a matrix with independent rows having spherically symmetric distributions) was considered by Borgwardt [7, 9, 8] in the context of estimating the average-case complexity of the shadow simplex method. The average-case complexity of the Dantzig algorithm was addressed by Smale in [43] (see also [6]).

- •

- •

-

•

Random integer feasibility problems. We refer to [10] for the problem of integer feasibility in the randomized setting.

-

•

The optimal objective value of LPs with random cost vectors [16].

1.4.3 The mean width of random polyhedra

As we have mentioned at the beginning of the introduction, the mean width of random polytopes has been studied in the convex geometry literature, although much of the work deals with the mean width of the convex hulls of random vectors i.e of the polars to the random polyhedra considered in the present work. We refer, in particular, to [13, 3, 21] for related results (see also [22, 23]).

A two-sided bound on the mean width in the i.i.d subgaussian setting was derived in [30] (see also [20] for earlier results); specifically, it was shown that under the assumption that the entries of are i.i.d subgaussian variables of zero mean and unit variance, the mean width of the symmetric polyhedron satisfies

| (2) |

with high probability, where the constants depend on the subgaussian moment of the matrix entries. The argument in [30] heavily relies on results which introduce suboptimal constant multiples to the estimate of , and we believe that it cannot be adapted to derive an asymptotically sharp version of (2) which is one of the goals of the present work.

1.5 Organization of the paper

We derive Theorem 1.2 and Corollary 1.4 as a combination of two separate statements: a lower bound on obtained in Section 3, and a matching upper bound treated in Section 4. The lower bound on (Theorem 3.1) is in turn obtained by combining a moderate deviations estimate from Proposition 2.5 and an iterative block-projection algorithm for constructing a feasible solution which was briefly mentioned before. The upper bound on (Theorem 4.1) proved in Section 4 relies on moderate deviations Proposition 2.6 and a special version of a covering argument.

The Gaussian setting (Theorem 1.3 and Corollary 1.5) is considered in Section 5. Finally, results of numerical simulations are presented in Section 6.

The diagrams below provide a high-level structure of the proofs of the main results of the paper.

2 Preliminaries

2.1 Compressible and incompressible vectors

Definition 2.1 (Sparse vectors).

A vector in is –sparse for some if the number of non-zero components in is at most .

Definition 2.2 (Compressible and incompressible vectors, [42]).

Let be a unit vector in , and let . The vector is called –compressible if the Euclidean distance from to the set of –sparse vectors is at most , that is, if there is a –sparse vector such that . Otherwise, is –incompressible.

Observe that a vector is –compressible if and only if the sum of squares of its largest (by the absolute value) components is at least .

2.2 Standard concentration and anti-concentration for subgaussian variables

The following result is well known, see for example [50, Section 3.1].

Proposition 2.3.

Let be a vector in with mutually independent centered –subgaussian components of unit variance. Then for every ,

where the constant depends only on .

The next proposition is an example of Paley–Zygmund–type inequalities, and its proof is standard (we provide the proof for completeness).

Proposition 2.4.

For any there is depending only on with the following property. Let be a centered –subgaussian variable of unit variance. Then

Proof.

Since is –subgaussian, all moments of are bounded, and, in particular, for some depending only on . Applying the Paley–Zygmund inequality, we get

| (3) |

Let be the largest number in such that

We will show by contradiction that . Assume the contrary. Then implying, in view of (3),

On the other hand,

We conclude that leading to contradiction. ∎

Remark.

Instead of the requirement that the variable is subgaussian in the above proposition, we could use the assumption for a fixed .

2.3 Moderate deviations for linear combinations

In this section we are interested in upper and lower bounds on probabilities

where is a fixed vector and are mutually independent centered subgaussian variables of unit variances. Under certain assumptions on and , the probability bounds match (up to term in the power of exponent) those in the Gaussian setting. The estimates below are examples of moderate deviations results for sums of mutually independent variables (see, in particular, [15, Section 3.7]), and can be obtained with help of standard Bernstein–type bounds and the change of measure method. However, we were not able to locate the specific statements that we need in the literature, and provide proofs for completeness.

Proposition 2.5 (Moderate deviations: upper bound).

Let , , be a sequence of numbers such that . For each , let be a non-random unit vector in , and assume that for every there is such that is –incompressible (in ) for all . Fix any , and for each let be mutually independent –subgaussian variables of zero mean and unit variance. Then for every there is such that

Proof.

Throughout the proof, we assume that are fixed. Let . We have, by Markov’s inequality,

| (4) |

Since has zero mean and unit variance, for every we have

| (5) |

Hence, for all such that ,

| (6) |

where the implicit constant in depends on only. On the other hand, for every we can write (see, in particular, [50, Section 2.5])

for some depending only on . Next, by the assumptions on incompressibility of the cost vectors , for every there is such that for all , the sum of squares of largest (by the absolute value) components of does not exceed . Note that every component of larger than must necessarily be among the largest components. Therefore, we obtain that for all ,

The last assertion can be written in a more compact form using asymptotic notation as follows: there is a sequence of numbers , , converging to zero as , such that

Applying (4), (5), (6), and the last relation, we then get

The result follows. ∎

Proposition 2.6 (Moderate deviations: lower bound).

Let , , be a sequence of numbers such that . For each integer , let be a non-random unit vector in , and assume that . Fix any , and for each , let be mutually independent –subgaussian variables of zero mean and unit variance. Then for every there is with

Proof.

Fix and . We shall apply the standard technique of change of measure. Define . For each , let

| (7) |

where the estimate on the right hand side is due to the assumptions , , . For every , let be a random variable defined via its cumulative distribution function

where is the probability measure on induced by , and such that are mutually independent. Denote by the set of all vectors in such that . We have

| (8) |

To estimate , we will compute the means and the variances of . Using Taylor’s expansion of , we get

where for the last identity we again used that , together with the assumption that is subgaussian. Similarly, we compute

Thus, in view of (7) and the definition of ,

and

It follows from the Markov–Chebyshev inequality and the definition of that , and thus, by (8),

To complete the proof, it remains to note that, in view of (7),

∎

3 The lower bound on in subgaussian setting

The main result of this section is

Theorem 3.1 (Lower bound on ).

Let , and let be a sequence of positive integers with . For each , let be an coefficient matrix with mutually independent centered –subgaussian entries of unit variance. Assume further that the non-random unit cost vectors satisfy

| for every there is such that for all , | ||

| is –incompressible. |

Let be the optimal objective value of random LP (1). Then for every constant , we have

In particular, almost surely.

Remark.

Although the assumptions on the cost vectors in Theorem 3.1 may appear excessively technical, we conjecture that they are optimal in the following sense: whenever there is such that is –compressible for infinitely many , there is (independent of ) and a sequence of random matrices with mutually independent centered entries of unit variances and subgaussian moments bounded by , such that almost surely.

Remark.

As a simple sufficient condition on to satisfy assumptions of the above theorem, one may require that .

We refer to Section 6.2 for numerical experiments regarding the assumptions on the cost vectors.

As we mentioned in the introduction, the main idea of our proof of Theorem 3.1 is to construct a feasible solution to the LP (1) satisfying via an iterative process. We start by defining a vector as the multiple of the cost vector . Our goal is to add a perturbation to which would restore its feasibility. We shall select a vector which would repair the constraints violated by , i.e for all with . The vector may itself introduce some constraints’ violation; to repair those constraints, we will find another vector , and consider , etc. At –th iteration, the vector will be chosen as a linear combination of the matrix rows having large scalar products with . The process continues for some finite number of steps which depends on the values of and . We shall prove that the resulting vector is feasible with high probability. To carry this argument over, we start with a number of preliminary estimates concerning subgaussian vectors as well as certain estimates on the condition numbers of random matrices.

We write for the set of integers . Further, given a finite subset of integers , we write for the linear real space of –dimensional vectors with components indexed over . Given a set or an event , we will write for the indicator of the set/event.

3.1 Auxiliary results

Proposition 2.3 and a simple union bound argument yields

Corollary 3.2.

For every there is a number depending only on with the following property. Let , let be a –set, and let be a random vector in with mutually independent centered –subgaussian components of unit variance. Then the event

| The number of indices with is at most , and | |||

has probability as least .

Proof.

Set

where is chosen sufficiently large (the specific requirements on can be extracted from the argument below). Since the vector is subgaussian, every component of satisfies

for some depending only on . Hence, the probability that more than components of are greater than , can be estimated from above by

| (9) |

If is chosen so that then the last expression in (9) is bounded above by .

Similarly to the above and assuming is sufficiently large, in view of Proposition 2.3, for any choice of a –subset , the probability that the vector has the Euclidean norm greater than , is bounded above by

Combining the two observations, we get the result. ∎

Our next observation concerns random matrices with subgaussian entries. Recall that the largest and smallest singular values of an () matrix are defined by

and

Proposition 3.3.

For every there are depending only on with the following property. Let and let be an random matrix with mutually independent centered subgaussian entries of unit variance and subgaussian moment at most . Further, let be a non-random projection operator of rank i.e is the orthogonal projection onto an –dimensional subspace of . Then

Proof.

We will assume that the aspect ratio is sufficiently large (the value can be extracted from the proof below). Let be the unit vector in the null space of (note that it is determined uniquely up to changing the sign).

Fix any unit vector . Then the random vector has mutually independent components of unit variance, and is subgaussian, with the subgaussian moment of the components depending only on (see [50, Section 2.6]). Applying Proposition 2.3, we get

| (10) |

where only depends on . Since the projection operator acts as a contraction we have everywhere on the probability space. On the other hand, , where, again according to [50, Section 2.6], is a subgaussian random variable with the subgaussian moment only depending on , and therefore

| (11) |

Combining (10) and (11), we get

for some depending only on .

The rest of the proof of the proposition is based on the standard covering argument (see, for example, [50, Chapter 4]), and we only sketch the idea. Consider a Euclidean –net on (for a sufficiently small constant ) i.e a non-random discrete subset of the Euclidean sphere such that for every vector in there is some vector in at distance at most from . It is known that can be chosen to have cardinality at most [50, Section 4.2]. In view of the last probability estimate, the event

has probability at least . Everywhere on that event, we have (see [50, Section 4.4])

and

and, in particular,

assuming that is a sufficiently small positive constant. It remains to note that, as long as the aspect ratio is sufficiently large, the quantity is exponentially small in . ∎

Remark.

It can be shown that and with probability exponentially close to one for arbitrary constant as long as is sufficiently large.

Corollary 3.4.

For every there are depending only on with the following property. Let , and let be a non-random orthogonal projection of rank . Further, let be independent random vectors in with mutually independent centered –subgaussian components of unit variance. Let be any non-random vector in . Then with probability there is the unique vector in the linear span of such that

| (12) |

and, moreover, that vector satisfies .

Proof.

The next lemma provides a basis for a discretization argument which we will apply in the proof of the theorem.

Lemma 3.5.

There is a universal constant with the following property. Let . Then there is a set of vectors in satisfying all of the following:

-

•

All vectors in have non-negative components taking values in ;

-

•

The Euclidean norm of every vector in is in the interval ;

-

•

For every unit vector there is a vector such that , ;

-

•

The size of is at most .

Proof.

Define as the collection of all vectors in with non-negative components taking values in and with the Euclidean norm in the interval . Observe that for every unit vector , by defining coordinate-wise as

we get a vector with Euclidean norm in the interval , i.e a vector from . Thus, constructed this way satisfies the first three properties listed above. It remains to verify the upper bound on .

To estimate the size of we apply the standard volumetric argument. Observe that can be bounded from above by the number of integer lattice points in the rescaled Euclidean ball of radius . That, in turn, is bounded above by the maximal number of non-intersecting parallel translates of the unit cube which can be placed inside the ball . Comparison of the Lebesgue volumes of and confirms that the latter is of order , completing the proof. ∎

3.2 Proof of Theorem 3.1

First, suppose that . Observe that in this case . Fix a small constant . Define , so that by the assumptions of the theorem, for every constant and all large enough , the cost vectors are –incompressible. Hence, applying Proposition 2.5, we get for all large enough and every ,

implying

We infer that, by considering , the optimal objective value of the LP satisfies

with probability , and the statement of the theorem follows.

In view of the above, to complete the proof it is sufficient to verify the statement under the assumption . In what follows, we assume that for some number independent of , and is a small constant.

We shall construct a “good” event of high probability, condition on a realization of the matrix from that event, and then follow the iterative scheme outlined at the beginning of the section to construct a feasible solution. Set

and define an integer as

Definition of a “good” event. The event to be conditioned on is constructed as an intersection of multiple events. We start by defining

| At most components of the vector are greater than , | |||

where is a sufficiently large universal constant whose value can be extracted from the argument below. Observe that, by our definition of and by our assumption that is small, for all large enough ,

whence for every , in view of the definition of ,

| (13) |

Define , and observe that, by the assumptions of the theorem, for every constant and all large enough , the cost vectors are –incompressible. Hence, we can apply Proposition 2.5 to get for all large enough ,

In particular, in view of (13), the probability that for more than indices , is bounded above by

On the other hand, for every , by Proposition 2.3 and by the union bound over –subsets of , the probability that the sum of squares of largest components of is greater than , is bounded above by

where is a universal constant. Taking to be a sufficiently large constant multiple of and combining the above estimates, we obtain that the event has probability .

Fix for a moment any subset of size at most and at least . Further, denote by the non-random discrete subset of vectors in with the properties listed in Lemma 3.5. Denote by the projection onto the orthogonal complement of the cost vector . For every , define

| There is a unique vector in the linear span of , , | |||

| such that , ; moreover, that vector satisfies: | |||

| (a) ; | |||

| (b) number of indices with is at most ; | |||

where is a sufficiently large constant depending only on . We claim that, assuming is sufficiently large, the event has probability close to one. Indeed, since the collections of random vectors and are independent, we have

| There is a unique | |||

where the infimum is taken over all non-random vectors satisfying . Using that for every and applying Corollary 3.4 to the first probability on the right-hand side, we get for all large enough

Further, applying Corollary 3.2 to the second probability, we obtain that the event has probability at least

whence the intersection of events taken over the collection of all subsets of of size at least and at most , has probability .

Define the “good” event

so that . Our goal is to show that, conditioned on any realization of from , the optimal objective value of the LP is at least . From now on, we assume that the matrix is non-random and satisfies the conditions from the definition of . For reader’s convenience, we outline an algorithm for constructing a feasible solution certifying the aforementioned lower bound on :

Having outlined the algorithm, we proceed with a formal verification of its correctness.

Definition of . Let be the –subset of corresponding to largest components of the vector (we resolve ties arbitrarily). In view of our conditioning on , for every we have Denote by the restriction of the vector to , and let be a vector which majorizes coordinate-wise. Note that in view of the definition of , the Euclidean norm of is of order . Further, since we conditoned on , we find a unique vector in the linear combination of , (and, in particular, orthogonal to ) such that

satisfying the conditions (a), (b), (c) from the definition of . Define

so that , . Observe that with such a definition of , the sum satisfies

| (14) |

whereas

Applying the definition of the event and the bound , we get that the vector satisfies

| The number of indices with is at most ; | ||

where depends only on . We will simplify the conditions on . First, observe that in view of the definition of and since , we can assume that . Further, we can estimate from above by . Thus, the vector satisfies

| The number of indices with is at most ; | |||

| (15) |

Definition of The vectors are constructed via an inductive process. Let

We define numbers recursively by the formula

With large, we then have

Further, assuming that for some the vector has been defined, we let be a –subset of corresponding to largest components of (with ties resolved arbitrarily).

Let , and assume that a vector has been constructed that satisfies

| The number of indices with is at most ; | ||

(observe that satisfies the above assumptions, in view of (15), which provides a basis of induction). We denote by the restriction of the vector to (note that has the Euclidean norm at most by the induction hypothesis), and let be a vector which majorizes coordinate-wise. Similarly to the above, we let be the unique vector in the linear span of , , such that

and satisfying the conditions (a), (b), (c) from the definition of , and define

| (16) |

so that

| (17) |

By the definition of , the vector satisfies

for some constant . In is not difficult to check that, with our definition of and the assumption and as long as is large, the quantity is (much) less than ; further, is dominated by . Thus, satisfies

| The number of indices with is at most ; | (18) | ||

| (19) |

completing the induction step.

Next, we gather the properties of the constructed sets and vectors that will be useful to us. Observe that, in view of (17) and the condition that majorizes coordinate-wise (see also (14)), we have

| (20) |

(implying that constraints violated by are repaired by ) and, as a weaker property that follows directly from (16),

| (21) |

Further, since by the construction for every , the number of indices with is at most (see (18)), we infer that

Finally, the condition (19) for reads

so that, in particular,

| (22) |

Restoring feasibility. The above process produced vectors . Define the sum

By the construction, every , , lies in the orthogonal complement of , and hence

To complete the proof that , it remains to verify that is a feasible solution to the linear program. For any index , let

-

•

be the Boolean indicator of the expression “”;

-

•

for each , let be the indicator of “”;

-

•

set .

Note that, in view of the definition of the sets , for every we have only if . Indeed, the condition implies that , so that (21) yields .

From now on, we fix . The set can be partitioned into consecutive subsets in such a way that

-

•

The size of each set is either or ;

-

•

For each singleton , ;

-

•

For each subset of size two, and .

We have

Fix for a moment any and consider the corresponding sum . First, assume that is a singleton; . By our construction of the partition, we have .

-

•

If then

-

•

If then

- •

Next, assume that the size of is two; . Since in this case , we have and, by (20),

Combining the two possible cases and summing over , we get

and the proof is finished.

3.3 Applications of Theorem 3.1

As a simple sufficient condition on the cost vectors which implies the assumptions in Theorem 3.1, we consider a bound on the –norms which, in particular, implies the lower bound in the main Theorem 1.2:

Corollary 3.6 (Lower bound on under sup-norm delocalization of the cost vectors).

Let satisfy , and let matrices be as in Theorem 3.1. Consider a sequence of non-random cost vectors satisfying . Then for any constant and all sufficiently large ,

implying that almost surely.

Proof.

Fix any constant , and let be any subset of of size at most . In view of the assumptions on , we have

Since the choice of the subsets was arbitrary, the last relation implies that the vector is –incompressible for all large . It remains to apply Theorem 3.1. ∎

The next corollary constitutes the lower bound in Corollary 1.4:

Corollary 3.7 (The mean width: a sharp lower bound).

Let and be as in Theorem 3.1, and assume additionally that . Then the spherical mean width of the polyhedron satisfies

Proof.

In this proof, we assume that for each , is a uniform random unit vector in , and that , , are mutually independent and independent from . Recall that the mean width of the polyhedron is defined as

where denotes the expectation taken with respect to . It will be most convenient for us to prove the statement by contradiction. Namely, assume that there is a small positive number such that

Denote by the –field generated by the random matrices . Observe that the event

is –measurable. Condition for a moment on any realization of the polyhedra , , from , and let be an increasing sequence of integers such that for every . The condition implies

and hence

where is the conditional probability given the realization of , , from . By the Borel–Cantelli lemma, the last assertion yields

Removing the conditioning on , we arrive at the estimate

| (23) |

In the second part of the proof, we will show that the assertion (23) leads to contradiction. Fix for a moment any . We claim that is –incompressible for every large enough with probability . Indeed, the standard concentration inequality on the sphere (see, in particular, [50, Chapter 5]) implies that for every choice of a non-random –subset ,

for some universal constants . Taking the union bound, we then get

Our assumption implies that

For all such , the last estimate with yields

| (24) |

It remains to observe that as long as , we have

to that the expression on the right hand side of (24) is bounded above by . This verifies the claim.

4 The upper bound on in subgaussian setting

The goal of this section is to prove the following result:

Theorem 4.1 (Upper bound on ).

Fix any . Let , . For each let be a non-random unit vector in , and assume that . For each , let be an matrix with mutually independent centered –subgaussian entries of unit variances. Then for every and all large we have

In particular, almost surely.

Observe that the statement of the theorem is equivalent to the assertion that the intersection of the feasible polyhedron with the affine hyperplane

is empty with probability . To prove the result, we will combine the moderate deviations estimate from Proposition 2.6 with a covering argument.

4.1 Auxiliary results

Proposition 2.6 cannot be directly applied in our setting since the vectors in generally do not satisfy (even if normalized) the required –norm bound. To overcome this issue, we generalize the deviation bound to sums of two orthogonal vectors where one of the vectors satisfies a strong –norm estimate:

Proposition 4.2.

Fix any . For each let be a non-random unit vector in , be any fixed vector in , and let be a sequence of numbers such that converges to infinity. Assume that . For each , let be mutually independent centered –subgaussian variables of unit variances. Then for every and all large we have

Proof.

Fix a small . In view of the assumptions on , there is a sequence of positive numbers converging to zero such that for all . We shall consider two scenarios:

-

•

. Observe that , whereas the variable is centered and –subgaussian, for some depending only on . Lemma 2.4 then implies that, assuming is sufficiently large,

for some depending only on .

-

•

. Let be a –subset of corresponding to largest (by the absolute value) components of , with ties resolved arbitrarily. Further, let be the restriction of to . In view of the condition , we have

Further, in view of orthogonality of and ,

whereas,

We infer that . Thus, setting , we obtain a unit vector with . Applying Proposition 2.6 with in place of and in place of , we get

assuming is sufficiently large. On the other hand, again applying Lemma 2.4,

for some depending only on . Combining the last two relations, we get the desired estimate.

∎

To apply the last proposition to our setting of interest, we shall bound the number of constraints violated by a test vector:

Corollary 4.3.

Let , , , and be as in Theorem 4.1, and let be any sequence of vectors orthogonal to . Then for every small constant and all large we have

with probability at least .

Proof.

In view of Proposition 4.2, applied with , for all large and every we have

Hence, the probability that the last condition holds for less than indices , is bounded above by

for all sufficiently large . ∎

Recall that the outer radius of a polyhedron is defined as .

Proposition 4.4 (An upper bound on the outer radius).

Let be as in Theorem 4.1. Then with probability , the polyhedron has the outer radius bounded above by a function of .

Proof.

Let be a small parameter to be defined later, and let be a Euclidean –net on of size at most [50, Chapter 4]. Lemma 2.4 implies that for some depending only on and for every and ,

Define as the largest number satisfying

Then, by the above, for every ,

Setting and using the above bound on the size of , we obtain that the event

has probability (recall that the with probability ; see [50, Chapter 4]). Condition on any realization of from the above event. Assume that there exists . Let be a vector satisfying . In view of the conditioning, there are at least indices such that . Consequently,

Since , we get

contradicting our choice of . The contradiction shows that the outer radius of is at most , and the claim is verified. ∎

4.2 Proof of Theorem 4.1, and an upper bound on

Proof of Theorem 4.1.

In view of Proposition 4.4, with probability the outer radius of is bounded above by , for some depending only on .

Fix any small . By the above, to complete the proof of the theorem it is sufficient to show that with probability , every vector orthogonal to and having the Euclidean norm at most , satisfies

Let be the largest integer bounded above by

Define , where is a sufficiently small constant depending only on and (the value of can be extracted from the argument below). Let be a Euclidean –net in . It is known that can be chosen to have cardinality at most (see [50, Chapter 4]).

Fix for a moment any , and observe that, in view of Corollary 4.3 and the definition of , we have

| (25) |

with probability at least

Therefore, assuming that is sufficiently small and taking the union bound over all elements of , we obtain that with probability , (25) holds simultaneously for all .

Condition on any realization of such that the last event holds and, moreover, such that . Assume for a moment that there is such that

In view of the above, it implies that there is a vector at distance at most from such that

for at least indices . Hence, the spectral norm of can be estimated as

contradicting the bound . The contradiction implies the result. ∎

The next corollary constitutes an upper bound in Corollary 1.4. Since its proof is very similar to that of Corollary 3.7, we only sketch the argument.

Corollary 4.5.

Let be as in Theorem 4.1, and assume additionally that . Then, almost surely.

Proof.

In view of Proposition 4.4, there is depending only on such that the event

has probability one, where, as before, denotes the outer radius of the polyhedron . Set

We will prove the corollary by contradiction. Assume that the assertion of the corollary does not hold. Then, in view of the above definitions, there is such that

Condition for a moment on any realization of the polyhedra , , from , and let be an increasing sequence of integers such that and for every . Assume that , , are mutually independent uniform random unit vectors which are also independent from the matrices . The conditions

imply that for some depending only on and ,

where is the conditional probability given the realization of , , from . By the Borel–Cantelli lemma, the last assertion yields

Removing the conditioning on , we arrive at the estimate

| (26) |

The standard concentration inequality on the sphere [50, Chapter 5] and the conditions on imply that with probability , and therefore, by Theorem 4.1,

The latter contradicts (26), and the result follows. ∎

5 The Gaussian setting

In this section, we prove Theorem 1.3 and Corollary 1.5. Note that in view of rotational invariance of the Gaussian distribution, we can assume without loss of generality that the cost vectors in Theorem 1.3 are of the form . Thus, in the regime , the statement is already covered by the more general results of Sections 3 and 4.

5.1 The outer radius of random Gaussian polytopes

In this subsection, we consider the bound on the outer radius of random Gaussian polytopes. The next result immediately implies upper bounds on and in Theorem 1.3 and Corollary 1.5 in the entire range . We anticipate that the statement is known although we are not aware of a reference, and for that reason provide a proof.

Proposition 5.1 (Outer radius of the feasible region in the Gaussian setting).

Let satisfy , and for every let be an random matrix with i.i.d standard Gaussian entries. Then, denoting by the outer radius of the feasible region, for any constant we have

In particular, almost surely.

The following approximation of the standard Gaussian distribution is well known (see, for example, [19, Volume I, Chapter VII, Lemma 2]):

Lemma 5.2.

Let be a standard Gaussian variable. Then for every ,

Let be a standard Gaussian random vector in , and be the non-decreasing rearrangement of its components. Let . Then, from the above lemma, for every we have

| (27) |

As a corollary, we obtain the following deviation estimate:

Corollary 5.3.

Fix any . Let sequences of positive integers , , and , , satisfy , , and . Further, for each , let be a standard Gaussian vector in . Then

Proof.

Proof of Proposition 5.1.

Fix any . Observe that the statement is equivalent to showing that with probability the matrix has the property that for every there is with .

The argument below is similar to the proof of Proposition 4.4. Let be the largest integer bounded above by

Define , where is a sufficiently small constant depending only on . Let be a Euclidean –net in of cardinality at most (see [50, Chapter 4]).

Fix for a moment any , and observe that, in view of Corollary 5.3 and the definition of , we have

| (28) |

with probability at least . Therefore, assuming that is sufficiently small and taking the union bound over all elements of , we obtain that with probability , (28) holds simultaneously for all .

Condition on any realization of such that the last event holds and, moreover, such that (recall that the latter occurs with probability ; see [50, Chapter 4]). Assume for a moment that there is such that for all . In view of the above, it implies that there is a vector at distance at most from such that

for at least indices . Hence, the spectral norm of can be estimated as

contradicting the bound . The contradiction shows that for every there is such that . The result follows. ∎

5.2 Proof of Theorem 1.3 and Corollary 1.5

As we have noted, the upper bounds in Theorem 1.3 and Corollary 1.5 follow readily from Proposition 5.1, and so we only need to verify the lower bounds. In view of results of Section 3 which also apply in the Gaussian setting, we may assume that satisfies .

Regarding the proof of Theorem 1.3, since is a standard Gaussian vector, it follows from the formula for the Gaussian density that

whereas, by the assumption , we have . This implies the result.

6 Numerical experiments

Our results described in the previous sections naturally give rise to the questions: (a) How close to each other are the asymptotic estimates of the optimal objective value and empirical observations?, (b) What is the asymptotic distribution and standard deviation of ?, and (c) How does the algorithm in the proof of Theorem 3.1 perform in practice? We discuss these questions in the following subsections, and make conjectures while providing numerical evidence. We use Gurobi 10.0.1 for solving instances of the LP (1), and set all Gurobi parameters to default.

6.1 Magnitude of the optimal objective value

Below, we investigate the quality of approximation of the optimal objective value by the asymptotic bound given in Theorems 1.2 and 1.3. The empirical outcomes are obtained through multiple runs of the LP (1) under various choices of parameters. We consider two distributions of the entries of : either is standard Gaussian or its entries are i.i.d Rademacher () random variables. In either case and for different choices of , we sample the random LP (1) taking the sample size and letting be the vector of i.i.d Rademacher variables rescaled to have unit Euclidean norm. The cost vector is generated once and remains the same for each of the instances of the LP within a sample.

| relative gap() | ||||

|---|---|---|---|---|

| 1000 | 50 | 0.40853 | 0.50626 | 23.92 |

| 2000 | 50 | 0.36816 | 0.44119 | 19.83 |

| 6000 | 50 | 0.32317 | 0.37256 | 15.28 |

| 10000 | 50 | 0.30719 | 0.35176 | 14.50 |

| 20000 | 50 | 0.28888 | 0.32473 | 12.41 |

As is shown in Tables 1 and 2, for a fixed value of , as the number of constraints progressively increases in magnitude, the relative gap between and the sample mean of the optimal objective values, defined as

decreases.

| relative gap() | ||||

|---|---|---|---|---|

| 1000 | 50 | 0.40853 | 0.50369 | 23.29 |

| 2000 | 50 | 0.36816 | 0.43801 | 18.97 |

| 6000 | 50 | 0.32317 | 0.37200 | 15.11 |

| 10000 | 50 | 0.30719 | 0.35220 | 14.65 |

| 20000 | 50 | 0.28888 | 0.32856 | 13.73 |

6.2 Structural assumptions on the cost vector

In this subsection, we carry out a numerical study of the technical conditions on the cost vectors from Theorem 1.2. Roughly speaking, those conditions stipulate that the cost vector has significantly more than “essentially non-zero” components. Since Theorem 1.2 is an asymptotic result, it is not at all clear what practical assumptions on the cost vectors should be imposed to guarantee that the resulting optimal objective value is close to the asymptotic bound.

| relative gap () | ||

|---|---|---|

| 1 | 0.429907 | 15.08 |

| 2 | 0.454357 | 10.25 |

| 3 | 0.459387 | 9.25 |

| 4 | 0.479007 | 5.38 |

| 5 | 0.481839 | 4.82 |

| 6 | 0.486141 | 3.97 |

| 7 | 0.479635 | 5.25 |

| 8 | 0.493168 | 2.58 |

| 9 | 0.490829 | 3.04 |

| 10 | 0.498035 | 1.62 |

In the following experiment, we consider a random coefficient matrix with i.i.d subgaussian components equidistributed with the product of Bernoulli() and N(,) random variables. Note that with this definition the entries have zero mean and unit variance. Further, we consider a family of cost vectors parametrized by an integer , so that the vector has non zero components equal to each, and the rest of the components are zeros. For a given choice of , we sample the LP (1) with the above distribution of the entries and the cost vector . Our goal is to compare the resulting sample mean of the optimal objective value to the sample mean obtained in the previous subsection for the same matrix dimensions and for the strongly incompressible cost vector. We fix and , and let to be the sample mean of optimal objective value of LP(1) with the cost vector . We denote the sample mean of objective value with the strongly incompressible cost vector by . Our empirical results show that, as long as is small (so that is very sparse), the value of the sample mean differs significantly from the one in Table 1. On the other hand, for sufficiently large the relative gap between the sample means defined by

becomes negligible. The results are presented in Table 3.

6.3 Limiting distribution of the optimal objective value

Recall that, given mutually independent standard Gaussian variables, their maximum converges (up to appropriate rescaling and translation) to the Gumbel distribution as the number of variables tends to infinity. If the vertices of the random polyhedron were behaving like independent Gaussian vectors (with a proper rescaling) then the limiting distribution of for any given fixed cost vector would be asymptotically Gumbel. Our computations suggest that in fact the limiting distribution is Gaussian.

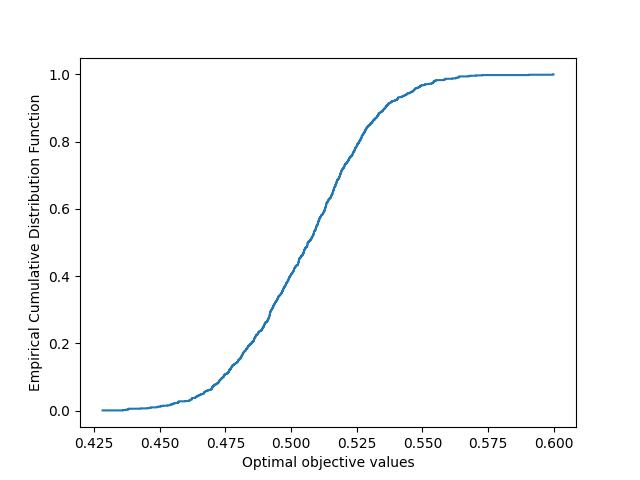

In our numerical experiments, we consider Gaussian and Rademacher random coefficient matrices of dimensions and . The sample size in either case is taken to be . As in the previous experiment, we take to be a random vector with i.i.d Rademacher components rescaled to have the Euclidean norm one. We generate the cost vector once so that it is the same for every LP from a sample. We employ the Kolmogorov–Smirnov (KS) test to compare the sample distribution of to Gaussian of a same mean and variance. In either case, the obtained p-value exceeds the conventional significance level of 0.05, indicating lack of substantial evidence to refute the null hypothesis that the data is normally distributed. Further, visual representation of the frequency histogram and the empirical cumulative distribution function of the optimal values shown in Figures 3 and 4 validate this conjecture.

The next conjecture summarizes the experimental findings:

Conjecture 6.1 (Limiting distribution of ).

Let , , be as in Theorem 1.2, and for each let be uniform random unit cost vector independent from . Then the sequence of normalized random variables

converges in distribution to the standard Gaussian.

6.4 Standard deviation of the optimal objective value

As in the previous two numerical experiments, in this one we consider two types of the entries distributions: Gaussian and Rademacher. The cost vector is generated according to the same procedure as above. We sample the LP (1) taking the sample size to be , and compute the sample standard deviation (the square root of the sample variance) of the optimal objective value. Based on our numerical studies we speculate that standard deviation of is roughly of the order , at least in the setting where is very large compared to . Indeed, upon examination of the last column in Tables 4 and 5, we observe a consistent phenomenon: the quantities are of order for various choices of and .

| 1000 | 50 | 0.408539 | 0.02420 | 0.765 |

|---|---|---|---|---|

| 2000 | 50 | 0.368161 | 0.01728 | 0.773 |

| 4000 | 50 | 0.337791 | 0.01333 | 0.843 |

| 6000 | 50 | 0.323170 | 0.01142 | 0.885 |

| 8000 | 50 | 0.313877 | 0.01059 | 0.947 |

| 10000 | 50 | 0.307196 | 0.01027 | 1.027 |

| 1000 | 100 | 0.465991 | 0.03014 | 0.953 |

| 2000 | 100 | 0.408539 | 0.01592 | 0.712 |

| 4000 | 100 | 0.368161 | 0.01172 | 0.742 |

| 6000 | 100 | 0.349456 | 0.00990 | 0.767 |

| 1000 | 150 | 0.528257 | 0.03192 | 1.010 |

| 2000 | 150 | 0.441515 | 0.015066 | 0.674 |

| 4000 | 150 | 0.391745 | 0.01155 | 0.731 |

| 6000 | 150 | 0.368161 | 0.011850 | 0.918 |

| 1000 | 50 | 0.408539 | 0.020420 | 0.645 |

|---|---|---|---|---|

| 2000 | 50 | 0.368161 | 0.017393 | 0.777 |

| 4000 | 50 | 0.337791 | 0.011962 | 0.756 |

| 6000 | 50 | 0.323170 | 0.010207 | 0.790 |

| 8000 | 50 | 0.313877 | 0.010333 | 0.924 |

| 10000 | 50 | 0.307196 | 0.008997 | 0.899 |

| 1000 | 100 | 0.465991 | 0.023097 | 0.730 |

| 2000 | 100 | 0.408539 | 0.014648 | 0.655 |

| 4000 | 100 | 0.368161 | 0.010436 | 0.660 |

| 6000 | 100 | 0.349456 | 0.011791 | 0.913 |

| 1000 | 150 | 0.528257 | 0.032600 | 1.030 |

| 2000 | 150 | 0.441515 | 0.015466 | 0.691 |

| 4000 | 150 | 0.391745 | 0.011030 | 0.697 |

| 6000 | 150 | 0.368161 | 0.009153 | 0.708 |

6.5 An algorithm for finding a near-optimal feasible solution

As previously discussed, the proof of Theorem 3.1 involves an iterative projection process to restore feasibility from an initial point. In the process, we discretize the continuous space spanned by violated constraints at each iteration (i.e use a covering argument) as a means to apply probabilistic union bound. Recall that the goal of Algorithm 1 described in the proof of Theorem 3.1 is to provide theoretical guarantees for . An exact software implementation of that algorithm is heavy in terms of both the amount of code and computations. On the other hand, it is of considerable interest to measure performance of block-iterative projection methods in the context of finding near optimal solution to instances of the random LP (1). To approach this task, we consider a “light” version of the algorithm from the proof of Theorem 3.1, which does not involve any discretizations (see Algorithm 2 below). The algorithm is a version of the classical Kaczmarz block-iterative projection method as presented in [18] and its randomized counterparts in [38] and [53]. In our context, the blocks correspond to the rows of the matrix that are violated by the initial point and its updates at each iteration. Table 6 shows the results of running the algorithm for various parameters and . For each instance of the LP, is the the number of iterations required to restore feasibility, is the initial point and is the output of the Algorithm 2. Note that the obtained perturbations to are in the orthogonal complement of the cost vector and as a result . The numbers and are the number of violated constraints by at iteration 1 and at iteration 2, respectively. Note that these numbers are rather small compared to the size of the LP instance. We note that in our experiment, the algorithm did not converge for the instance of the LP, which we attribute to the random nature of the problem. At the same time, the Algorithm converged fast due to small number of constraint violations for all other given instances.

| 1000 | 50 | 2 | 0.408539 | 11 | 1 |

| 1000 | 100 | 2 | 0.465991 | 28 | 4 |

| 2000 | 50 | 2 | 0.368161 | 6 | 1 |

| 2000 | 100 | 2 | 0.408539 | 23 | 1 |

| 4000 | 50 | 2 | 0.337791 | 13 | 2 |

| 4000 | 100 | 2 | 0.368161 | 30 | 1 |

| 6000 | 50 | 2 | 0.323170 | 22 | 21 |

| 6000 | 100 | 2 | 0.349456 | 31 | 8 |

| 8000 | 50 | 2 | 0.313877 | 22 | 6 |

| 8000 | 100 | 2 | 0.337791 | 21 | 5 |

| 10000 | 50 | 2 | 0.307196 | 19 | 1 |

| 10000 | 100 | 1 | 0.329505 | 34 | 0 |

| 20000 | 100 | 1 | 0.307196 | 29 | 0 |

| 40000 | 50 | 1 | 0.273493 | 12 | 0 |

| 40000 | 100 | 2 | 0.288881 | 34 | 3 |

| 60000 | 50 | 2 | 0.265558 | 16 | 2 |

| 60000 | 100 | 1 | 0.279576 | 36 | 0 |

| 80000 | 50 | 1 | 0.260329 | 21 | 0 |

| 80000 | 100 | 2 | 0.273493 | 36 | 1 |

| 100000 | 50 | 2 | 0.256479 | 28 | 5 |

| 100000 | 100 | 2 | 0.269040 | 35 | 1 |

7 Conclusion

In this paper, we study the optimal objective value of a random linear program where the entries of the coefficient matrix have subgaussian distributions, the variables are free and the right hand side of each constraint is . We establish sharp asymptotics in the regime , and some additional assumptions on the cost vectors. This asymptotic provides quantitative information about the geometry of the random polyhedron defined by the feasible region of the random LP (1), specifically about its spherical mean width. The computational experiments support our theoretical guarantees and give insights into several open questions regarding the asymptotic behaviour of the random LP. The connection between the proof of the main result and convex feasibility problems allows us to provide a fast algorithm for obtaining a near optimal solution in our randomized setting. The random LP (1) is a step towards studying models with inhomogeneous coefficient matrices and establishing stronger connections to practical applications.

Acknowledgements

We are grateful to Dylan Altschuler for bringing our attention to [15, Section 3.7].

Declarations

Funding. Konstantin Tikhomirov is partially supported by the NSF grant DMS-2331037.

Conflict of interest/Competing interests. The authors declare no conflict of interest in regard to this publication.

Code availability. The code for the numerical experiments is available on https://github.com/marzb93/RandomLinearProgram

References

- [1] (1954) The relaxation method for linear inequalities. Canad. J. Math. 6, pp. 382–392. External Links: ISSN 0008-414X, Document, Link, MathReview (L. M. Blumenthal) Cited by: §1.4.1.

- [2] (1989) Block-iterative projection methods for parallel computation of solutions to convex feasibility problems. Linear Algebra and Its Applications 120, pp. 165–175. Cited by: §1.4.1.

- [3] (2015) On the Gaussian behavior of marginals and the mean width of random polytopes. Proc. Amer. Math. Soc. 143 (2), pp. 821–832. External Links: ISSN 0002-9939, Document, Link, MathReview (Gergely Ambrus) Cited by: §1.4.3.

- [4] (1955) Distributions of solutions of a set of linear equations (with an application to linear programming). Journal of the American Statistical Association 50 (271), pp. 854–869. Cited by: 3rd item.

- [5] (2018) On greedy randomized Kaczmarz method for solving large sparse linear systems. SIAM J. Sci. Comput. 40 (1), pp. A592–A606. External Links: ISSN 1064-8275, Document, Link, MathReview (Stefan A. Funken) Cited by: §1.4.1.

- [6] (1986) Random linear programs with many variables and few constraints. Math. Programming 34 (1), pp. 62–71. External Links: ISSN 0025-5610, Document, Link, MathReview (H. L. Bhatia) Cited by: 1st item.

- [7] (1982) The average number of pivot steps required by the simplex-method is polynomial. Z. Oper. Res. Ser. A-B 26 (5), pp. A157–A177. External Links: ISSN 0340-9422, Document, Link, MathReview (C. A. Botsaris) Cited by: item (i), 1st item.

- [8] (1999) A sharp upper bound for the expected number of shadow vertices in LP-polyhedra under orthogonal projection on two-dimensional planes. Math. Oper. Res. 24 (3), pp. 544–603. External Links: ISSN 0364-765X, Document, Link, MathReview (K. G. Murty) Cited by: item (i), 1st item.

- [9] (1987) The simplex method. Algorithms and Combinatorics: Study and Research Texts, Vol. 1, Springer-Verlag, Berlin. Note: A probabilistic analysis External Links: ISBN 3-540-17096-0, Document, Link, MathReview (Jürgen Köhler) Cited by: item (i), 1st item.

- [10] (2014) Integer feasibility of random polytopes: random integer programs. In Proceedings of the 5th conference on Innovations in theoretical computer science, pp. 449–458. Cited by: 4th item.

- [11] (2015) A polynomial projection algorithm for linear feasibility problems. Math. Program. 153 (2, Ser. A), pp. 687–713. External Links: ISSN 0025-5610, Document, Link, MathReview (Wei Hong Yang) Cited by: §1.4.1.

- [12] (2018) A friendly smoothed analysis of the simplex method. In STOC’18—Proceedings of the 50th Annual ACM SIGACT Symposium on Theory of Computing, pp. 390–403. External Links: Document, Link, MathReview Entry Cited by: 2nd item.

- [13] (2009) Asymptotic shape of a random polytope in a convex body. J. Funct. Anal. 257 (9), pp. 2820–2839. External Links: ISSN 0022-1236, Document, Link, MathReview (J. Hüsler) Cited by: §1.4.3.

- [14] (2017) A sampling Kaczmarz-Motzkin algorithm for linear feasibility. SIAM J. Sci. Comput. 39 (5), pp. S66–S87. External Links: ISSN 1064-8275, Document, Link, MathReview (Emanuele Galligani) Cited by: §1.4.1.

- [15] (1998) Large deviations techniques and applications. Second edition, Applications of Mathematics (New York), Vol. 38, Springer-Verlag, New York. External Links: ISBN 0-387-98406-2, Document, Link, MathReview Entry Cited by: §2.3, Acknowledgements.

- [16] (1986) On linear programs with random costs. Mathematical Programming 35, pp. 3–16. Cited by: 5th item.

- [17] (2011) Acceleration of randomized Kaczmarz method via the Johnson-Lindenstrauss lemma. Numer. Algorithms 58 (2), pp. 163–177. External Links: ISSN 1017-1398, Document, Link, MathReview (Alexander N. Malyshev) Cited by: §1.4.1.

- [18] (1980) Block-iterative methods for consistent and inconsistent linear equations. Numerische Mathematik 35, pp. 1–12. Cited by: §6.5.

- [19] (1991) An introduction to probability theory and its applications, volume 2. Vol. 81, John Wiley & Sons. Cited by: §5.1.

- [20] (2002) Random spaces generated by vertices of the cube. Discrete Comput. Geom. 28 (2), pp. 255–273. External Links: ISSN 0179-5376, Document, Link, MathReview (Z. Nádeník) Cited by: §1.4.3.

- [21] (2016) Asymptotic shape of the convex hull of isotropic log-concave random vectors. Adv. in Appl. Math. 75, pp. 116–143. External Links: ISSN 0196-8858, Document, Link, MathReview (Julio Bernués) Cited by: §1.4.3.

- [22] (1986) An octahedron is poorly approximated by random subspaces. Funktsional. Anal. i Prilozhen. 20 (1), pp. 14–20, 96. External Links: ISSN 0374-1990, MathReview (M. I. Kadets) Cited by: §1.4.3.

- [23] (1988) Extremal properties of orthogonal parallelepipeds and their applications to the geometry of Banach spaces. Mat. Sb. (N.S.) 136(178) (1), pp. 85–96. External Links: ISSN 0368-8666, Document, Link, MathReview (G. M. Ustinov) Cited by: §1.4.3.

- [24] (2021) On adaptive sketch-and-project for solving linear systems. SIAM J. Matrix Anal. Appl. 42 (2), pp. 954–989. External Links: ISSN 0895-4798, Document, Link, MathReview Entry Cited by: §1.4.1.

- [25] (2015) Randomized iterative methods for linear systems. SIAM J. Matrix Anal. Appl. 36 (4), pp. 1660–1690. External Links: ISSN 0895-4798, Document, Link, MathReview (Ninoslav Truhar) Cited by: §1.4.1.

- [26] ([2023] ©2023) Upper and lower bounds on the smoothed complexity of the simplex method. In STOC’23—Proceedings of the 55th Annual ACM Symposium on Theory of Computing, pp. 1904–1917. External Links: Document, Link, MathReview Entry Cited by: 2nd item.

- [27] (2017) Preasymptotic convergence of randomized Kaczmarz method. Inverse Problems 33 (12), pp. 125012, 21. External Links: ISSN 0266-5611, Document, Link, MathReview (Barbara Zubik-Kowal) Cited by: §1.4.1.

- [28] (1937) Angenäherte auflösung von systemen linearer gleichungen (english translation by jason stockmann): bulletin international de l’académie polonaise des sciences et des lettres. Cited by: §1.4.1.

- [29] (2022) Limit laws for empirical optimal solutions in random linear programs. Annals of Operations Research 315 (1), pp. 251–278. Cited by: 3rd item.

- [30] (2005) Smallest singular value of random matrices and geometry of random polytopes. Adv. Math. 195 (2), pp. 491–523. External Links: ISSN 0001-8708, Document, Link, MathReview (Béla Uhrin) Cited by: §1.4.3, §1.4.3.

- [31] (2016) An accelerated randomized Kaczmarz algorithm. Math. Comp. 85 (297), pp. 153–178. External Links: ISSN 0025-5718, Document, Link, MathReview (Judith M. Ford) Cited by: §1.4.1.

- [32] (2023) Asymptotic confidence sets for random linear programs. arXiv preprint arXiv:2302.12364. Cited by: 3rd item.

- [33] (2021) On greedy randomized block Kaczmarz method for consistent linear systems. Linear Algebra Appl. 616, pp. 178–200. External Links: ISSN 0024-3795, Document, Link, MathReview (Bruno Carpentieri) Cited by: §1.4.1.

- [34] (2015) Convergence properties of the randomized extended Gauss-Seidel and Kaczmarz methods. SIAM J. Matrix Anal. Appl. 36 (4), pp. 1590–1604. External Links: ISSN 0895-4798, Document, Link, MathReview (Marco Donatelli) Cited by: §1.4.1.

- [35] (2020) Accelerated sampling Kaczmarz Motzkin algorithm for the linear feasibility problem. J. Global Optim. 77 (2), pp. 361–382. External Links: ISSN 0925-5001, Document, Link, MathReview (S. A. Edalatpanah) Cited by: §1.4.1.

- [36] (2022) Sampling kaczmarz-motzkin method for linear feasibility problems: generalization and acceleration. Mathematical Programming 194 (1-2), pp. 719–779. Cited by: §1.4.1.

- [37] (1954) The relaxation method for linear inequalities. Canadian Journal of Mathematics 6, pp. 393–404. Cited by: §1.4.1.

- [38] (2014) Paved with good intentions: analysis of a randomized block Kaczmarz method. Linear Algebra Appl. 441, pp. 199–221. External Links: ISSN 0024-3795, Document, Link, MathReview (A. Bultheel) Cited by: §1.4.1, §6.5.

- [39] (2020) A greedy block Kaczmarz algorithm for solving large-scale linear systems. Appl. Math. Lett. 104, pp. 106294, 8. External Links: ISSN 0893-9659, Document, Link, MathReview Entry Cited by: §1.4.1.

- [40] (1989) The volume of convex bodies and Banach space geometry. Cambridge Tracts in Mathematics, Vol. 94, Cambridge University Press, Cambridge. External Links: ISBN 0-521-36465-5; 0-521-66635-X, Document, Link, MathReview (Mikhail Ostrovskii) Cited by: item (ii).

- [41] (1966) On the probability distribution of the optimum of a random linear program. SIAM Journal on Control 4 (1), pp. 211–222. Cited by: 3rd item.

- [42] (2008) The Littlewood-Offord problem and invertibility of random matrices. Adv. Math. 218 (2), pp. 600–633. External Links: ISSN 0001-8708, Document, Link, MathReview (Ben Joseph Green) Cited by: Definition 2.2.

- [43] (1983) On the average number of steps of the simplex method of linear programming. Math. Programming 27 (3), pp. 241–262. External Links: ISSN 0025-5610, Document, Link, MathReview (M. Brannigan) Cited by: 1st item.

- [44] (2004) Smoothed analysis of algorithms: why the simplex algorithm usually takes polynomial time. J. ACM 51 (3), pp. 385–463. External Links: ISSN 0004-5411, Document, Link, MathReview (Panos M. Pardalos) Cited by: item (i), 2nd item.

- [45] (2009) A randomized Kaczmarz algorithm with exponential convergence. J. Fourier Anal. Appl. 15 (2), pp. 262–278. External Links: ISSN 1069-5869, Document, Link, MathReview (Xiaoping A. Shen) Cited by: §1.4.1.

- [46] (2011) Mean field models for spin glasses. Volume I. Ergebnisse der Mathematik und ihrer Grenzgebiete. 3. Folge. A Series of Modern Surveys in Mathematics [Results in Mathematics and Related Areas. 3rd Series. A Series of Modern Surveys in Mathematics], Vol. 54, Springer-Verlag, Berlin. Note: Basic examples External Links: ISBN 978-3-642-15201-6, Document, Link, MathReview (Francis Comets) Cited by: §1.4.1.

- [47] (2011) Mean field models for spin glasses. Volume II. Ergebnisse der Mathematik und ihrer Grenzgebiete. 3. Folge. A Series of Modern Surveys in Mathematics [Results in Mathematics and Related Areas. 3rd Series. A Series of Modern Surveys in Mathematics], Vol. 55, Springer, Heidelberg. Note: Advanced replica-symmetry and low temperature External Links: ISBN 978-3-642-22252-8; 978-3-642-22253-5, MathReview (Francis Comets) Cited by: §1.4.1.

- [48] (1982) On relaxation methods for systems of linear inequalities. European J. Oper. Res. 9 (2), pp. 184–189. External Links: ISSN 0377-2217, Document, Link, MathReview Entry Cited by: §1.4.1.

- [49] (2009) Beyond Hirsch conjecture: walks on random polytopes and smoothed complexity of the simplex method. SIAM J. Comput. 39 (2), pp. 646–678. External Links: ISSN 0097-5397, Document, Link, MathReview Entry Cited by: 2nd item.

- [50] (2018) High-dimensional probability. Cambridge Series in Statistical and Probabilistic Mathematics, Vol. 47, Cambridge University Press, Cambridge. Note: An introduction with applications in data science, With a foreword by Sara van de Geer External Links: ISBN 978-1-108-41519-4, Document, Link, MathReview (Sasha Sodin) Cited by: item (ii), §1.2, §2.2, §2.3, §3.1, §3.1, §3.1, §3.1, §3.3, §4.1, §4.1, §4.2, §4.2, §5.1, §5.1.

- [51] (2021) Block sampling kaczmarz–motzkin methods for consistent linear systems. Calcolo 58 (3), pp. 39. Cited by: §1.4.1.

- [52] (2022) Greedy Motzkin-Kaczmarz methods for solving linear systems. Numer. Linear Algebra Appl. 29 (4), pp. Paper No. e2429, 24. External Links: ISSN 1070-5325, MathReview Entry Cited by: §1.4.1.

- [53] (2023) Randomized block subsampling Kaczmarz-Motzkin method. Linear Algebra Appl. 667, pp. 133–150. External Links: ISSN 0024-3795, Document, Link, MathReview Entry Cited by: §1.4.1, §6.5.