Simultaneous Inference for Time Series Functional Linear Regression

Abstract

We consider the problem of joint simultaneous confidence band (JSCB) construction for regression coefficient functions of time series scalar-on-function linear regression when the regression model is estimated by a roughness penalization approach with flexible choices of orthonormal basis functions. A simple and unified multiplier bootstrap methodology is proposed for the JSCB construction which is shown to achieve the correct coverage probability asymptotically. Furthermore, the JSCB is asymptotically robust to inconsistently estimated standard deviations of the model. The proposed methodology is applied to a time series data set of electricity demands to visually investigate and formally test the overall regression relationship, as well as perform model validation.

Abstract

Section A of this supplemental material discusses several important aspects related to the main article, including the effects of pre-smoothing, practical choices of the basis functions and extensions to regression models with functional response. Section B provides additional simulation results under various numbers of predictors and data generating mechanisms. In Section C, we establish a Gaussian approximation theory for the roughness penalization estimation method, which may be of independent interest. Examples on calculations of the physical dependence measure for a class of functional MA models and a class of functional AR(1) models are presented in Section D. Additional theoretical results, together with proofs of all main results, are provided in Section E.

Keywords: Convex Gaussian approximation; Functional time series; Joint simultaneous confidence band; Multiplier bootstrap; Roughness penalization.

1 Introduction

Modern data collection technologies routinely produce high-frequency time series with complex functional structure, where each observation consists of an entire curve recorded over a time interval. Examples arising in contemporary data science applications include electricity demand curves measured across a day, environmental monitoring data such as pollution or temperature profiles, biomedical signals, and financial intraday curves. To address the resulting statistical issues, functional (or curve) time series analysis has undergone unprecedented development over the last two decades. See [30] and [6] for excellent book-length treatments of the topic. We also refer the readers to [27], [3, 2], [46], [45] and [17], among many others, for articles that address various modelling, estimation, forecasting and inference aspects of functional time series analysis from both time and spectral domain perspectives.

The main purpose of this article is to perform simultaneous statistical inference for time series scalar-on-function linear regression. Specifically, consider the following time series functional linear model (FLM):

| (1) |

where is a -variate stationary time series of known functional predictors observed on , is a univariate stationary time series of responses, and is a centered stationary time series of regression errors satisfying for all and . Observe that and could be dependent and can be viewed as the best linear forecast of based on . Despite the rapid development of estimation and forecasting methods for functional time series, rigorous statistical inference remains largely underdeveloped, especially for FLMs like (11) involving functional predictors under temporal dependence. Therefore, we are interested in constructing asymptotically correct joint simultaneous confidence bands (JSCB) for the regression coefficients ; that is, we aim to find random functions and , , such that

for a pre-specified coverage probability . The need for JSCB arises in many situations when one wants to, for instance, rigorously investigate the overall magnitude and pattern of the regression coefficient functions, test various assumptions on the regression relationship and perform diagnostic checking and model validation of (11) without multiple hypothesis testing problems.

1.1 Main contribution

To better understand the main contributions of this paper, we start by emphasizing that there are two major challenges involved in the JSCB construction of for the time series FLM (11). First, the estimation of model (11) is related to an ill-posed inverse problem [10, Section 2.2] and estimators of are typically not tight on . As a result, it has been a difficult and open problem to investigate the large sample distributional behavior of estimators of uniformly across . Second, the rates of convergence for various estimators of are sensitive to the smoothness of and , and the penalization parameter used in the regression. Consequently, in practice it is challenging to determine convergence rates of the estimated coefficient functions and hence the appropriate normalizing constants for uniform inference of .

To address the aforementioned challenges, this article makes two principal contributions. First, we develop a uniform Gaussian approximation theory and comparison results over all Euclidean convex sets for the sum of stationary and weakly dependent time series in moderately high-dimensional settings. To the best of our knowledge, this presents a novel theoretical advancement as such results have not previously been investigated within the contexts of functional time series or functional data. Our findings extend the corresponding results established for independent or -dependent data, as explored in [5], [21], and among others. Specifically, the uniform convex Gaussian approximation theory is established for a weighted maximum deviation uniformly over all quantiles and a wide class of weight functions (c.f. Theorem 1 in the supplemental material). Additionally, we derive the explicit comparison bounds on the Kolmogorov distance between the sum of moderately high-dimensional Gaussian vectors, which plays a crucial role in validating the use of multiplier bootstrap procedures. These contributions significantly broaden the range of problems that can be rigorously addressed within functional time series analysis, and offer practical tools for addressing inferential challenges in both functional data and time series domains.

Second, we propose a simple and unified multiplier bootstrap procedure for constructing asymptotically correct JSCBs for . Leveraging the fact that the convex Gaussian approximation and Gaussian comparison results hold uniformly over all Euclidean convex sets, our approach circumvents the need to explicitly derive the limiting distribution of the corresponding maximum deviation or the convergence rates, which are often analytically intractable or extremely difficult to estimate accurately in time-dependent settings. Considering the roughness penalized estimators of for instance, we demonstrate that the multiplier bootstrap accurately approximates their weighted maximum deviations on uniformly across all quantiles and a wide class of smooth weight functions under quite general conditions in large samples (c.f. Theorem 1 in Section 5.2). Furthermore, the constructed JSCBs remain asymptotically correct even when the weight function is estimated inconsistently under some mild conditions, thereby adding an additional layer of robustness to the proposed methodology. The multiplier bootstrap procedure is easy to implement and practically useful, offering a powerful and versatile tool for empirical studies. To the best of our knowledge, this is the first work to provide JSCBs for FLM under general time series dependence, thereby filling an important gap in uncertainty quantification of functional time series analysis.

1.2 Literature review

To date, results for the time series scalar-on-function regression (11) are scarce and mainly focus on the consistency of functional principal component (FPC) based estimators [27, 26]. To our best knowledge, there is no existing literature on the asymptotically correct JSCB construction for under time series dependence. On the other hand, there is a wealth of statistics literature dealing with estimation, convergence rates, prediction, and application of FLM (11) when the data are independent and identically distributed (i.i.d.). See, for instance, [9], [16], [36], [8] and [32] for a far from exhaustive list of references. In parallel with the FPC based estimators, [64], developed a Reproducing Kernel Hilbert Space based approach for estimating the slope coefficient function in FLMs. Subsequent studies on minimax convergence rates, prediction, and statistical inference include [7], [53], [18], among others. We also refer the readers to [10], [42], [59] and [49] for excellent recent reviews of the topic and more references.

Meanwhile, the last two decades also witnessed an increase in statistics literature on the inference of FLM (11) for i.i.d. data. Since a JSCB is primarily an inferential tool, we shall review this literature in more detail. The main body of the aforementioned literature consists of results related to -type tests on whether or a fixed known function; see for instance [25], [35], [33] and [55], among others. Other contributions include confidence interval construction for the conditional mean and hypothesis testing for functional contrasts [53] and goodness of fit tests for (11) versus possibly nonlinear alternatives [29, 22, 40]. In contrast, for independent observations, there appear to be few results in the literature discussing the construction of confidence bands for . [31] proposed a simple methodology to construct a conservative confidence band for the slope function of scalar-on-function linear regression aiming at covering “most” of the points with a prespecified probability for independent data. Recently, [18] constructed an asymptotically correct simultaneous confidence band for function-on-function linear regression of independent data, and the authors also discussed the scalar-on-function case briefly. However, the implementation of the latter paper requires estimating the convergence rate of the regression, which could be a relatively difficult task in moderate samples.

On the other hand, the multiplier bootstrap technique has attracted much attention recently. Among others, [11] derived asymptotic consistency of the generalized bootstrap technique for estimating equations. [39] established the validity of the weighted bootstrap technique based on a weighted -estimation framework. Later, [54] considered a multiplier bootstrap procedure in the construction of likelihood-based confidence sets under possible model misspecification. Non-asymptotic results on the multiplier bootstrap have been used for high dimensional inference on hyper-rectangles and certain classes of simple convex sets that can be well approximated by (possibly higher dimensional) hyper-rectangles after linear transformations; see for instance [14] and [13] for independent data and [67] for functional time series.

The paper is organized as follows. In Section E.5, we propose the methodology of the JSCB construction based on a roughness penalization approach. Section 3 investigates finite sample accuracy of the bootstrap methodology for various basis functions and weighting schemes using Monte Carlo experiments. We analyze a time series dataset on electricity demand curves and daily total demand in Spain in Section 4. The theoretical result on the multiplier bootstrap for roughness penalized estimators of is discussed in Section 5. Additional discussions, simulations, examples, theoretical results and the proofs of all theoretical results are deferred to the supplemental material. Reproducible code for the implementation of the JSCB construction is available at https://github.com/YC-stats/FLM_numerical.

2 Methodology

Hereafter, for simplicity we shall assume that and are centered and hence . Let be the Hilbert space of all square integrable functions on with inner product . We also denote by the collection of functions that are -times continuously differentiable with absolutely continuous -th derivative on . The notation stands for the standard deviation of a random variable . Without further specifications, the constants are all independent of .

2.1 Roughness Penalization Estimation

In order to facilitate the formulation of roughness penalization estimation, we first introduce some notation. Throughout this paper, we assume that for is continuous on a.s. and hence admits the expansion where is a set of pre-selected orthonormal basis functions of . From Theorem 1 of [52], has the standard Karhunen-Loève type expansion,

| (2) |

where is the standard deviation of and if . Set if . Notice that captures the decay speed of as increases and the random coefficient remains at the same magnitude with variance as increases when . Similarly, one can write

The roughness penalization approach to the FLM (11) is designed to deal with a penalized least squares problem. Following the method proposed by [48], we truncate the number of coefficient functions to finite (but diverging) dimensional spans of a priori set of basis functions and involves a roughness penalty to obtain an estimator of . Specifically, define the truncated basis expansion of the coefficient function as for with the truncation number . We consider the penalty term throughout the paper and denote the total truncation number as . Furthermore, let be a -dimensional block vector where is the -th block with for , then the penalized least squares estimator becomes

where , is an block design matrix with its th row . The penalty term is a block diagonal matrix with as its diagonals, and is a matrix with its th element . We refer readers to Section D.2 of the supplemental material for further details of the roughness penalization approach. Consequently, the roughness penalized estimator is given by where is a block-sparse matrix whose -th row contains in columns to , and zeros elsewhere for .

2.2 JSCB Construction

JSCB construction of boils down to evaluating the distributional behavior of the weighted maximum deviation

where for any function and weight function . The weight function is assumed to belong to a class with

For a given , denote by the -th quantile of . Then a JSCB with coverage probability can be constructed as , , .

Observe that the width of the JSCB is proportional to the weight function . In practice one could simply choose some fixed weight functions such as which yields equal JSCB width at each and . Alternatively, when the sample size is sufficiently large and temporal dependence is weak or moderately strong, we recommend choosing There are two advantages to this data-driven choice of weights. First, the resulting width of the JSCB reflects the standard deviation of which gives direct visual information on the estimation uncertainty at every and . Second, this choice of weight function yields much smaller average width of the JSCB compared to some fixed choices such as ; see our simulations in Section 3 for a finite-sample illustration. On the other hand, has to be estimated in practice. Later in this article, we shall discuss its estimation and also asymptotic robustness of our multiplier bootstrap methodology when the weight function is inconsistently estimated.

To motivate the multiplier bootstrap, denote . For simplicity, we assume that each has the same degree of smoothness, thereby we let each have the same rate of divergence. By elementary calculations and basis expansions, we have

| (3) |

where . Hence if is sufficiently large and is relatively small such that is under-smoothed, i.e., the standard deviation of the estimation (captured by the first term on the right hand side of (3)) dominates the bias asymptotically, Eq.(3) reveals that the maximum deviation of from on is determined by the uniform probabilistic behavior of , where and with the -th column of .

There are two major difficulties in the investigation of uniformly in . Firstly, is typically a moderately high-dimensional time series whose dimensionality diverges slowly with , and is not a tight sequence of stochastic processes on . Consequently, deriving the explicit limiting distribution of the maximum deviation of is a difficult task. Second, the convergence rate of depends on many nuisance parameters such as the smoothness of and , and the diverging rate of the truncation parameters , which are difficult to estimate in practice. To circumvent the aforementioned difficulties, one possibility is to utilize certain bootstrap methods to avoid deriving and estimating the limiting distributions and nuisance parameters explicitly. In this article, we resort to the multiplier/wild/weighted bootstrap to mimic the probabilistic behavior of the process uniformly over . The inference of uniformly over all quantiles and weight functions in can be transformed into investigating the probabilistic behavior of over a large class of moderately high-dimensional convex sets. However, these convex sets have complex geometric structures for which results that are based on approximations on hyper-rectangles and their linear transformations are not directly applicable. As a result, in this article we shall extend the uniform Gaussian approximation and comparison results over all high-dimensional convex sets for sums of independent and -dependent data established in, for instance, [5] and [21] to sums of stationary and short memory time series in order to validate the multiplier bootstrap. These results may be of wider applicability in other moderately high-dimensional time series problems.

To be more specific, we will consider the multiplier bootstrapped sum given a block size : where is a sequence of i.i.d. standard normal random variables which is independent of .We refer to the method for constructing as the “Multiplier Bootstrap”; this approach is built on the ideas of the weighted or wild bootstrap [60] and moving block bootstrap [34]. It convolutes the block sums of the random vectors , with i.i.d. standard normal weights . The key observation here is that, thanks to the short range dependence assumption (c.f. 1 in Section 5.1), sufficiently long block sums of moderately high dimensional vector time series preserve the main temporal dependence structure and consistently estimates the long-run variance matrix of the series. Notice that aligns with the classic lagged window estimators for long-run variance explored by [43]. Indeed, the conditional variance of the proposed multiplier bootstrap closely approximates the covariance structure of the random vector and its Gaussian analogue, as justified by the convex Gaussian comparison result. Armed with the convex Gaussian approximation theory, we validate the use of the multiplier bootstrap as an effective tool to capture the uniform probabilistic behavior of .

In practice, to implement the multiplier bootstrap, we consider the empirical bootstrap statistic denoted by and its detailed construction can be found in Section 2.3. It will be shown in Theorem 3 of Section 5 that under appropriate assumptions,

as the sample size and the bootstrapped sample size diverge to infinity. It further demonstrates that the conditional distribution of approximates the law of uniformly over all quantiles and weight functions in .

2.3 Tuning Parameter Selection and The Implementation Algorithm

In this subsection, we will first discuss the issue of tuning parameter selection for the roughness penalization regression. We have three parameters to choose, that is the auxiliary truncation parameter , the smoothing parameter and the window size . We recommend choosing where can be selected via the cumulative percentage of total variance criterion. Specifically, we choose such that the quantity exceeds a pre-determined high percentage value (e.g., 85% used in the simulations), where is the th eigenvalue of the empirical covariance operator . The rationale is that with the aid of the roughness penalization, can be chosen at a relatively large value to reduce the sieve approximation bias without blowing up the variance of the estimation.

In addition, the generalized cross validation (GCV) method can be used to choose , see for examples [9, 50]. To be more specific, the GCV criterion for the smoothing parameter is defined as where and is the -th element of the vector . Thus one can select over a range by minimizing the above function.

For the window size , we suggest using the minimum volatility method, which was proposed by [47]. Denote the estimated conditional covariance matrix where with the estimated residual . The rationale behind the minimum volatility method is that the estimator becomes stable as a function of when is in an appropriate range. Let the grid of candidate window sizes be . The minimum volatility criterion selects window size such that it minimizes the function , where denotes the standard error

with .

Next, we will describe the detailed steps of the multiplier bootstrap procedure for JSCB construction when the weight function , . Note that in probability under some mild conditions.

-

(a)

Select the window size , such that .

-

(b)

Choose the number of basis expansion for each and choose the smoothing parameter .

-

(c)

Fit an FLM with estimated coefficients where is the sample standard derivation of , and obtain the residuals .

-

(d)

Generate (say 1000) sets of i.i.d. standard normal random variables , . For each , calculate , where with , and have similar definitions to and with and involved replaced by their estimates and .

-

(e)

Estimate the sample standard deviation of , denoted by , where is the -th entry of . Estimate by and obtain for , with .

-

(f)

For a given level , let the -th sample quantile of the sequence be . Then the JSCB of can be constructed as for , .

In the rare case where is close to 0 at some , one can raise to a certain threshold (say, ) while keeping the weight function continuous such that . As we will show in Section 3, the above manipulations do not affect the asymptotic validity of the bootstrap.

If one is interested in constructing JSCB for a group of parameter functions, say , then one just needs to focus on the th, th, , th elements of the bootstrap process , , to conduct simultaneous inference on those parameter functions. The implementation procedure is very similar to the above, and we shall omit the details.

3 Simulation Studies

Throughout this section, we focus on the case where . Three basis functions will be considered, i.e., Fourier bases (Fou.), Legendre polynomial bases (Leg.) and functional principal components (FPC). Due to page constraints, we refer the readers to Section B of the supplemental material for more numerical experiments, including the JSCB construction under the Brownian motion case, comparison with other methods for , simulation studies for and rejection rates of our JSCB for when it is used as a test.

Recall model (11) and restate the basis expansions as

, when . Next, denote , and as an infinite-dimensional tridiagonal matrix with on the diagonal and on the off-diagonal. We investigate the following model:

FMA(1) model. , and the MA coefficient or . The entries of are independent random variables.

The following basis expansion coefficients of and the error process in model (11) are considered:

and . are dependent on . Let be an AR(1) process where are i.i.d. standardized -distributed random variables with degrees of freedom (denoted by ) and set where is the first FPC score of .

When using the FPC basis, we adopt the same settings as above except that the component-wise dependence structure of is adjusted so that becomes a diagonal matrix with all diagonal elements equal to . This guarantees the true FPCs of are .

| Basis | |||||

|---|---|---|---|---|---|

| 1 | Fou. | 0.943(1.46) | 0.936(1.46) | 0.884(1.28) | 0.886(1.29) |

| Leg. | 0.952(2.95) | 0.945(2.86) | 0.907(2.55) | 0.895(2.48) | |

| FPC | 0.960(1.65) | 0.932(1.69) | 0.903(1.45) | 0.886(1.49) | |

| Fou. | 0.936(1.18) | 0.936(1.22) | 0.875(1.07) | 0.879(1.10) | |

| Leg. | 0.947(1.34) | 0.940(1.33) | 0.884(1.21) | 0.885(1.21) | |

| FPC | 0.938(1.37) | 0.924(1.40) | 0.870(1.25) | 0.858(1.27) | |

| Basis | |||||

| 1 | Fou. | 0.957(1.16) | 0.958(1.12) | 0.903(1.01) | 0.914(0.99) |

| Leg. | 0.953(2.20) | 0.951(2.08) | 0.900(1.90) | 0.890(1.81) | |

| FPC | 0.945(1.17) | 0.948(1.19) | 0.893(1.04) | 0.894(1.06) | |

| Fou. | 0.949(0.92) | 0.940(0.94) | 0.883(0.84) | 0.903(0.86) | |

| Leg. | 0.943(0.98) | 0.941(0.97) | 0.887(0.89) | 0.888(0.88) | |

| FPC | 0.943(1.00) | 0.934(1.01) | 0.874(0.90) | 0.871(0.92) | |

In the simulation studies, the bootstrap procedures discussed in Section 2.3 are employed with to find the critical values at levels and . The simulation results are based on 1000 Monte Carlo experiments. Table 1 reports the simulated coverage probabilities and average JSCB widths with aforementioned three types of basis functions and two types of weight functions; i.e., and . For a confidence band of , we compute its average width as according to Step (f) of the multiplier bootstrap procedure in Section 2.3, where represents the total number of equally spaced grids into which the unit interval is discretized. Here, we choose .

From Table 1, we observe reasonably accurate performance of the JSCB for and most of the results for are close to the nominal levels. Armed with the additional simulation results in Section B.1 of the supplemental material, the performances of the JSCB for dependent predictors and errors are similar to those for independent case, which supports our theoretical result that the multiplier bootstrap is robust to dependence between the predictors and errors. Furthermore, we observe from the simulation results that the JSCB is narrower when the weights are selected proportional to the standard deviations of the estimators. We recommend using the data-driven weights when for Fourier and Legendre basis functions under weak dependence, and for all basis functions if . In practice, our procedure is computationally efficient as it involves selecting only two tuning parameters. On a standard laptop computer, for 1000 bootstrap replications and 1000 simulation runs, the computation takes roughly 3.5 mins and 5.9 mins for and 800, respectively.

4 Empirical Illustrations

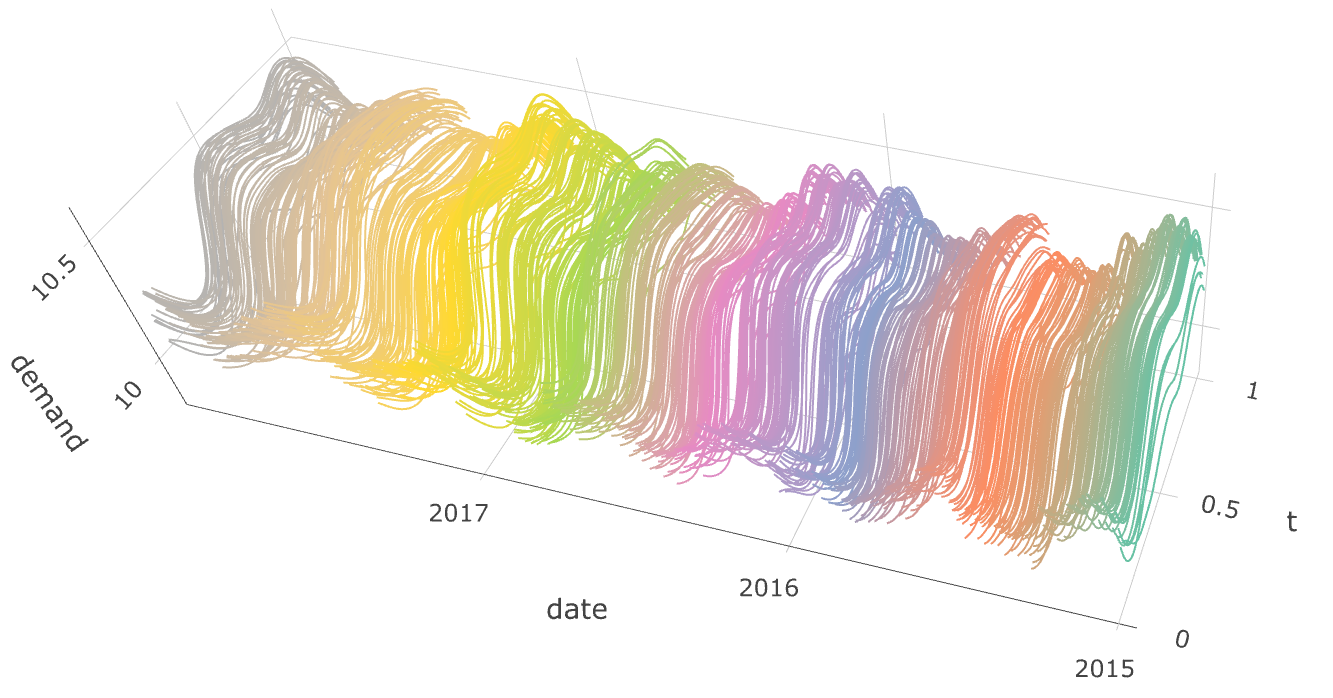

We consider the daily curves of electricity real demands (MWh) in Spain from January 1st 2015 to December 31st 2017. These data can be obtained from Red Eléctrica de Espãna system operator. Since the daily electricity demands on weekdays and weekends differ, in this paper we focus on the weekday curves (from Monday to Friday) with days. The hourly records of electricity demands in year 2011–2012 have been investigated in [1].

The original dataset are recorded by 10-minute intervals from 00:00–23:50 on each day, which consists of 144 observations. We consider the daily log-transformed real demand curves by smoothing and rescaling them to a continuous interval . The plot of the smoothed functional time series is shown in Fig. 1. The stationarity test of [28] is also implemented and it turns out that the test does not reject the stationarity hypothesis at level during the considered period. Next, we aim to investigate the relationship between daily electricity real demand curves and future daily total demands. We explore the FLM:

where stands for the daily electricity demand curve on the -th weekday, and represents the daily total real demands on the -th weekday.

The Legendre polynomial and FPC bases are used in this example. Firstly, we select by cumulative percentage of total variance criterion in Section 2.3, ensuring that at least 95% of the variability in the data is explained. We then set . The block size is chosen as by minimum volatility method in Section 2.3 for aforementioned bases, the smoothing parameter is selected according to the GCV criterion, yielding for the Legendre polynomial bases and for the FPC bases. The JSCBs are constructed in 10000 bootstrap replicates.

We show the plots of JSCBs and point-wise confidence bands for and in Fig. 2. Note that for each time point , the coefficient is asymptotically normal. Therefore, the point-wise confidence bands can be constructed by aggregating all point-wise confidence intervals for each single , where is the -th quantile of . From Fig. 2, both and are significantly non-zero, and is insignificant under the JSCB construction for both bases. In particular, for both bases is significantly positive at the morning and evening peak times, and significantly negative at off-peak time. By contrast, is only significantly positive in the afternoon period and significantly negative in the late evening period, contributing to a slightly weaker impact on the response compared to . On the other hand, while the JSCB of indicates that it is not significantly different from 0, the point-wise confidence bands for based on both bases do not fully cover the horizontal axis , which leads to a spurious significance of . These findings point to a lag 2 FLM where the electricity demands over the previous two weekdays (especially the peak time from the previous weekday) is highly correlated with the total demands of the next weekday. This also indicates that the FLM successfully captures predictive signals in demand curves when forecasting the next-day total demand. Moreover, according to the JSCB fluctuations for the coefficients and , the constant coefficient hypothesis for some finite constant and the linear coefficient hypothesis for some constants are both rejected.

The evaluations of JSCBs and computations of average widths are carried out by 144 discretized data points in a curve. The average widths of SCBs for and are calculated as under Legendre polynomials and under FPC bases, respectively. For the point-wise confidence bands of and , they turn out to be narrower as based on Legendre polynomials and for FPC bases. In contrast, we also implement the confidence band constructions proposed by [31] and [18]. The former method fails to detect any statistically significant coefficient functions and yields average confidence band widths of 5.90 across . For the latter approach, following the authors’ recommended choice of the truncation level , all three coefficient functions are identified as statistically significant. However, this comes at the cost of substantially wider confidence bands. To obtain a more appropriate truncation level for this dataset with a large sample size, we employ our cumulative percentage of total variance method to determine . For this case, only remains statistically significant, the resulting confidence bands remain considerably wider than those produced by our approach, with average widths of 9.82, 8.38, and 4.25 for , respectively.

In line with the AE’s suggestion, we extend our FLM to incorporate weather-related predictors. We consider 2015-2017 daily maximum temperatures in Spain obtained from Agencia Estatal de Meteroloíga and construct the national daily maximum temperature () as a population-weighted average across provinces using population data from Instituto Nacional de Estadística. To capture the nonlinear impact of temperature on the total demand, we introduce indicator variables and representing potential air conditioning and heating effects, respectively. By evaluating the linear association between the total demand and temperature variables across candidate thresholds, we select C and C, corresponding to temperatures at which the use of cooling and heating systems becomes more pronounced. Based on confidence intervals of the coefficients, we find that the temperature predictors are statistically significant at the 5% level. It suggests that temperature variables provides valuable information for forecasting total electricity demand.

To illustrate the prediction performance of the selected FLM in comparison with classic time series prediction methods, we apply a univariate ARIMAX model with exogenous temperature variables to predict total electricity demand on weekdays. The optimal model specification is ARIMAX(6,0,0) according to the AIC criterion.

We compare the out-of-sample forecasts for the last seven days’ total electricity demands for our FLM with temperature covariates and the above-mentioned ARIMAX(6,0,0) model. Our FLM achieves a mean squared prediction error of , an improvement over that of the ARIMAX model which is . These results demonstrate that functional linear regression modeling better captures high-frequency electricity demand patterns than univariate ARIMAX, leading to more accurate predictions in this dataset.

Finally, we perform an additional out-of-sample forecast to examine the prediction intervals. Specifically, we trained the model using the first 767 weekdays (with lag 2 structure and two exogenous temperature predictors) and predicted the total demand for the last 15 weekdays (three weeks) of 2017. The resulting 95% prediction intervals are in Fig. 3. Among all 15 weekdays, only two observations fall outside the 95% prediction interval. Interestingly, both correspond to Mondays. This pattern is consistent with the fact that our model is trained exclusively on weekday dynamics and does not explicitly incorporate weekend effects. Since Monday demand may depend partly on weekend consumption patterns, the reduced accuracy for those days is not unexpected.

5 Theoretical Results

In this section, we first model the functional time series from a basis expansion and nonlinear system [62] point of view, and then investigate the multiplier bootstrap theory.

5.1 Functional Time Series Models

Based on the basis expansion (2), we aim to utilize a general time series model for from a nonlinear system point of view. This will serve as a preliminary for our theoretical investigations.

Definition 1.

Assume that satisfy , , where for a random variable . We say that admits a physical representation if for each fixed and , the stationary time series can be written as where is a measurable function and is the one-sided shift process with being i.i.d. random elements. For , define the -th physical dependence measure for the functional time series with respect to the basis and moment as where is a coupled process with an i.i.d. copy of .

Note that in the above definition, does not depend on . The above formulation of time series can be viewed as a physical system where functions are the underlying data generating mechanisms and are the shocks or innovations that drive the system. Meanwhile, measures the temporal dependence of by quantifying the corresponding changes in the system’s output uniformly across all basis expansion coefficients when the shock of the system steps ahead is changed to an i.i.d. copy. We refer to [62] for more discussions of the physical dependence measures with examples on how to calculate them for a wide range of linear and nonlinear time series models.

Definition 1 is related to the class of functional time series formulated in [67]. The difference is that in (2) we separate the standard deviation from and the functional time series model in [67] is formulated without this extra step. Standardization of the basis expansion coefficients is needed in the fitting of the FLM (11) to avoid near singularity of the design matrix. Furthermore, Definition 1 is also related to the concept of -approximable functional time series introduced in [27], as both formulations utilize the concepts of Bernoulli shifts and coupling. The difference lies in our adaptation of the basis expansion, similar to that in [67], which separates the functional index and time index and hence makes it easier technically to investigate the behavior of various estimators of uniformly over . Now, we impose an assumption on the speed of decay for the dependence measures .

Assumption 1.

There exists some constant such that for some universal constant , the physical dependence measure satisfies

Assumption 1 is a mild short-range dependence assumption which asserts that the temporal dependence of the functional time series decays at a sufficiently fast polynomial rate. For independent functional data, the condition is automatically satisfied as there is no temporal dependence (). In Section D of the online supplemental material, we will provide two examples on how to calculate for a class of functional MA and functional AR(1) processes, respectively.

5.2 Validating The Multiplier Bootstrap

Adopting the nonlinear system point of view [62], we model the stationary error process as for some measurable function . Observe that both and are generated by the same set of shocks and hence they could be statistically dependent. Further define . To establish the main results, we need the following conditions:

Assumption 2.

For some non-negative integers and with , assume that and a.s.. Suppose that , and is some finite constant. Moreover, assume that the random coefficients for .

Assumption 3.

The smallest eigenvalue of is greater or equal to some constant , which does not depend on or .

Assumption 4.

The stationary process satisfies , there exist some constants , and such that its physical dependence measure achieves .

Assumption 5.

for some .

The above conditions are mild and are needed for establishing a Gaussian approximation and comparison theory for roughness-penalized estimators. Let be an integer. It is well-known that for a general function, the fastest decay rate for its -th basis expansion coefficient is for a wide class of basis functions [12]. For instance, the Fourier basis (for periodic functions), the weighted Chebyshev polynomials [56] and the orthogonal wavelets with degree [41] admit the latter decay rate under some additional mild assumptions on the behavior of the function’s -th derivative. Hence Assumption 2 essentially requires that the basis expansion coefficients of and decay at the fastest rate. On the other hand, we remark that the basis expansion coefficients may decay at slower speeds for some orthonormal bases. An example is Legendre polynomials, where the coefficients decay at an speed [58]. For basis functions whose coefficients decay at slower rates, following the proofs of this paper it is obvious that the multiplier bootstrap method for the JSCB construction is still asymptotically valid under the corresponding restrictions on the tuning parameters. However, in this case the estimates of will converge at a slower speed, and the bootstrap approximation may be less accurate. For the sake of brevity, we shall stick to Assumption 2 for our theoretical investigations throughout this paper. 3 ensures positive definiteness of the design matrix in order to avoid multicollinearity. 4 is a short range dependent condition on in accordance with 1. Finally, 5 puts some moment restrictions on the random variable . We refer the readers to Section E.3 for examples and discussion on these assumptions.

Let be a matrix with its element . The following additional assumptions are needed for the validation of the multiplier bootstrap.

Assumption 6.

For , we assume , where is a positive constant depending on the basis function, and is the spectral norm (largest singular value) of a matrix .

Assumption 7.

For each , there exists some constant such that for some positive constant , where denotes the uniform norm of a bounded function, i.e, if then In addition, for any and , there exists a nonnegative constant and some finite constant such that

Assumption 8.

For sufficiently large and , , where is a universal finite constant.

Assumption 6 is mild and can be easily checked for many frequently-used basis functions, such as the Fourier basis and the Legendre polynomial basis . Meanwhile, Assumption 7 is satisfied by most frequently-used sieve bases. For instance, the pair for the trigonometric polynomial series, for the polynomial spline basis functions and for the normalized Legendre polynomial basis. We refer to Section E.3 of the supplemental material for a detailed discussion of the above claims on Assumptions 6 and 7. Assumption 8 is frequently adopted in the FLM literature, for example [23], which imposes a lower bound on the decay rate of . Similar to our discussion of Assumption 2, for functions the fastest decay speed of their basis expansion coefficients is of the order for a wide class of basis functions. Hence Assumption 8 is mild.

Define and the Kolmogorov distance by

Then we have the following theorem on the consistency of the proposed multiplier bootstrap method.

Theorem 1.

Under Assumptions 1–8, the smallest eigenvalue of is bounded below by some constant and . Define where represents the element in the probability space, indicates Frobenius norm, diverges to infinity at an arbitrarily slow rate and is a finite constant. Then . Under the event , we have

where is some finite constant and as . Further suppose the conditions in Section E.1 of the supplemental material hold true, the JSCB achieves

| (4) | ||||

Theorem 3 states that under certain regularity conditions, the JSCB achieves the correct coverage probability asymptotically. In particular, captures the rate of the bootstrap approximation to , including the Gaussian approximation error, multiplier bootstrap approximation error, and estimation error; see Section E.1 of the supplemental material for its detailed representation. The rate is the optimal one that balances the bias and variance of the bootstrapped covariance matrices. Since Theorem C.1 in Section C of the supplemental material and Theorem 3 above are established uniformly over all weight functions in , the JSCB achieves asymptotically correct coverage probability without assuming that is a uniformly consistent estimator of as long as almost surely. Hence the multiplier bootstrap is asymptotically robust to inconsistently estimated weight functions. The price one has to pay for inconsistently estimated weight functions is that the average width of the JSCB may be inflated.

5.3 Data-Driven Basis Functions Based on Functional Principal Components

A popular data-driven orthonormal basis in functional data analysis is the FPC. Observe that FPCs have to be estimated from the data which inevitably causes estimation errors. When one employs data-driven basis functions such as the FPCs to fit model (11), the additional estimation error must be taken into account. Note that are the eigenvalues of the corresponding covariance operator. Throughout this subsection, for any given , we assume that . This assumption implies that the first eigenvalues are separated, which is commonly used in the theoretical investigation for FPC-based methods. The next proposition establishes the asymptotic validity of the bootstrap for the FPC basis functions under some extra condition.

Proposition 5.1.

This proposition imposes an extra constraint (5) on the smoothness of and to make the additional bias term resulting from FPC estimation negligible compared to the standard deviation term.

References

- [1] (2016) Short-term forecast of daily curves of electricity demand and price. Electrical Power & Energy Systems 80, pp. 96–108. Cited by: §4.

- [2] (2017) Functional generalized autoregressive conditional heteroskedasticity. Journal of Time Series Analysis 38 (1), pp. 3–21. Cited by: §1.

- [3] (2012-08-14) On the prediction of stationary functional time series. Journal of the American Statistical Association 110, pp. 378–392. External Links: http://arxiv.org/abs/1208.2892v4 Cited by: §1.

- [4] (2015) Some new asymptotic theory for least squares series: pointwise and uniform results. Journal of Econometrics 186 (2), pp. 345–366. Cited by: §E.3.

- [5] (2003) On the dependence of the Berry–Esseen bound on dimension.. Journal of Statistical Planning and Inference 113 (2), pp. 385–402. Cited by: Appendix C, §E.4, §E.4, §1.1, §2.2.

- [6] (2012) Linear processes in function spaces: theory and applications. Vol. 149, Springer Science & Business Media. Cited by: Appendix A, §1.

- [7] (2012) Minimax and adaptive prediction for functional linear regression. Journal of the American Statistical Association 107 (499), pp. 1201–1216. Cited by: §1.2.

- [8] (2006) Prediction in functional linear regression. The Annals of Statistics 34 (5), pp. 2159–2179. Cited by: §1.2.

- [9] (2003) Spline estimators for the functional linear model. Statistica Sinica 13 (3), pp. 571–591. Cited by: §1.2, §2.3.

- [10] (2011) Functional linear regression. In The Oxford Handbook of Functional Data Analysis, Cited by: §1.1, §1.2.

- [11] (2005) Generalized bootstrap for estimating equations. The Annals of Statistics 33 (1), pp. 414–436. External Links: ISSN 0090-5364, Document Cited by: §1.2.

- [12] (2007) Large sample sieve estimation of semi-nonparametric models. Handbook of Econometrics 6(B), pp. 5549–5632. Cited by: §5.2.

- [13] (2017) Central limit theorems and bootstrap in high dimensions. The Annals of Probability 45 (4), pp. 2309–2352. Cited by: §1.2.

- [14] (2013) Gaussian approximations and multiplier bootstrap for maxima of sums of high–dimensional random vectors. The Annals of Statistics 41 (6), pp. 2786–2819. External Links: ISSN 0090-5364, Document, MathReview Entry Cited by: §1.2.

- [15] (2015) Comparison and anti-concentration bounds for maxima of gaussian random vectors. Probability Theory and Related Fields 162 (1), pp. 47–70. Cited by: §E.5.

- [16] (2009) Smoothing splines estimators for functional linear regression. The Annals of Statistics 37 (1), pp. 35–72. Cited by: §1.2.

- [17] (2020) Testing relevant hypotheses in functional time series via self-normalization. Journal of the Royal Statistical Society: Series B: Statistical Methodology 82, pp. 629–660. Cited by: §1.

- [18] (2024) Statistical inference for function-on-function linear regression. Bernoulli 30 (1), pp. 304–331. Cited by: §B.3, §B.3, §B.3, §1.2, §1.2, §4.

- [19] (2001) Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American Statistical Association 96 (456), pp. 1348–1360. Cited by: §E.2.

- [20] (2015) Rates of convergence for multivariate normal approximation with applications to dense graphs and doubly indexed permutation statistics. Bernoulli 21 (4), pp. 2157–2189. Cited by: Appendix C, Lemma E.1.

- [21] (2016) A multivariate CLT for bounded decomposable random vectors with the best known rate. Journal of Theoretical Probability 29 (4), pp. 1510–1523. Cited by: Appendix C, §E.4, §E.4, §E.4, §E.4, Lemma E.2, §1.1, §2.2.

- [22] (2014) A goodness-of-fit test for the functional linear model with scalar response. Journal of Computational and Graphical Statistics 23 (3), pp. 761–778. Cited by: §1.2.

- [23] (2007) Methodology and convergence rates for functional linear regression. The Annals of Statistics 35 (1), pp. 70–91. Cited by: §E.6, §5.2.

- [24] (2006) Properties of principal component methods for functional and longitudinal data analysis. The Annals of Statistics 34 (3), pp. 1493–1517. Cited by: Appendix A.

- [25] (2013) Minimax adaptive tests for the functional linear model. The Annals of Statistics 41 (2), pp. 838–869. Cited by: §1.2.

- [26] (2015) A note on estimation in Hilbertian linear models. Scandinavian Journal of Statistics 42 (1), pp. 43–62. Cited by: §1.2.

- [27] (2010) Weakly dependent functional data. The Annals of Statistics 38 (3), pp. 1845–1884. Cited by: §1.2, §1, §5.1.

- [28] (2014) Testing stationarity of functional time series. Journal of Econometrics 179 (1), pp. 66–82. Cited by: §4.

- [29] (2012) A test of significance in functional quadratic regression. In Inference for Functional Data with Applications, pp. 225–232. Cited by: §1.2.

- [30] (2012) Inference for functional data with applications. Springer Science & Business Media. Cited by: §1.

- [31] (2019) A simple method to construct confidence bands in functional linear regression. Statistica Sinica 29 (4), pp. 2055–2081. Cited by: §B.3, §B.3, §B.3, §B.3, §1.2, §4.

- [32] (2009) Functional linear regression that’s interpretable. The Annals of Statistics 37 (5A), pp. 2083–2108. Cited by: §1.2.

- [33] (2016) Classical testing in functional linear models. Journal of Nonparametric Statistics 28 (4), pp. 813–838. Cited by: §1.2.

- [34] (2003) Resampling methods for dependent data. New York: Springer. Cited by: §2.2.

- [35] (2014) Adaptive global testing for functional linear models. Journal of the American Statistical Association 109 (506), pp. 624–634. Cited by: §1.2.

- [36] (2007) On rates of convergence in functional linear regression. Journal of Multivariate Analysis 98 (9), pp. 1782–1804. Cited by: §E.2, §1.2.

- [37] (2010) Uniform convergence rates for nonparametric regression and principal component analysis in functional/longitudinal data. The Annals of Statistics 38 (6), pp. 3321–3351. Cited by: §E.6.

- [38] (2009) Strong approximation for a class of stationary processes. Stochastic Processes and their Applications 119 (1), pp. 249–280. Cited by: §E.4.

- [39] (2005) Robust semiparametric M-estimation and the weighted bootstrap. Journal of Multivariate Analysis 96, pp. 190–217. External Links: ISSN 0047-259X, Document Cited by: §1.2.

- [40] (2015) Restricted likelihood ratio tests for linearity in scalar-on-function regression. Statistics and Computing 25 (5), pp. 997–1008. Cited by: §1.2.

- [41] (1992) Ondelettes et operateurs i: ondelettes. Hermann, Paris. Cited by: §5.2.

- [42] (2015) Functional regression. Annual Review of Statistics and Its Application 2, pp. 321–359. Cited by: §1.2.

- [43] (1987) A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica 55 (3), pp. 703–708. External Links: ISSN 00129682, 14680262, Link Cited by: §2.2.

- [44] (1997) Convergence rates and asymptotic normality for series estimators. Journal of Econometrics 79 (1), pp. 147–168. External Links: ISSN 0304-4076, Document Cited by: §E.3.

- [45] (2013) Fourier analysis of stationary time series in function space. The Annals of Statistics 41 (2), pp. 568–603. Cited by: §1.

- [46] (2018) Sieve bootstrap for functional time series. The Annals of Statistics 46 (6B), pp. 3510–3538. Cited by: §1.

- [47] (1999) Subsampling. Springer Science & Business Media. Cited by: §2.3.

- [48] (2005) Functional data analysis. 2nd edition, New York: Springer. Cited by: §2.1.

- [49] (2017) Methods for scalar-on-function regression. International Statistical Review 85 (2), pp. 228–249. Cited by: Appendix A, §1.2.

- [50] (2007) Functional principal component regression and functional partial least squares. Journal of the American Statistical Association 102 (479), pp. 984–996. External Links: ISSN 0162-1459, Document Cited by: §2.3.

- [51] (1992) Perturbation bounds for matrix square roots and pythagorean sums. Linear Algebra and its Applications 174, pp. 215–227. Cited by: §E.5.

- [52] (2014) A survey of functional principal component analysis. AStA Advances in Statistical Analysis 98 (2), pp. 121–142. Cited by: §2.1.

- [53] (2015) Nonparametric inference in generalized functional linear models. The Annals of Statistics 43 (3), pp. 1742–1773. External Links: ISSN 0090-5364, Document Cited by: §E.2, §1.2, §1.2.

- [54] (2015) Bootstrap confidence sets under model misspecification. The Annals of Statistics 43 (6), pp. 2653–2675. External Links: ISSN 0090-5364, Document Cited by: §1.2.

- [55] (2017) Hypothesis testing in functional linear models. Biometrics 73 (2), pp. 551–561. Cited by: §1.2.

- [56] (2008) Is Gauss quadrature better than Clenshaw–Curtis?. SIAM Review 50 (1), pp. 67–87. Cited by: §5.2.

- [57] (2012) User-friendly tail bounds for sums of random matrices. Foundations of computational mathematics 12 (4), pp. 389–434. Cited by: §E.7.

- [58] (2012) On the convergence rates of Legendre approximation. Mathematics of Computation 81 (278), pp. 861–877. Cited by: §5.2.

- [59] (2016) Functional data analysis. Annual Review of Statistics and Its Application 3, pp. 257–295. Cited by: §1.2.

- [60] (1986) Jackknife, bootstrap and other resampling methods in regression analysis. The Annals of Statistics 14 (4), pp. 1261–1295. Cited by: §2.2.

- [61] (2007) Inference of trends in time series. Journal of the Royal Statistical Society: Series B: Statistical Methodology 69 (3), pp. 391–410. Cited by: Appendix A.

- [62] (2005) Nonlinear system theory: another look at dependence. Proceedings of the National Academy of Sciences 102 (40), pp. 14150–14154. Cited by: §E.3, §E.6, §E.7, §5.1, §5.2, §5.

- [63] (2005) Functional data analysis for sparse longitudinal data. Journal of the American Statistical Association 100 (470), pp. 577–590. Cited by: Appendix A.

- [64] (2010) A reproducing kernel hilbert space approach to functional linear regression. The Annals of Statistics 38 (6), pp. 3412–3444. Cited by: §1.2.

- [65] (2007) Statistical inferences for functional data. The Annals of Statistics 35 (3), pp. 1052–1079. Cited by: Appendix A.

- [66] (2018) Gaussian approximation for high dimensional vector under physical dependence. Bernoulli 24 (4A), pp. 2640–2675. Cited by: §E.7.

- [67] (2023-04) Statistical inference for high-dimensional panel functional time series. Journal of the Royal Statistical Society Series B: Statistical Methodology 85 (2), pp. 523–549. External Links: ISSN 1369-7412, Document Cited by: §1.2, §5.1.

- [68] (2013) Heteroscedasticity and autocorrelation robust structural change detection. Journal of the American Statistical Association 108 (502), pp. 726–740. External Links: Document Cited by: §E.7, §E.7.

Supplementary Material of ”Simultaneous Inference for Time Series Functional Linear Regression”

Appendix A Discussion on the Main Article

We now discuss some issues related to the practical implementation of the regression as well as possible extensions. Firstly, the predictors are typically only discretely observed with noises. Hence, pre-smoothing is required to transfer the discretely observed predictors into continuous curves which inevitably produces some smoothing errors. In this article, for the purposes of brevity and to keep the discussion focused, we assume that the smooth curves of are observed. It can be seen from the proofs that the results of the paper hold under the densely observed functional data scenario as long as the smoothing error achieves an order uniformly. Smoothing for time series or densely observed functional data has been intensively investigated in the literature; see for instance [24], [65] and [61], among many others. Though the aforementioned references are not exactly intended for functional time series, their results can be extended to the functional time series setting, which we will pursue in a separate future work. On the other hand, we do not expect that our theory and methodology will directly carry over to the sparsely observed functional data setting [63], and the corresponding investigations are beyond the scope of the current paper.

Secondly, we note that the choice of basis functions is a non-trivial task in practice. In the literature, there are several discussions with respect to the choice of basis functions, or methods for the functional linear regression models in general. See for instance Section 6.1 in [49] and the references therein. Here we shall add some additional notes. For functional time series whose observation curves are clearly periodic, such as the yearly temperature curves, the Fourier basis is a natural choice. Similar choices can be made based on prior knowledge of the shapes of the observation curves in various scenarios. Our limited simulation studies and data analysis in Sections 3 and 4 of the main article suggested many popular classes of basis functions produce similar estimates of the regression curves and comparable inference results, which demonstrates a certain level of robustness towards the basis choices.

Finally, in some real data applications the response time series may be function-valued as well. One prominent example is functional auto-regression [6]. We hope that our multiplier bootstrap methodology as well as the underlying Gaussian approximation and comparison results will shed light on the simultaneous inference problem for FLM with functional responses. We will investigate this direction in a future research endeavor.

Appendix B Additional Simulation Results

In this section we would like to conduct some additional simulation studies that complement those in Section 3 of the main paper. The significance levels are set at and . We choose the sample size as and the bootstrap replications based on 1000 simulation runs throughout this section.

B.1 Simulation Studies for an FAR(1) Model

To measure the effects of temporal dependence, we also conduct a simulation study for an FAR(1) model. First, we consider and denote . The autoregressive model can be constructed as

with , and we choose the AR coefficient or to represent weak to moderately strong dependencies. The entries of are chosen as independent random variables.

Furthermore, the generating mechanism for and error process can be given by

and for . are independent of . Let follow an AR(1) process where is i.i.d. standard normally distributed.

| Basis | |||||||

|---|---|---|---|---|---|---|---|

| 1 | Fou. | 0.945(1.77) | 0.944(1.79) | 0.935(1.72) | 0.898(1.55) | 0.883(1.56) | 0.884(1.51) |

| Leg. | 0.942(3.10) | 0.947(3.16) | 0.940(3.05) | 0.901(2.67) | 0.888(2.72) | 0.877(2.64) | |

| FPC | 0.939(1.91) | 0.941(1.91) | 0.947(1.90) | 0.893(1.67) | 0.889(1.66) | 0.892(1.66) | |

| Fou. | 0.938(1.47) | 0.932(1.47) | 0.923(1.43) | 0.884(1.32) | 0.876(1.32) | 0.864(1.29) | |

| Leg. | 0.934(1.50) | 0.923(1.53) | 0.922(1.56) | 0.883(1.35) | 0.870(1.37) | 0.860(1.40) | |

| FPC | 0.938(1.58) | 0.927(1.57) | 0.923(1.56) | 0.871(1.41) | 0.869(1.41) | 0.851(1.40) | |

| Basis | |||||||

| 1 | Fou. | 0.960(1.25) | 0.944(1.27) | 0.940(1.23) | 0.903(1.10) | 0.896(1.11) | 0.891(1.08) |

| Leg. | 0.959(2.12) | 0.946(2.12) | 0.940(2.14) | 0.908(1.83) | 0.894(1.83) | 0.888(1.85) | |

| FPC | 0.952(1.28) | 0.952(1.30) | 0.955(1.26) | 0.909(1.12) | 0.893(1.14) | 0.914(1.10) | |

| Fou. | 0.947(1.04) | 0.940(1.06) | 0.930(1.02) | 0.890(0.93) | 0.878(0.95) | 0.871(0.91) | |

| Leg. | 0.940(1.02) | 0.944(1.04) | 0.938(1.04) | 0.895(0.91) | 0.886(0.93) | 0.886(0.93) | |

| FPC | 0.942(1.06) | 0.939(1.08) | 0.934(1.04) | 0.889(0.95) | 0.882(0.97) | 0.887(0.93) | |

The simulated coverage probabilities and average widths of the joint simultaneous confidence bands (JSCB) with two types of weight functions are reported in Table 2. It is obvious to find that when and the data-adaptive weights are used, the coverage probabilities are reasonably close to the nominal levels for most cases under weaker dependence (). However, under stronger dependence the performances of the three bases weaken slightly when . The decrease in estimation accuracy and coverage probability in finite samples under stronger temporal dependence is well-known in time series analysis. This decrease seems to be universal across various inferential tools (such as subsampling, block bootstrap, multiplier bootstrap, and self-normalization) though some methods may be less sensitive to stronger dependence. One explanation is that the variances of the estimators tend to be higher under stronger dependence, which leads to less accurate estimators. This reduced accuracy then results in deteriorated coverage probabilities in small to moderately large samples.

B.2 Simulation Studies for Brownian Motions

We consider an additional simulation experiment where the functional predictor is a Brownian motion process. We use three types of basis functions, Fourier bases, shifted Jacobi polynomial bases and functional principal components (FPC). First, we list the following approximation representations for the generation of Brownian motions based on two kinds of basis functions:

Fourier bases:

where are independent and identically distributed (i.i.d.) random variables.

Shifted Jacobi polynomial bases:

where for and all are independent. are orthogonal basis functions constructed by Jacobi polynomial bases as

where is the -Jacobi polynomial defined by

with the original Legendre polynomial defined in Example 5 of Section E.3.

Now, restate the basis expansion when . We consider the following parameter configurations:

and for .

Case (a): are i.i.d. and the error process are i.i.d. with .

Case (b): are i.i.d. across and

follow an AR(1) process , where is i.i.d. with . Furthermore, are independent of .

Similar to the simulation studies in Section 3 of the main paper, the evaluations of the JSCB and computations of the average widths are carried out by discretizing the unit interval into equally spaced grids. Table 3 shows simulated coverage probabilities and average JSCB widths with three types of basis functions based on both constant and data-driven weight functions. From that, one can observe that most of the results, especially for , are close to the nominal levels. Specifically, the average widths of JSCB for are narrower than those for . In summary, we claim that our methodology can be applied to the scenario where the functional data is continuous but non-differentiable everywhere, such as Brownian motion.

| Case (a) | |||||

|---|---|---|---|---|---|

| Basis | |||||

| 1 | Fourier | 0.947(0.99) | 0.946(0.67) | 0.898(0.87) | 0.889(0.59) |

| Jacobi | 0.934(1.66) | 0.934(1.27) | 0.882(1.49) | 0.886(1.14) | |

| FPC | 0.947(0.97) | 0.946(0.66) | 0.895(0.85) | 0.889(0.58) | |

| Std | Fourier | 0.934(0.86) | 0.935(0.58) | 0.870(0.78) | 0.879(0.52) |

| Jacobi | 0.929(1.60) | 0.936(1.22) | 0.880(1.45) | 0.872(1.11) | |

| FPC | 0.934(0.85) | 0.934(0.57) | 0.872(0.76) | 0.879(0.52) | |

| Case (b) | |||||

| Basis | |||||

| 1 | Fourier | 0.934(0.99) | 0.937(0.69) | 0.877(0.87) | 0.889(0.60) |

| Jacobi | 0.936(1.70) | 0.942(1.30) | 0.886(1.52) | 0.880(1.16) | |

| FPC | 0.935(0.97) | 0.937(0.68) | 0.890(0.85) | 0.890(0.60) | |

| Std | Fourier | 0.937(0.86) | 0.938(0.59) | 0.876(0.77) | 0.889(0.53) |

| Jacobi | 0.930(1.62) | 0.942(1.24) | 0.874(1.47) | 0.881(1.13) | |

| FPC | 0.935(0.84) | 0.939(0.59) | 0.876(0.76) | 0.888(0.53) | |

B.3 Numerical Experiments Comparing with Other Methods

In this subsection, we conduct another simulation study, comparing our JSCB construction with the conservative confidence bands proposed by [31] and the confidence bands construction investigated by [18]. Since the methodologies of the latter two papers are limited to i.i.d. data, we will perform three distinct sets of comparison experiment with , including i.i.d. scenario, weak temporal dependent and moderately strong dependent cases. Here, recall the basis expansions as . Consider

and for .

where i.i.d. follow the Uniform distribution as .

Now, we investigate the following cases:

Case (c): Consider the above data generation processes for and , and the error term is i.i.d. .

Case (d): The above data generation processes for and are considered, the error process follows an AR(1) model where is i.i.d. .

Case (e): The generation process for

retains the same of that in Case (d), follows the FAR(1) model in Section 4 of the main paper where the coefficient matrix is diagonal with all diagonal elements being 1 to make sure the true FPCs of are and the autoregressive coefficient . The error process follows the same AR(1) model as described in Case (d).

| Case (c) | |||||

|---|---|---|---|---|---|

| Method | Cutoff level/Weight | ||||

| MCP | 0.985(1.94) | 0.947(1.51) | 0.926(1.68) | 0.862(1.32) | |

| 0.999(2.72) | 1(2.04) | 0.999(2.40) | 1(1.80) | ||

| MCP∗ | 0.917(1.94) | 0.874(1.51) | 0.795(1.69) | 0.820(1.32) | |

| 0.995(2.72) | 1(2.04) | 0.987(2.40) | 1(1.80) | ||

| JSCB | 0.940(2.63) | 0.941(1.88) | 0.887(2.38) | 0.893(1.70) | |

| Case (d) | |||||

| Method | Cutoff level/Weight | ||||

| MCP | 0.985(1.97) | 0.936(1.53) | 0.935(1.62) | 0.844(1.34) | |

| 1(2.75) | 1(2.11) | 1(2.42) | 1(1.86) | ||

| MCP∗ | 0.928(1.87) | 0.858(1.53) | 0.807(1.62) | 0.785(1.34) | |

| 0.995(2.75) | 0.999(2.11) | 0.990(2.42) | 0.993(1.86) | ||

| JSCB | 0.926(2.67) | 0.944(1.92) | 0.871(2.42) | 0.887(1.74) | |

| Case (e) | |||||

| Method | Cutoff level/Weight | ||||

| MCP | 0.896(1.79) | 0.888(1.34) | 0.784(1.56) | 0.884(1.16) | |

| 1(2.90) | 1(2.41) | 1(2.52) | 0.999(2.09) | ||

| MCP∗ | 0.804(1.79) | 0.885(1.34) | 0.712(1.56) | 0.867(1.16) | |

| 0.999(2.90) | 0.999(2.41) | 0.999(2.52) | 0.996(2.09) | ||

| JSCB | 0.930(1.53) | 0.936(1.03) | 0.862(1.37) | 0.879(0.92) | |

In the simulation experiment, we focus on Fourier basis functions and examine the coverage probabilities of confidence bands for sample sizes with replicates. For the conservative confidence bands construction in [31], we choose the significance levels , the other level and preserve two kinds of choices for the cutoff level (i.e. truncation number used in the PCA-based estimation) , denoted by and . To provide further clarity, we evaluate the confidence bands of our method in comparison with methods in [31] using

where is considered in the JSCB construction. The confidence bands in MCP construction are specified as

with representing the simulated conditional -quantile of the corresponding statistic given functional data , where is the estimated FPC score and is the estimated coefficient of . The notation in the equation of MCP denotes the Lebesgue measure.

The simulated coverage probabilities and average widths for JSCB, MCP and MCP∗ are shown in Table 4. For the MCP method proposed in [31], when the cutoff level is chosen as , the coverage probabilities for Cases (c) and (d) exceed the nominal levels for , while most coverage probabilities are below the nominal level for . Furthermore, when the cutoff level is specified as , most of the coverage probabilities under MCP turn out to decrease as the sample size increases, which implies possible instability in simultaneous coverage of this confidence band construction. We note that the observed instability possibly stems from the fact that the MCP method aims at covering the slope function at “most” of the points with a prespecified probability, but is not designed for simultaneous coverage. On the other hand, the simulated coverage probabilities for MCP based on the cutoff level appear to be close to 1 in Cases (c)–(e), at the cost of substantially wider confidence bands.

Note that we also include MCP∗ construction with a stringent requirement. Instead of allowing a small proportion () of the set of points not covered by the confidence bands in MCP construction, MCP∗ method evaluates the coverage probabilities that all discrete points are simultaneously covered by the confidence bands. From Table 4, we observe that for Cases (c)-(d), the MCP∗ method with the cutoff level have narrower average widths than those of our JSCB construction, but at the expense of under coverage probabilities for both and . Furthermore, for Case (e), MCP∗ produces confidence bands with wider widths and coverage probabilities substantially below the nominal level. While with the cutoff level , all coverage probabilities of MCP∗ are close to 1 with wider average widths, yielding a less informative confidence band construction.

In comparison, our JSCB method shows quite accurate coverage probabilities for i.i.d. data, weak and moderately strong dependent data (Cases (c)-(e)). Particularly for Cases (c)-(d), the JSCB construction under the data-driven weights yields narrower average widths than both MCP and MCP∗ methods at the cutoff level . This advantage extends to Case (e), where our JSCB construction achieves narrower widths than competing methods at both cutoff levels. As a result, it demonstrates the better finite sample performance of our JSCB construction especially for dependent functional time series. Again, we remark that MCP and MCP∗ methods in [31] are tailored for i.i.d. functional data, therefore our limited simulation study here merely suggests that their methods cannot be directly extended to the dependent setting.

As a reviewer suggested, we also include a simulation experiment to compare our method with the approach proposed in [18]. Specifically, their work considers a reproducing kernel Hilbert space (RKHS)-based approach for estimating the slope coefficient function by

where is the Sobolev space of order of functions defined on . To implement their bootstrap procedure and construct simultaneous confidence bands for , we similarly follow Algorithm 4.1 in [18] with appropriate modifications for a scalar response linear regression model. The bootstrap weights are generated from a two-point distribution, taking with probability and taking with probability based on bootstrap replications. Then the bootstrap estimator for each can be obtained by

Consequently, the uniform coverage probability can be defined by

and the simultaneous asymptotic confidence band of can be expressed as

where is the empirical -quantile of the sample , and are some tuning parameters.

The following Table 5 reports the simulated coverage probabilities and average widths. For Case (c), the empirical coverage probabilities provide good approximations to the nominal confidence levels for both and , suggesting satisfactory performance of the confidence band construction for independent functional data. For Case (d), the functional covariates are independent, while the responses exhibit weak correlation induced by the temporal dependence in the error process . Under this weak dependent setting, the coverage probabilities remain close to the nominal level for both and . However, in Case (f) which corresponds to a moderately strong dependence data generating structure, the confidence band construction fails to deliver accurate inference even for larger sample size . It is evident that the RKHS-based method produces systematic undercoverage probabilities, indicating its limitation to i.i.d. functional data. On the other hand, the RKHS-based approach yields noticeably wider average widths compared with other methods discussed earlier, which also results in less informative statistical inference.

| Case (c) | 0.937(4.33) | 0.950(3.21) | 0.884(3.78) | 0.895(2.80) |

|---|---|---|---|---|

| Case (d) | 0.947(4.42) | 0.950(3.28) | 0.890(3.86) | 0.898(2.86) |

| Case (e) | 0.855(5.26) | 0.897(3.36) | 0.786(4.59) | 0.826(2.93) |

B.4 Simulation Studies with Order

In the simulation studies of the paper, we only consider the case . In this subsection we shall consider with the following parameter setups:

For , and for ;

For every , consider FMA(1) model where is defined in Section 4 of the paper and the MA coefficient . The random vectors are independent across . The innovation entries of are independent random variables.

The error process are independent and identically distributed (i.i.d.) with standard normal distribution.

| Basis | ||||

|---|---|---|---|---|

| Fou. | 0.935(1.78) | 0.946(1.29) | 0.892(1.59) | 0.897(1.16) |

| Leg. | 0.930(1.72) | 0.946(1.24) | 0.881(1.54) | 0.898(1.11) |

| FPC | 0.932(1.76) | 0.940(1.26) | 0.897(1.57) | 0.878(1.12) |

| Basis | ||||

| Fou. | 0.928(1.95) | 0.942(1.41) | 0.873(1.77) | 0.874(1.36) |

| Leg. | 0.928(1.88) | 0.941(1.36) | 0.853(1.71) | 0.888(1.24) |

| FPC | 0.931(1.92) | 0.935(1.37) | 0.872(1.76) | 0.882(1.25) |

| Basis | ||||

| Fou. | 0.920(2.03) | 0.949(1.48) | 0.859(1.87) | 0.886(1.36) |

| Leg. | 0.923(1.97) | 0.936(1.42) | 0.855(1.81) | 0.873(1.30) |

| FPC | 0.925(2.01) | 0.935(1.43) | 0.859(1.85) | 0.875(1.32) |

We list the simulated results for various orders in Table 6. From it, we find that for all three basis functions, the coverage probabilities for are similar although the coverage probabilities for and tend to be slightly smaller than those of . In particular, all coverage probabilities for and are reasonably close to the nominal levels when .

B.5 Statistical Power of the JSCB Test

Next, we shall perform simulation studies with to investigate the accuracy and power of the JSCB when it is used as a test. Specifically, we shall perform the significance test versus . Consider the following setting under scenario:

and ranges from 0 to with sample size .

where is an infinite-dimensional tridiagonal matrix with on the diagonal and on the off-diagonal, for .

Let the error process follow an AR(1) process where is i.i.d. standard normally distributed. Moreover are independent of .

Fig. 4 shows the simulated rejection probabilities for the test with three types of basis functions at nominal levels . From it, we observe that the power performances of the three basis functions are quite similar with data-driven weight functions in the sense that as increases, the simulated power increases fast. On the other hand, the power curves of the constant weight function increase slower than those of the adaptive weight function. This is consistent with our simulation results that the JSCB is narrower on average when the weights are proportional to the standard deviation of the estimators.

Appendix C Gaussian Approximation Theory

Throughout the supplemental material, we will consistently use the following notation. For a random variable , denote as its norm. For a square integrable random function , we use to stand for its norm. Furthermore, we denote as the spectral norm (largest singular value) for a matrix or the Euclidean norm for a random vector. The notations and indicate the Frobenius norm and Orlicz norm respectively, the notation signifies the largest element of a matrix. We define to state the supremum norm of and the symbol denotes a generic finite constant whose value may vary from place to place.

In this section we shall establish a Gaussian approximation theory for the weighted maximum deviations of uniformly over all quantiles and a wide class of weight functions. As we mentioned in the main article, this result is based on uniform Gaussian approximation results over all Euclidean convex sets for sums of stationary and weakly dependent time series of moderately high dimensions which we will establish in Section E of this supplemental material when we prove the results of this section. The result extends the corresponding findings for independent and -dependent data established in [5], [20] and [21] among others, which may be of separate interest.

Define where is a sequence of -dimensional Gaussian random vectors which is independent of and preserves the covariance structure of . Further denote and define the distance of interest as

Now, we state the Gaussian approximation result for the roughness penalization estimator.

Theorem 2.

Under Assumptions 1–8 of the main article and suppose the smallest eigenvalue of is bounded below by some constant , there exists a constant such that

| (6) |

Proof.

See Section E.4 for the proof. ∎

The above theorem shows that when , and are sufficiently large and is sufficiently small, the distribution of can be well approximated by that of uniformly over all quantiles and weight functions in .

The constraints on and are also mild. For example, if and based on the normalized Legendre polynomial bases, Theorem 3 in Section E.1 shows that is an under-smoothed estimator as long as and . Hence is under-smoothed and at the same time (6) goes to 0 for a relatively wide range of and .

Appendix D Calculating Physical Dependence Measures for Two Classes of Functional Time Series Models

Here, we show two examples on how to calculate for a class of functional MA processes and functional AR(1) processes, respectively.

D.1 FMA Model

Example 1 (Functional MA model).

Let be i.i.d. centered and continuous Gaussian random functions with . For each integer , let where is a positive deterministic sequence with and is a deterministic function such that for all and and some finite constant . Consider the functional MA model,

| (7) |

Let be the covariance function of . Let and the corresponding be the eigenfunctions and eigenvalues of . By the basis expansion method, we can write and . Next, by substituting the above into (7), we obtain

Here is the variance of the random coefficient , where . Let . Then we see that can be written in the form of physical dependence measure in Definition 1 of the paper. The following lemma bounds the physical dependence measures for (7).

Lemma D.1.

The dependence measures for any given if

| (8) |

for sufficiently large and and some positive constant that does not depend on or .

Assumption (8) is a mild condition in general. For instance, it is easy to see that (8) holds if is finitely generated; that is, for each non-negative integer , can only choose from candidate functions for some . Note that functional MA() models belong to the finitely generated category when is finite. For another example, (8) holds if admits the decomposition for some uniformly bounded and continuous functions and . We refer to Lemma D.2 in the following for the proof. We make a further note that another sufficient condition for (8) is that, for some non-negative integer , for sufficiently large and and some positive constant that does not depend on or . For many frequently used basis functions such as the Fourier, wavelet and orthogonal polynomial bases, the decay speed of with respect to is determined by the smoothness of in and is satisfied when there exists a such that is at most as smooth as in for all sufficiently large under some extra mild basis-specific assumptions.

Proof of Lemma D.1. Note that for some finite constant that does not depend on or . Hence inequality (8) holds for all and sufficiently large if it holds for sufficiently large and . Observe that has the following MA representation

where . Therefore a direct application of the definition of the physical dependence measure yields that